Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Wheat Flour

- By Type Analysis

- By Category Analysis

- By Application Analysis

- By End-Use Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

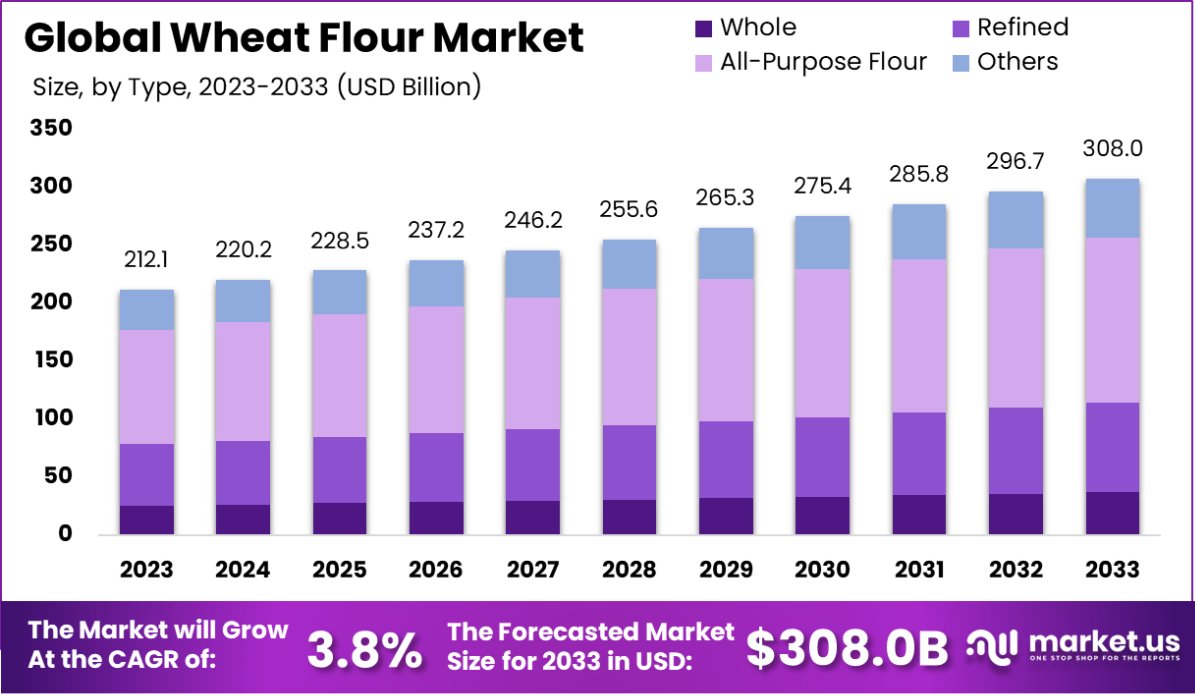

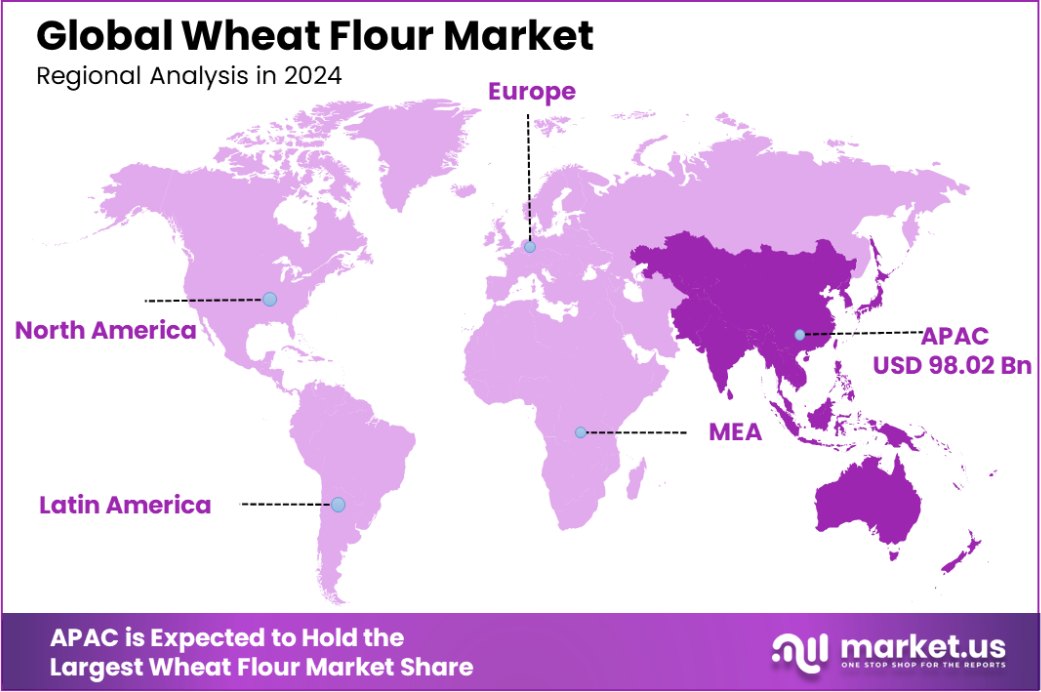

The Global Wheat Flour Market is expected to be worth around USD 308.0 Billion by 2033, up from USD 212.1 Billion in 2023, and grow at a CAGR of 3.8% from 2024 to 2033. Asia-Pacific Wheat Flour Market: 46.7% share, valued at USD 98.02 billion.

The Global Wheat Flour Market is a vital part of the global food industry, driven by its use in diverse culinary applications such as bread, pasta, noodles, and baked goods. Its demand remains steady due to its role in global diets, with innovations in processing broadening its applications in emerging markets.

The market is competitive, and dominated by large-scale milling companies and regional players. Stringent quality standards and government regulations on food safety and fortification influence the industry. Fortified wheat flour, enriched with vitamins and minerals, has gained traction, addressing nutritional deficiencies and supporting public health efforts in many regions.

Key growth drivers include a growing global population and the rising demand for convenience foods like ready-to-eat baked goods and instant noodles. Wheat flour’s affordability and accessibility make it a dietary staple in developing economies, playing a critical role in food security. The FAO reports that over 60% of global wheat production, which exceeded 780 million tons in 2023, is processed into flour.

Emerging trends highlight increasing consumer demand for gluten-free, whole-grain, and organic wheat flour, driven by health and sustainability concerns. Advances in milling technology are improving wheat flour quality, enabling its use in premium products, and catering to evolving consumer preferences.

Future growth is expected from expanding applications in food and non-food sectors, such as bio-based packaging and adhesives. Developing regions like Asia-Pacific and Africa are set to see significant growth due to rising incomes, urbanization, and government initiatives promoting local wheat production.

Per capita consumption of wheat flour varies, with Europe and North America exceeding 70 kilograms annually, while Asia-Pacific sees growing reliance on wheat-based products. The market is poised for steady growth, driven by technological innovations, shifting preferences, and wheat’s continued dietary importance.

Key Takeaways

- The Global Wheat Flour Market is expected to be worth around USD 308.0 Billion by 2033, up from USD 212.1 Billion in 2023, and grow at a CAGR of 3.8% from 2024 to 2033.

- All-purpose flour dominates the wheat flour market, holding a significant 46.4% share by type.

- Conventional wheat flour remains prevalent, accounting for 87.4% of the market by category.

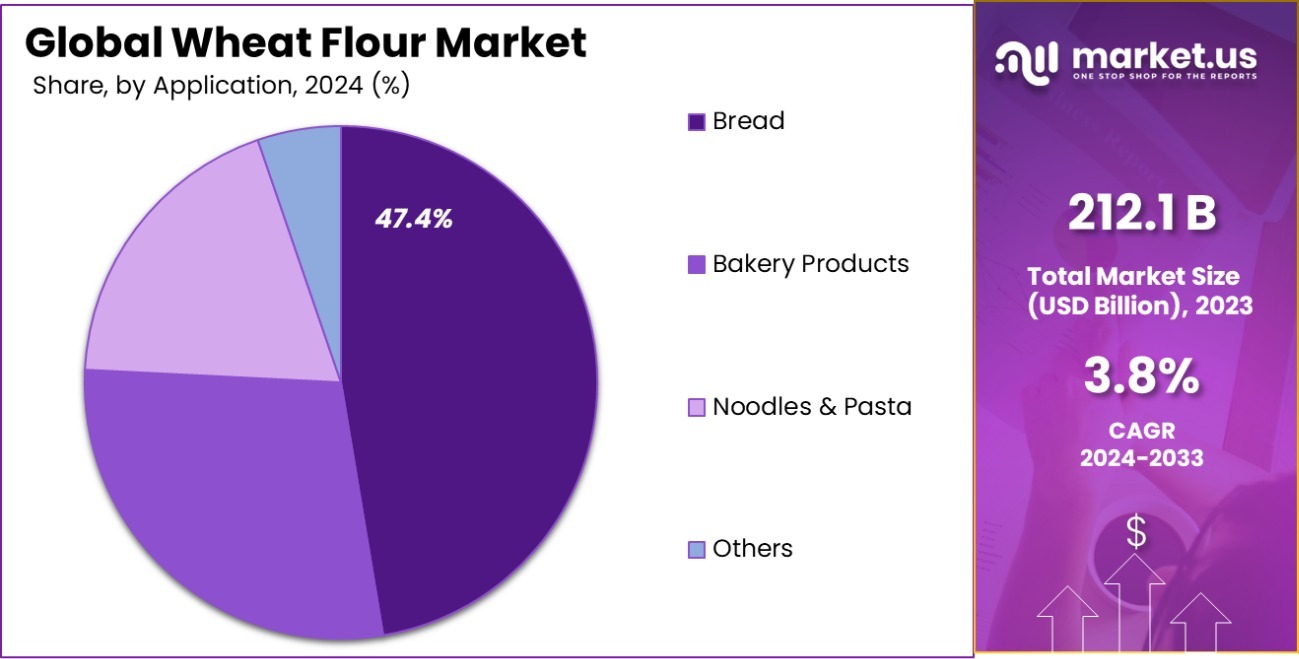

- Bakery products are the primary application of wheat flour, making up 47.4% of its use.

- Food use is the major end-use segment for wheat flour, capturing 87.7% of the market.

- Supermarkets and hypermarkets are the leading distribution channels, representing 53.2% of wheat flour sales.

- The Asia-Pacific Wheat Flour Market holds 46.7%, valued at USD 98.02 billion.

Business Benefits of Wheat Flour

Wheat flour is a cornerstone of the global food industry, offering significant business advantages due to its versatility, nutritional value, and widespread consumer acceptance. In India, wheat is a staple food, particularly in regions like North, West, and Central India, where it is commonly consumed as homemade chapattis or rotis made from whole wheat flour.

The Food Safety and Standards Authority of India (FSSAI) highlights that wheat flour fortification is a cost-effective strategy to combat nutritional deficiencies, enhancing public health by adding essential nutrients such as iron, folic acid, and vitamin B12.

The U.S. Department of Agriculture (USDA) underscores the health benefits of whole grains, including wheat flour, in reducing the risk of chronic diseases. Research indicates that substituting refined grains with whole-grain products can aid in weight management and improve gastrointestinal health.

From a business perspective, the consistent demand for wheat flour-based products like bread, pasta, and pastries ensures a stable market. The USDA’s Economic Research Service notes that consumer preferences have evolved, with an increasing inclination towards whole-grain products, reflecting a growing health consciousness.

Additionally, wheat flour’s adaptability in various culinary applications allows businesses to innovate and diversify their product lines, catering to a broad spectrum of consumer tastes and dietary needs. The USDA’s Agricultural Marketing Service provides detailed industry analyses, emphasizing the economic significance of wheat flour in food production.

By Type Analysis

Wheat flour dominates the market, with all-purpose types holding a 46.4% share in product varieties.

In 2023, All-Purpose Flour held a dominant market position in the “By Type” segment of the Wheat Flour Market, capturing a 46.4% share. This type of flour is favored for its versatility, being suitable for a wide range of baking and cooking applications, from bread and pastries to thickening sauces. Its broad utility makes it a staple in both household and commercial kitchens, driving its substantial market share.

The segment also includes Whole Wheat Flour and Refined Wheat Flour, which have carved out significant portions of the market. Whole Wheat Flour, appreciated for its nutritional benefits, caters to the health-conscious segment of consumers seeking fiber-rich options.

Meanwhile, Refined Wheat Flour, which undergoes a process to remove the bran and germ, is preferred for its finer texture and longer shelf life, making it ideal for baking light, airy baked goods.

These different types of flour cater to diverse consumer preferences and dietary requirements, highlighting the segmented nature of the market. Each type holds its unique appeal and application, influencing consumer choice and market dynamics within the broader Wheat Flour Market.

By Category Analysis

Conventional wheat flour remains prevalent, making up 87.4% of the market by category, favored for its accessibility.

In 2023, Conventional wheat flour held a dominant market position in the “By Category” segment of the Wheat Flour Market, with an 87.4% share. This prevalence is attributed to its widespread availability, cost-effectiveness, and extensive use across various food industries including baking, processed foods, and culinary preparations.

Conventional flour’s dominance is underpinned by established supply chains and the high-volume requirements of food service providers and manufacturers, who rely on its consistent quality and performance.

On the other hand, Organic wheat flour, which accounted for the remaining market share, is gaining traction among health-conscious consumers who prefer products free from pesticides and synthetic fertilizers. Organic flour appeals to a niche but growing segment of the market that values sustainable and environmentally friendly farming practices.

Although it commands a higher price point, the demand for organic flour is expected to grow as consumer awareness increases and organic farming practices become more widespread. This growth is supported by a shift in consumer preferences towards healthier and more sustainable diets, challenging the traditional dominance of conventional flour in the market.

By Application Analysis

Bakery products are the primary application of wheat flour, accounting for 47.4% of its usage in the industry.

In 2023, Bakery Products held a dominant market position in the “By Application” segment of the Wheat Flour Market, with a 47.4% share. This segment includes a broad range of products such as cakes, pastries, cookies, and other confectioneries, which are staple goods in both household and commercial settings.

The prominence of bakery products in the market is driven by their central role in daily diets globally, coupled with the increasing innovation in bakery offerings that cater to evolving consumer tastes and dietary preferences.

Bread, another significant category within this segment, also commands a substantial market share due to its fundamental role as a daily staple in many cultures worldwide. Its versatility and the variety of types available—from whole wheat to multigrain and white bread—ensure its continued popularity.

Additionally, Noodles & Pasta represent a vital and growing segment, fueled by the global popularity of these products and the rising demand for convenience foods. This category benefits from the fast-paced lifestyles of consumers, particularly in urban areas, driving growth through a wide range of product offerings that appeal to diverse palates and dietary requirements.

By End-Use Analysis

Food use is the leading end-use segment for wheat flour, capturing 87.7% of the market focus.

In 2023, Food Use held a dominant market position in the “By End-Use” segment of the Wheat Flour Market, with an 87.7% share. This dominance is largely due to wheat flour’s indispensable role in human nutrition as a primary ingredient in a vast array of food products including bread, pastries, noodles, and other staple carbohydrates.

The vast consumption patterns across global cuisines underline the continuous demand for wheat flour in food production, sustained by both traditional dietary habits and modern food trends.

Feed Use and Bio-Fuel represent smaller but significant segments of the market. Feed Use utilizes wheat flour as a component in animal feed, particularly for livestock, leveraging the nutritional content of lesser-grade flours or byproducts from milling. This segment caters to the agricultural industry’s needs for cost-effective feed solutions.

Bio-Fuel production, though a minor segment, is emerging as an innovative use of wheat flour, particularly in regions focusing on alternative energy sources. This segment exploits the fermentable nature of wheat for bioethanol production, aligning with global sustainability goals and the push for renewable energy resources.

Together, these segments highlight the versatility and widespread applicability of wheat flour beyond traditional food uses, adapting to diverse market demands and technological advancements.

By Distribution Channel Analysis

Supermarkets and hypermarkets are the major distribution channels, delivering 53.2% of wheat flour sales globally.

In 2023, Supermarkets and Hypermarkets held a dominant market position in the “By Distribution Channel” segment of the Wheat Flour Market, with a 53.2% share. This distribution channel’s supremacy is attributed to its ability to offer a wide range of wheat flour products under one roof, catering to diverse consumer needs and preferences.

Supermarkets and hypermarkets provide accessibility and convenience, which are crucial factors for consumers when purchasing staple goods like wheat flour. Their widespread presence and strategic placement in both urban and suburban areas enhance their market reach.

Convenience Stores also play a critical role in the distribution of wheat flour, particularly in regions where consumers seek quick and easy access to food staples. Although they hold a smaller share compared to supermarkets and hypermarkets, their importance grows in densely populated urban areas where larger stores may not be as accessible.

Online Retail Stores represent the fastest-growing segment within this category, driven by the increasing consumer preference for online shopping. The convenience of home delivery and the rising penetration of e-commerce platforms are propelling the growth of this channel. This shift is reshaping the retail landscape, offering potential growth opportunities for wheat flour sales through digital channels.

Key Market Segments

By Type

- Whole

- Refined

- All-Purpose Flour

- Others

By Category

- Organic

- Conventional

By Application

- Bread

- Bakery Products

- Noodles & Pasta

- Others

By End-Use

- Food Use

- Feed Use

- Bio-Fuel

- Others

By Distribution Channels

- Supermarket/Hypermarket

- Convenience Stores

- Online Retail Stores

- Other

Driving Factors

Global Population Growth Fuels Wheat Flour Demand

As the global population continues to expand, the demand for wheat flour escalates correspondingly. Wheat flour is a fundamental component in numerous diets worldwide, providing an essential source of carbohydrates.

This increasing population, particularly in developing countries, drives the need for affordable, versatile food staples, making wheat flour a critical item in daily nutrition and food security. The steady rise in population numbers ensures a sustained demand, underpinning long-term growth in the wheat flour market.

Rise of Convenience Foods Boosts Flour Consumption

The growing global trend towards convenience foods significantly influences wheat flour consumption. With urbanization and the fast-paced lifestyle of modern consumers, there is a rising demand for ready-to-eat and easy-to-prepare fresh food products.

Wheat flour is integral to many such products, including frozen food meals, bakery goods, and instant noodles. This trend not only increases the volume of wheat flour used in food manufacturing but also encourages innovation in flour-based product development to meet consumer expectations for both convenience and taste.

Health and Wellness Trends Shape Market Dynamics

Health and wellness trends are profoundly reshaping consumer preferences, impacting the wheat flour market. Nowadays, more consumers are opting for healthier food choices, which include whole-grain, organic, and gluten-free wheat flour options. This shift is driving manufacturers to diversify their product portfolios to include flours that cater to health-conscious consumers.

Additionally, the demand for fortified wheat flour enriched with vitamins and minerals is climbing, driven by growing awareness of nutritional needs and preventive health care. This factor is prompting innovations and adaptations in the wheat flour industry.

Restraining Factors

Rising Prevalence of Gluten Intolerance and Celiac Disease

The increasing awareness and diagnosis of gluten intolerance and celiac disease significantly restrain the growth of the wheat flour market. As more consumers are advised to avoid gluten for health reasons, the demand for traditional wheat-based products declines.

This shift has prompted many consumers to seek alternative flours and gluten-free products, impacting the sales of conventional wheat flour. Manufacturers are thus challenged to innovate and expand their offerings to include gluten-free alternatives, which can be costlier and less accessible in some markets.

Volatility in Wheat Prices Affects Market Stability

Fluctuations in wheat prices, driven by factors such as climate change, agricultural policies, and global trade dynamics, pose a significant challenge to the wheat flour market. Price volatility can lead to uncertainty in production costs and retail pricing, affecting the entire supply chain from farmers to consumers.

This unpredictability can deter investment in the wheat flour industry and lead to instability in supply, ultimately impacting consumer prices and accessibility of wheat flour products.

Competition from Alternative Flours and Grains

The growing popularity of alternative flour and grains like almond flour, coconut flour, and quinoa represents a major restraint in the wheat flour market. These alternatives are not only appealing to those with gluten sensitivities but also to consumers seeking variety or perceived health benefits from other grain and seed-based flours.

The diversification of consumer preferences challenges the dominance of wheat flour, as manufacturers and retailers broaden their product ranges to include these alternatives, which can dilute the market share of traditional wheat flour.

Growth Opportunity

Expansion into Emerging Markets Promises Robust Growth

Emerging markets present significant growth opportunities for the wheat flour industry. Countries in Asia, Africa, and South America, with growing populations and rising incomes, are increasingly adopting Western dietary patterns that include more wheat-based products.

Tapping into these markets could dramatically increase the demand for wheat flour, providing a considerable boost to global sales. Local production and processing initiatives, supported by government policies aimed at enhancing food security and nutritional quality, can further enhance market penetration and growth in these regions.

Development of Specialized Flour Variants for Health-Conscious Consumers

The trend towards healthier eating habits offers a substantial growth opportunity in the wheat flour market. Developing specialized flour variants, such as high-fiber, fortified, and organic flours, caters to the health-conscious segment of consumers seeking nutritional benefits without compromising on taste or texture.

These specialized products can command higher prices and margins, attracting premium segments of the market. Additionally, aligning product innovations with health trends, like reducing carbohydrate content or enhancing protein levels, can expand the consumer base and increase market share.

Technological Advancements in Flour Processing Technology

Investing in advanced processing technologies represents a crucial growth opportunity in the wheat flour market. Modern milling technologies that improve the efficiency and quality of flour production can lead to better product consistency and open up new applications for wheat flour in both food and non-food sectors.

For example, finer and more uniformly milled flour can enhance the quality of baked goods and pasta. Moreover, technological enhancements that reduce production costs and increase scalability can make wheat flour products more competitive and accessible, driving further market expansion.

Latest Trends

Rising Demand for Gluten-Free and Alternative Wheat Flours

A major trend in the wheat flour market is the increasing consumer demand for gluten-free and alternative wheat flour varieties. As awareness of dietary restrictions and preferences grows, more consumers are seeking out flours that cater to their specific health needs, such as gluten intolerance or celiac disease.

This trend is not only expanding the variety of products available but is also encouraging manufacturers to innovate and refine alternative flour options like those made from ancient grains or non-traditional sources, diversifying the market and catering to a broader audience.

Adoption of Sustainable and Organic Farming Practices

Sustainability has become a key trend in the wheat flour market, with an emphasis on organic and eco-friendly farming practices. Consumers are increasingly prioritizing products that are not only healthy to consume but also beneficial for the environment.

This shift is driving the growth of organic wheat flour, produced without synthetic pesticides or fertilizers. The trend towards organic products is supported by a willingness among consumers to pay a premium for goods that promote ecological balance and offer assurances of natural production methods.

Technological Innovations in Milling and Distribution

Technological advancements in the milling and distribution processes are transforming the wheat flour market. New milling technologies that enhance texture, flavor, and nutritional content are becoming more prevalent, meeting consumer demands for higher-quality products.

Additionally, improvements in logistics and distribution technologies are enabling faster, more efficient supply chains, reducing waste and costs while increasing the freshness of flour products. These innovations are critical in maintaining the competitiveness of wheat flour producers and appealing to a market that values both quality and convenience.

Regional Analysis

In 2023, the Asia-Pacific Wheat Flour Market accounted for 46.7% of the market, valued at USD 98.02 billion.

The Wheat Flour Market is segmented by key regions including North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, each exhibiting unique market dynamics influenced by local consumption patterns, dietary habits, and economic conditions.

Asia-Pacific is the dominating region, holding a 46.7% market share and valued at USD 98.02 billion, driven by large population bases in countries like China and India, where wheat-based products are staple foods. The region’s rapid urbanization and increasing disposable incomes also contribute to the growth of convenient and processed wheat flour products.

In Europe, the market is supported by a preference for premium bakery products and a strong focus on healthy, fortified, and organic flour variants. This region emphasizes sustainable agricultural practices and stringent quality standards, enhancing the demand for high-grade wheat flour.

North America’s market is characterized by high consumption of baked goods and a rising demand for gluten-free and whole wheat options due to growing health consciousness among consumers. This region also shows a significant shift towards sustainable and locally sourced food products.

Middle East & Africa are witnessing growth in the wheat flour market due to economic diversification and the expansion of food service industries. Increasing urbanization and lifestyle changes are driving the demand for wheat-based convenience foods.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global Wheat Flour Market saw substantial activity from key players, each contributing to market dynamics with their strategic initiatives and expansive product portfolios. Ardent Mills, a leader in the North American market, continued to expand its reach and innovate in product offerings, focusing on health-oriented and specialty grains to cater to the evolving consumer demands for nutritious and diverse flour options. Their leadership underscores the trend towards premiumization and specialization in flour products.

Wudeli Flour Mill Group, one of China’s largest flour producers, capitalized on the expanding Asian market. Their strategic focus on volume growth and efficiency has helped them maintain a significant share in one of the fastest-growing regions. Their ability to cater to large-scale domestic needs demonstrates the importance of regional market understanding and scalability in operations.

ADM Company and General Mills are other notable contributors, both enhancing their global supply chains and investing in new technologies to improve flour quality and production efficiency. Their commitment to sustainability and meeting global food safety standards helps them stay competitive in a market that is increasingly driven by consumer preferences for transparency and ethical production.

Emerging players like Bob’s Red Mill Natural Foods and King Arthur Flour Company emphasize organic and non-GMO flour products, tapping into the niche but rapidly growing segment of consumers looking for minimally processed and environmentally friendly options. These companies highlight the shift towards specialty products within the industry.

On the other hand, companies like Cargill Inc. and Bunge Milling continue to leverage their vast networks and resources to optimize production and distribution, ensuring reliability and cost-efficiency in their operations.

Overall, these key players’ strategies in 2023 reflect a blend of regional focus, product innovation, and adaptation to global consumer trends, indicating a robust and dynamic future for the Wheat Flour Market. Each company’s approach to challenges such as supply chain management, sustainability, and changing consumer preferences will significantly influence its positioning and success in the evolving global marketplace.

Top Key Players in the Market

- Ardent Mills

- Wudeli Flour Mill Group

- ADM Company

- General Mills

- Allied Pinnacle Pty Ltd.

- Manildra Milling Pvt. Ltd.

- Acarsan Flour

- Korfez Flour Mill

- George Weston Foods Ltd.

- Hodgson Mills, Inc.

- Bunge Milling

- Cargill Inc.

- King Arthur Flour company

- Bob’s Rede mill Natural Foods

- Conagra Foods Inc

- Ardent Mills Corporate

- J.M. Smucker Company

Recent Developments

- In 2023, Ardent Mills launched innovative products like Egg Replace™ and Ancient Grains Plus™ Baking Flour Blend, focusing on health, sustainability, and consumer trends, reinforcing its market leadership in wheat flour.

- In 2023, ADM Company highlighted its commitment to sustainability by achieving net carbon neutrality across its U.S. flour milling operations and promoting regenerative agricultural practices. Their HarvestEdge® Gold line features sustainably sourced wheat and sorghum flours, aligning with consumer demand for environmentally responsible products.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 212.1 Billion |

| Forecast Revenue (2033) | USD 308.0 Billion |

| CAGR (2024-2033) | 3.8% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Whole, Refined, All-Purpose Flour, Others), By Category (Organic, Conventional), By Application (Bread, Bakery Products, Noodles and Pasta, Others), By End-Use (Food Use, Feed Use, Bio-Fuel, Others), By Distribution Channels (Supermarket and Hypermarket, Convenience Stores, Online Retail Stores, Other) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Ardent Mills, Wudeli Flour Mill Group, ADM Company, General Mills, Allied Pinnacle Pty Ltd., Manildra Milling Pvt. Ltd., Acarsan Flour, Korfez Flour Mill, George Weston Foods Ltd., Hodgson Mills, Inc., Bunge Milling, Cargill Inc., King Arthur Flour company, Bob’s Rede mill Natural Foods, Conagra Foods Inc, Ardent Mills Corporate, J.M. Smucker Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |