Quick Navigation

Report Overview

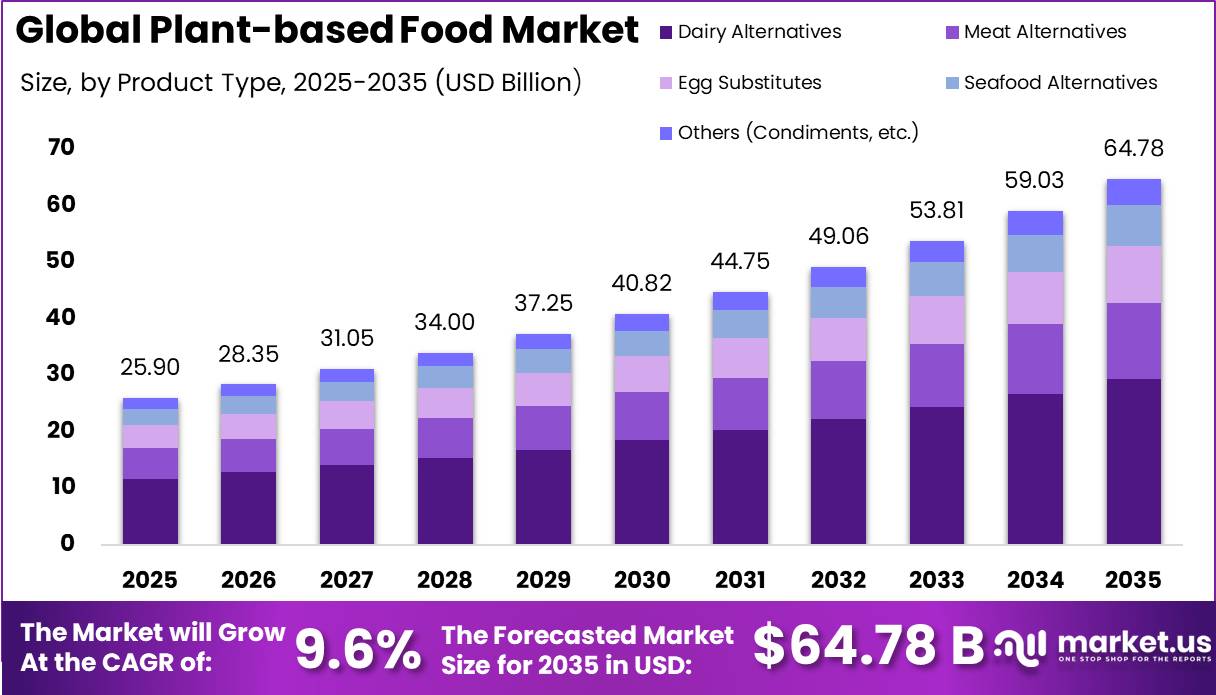

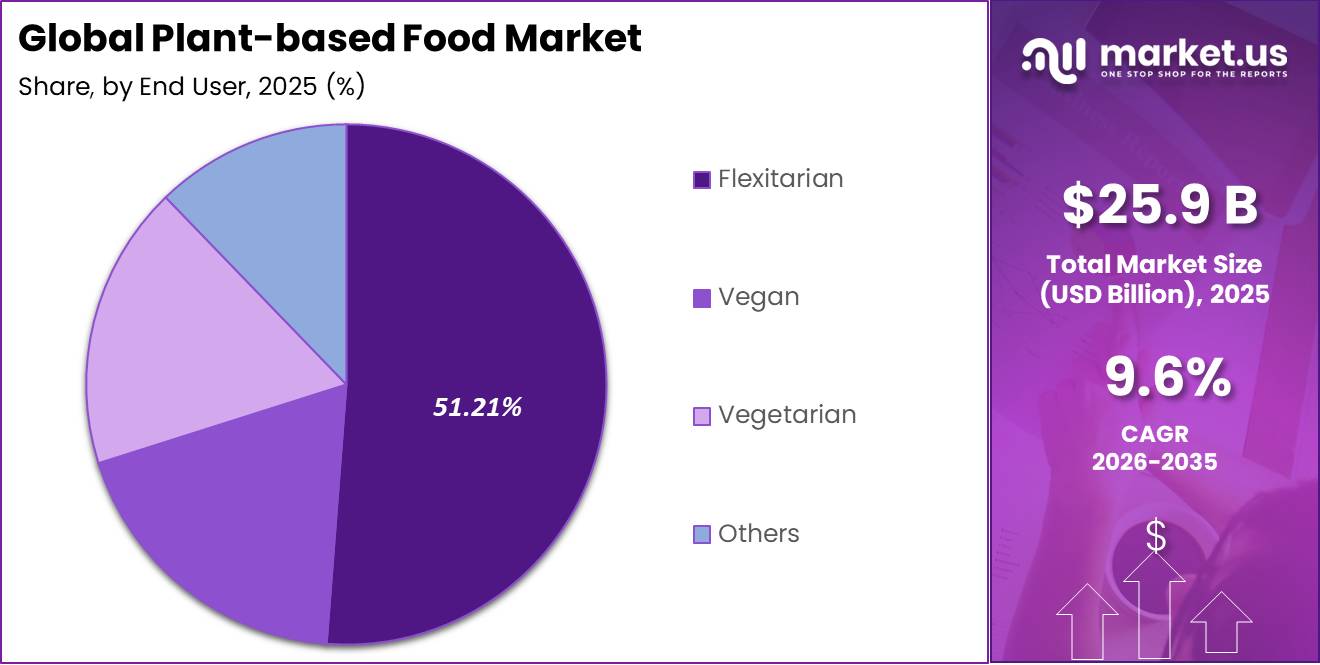

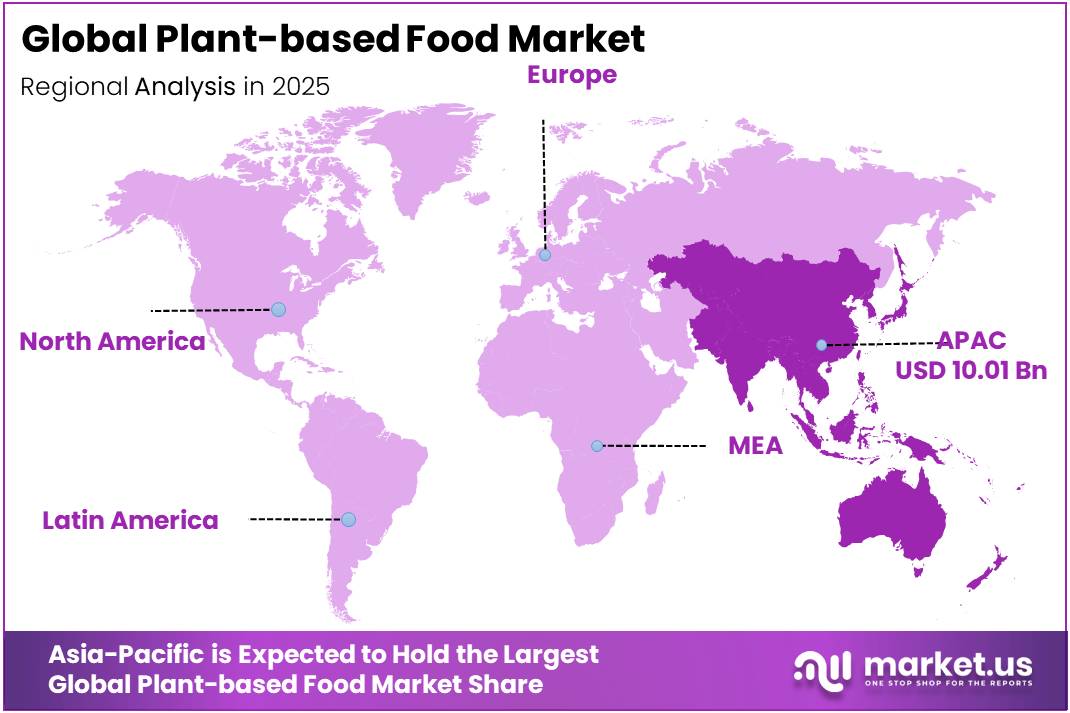

In 2025, the Global Plant-based Food Market was valued at USD 25.9 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 9.6%, reaching about USD 64.78 billion by 2035. In 2025, Asia Pacific led the market, achieving over 38.64% share with a revenue of USD 10.01 billion.

The global plant-based food industry has evolved from a niche health-focused category into a mainstream segment of the food and beverage sector, driven by changing dietary preferences, sustainability priorities, and continuous product innovation. Consumers are increasingly shifting toward foods made from plant-derived proteins, grains, legumes, nuts, seeds, fruits, and vegetables due to growing awareness of nutrition and environmental impacts.

- According to the Food and Agriculture Organization (FAO), global meat production reached approximately 371 million tonnes in 2023, highlighting the scale of conventional protein consumption while also creating opportunities for plant-based alternatives to complement future protein demand.

- The United Nations projects that the global population will reach around 9.7 billion by 2050, increasing pressure on food production systems and encouraging greater adoption of resource-efficient protein sources.

Key Takeaways

- The Global Plant-based Food Market was valued at USD 25.9 billion in 2025.

- The market is projected to grow at a CAGR of 9.6% and is estimated to reach USD 64.78 billion by 2035.

- Dairy Alternatives is the dominant product type, accounting for 45.20% of the market in 2025.

- Soy is the dominant source segment at 32.13%, driven by its established supply chain.

- Supermarkets & Hypermarkets is the dominant distribution channel at 41.20% Share.

- Flexitarian is the dominant end-user segment at 51.21%, Share.

- Asia Pacific holds the largest regional share at 38.64%.

Government agencies and international organizations continue to promote sustainable agriculture and healthier food consumption, indirectly supporting the expansion of plant-based food production. The European Commission’s Farm to Fork Strategy, introduced under the European Green Deal, aims to create a more sustainable food system by encouraging healthier diets, reducing environmental impacts, and expanding sustainable agricultural practices across member states. Food manufacturers are investing in improved protein extraction, precision fermentation, advanced texturization, and ingredient innovation to enhance taste, texture, and nutritional quality.

- The Good Food Institute (GFI) reported that public investments in alternative protein research exceeded US$635 million globally in 2024, demonstrating growing institutional support for next-generation food technologies.

In addition, manufacturers are expanding plant-based dairy, meat, seafood, bakery, snacks, and ready-to-eat product portfolios to meet evolving consumer preferences across retail and foodservice channels. Future growth opportunities remain significant as urbanization, flexitarian eating patterns, and environmental awareness continue to influence purchasing behavior.

- According to the United Nations, 68% of the world’s population is expected to live in urban areas by 2050, increasing demand for convenient, nutritious, and sustainable food products.

Rising investments in novel plant proteins such as pea, fava bean, chickpea, oat, lentil, and mycoprotein ingredients, combined with improvements in supply chain efficiency and food processing technologies, are expected to broaden product accessibility and affordability. Expanding retail distribution, institutional food procurement, and supportive sustainability policies are expected to strengthen long-term industry development while enabling plant-based food manufacturers to address growing global demand for diversified and resilient food systems.

Product Type Analysis

Dairy Alternatives dominate the Plant-based Food Market with 45.20% share due to strong consumer demand for non-dairy beverages and dairy substitutes

In 2025, Dairy Alternatives held a dominant market position, capturing more than a 45.20% share of the global plant-based food market. The segment maintained its leadership because consumers increasingly preferred plant-based milk, yogurt, cheese, cream, and butter as part of everyday diets. Rising lactose intolerance, vegan lifestyles, and demand for products with lower saturated fat continued to support consumption across developed and emerging economies.

- The Food and Agriculture Organization (FAO) states that global milk production exceeded 980 million tonnes in 2024, encouraging food manufacturers to introduce sustainable dairy alternatives alongside conventional dairy products to meet changing consumer preferences.

Meat Alternatives is the fastest growing segment in the global plant-based food market during 2025 and 2026. Growth is being supported by rising consumer awareness of sustainable diets, increasing demand for high-protein foods, and continuous innovation in plant-based burgers, sausages, nuggets, mince, and seafood alternatives.

- According to the Food and Agriculture Organization (FAO), global meat production reached approximately 371 million tonnes in 2023, highlighting the large conventional meat market and the opportunity for plant-based meat alternatives to expand as consumers diversify their protein sources.

Source Analysis

Soy dominates the Plant-based Food Market with 32.13% share owing to its high protein content and broad food applications

In 2025, Soy held a dominant market position, capturing more than a 32.13% share of the global plant-based food market by source. The segment remained the leading raw material because soy offers a complete, high-quality protein profile and is widely used in plant-based milk, tofu, tempeh, meat alternatives, yogurt, and protein ingredients. Its well-established global supply chain, cost efficiency, and strong functional properties make it the preferred choice for food manufacturers.

- According to the United States Department of Agriculture (USDA), global soybean production is projected to reach 426.8 million metric tonnes in the 2025/26 marketing year, ensuring abundant raw material availability for plant-based food manufacturers.

Almond is the fastest growing segment in the global plant-based food market by source during 2025 and 2026. The segment is expanding steadily as consumers increasingly choose almond-based milk, yogurt, creamers, desserts, and snacks for their light taste and nutritional appeal. Manufacturers are also introducing clean-label and fortified almond products to meet growing demand for dairy-free and lactose-free foods.

- According to the United States Department of Agriculture (USDA), California produced approximately 2.8 billion pounds of almonds in the 2025 crop forecast, demonstrating a strong supply base for the global plant-based food industry and supporting continued growth in almond-derived food products.

Distribution Channel Analysis

Supermarkets & Hypermarkets lead the Plant-based Food Market with 41.20% share due to their wide product selection and strong consumer reach

In 2025, Supermarkets & Hypermarkets held a dominant market position, capturing more than a 41.20% share of the global plant-based food market by distribution channel. The segment remained the preferred sales channel because it offers consumers easy access to a broad range of plant-based milk, meat alternatives, snacks, yogurt, cheese, and frozen products under one roof. Large retail chains continue to expand shelf space for plant-based foods, supported by private-label offerings, promotional campaigns, and improved cold-chain infrastructure.

- According to the U.S. Census Bureau, U.S. retail and food services sales reached approximately US$ 8.6 trillion in 2025, reflecting the continued importance of organized retail in food distribution.

Online Retail is the fastest growing segment in the global plant-based food market by distribution channel during 2025 and 2026. Growth is being driven by rising consumer preference for home delivery, wider product availability, subscription-based purchases, and easy access to specialty plant-based brands that may not be available in physical stores. E-commerce platforms also enable manufacturers to introduce new products quickly while offering detailed nutritional information, customer reviews, and personalized recommendations.

End User Analysis

Flexitarian consumers lead the Plant-based Food Market with 51.21% share as balanced eating habits become more common.

In 2025, Flexitarian held a dominant market position, capturing more than a 51.21% share of the global plant-based food market by end user. The segment maintained its leadership as a growing number of consumers chose to reduce, rather than completely eliminate, animal-based foods from their diets. Flexitarian consumers regularly purchase plant-based milk, meat alternatives, yogurt, snacks, and ready-to-eat meals while continuing to consume conventional foods occasionally. This broader consumer base has encouraged food manufacturers and retailers to expand product portfolios across mainstream grocery channels.

- The Dietary Guidelines for Americans 2020–2025, jointly issued by the U.S. Department of Agriculture (USDA) and the U.S. Department of Health and Human Services (HHS), recognize healthy vegetarian dietary patterns as nutritionally adequate, supporting greater acceptance of plant-based eating among flexitarian consumers.

Vegan is the fastest growing segment in the global plant-based food market by end user during 2025 and 2026. Growth is being supported by increasing awareness of environmental sustainability, animal welfare, and the health benefits associated with plant-based diets. Consumers following vegan lifestyles are driving demand for dairy-free beverages, meat alternatives, plant-based cheese, desserts, bakery products, and ready meals. Manufacturers are responding by expanding vegan-certified product ranges, improving ingredient quality, and introducing fortified foods with added protein, calcium, and vitamins.

Key Market Segments

By Product Type

- Dairy Alternatives

- Meat Alternatives

- Egg Substitutes

- Seafood Alternatives

- Others (Condiments, etc.)

By Source

- Soy

- Almond

- Oat

- Pea Protein

- Rice

- Others

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail

- Specialty Stores

- Foodservice / HoReCa

By End User

- Flexitarian

- Vegan

- Vegetarian

- Others

Driver Analysis

Animal-protein price gap widens plant-based value proposition

U.S. food-at-home prices are forecast to rise 2.8% in 2026, but the important signal for plant-based substitution is the uneven inflation inside the basket: beef and veal prices are projected to rise 7.5% in 2026, pork 1.9%, and poultry 1.6%, while eggs are forecast to fall 30.4% after prior volatility.

In practical unit-economics terms, a category facing a 7.5% beef inflation backdrop can absorb promotional investment or hold list prices without widening the consumer “price pain gap” as sharply as in deflationary meat cycles, which supports retail trial, basket retention, and foodservice menu experimentation. This is why the driver is assigned a +1.4 percentage-point CAGR uplift in 2026-forward modeling: it does not guarantee universal demand acceleration, but it improves substitution economics in the highest-frequency protein occasions across North America and parts of Europe where beef remains the reference comparator.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Animal-protein price gap widens plant-based value proposition | +1.4% | North America core, EU, urban APAC spill-over | Short term (≤ 2 years) |

| Sodium/processed-food reformulation pushes cleaner plant-based portfolios | +1.1% | U.S. core, Canada adjacency, EU premium markets | Short term (≤ 2 years) |

| Dry pea and pulse acreage expansion improves protein input economics | +0.9% | North America core, EU sourcing corridors | Medium term (2-4 years) |

| EU policy momentum and institutional food transition de-risk category scale-up | +1.0% | EU core, UK adjacency, Nordic lead markets | Medium term (2-4 years) |

| Private-label and mainstream retail accessibility broaden household penetration | +1.3% | North America core, Western Europe core, developed APAC metros | Short term (≤ 2 years) |

Restraint Analysis

Price premium persistence

The most immediate restraint remains the sector’s inability to close the retail affordability gap fast enough versus conventional protein and dairy, because plant-based brands are absorbing inflation across ingredients, energy, co-manufacturing, freight, and working capital while still operating at lower asset utilization than mainstream food peers; USDA forecasts all food prices up 3.2% in 2026 and food-at-home up 2.8%, while BLS reported final demand producer prices up 6.5% year over year in May 2026 and final demand goods up 2.8% in that month alone, meaning plant-based SKUs with already-thin promotional elasticity face a compounded cost stack that limits everyday-price resets.

In practical terms, a category carrying a 15% to 35% shelf premium versus animal-based substitutes can lose mainstream household conversion when real basket sensitivity rises, forcing deeper trade spending, 200 to 400 basis points of gross-margin compression, and slower new-SKU rollout, which is why this restraint warrants an estimated -1.9 percentage-point drag on 2026-baseline CAGR, especially in North America and Western Europe where repeat purchasing is now more value-tested than novelty-driven.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium persistence | -1.9% | North America core, EU, urban APAC | Short term (≤ 2 years) |

| Labeling compliance friction | -1.2% | U.S., EU, UK-aligned export corridors | Short term (≤ 2 years) |

| Pulse input volatility | -1.0% | U.S., Canada-linked supply, EU import markets | Medium term (2-4 years) |

| Manufacturing under-scale | -1.6% | North America core, EU, ANZ | Medium term (2-4 years) |

| Consumer value skepticism | -1.5% | U.S., Western Europe, developed APAC | Medium term (2-4 years) |

| Novel ingredient approval drag | -0.9% | EU, UK, premium Asia markets | Long term (≥ 4 years) |

Opportunity Analysis

Clean-label local protein systems

This is a future white-space play because the next leg of value in plant-based foods is likely to come less from adding more meat analog SKUs and more from rebuilding formulations around local crop systems, simpler labels, and region-specific sourcing that can improve acceptance, resilience, and margin simultaneously.

In financial terms, companies that redesign portfolios around 2 to 4 high-volume local protein bases could realistically cut imported input exposure by 10% to 20%, reduce formulation complexity by 15% to 30%, and expand gross margin by 200 to 350 basis points through lower freight, fewer specialty additives, and stronger pricing credibility with consumers seeking recognizably sourced foods.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Public procurement conversion | +1.6% | North America core, EU | Short term (≤ 2 years) |

| Clean-label local protein systems | +1.3% | EU, North America core | Medium term (2-4 years) |

| APAC urban convenience formats | +2.1% | APAC emerging markets | Medium term (2-4 years) |

| Healthy aging nutrition platforms | +1.4% | North America core, EU, Japan | Medium term (2-4 years) |

| Ethnic cuisine white-space scaling | +1.2% | North America core, EU | Short term (≤ 2 years) |

| Ingredient-led B2B monetization | +1.8% | Global processing hubs, EU, North America | Long term (≥ 4 years) |

Challenges Analysis

Protein input bottlenecks

The plant-based food sector’s heavy dependence on a narrow band of protein inputs primarily soy, wheat, pea, and fava creates systemic sourcing risk, as 60–70% of current SKUs rely on just three crop complexes whose yields and export flows remain exposed to climate volatility and trade policy shifts. In practice, pea protein concentrate supply into major processing clusters shows year-to-year yield variability of 8–12% and export lead times that can swing from 18–25 days in stable seasons to 30–40 days in peak congestion, with container freight rate volatility still in a ±20–30% band compared with pre-2020 baselines, forcing manufacturers to hold 15–20 extra days of safety stock and accept 2–3 percentage point gross margin compression during tight cycles.

For mid-market brands operating with EBITDA margins of 10–14%, this supply-driven unit cost uplift translates into a realistic drag of around 1.4 percentage points on achievable CAGR, as capacity expansion plans are deferred by 6–12 months and new product rollouts are sequenced more conservatively to avoid stockouts, while procurement teams attempt to diversify into at least 3–4 secondary protein sources per portfolio and negotiate multi-origin contracts across North American, European, and Asian farms.

Strategically, leading companies are responding by investing in upstream contract farming for alternative pulses, building regional protein fractionation capacity with throughput targets of 20–50 kilotonnes per year, and embedding scenario-based supply planning into their S&OP cycles, but achieving stable, diversified input ecosystems will realistically take 2–4 years of coordinated capital deployment, agronomic extension, and updated risk-sharing arrangements with grower networks.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Protein input bottlenecks | -1.4% | North America, EU, APAC export hubs | Medium term (2-4 years) |

| Cold-chain & co-packing strain | -1.2% | Asia-Pacific, Latin America, MENA urban belts | Medium term (2-4 years) |

| Regulatory and labeling ambiguity | -0.9% | EU regulatory hubs, India, Middle East | Long term (≥ 4 years) |

| Sensory and formulation complexity | -1.0% | Global innovation clusters | Long term (≥ 4 years) |

| Skilled talent and R&D gap | -0.8% | North America, Europe, high-growth APAC | Long term (≥ 4 years) |

| Consumer price–value tension | -1.1% | North America core, EU, Emerging Asia | Medium term (2-4 years) |

Geopolitical Impact Analysis

Ongoing Geopolitical Conflicts Are Reshaping Supply Chains and Costs in the Plant-based Food Market

The ongoing geopolitical conflicts, including the Russia–Ukraine war and the conflict in the Middle East, have continued to influence the global plant-based food market in 2025 and 2026. Although plant-based foods are less dependent on livestock production, the industry still relies heavily on globally traded agricultural commodities such as soybeans, peas, sunflower oil, oats, wheat, and almonds. Disruptions in trade routes, higher freight charges, and delays in shipments have increased the cost of sourcing ingredients and packaging materials.

The Black Sea region remains an important supplier of grains and oilseeds, and supply uncertainties have encouraged manufacturers to diversify sourcing and build stronger regional supply networks. Companies are increasingly signing long-term agreements with local suppliers and investing in alternative ingredients to reduce dependence on a single region. At the same time, retailers have adjusted inventory strategies to maintain product availability despite logistical disruptions.

Despite these short-term challenges, consumer demand for plant-based foods has remained resilient. Interest in affordable, sustainable, and protein-rich food options continues to support sales across supermarkets, foodservice, and online channels. Over the longer term, the market is expected to benefit from greater supply chain diversification, increased investment in domestic ingredient production, and continued innovation in plant-based proteins, making the industry more resilient against future geopolitical disruptions.

Regional Analysis

Asia-Pacific dominated the Plant-based Food Market, accounting for 38.64% of the global market in 2025

In 2025, Asia-Pacific held the dominant position in the global plant-based food market, accounting for 38.64% of the total market, equivalent to approximately 10.01 billion in market value. The region’s leadership is supported by its large population, long-established consumption of soy-based foods, and growing demand for healthier and sustainable diets. Countries across the region have a strong tradition of consuming tofu, soy milk, tempeh, and other plant-derived foods, creating a favorable environment for product expansion.

North America is projected to be the fastest-growing regional market during the forecast period. Growth is being driven by increasing consumer preference for clean-label foods, dairy alternatives, and plant-based meat products, along with expanding investments in food technology and product innovation. The region has witnessed strong adoption of flexitarian diets, while major food manufacturers continue to introduce new plant-based products across multiple categories.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global Plant-based Food market exhibits a moderately fragmented competitive structure, with the presence of several multinational food companies alongside numerous regional manufacturers and emerging plant-based brands. No single company holds a dominant global market share, as competition is spread across product categories such as dairy alternatives, meat alternatives, plant-based beverages, snacks, and frozen foods.

Quorn Foods continues to strengthen its position in the plant-based food market through its mycoprotein-based portfolio. The company operates in 20+ countries and offers 100+ plant-based products, including meat alternatives, ready meals, and frozen foods. Alpro, a Danone brand, remains a leading producer of plant-based dairy alternatives across Europe. Its portfolio includes 50+ products covering plant-based drinks, yogurt, desserts, and cream alternatives.

Danone reported €27.4 billion in net sales during 2025, with Alpro contributing to the company’s expanding plant-based nutrition business. Lightlife Foods focuses on plant-based meat alternatives, including burgers, sausages, hot dogs, and tempeh products. The company has more than 45 years of experience in plant-based foods and distributes products through thousands of retail stores across North America.

The Major Players in The Industry

- Beyond Meat

- Impossible Foods

- Oatly Group AB

- Danone S.A.

- Nestlé S.A.

- Quorn Foods

- Alpro (Danone)

- Hain Celestial Group

- Lightlife Foods

- Tofurky Company

- Daiya Foods

- Kite Hill

Key Development

- In April 2026, Nestlé France expanded its Garden Gourmet range with 2 new products, Crousti Dés au Tofu and Nuggets Fromage. Garden Gourmet held nearly 20% of France’s plant-based prepared-food segment and reached more than 2 million consumer households, while its wider product portfolio recorded a repeat-purchase rate above 60%.

- In January 2026, Beyond Meat expanded the distribution of its latest Beyond Burger IV and Beyond Steak products across additional grocery and foodservice channels in North America, targeting wider consumer reach and improving retail availability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 25.9 Bn |

| Forecast Revenue (2035) | USD 64.78 Bn |

| CAGR (2026-2035) | 9.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Dairy Alternatives, Meat Alternatives, Egg Substitutes, Seafood Alternatives, and Others), By Source (Soy, Almond, Oat, Pea Protein, Rice, and Others), By Distribution Channel (Supermarkets & Hypermarkets, Online Retail, Specialty Stores, and Foodservice / HoReCa), By End User (Flexitarian, Vegan, Vegetarian, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Beyond Meat, Impossible Foods, Oatly Group AB, Danone S.A., Nestlé S.A., Quorn Foods, Alpro (Danone), Hain Celestial Group, Lightlife Foods, Tofurky Company, Daiya Foods, Kite Hill |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |