Quick Navigation

Report Overview

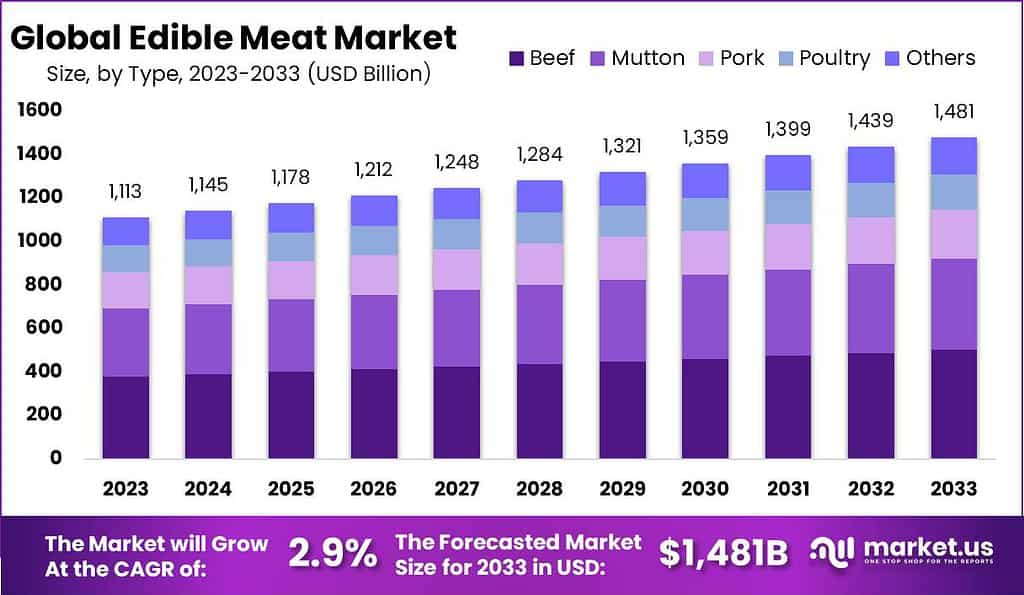

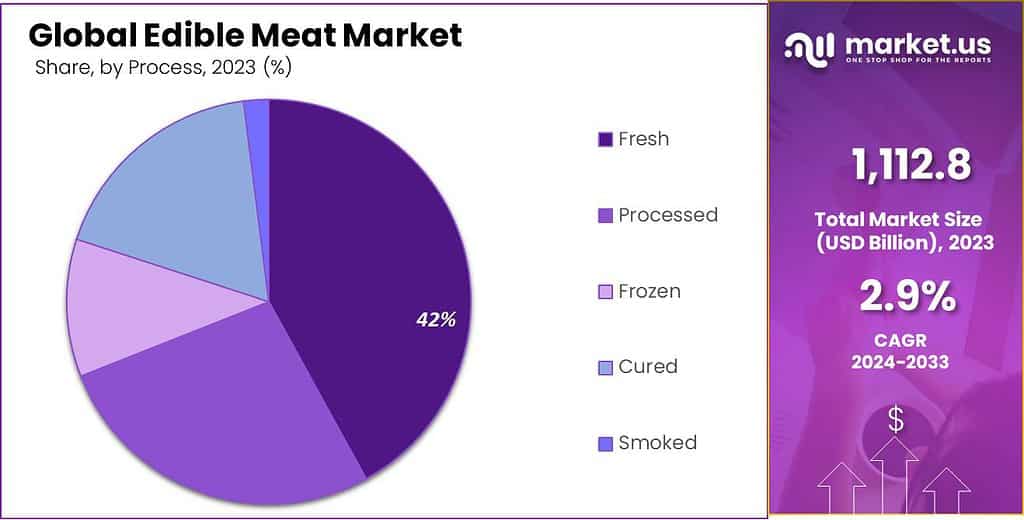

The Global Edible Meat Market is expected to be worth around USD 1481.0 billion by 2033, up from USD 1113 billion in 2023, and grow at a CAGR of 2.9% during the forecast period from 2024 to 2033.

The “Edible Meat Market” refers to the industry that focuses on producing and selling meat that is safe and intended for human consumption. This market includes various meat products derived from animals such as cattle, pigs, poultry, and other livestock that are processed and sold in various forms like fresh, frozen, and packaged meats.

In 2023, the edible meat market has seen substantial demand driven by a combination of factors such as increasing global consumption, evolving consumer preferences, and technological advancements in meat processing.

The United States, in particular, has a significant market value for edible meat, estimated to be around $127.49 billion in 2023, with expectations to grow moderately over the next decade. This growth is underpinned by a variety of meat options available to consumers, ranging from fresh and processed meats to more niche categories like cured and smoked meats.

Globally, the demand for beef, especially in high-income countries like the United States, remains strong despite rising prices. In 2023, retail beef prices have continued to rise, a trend driven by both high demand and limited supply due to factors such as drought affecting livestock numbers. In North America, the market has been further influenced by a resilient consumer spending pattern, even as economic factors like inflation affect consumer budgets.

The trends in consumer preferences also show a shift towards high-quality, convenient meat products, reflecting broader trends in urbanization and busy lifestyles. This shift is part of what continues to drive growth in the edible meat market, with opportunities for market players to innovate and cater to these evolving needs.

Government initiatives also played a critical role in supporting the sector. Stringent regulations concerning food safety and animal welfare significantly influence market dynamics.

For instance, the United States Department of Agriculture (USDA) enforces rigorous inspection and quality control standards, which affect both domestic production and imports. The European Union has similar stringent regulations, which include the Farm to Fork Strategy aiming at sustainable food systems.

In 2023, Brazil was the largest exporter of beef, exporting over 2 million metric tons, followed closely by Australia and the United States. On the import side, China leads, with imports surpassing 2.5 million metric tons in 2023, driven by domestic demand outpacing supply.

Investments in the meat industry are robust, with significant funding directed towards enhancing meat processing technologies. For example, in 2023, the U.S. government allocated $500 million to support meat processing facilities, aiming to improve supply chain efficiencies.

Innovation in meat production, including lab-grown meat and plant-based alternatives, is reshaping the market. In 2023, over $1 billion was invested globally in alternative meat development. Major acquisitions also shape the market landscape; for instance, JBS acquired a plant-based meat company for $341 million in 2023, signaling a strategic diversification.

Various national initiatives support the meat industry’s growth and sustainability. For instance, the Canadian Agricultural Partnership, a $3 billion investment by federal, provincial, and territorial governments, supports the meat sector among others, focusing on competitiveness and sustainability.

Key Takeaways

- The Global Edible Meat Market is expected to be worth around USD 1481.0 billion by 2033, up from USD 1113 billion in 2023, and grow at a CAGR of 2.9% during the forecast period from 2024 to 2033.

- Beef dominated the Edible Meat Market with a substantial 33.4% share.

- Fresh/Chilled led the Edible Meat Market forms with a dominant 37.4% share.

- Fresh meat dominated the Edible Meat Market’s process segment with a 42.4% share.

- Commercial sources led the Edible Meat Market by source with a 51.3% share.

- Supermarkets and Hypermarkets led meat distribution with a dominant 53.4% market share.

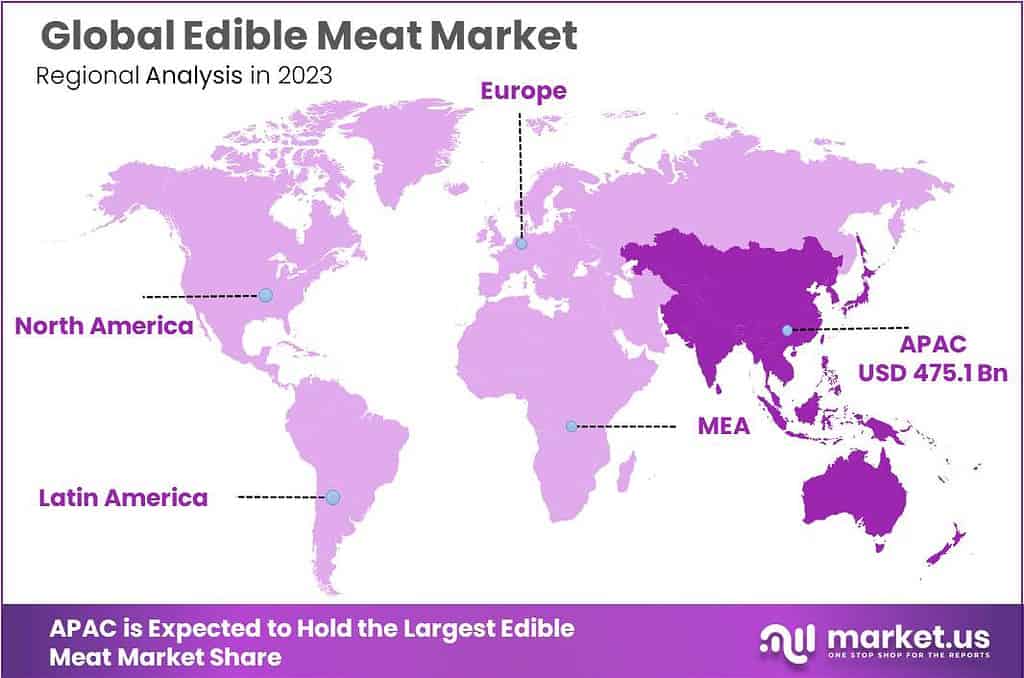

- APAC dominates the global Edible Meat Market with a 39.6% share, totaling $475.1 billion.

By Type Analysis

Beef dominated the Edible Meat Market with a substantial 33.4% share.

In 2023, Beef held a dominant market position in the By Type segment of the Edible Meat Market, capturing more than a 33.4% share. This substantial market share can be attributed to beef’s strong demand across various cuisines and its perceived value as a high-quality source of protein. Consumers’ preference for beef, especially in regions with a strong tradition of beef consumption such as North America and parts of Europe, underpins its leading position.

Following beef, poultry secured the second-largest share, driven by its affordability, versatility, and lower health risks compared to red meats. Poultry’s appeal is also enhanced by its lower environmental footprint, which aligns with the growing consumer trend towards more sustainable eating practices. The ease of poultry farming and its rapid growth rate contribute to its substantial market presence.

Pork ranks third in the market share within the Edible Meat Market. It is particularly favored in Asia, which is the largest consumer and producer of pork globally. Cultural preferences and the integration of pork into traditional dishes support its strong market performance.

Mutton, though smaller in market share compared to beef, pork, and poultry, maintains a significant presence, especially in the Middle East and Asia. Its consumption is often linked to cultural practices and festivities, which sustain its demand.

By Form Analysis

Fresh/Chilled led the Edible Meat Market forms with a dominant 37.4% share.

In 2023, Fresh/Chilled held a dominant market position in the By Form segment of the Edible Meat Market, capturing more than a 37.4% share. This preference for fresh or chilled meats is largely driven by consumer perceptions of better taste and higher nutritional value compared to other forms. The demand is particularly strong in markets where there is a high value placed on fresh produce, and among consumers who prioritize cooking with fresh ingredients.

Frozen meats secured the second largest share, favored for their convenience and longer shelf life. This form appeals especially to consumers looking to manage household budgets more effectively by reducing food waste, as well as to those in regions where access to fresh meat is limited by logistics.

Processed meats, while convenient, ranked third due to growing health consciousness among consumers, who are increasingly wary of additives and preservatives often found in these products. Nevertheless, their ease of preparation and variety maintain a steady demand.

Canned meats, although holding the smallest share, remain relevant in emergency preparedness kits and among specific demographics who prioritize shelf-stable foods. Their long shelf life and affordability make them a viable option for many, despite a general preference for fresher alternatives. Each form caters to distinct market needs, reflecting diverse consumer preferences and lifestyles.

By Process Analysis

Fresh meat dominated the Edible Meat Market’s process segment with a 42.4% share.

In 2023, Fresh meat held a dominant market position in the By Process segment of the Edible Meat Market, capturing more than a 42.4% share. This segment’s leadership stems from the growing consumer demand for products perceived as natural and healthier. Fresh meat is often chosen for its purity, lack of additives, and its versatility in various culinary applications, making it highly sought after in both retail and culinary industries.

Processed meats followed, with a significant portion of the market, appealing to consumers for their convenience and extended shelf life. These meats include a range of products from sausages to deli slices, catering to fast-paced lifestyles where ease of meal preparation is crucial. However, health concerns over preservatives and high sodium content are influencing some consumers to shift towards fresher alternatives.

Frozen meats ranked third, valued for their practicality and cost-effectiveness. Freezing technology preserves meat quality while extending shelf life, making it a popular choice in logistical operations to manage supply chains more effectively, particularly in areas distant from production facilities.

Cured meats, known for their unique flavors and preservation methods, capture a niche market focused on traditional eating experiences. These products, including hams and salamis, are particularly popular in regions with a strong heritage of meat curing.

Lastly, Smoked meats round out the market segments. This category offers distinctive taste profiles and is prized in both gourmet cooking and casual dining. The appeal of smoked meats lies in their rich flavors and the artisanal methods by which they are prepared, resonating with consumers seeking authentic culinary experiences. Each of these processing types caters to specific consumer preferences, lifestyle needs, and culinary traditions, reflecting a diverse and dynamic market landscape.

By Source Analysis

Commercial sources led the Edible Meat Market by source with a 51.3% share.

In 2023, Commercial sources held a dominant market position in the By Source segment of the Edible Meat Market, capturing more than a 51.3% share. This segment’s strength is driven by the scale and efficiency of commercial meat production, which allows for consistent quality and volume, catering to global demand. The commercial meat industry benefits from advanced technologies and processes that optimize everything from feed efficiency to distribution, making it the backbone of meat supply chains worldwide.

Artisanal meats, while smaller in market share, cater to a growing niche of consumers seeking traditional flavors and methods of meat production. These meats are often associated with higher quality and ethical standards, appealing to those willing to pay a premium for craftsmanship and sustainability.

Organic meats have also carved out significant market space, driven by consumers’ increasing health consciousness and environmental concerns. Organic certification implies adherence to strict guidelines regarding animal welfare, feed, and medication, attracting a segment of the market that prioritizes these factors.

Local sources are similarly gaining traction, particularly among consumers interested in supporting local economies and reducing the carbon footprint associated with long-distance meat transportation. This trend towards localism emphasizes freshness and community engagement.

Finally, Wild-Caught meats, although the smallest segment, attract specific consumer demographics who prefer wild game for its perceived naturalness and flavor. This type of meat is less common but highly valued in certain culinary circles for its unique qualities.

By Distribution Channel Analysis

Supermarkets and Hypermarkets led meat distribution with a dominant 53.4% market share.

In 2023, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Edible Meat Market, capturing more than a 53.4% share. This channel’s dominance is attributed to its ability to offer a wide range of meat products under one roof, coupled with the convenience of one-stop shopping for consumers. Supermarkets and hypermarkets also benefit from robust supply chain efficiencies that ensure fresh meat availability, which is a critical factor in consumer choice.

Online Channels have seen a significant rise in popularity. Driven by the convenience of home delivery and the increasing penetration of internet services, online meat shopping is becoming increasingly popular, especially among the younger, tech-savvy demographic. This channel is expected to grow further as e-commerce platforms enhance their logistics and refrigeration capabilities to handle perishable goods effectively.

Convenience Stores also hold a significant share, offering quick access to a limited range of meat products for immediate consumption or last-minute purchases. Their presence in numerous locations makes them an accessible option for many consumers.

Key Market Segments

By Type

- Beef

- Mutton

- Pork

- Poultry

- Others

By Form

- Canned

- Fresh/Chilled

- Frozen

- Processed

By Process

- Fresh

- Processed

- Frozen

- Cured

- Smoked

By Source

- Commercial

- Artisanal

- Organic

- Local

- Wild-Caught

By Distribution Channel

- Convenience Stores

- Online Channel

- Supermarkets and Hypermarkets

- Others

Driving factors

Shifts in Dietary Preferences Towards Protein-Rich Diets

The growth of the edible meat market can be attributed to significant shifts in dietary preferences towards protein-rich diets. As health awareness increases, consumers are actively seeking out protein sources to enhance their nutritional intake, which directly benefits the meat industry. For instance, in developed countries, the trend toward high-protein diets has led to an increased consumption of poultry, beef, and pork.

This dietary shift is not only propelled by individual health consciousness but also by a broader fitness trend that emphasizes muscle building and weight management. As per industry reports, the demand for meat protein has seen a consistent rise, with projections indicating a further increase in market size driven by this sustained interest in high-protein diets.

Integration of Meat in Cultural and Traditional Cuisines

The integration of meat into cultural and traditional cuisines stands as a fundamental factor in the sustained demand and growth of the edible meat market. Globally, meat plays a pivotal role in culinary traditions and festivities, cementing its demand across various regions. In many cultures, meat dishes are integral to celebrations and family gatherings, enhancing market stability and growth.

For example, in Asia, the demand for pork in traditional dishes and during festivals like the Lunar New Year ensures a consistent market. Similarly, in Western countries, turkey and ham consumption spikes during holiday seasons such as Thanksgiving and Christmas. This cultural significance not only maintains a steady demand but also opens avenues for market expansion through the introduction of varied meat-based products tailored to regional tastes and traditions.

Urbanization and Rising Income Levels

Urbanization and rising income levels contribute significantly to the growth of the edible meat market. As urban populations increase, there is a notable shift in lifestyle and consumption patterns, particularly in developing regions. Urban residents tend to have higher disposable incomes, which enables them to afford diverse and high-quality diets, including various types of meats. This economic capability is complemented by urban living standards that often prioritize convenience, leading to greater consumption of processed and ready-to-eat meat products.

For instance, the proliferation of quick-service restaurants and fast food chains in urban areas boosts meat consumption through accessible and appealing meat-based menu options. Furthermore, income growth is not merely a driver but also a facilitator of increased meat production and innovation in meat processing technologies, thereby enhancing the overall market dynamics.

Restraining Factors

Rising Veganism and Vegetarianism

The proliferation of veganism and vegetarianism presents a significant challenge to the growth of the edible meat market. These dietary shifts are primarily driven by health, ethical, and environmental concerns. Surveys indicate that a substantial portion of the population in regions like North America and Europe is adopting plant-based diets, with the global vegan food market expected to grow substantially within the next decade.

This trend directly impacts meat demand, as consumers increasingly opt for alternatives like plant proteins. While this poses a constraint, it also spurs innovation in the meat industry, leading to the development of meat substitutes and blended products that cater to flexitarians who wish to reduce but not eliminate meat consumption.

Health Concerns Over Meat Consumption

Health concerns associated with meat consumption, particularly red and processed meats, act as another restraining factor for the market’s growth. Scientific studies and health organizations have linked excessive meat consumption to various health issues, including heart disease, cancer, and high cholesterol. These health risks have been widely publicized, leading to a cautious approach towards meat consumption among health-conscious consumers.

As a result, there is an observed shift towards leaner meats and the moderation of meat portions in meals. This evolving consumer behavior necessitates adjustments in the meat industry’s strategies, focusing on quality and health benefits rather than just volume sales.

Environmental Impact and Sustainability Issues

Environmental impact and sustainability concerns related to meat production such as high water usage, deforestation, and greenhouse gas emissions further complicate the market dynamics. The environmental footprint of meat production has led to critical scrutiny and regulatory pressures, pushing the industry towards more sustainable practices.

The demand for sustainable meat options is growing, especially among younger consumers who prioritize environmental impacts in their purchasing decisions. This has prompted meat producers to invest in sustainable farming techniques, reduce their carbon footprints, and explore alternative proteins that offer a lower environmental impact.

Growth Opportunity

Innovations in Meat Substitutes and Blended Products

As consumer preferences evolve, the opportunity for growth through innovations in meat substitutes and blended products is significant. By integrating plant-based ingredients with traditional meat products, the industry can cater to a broader audience that includes flexitarians, vegetarians, and those seeking healthier dietary options.

The development of these innovative products not only helps in maintaining market relevance amidst rising veganism but also addresses health concerns linked to meat consumption. This strategy will likely bolster consumer acceptance and market expansion, particularly in developed markets where health consciousness is more pronounced.

Targeting Emerging Economies with High Growth Potential

Emerging economies represent a substantial growth avenue for the edible meat market. Countries with rapidly growing populations and rising income levels, such as India, China, and Brazil, offer significant opportunities for meat product expansion.

As urbanization accelerates and disposable incomes increase, the demand for diverse and premium meat products is expected to surge. Targeting these markets with culturally tailored and economically priced products can provide a lucrative growth pathway for global meat producers.

Leveraging Online and E-commerce Platforms

The expansion of online and e-commerce platforms presents a valuable growth opportunity for the edible meat market. The ongoing shift towards online shopping, accelerated by the COVID-19 pandemic, has opened new avenues for reaching consumers directly.

By enhancing online presence and optimizing e-commerce strategies, meat producers can improve market penetration and consumer reach. This approach not only facilitates easier access to various markets but also aligns with contemporary shopping behaviors, offering convenience and variety to consumers.

Latest Trends

Traceability and Transparency in the Supply Chain

In 2024, the trend towards traceability and transparency in the meat supply chain will be a critical focus. Consumers are increasingly demanding detailed information about the origin, processing, and handling of their food products. This trend is driven by growing health concerns and ethical considerations, prompting meat producers to invest in technologies such as blockchain and IoT to ensure comprehensive traceability. By enhancing transparency, companies not only build consumer trust but also streamline operations and manage risks more effectively, contributing to overall market stability and growth.

Growth of Meat Snacks and Convenience Foods

The edible meat market is also seeing a robust increase in the demand for meat snacks and convenience foods. Busy lifestyles and changing consumer behaviors have led to a surge in demand for ready-to-eat and easy-to-prepare meat products.

Meat snacks, in particular, are gaining popularity due to their convenience and high protein content, appealing to health-conscious consumers looking for quick nutritional options. This trend is expected to drive innovation in product offerings, with companies expanding their portfolios to include a variety of meat-based snacks that cater to on-the-go consumption.

Increased Focus on Protein Alternatives in Diet Plans

Another significant trend is the increased inclusion of protein alternatives in diet plans. As dietary preferences shift towards sustainability and health, more consumers are incorporating plant-based and alternative proteins alongside traditional meat products. This does not necessarily detract from meat consumption but diversifies the protein sources consumers rely on.

Meat industry players can capitalize on this trend by offering hybrid products that blend meat with plant-based proteins, catering to the palate of consumers seeking variety and nutritional balance in their diets.

Regional Analysis

APAC dominates the global Edible Meat Market with a 39.6% share, totaling $475.1 billion.

In the Edible Meat Market, regional dynamics significantly influence market trends and consumer behaviors. Asia Pacific (APAC) dominates the global landscape, holding a 39.6% market share with revenues reaching $475.1 billion. This region’s leading position is driven by its vast population, rapid urbanization, and increasing income levels, which collectively enhance meat consumption across diverse culinary traditions. China and India, in particular, are pivotal markets, given their large populations and growing middle-class consumer bases.

North America, also a significant player, exhibits a mature market characterized by high meat consumption per capita and a robust demand for diverse meat types, including beef, poultry, and pork. The region’s market is propelled by advanced processing technologies and strong distribution channels, enhancing product availability and variety.

Europe’s market is influenced by a strong preference for quality and sustainability, with significant demand for organic and locally sourced meats. The region also faces stringent regulatory environments that push for higher welfare standards in meat production.

The Middle East and Africa (MEA) show growth potential, driven by economic diversification efforts and population growth. However, the region’s market dynamics are varied, with the Middle East displaying a strong preference for poultry and lamb, while Africa’s consumption patterns are rapidly evolving with its economic development.

Latin America continues to grow as an exporter and consumer of meat, particularly beef and poultry, supported by its extensive livestock production capabilities. Brazil and Argentina are especially prominent in the global meat trade, influencing regional market trends significantly.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In 2024, the global Edible Meat Market continues to be shaped by the strategic movements and innovations of key players, each contributing uniquely to the industry’s dynamics.

Cargill stands out with its vast integration across the meat supply chain, from feed production to meat processing. Cargill’s commitment to sustainability and the traceability of its products caters to the growing consumer demand for ethical and environmentally conscious meat sources. This focus not only strengthens their market position but also sets industry standards for operational transparency and eco-friendly practices.

Tyson Foods, another major player, leverages its extensive product range and distribution network to maintain a strong market presence. In response to shifting consumer preferences, Tyson has been expanding into plant-based protein products, blending traditional meat offerings with innovative alternatives. This strategy enables Tyson to meet diverse consumer needs and tap into the burgeoning market for alternative proteins, positioning it as a forward-thinking leader in both traditional and emerging meat markets.

JBS S.A., recognized as one of the largest meat producers globally, continues to dominate with strategic acquisitions and expansions, especially in emerging markets. Their aggressive growth strategy not only increases their global footprint but also enhances their capacity to meet the rising meat demand in fast-developing regions.

Maple Leaf Foods focuses on quality and sustainability, appealing to health-conscious consumers looking for premium, sustainable meat products. Their investments in meat alternatives also reflect an adaptive strategy to industry trends, aiming to capture a significant share of the health and environmentally focused market segment.

These companies exemplify how diverse strategies from sustainability and supply chain control to product innovation and market expansion drive the global edible meat market’s growth and resilience. Each company’s approach reflects its response to global trends and consumer demands, shaping the competitive landscape of the industry.

Market Key Players

- Al Aali Exports Pvt. Ltd

- Allanasons Private Limited

- BRF S.A

- Cargill

- Cloverdale Foods

- Danone

- Farm Suzanne Pvt Limited

- HMA Agro Industries Limited

- Hormel Foods

- JBS S.A.

- Maple Leaf Foods

- Marfrig

- Mark International Food Stuff Pvt. Ltd

- Mirha Exports Pvt. Ltd

- MK Overseas Private Limited

- Moy Park

- Perdue Farms

- Pilgrim’s Pride

- Sanderson Farms

- Smithfield Foods

- Suguna Foods Private Limited

- Tyson Foods

- VH Group

- Vion Food Group

Recent Development

- In July 2024, Upside Foods, a leading cultivated meat company, reduced its workforce by 26 positions due to industry challenges and a decline in venture capital funding. The company is restructuring to focus on critical milestones in preparation for product launches within the next two years.

- In June 2024, Amid significant increases in egg and meat prices in the U.S. due to an avian flu outbreak and record inflation, Vital Farms experienced a 177% stock increase. The company’s success is attributed to its premium, pasture-raised egg offerings, achieving strong earnings growth despite challenging market conditions.

- In June 2024, The European pork industry faced potential challenges with the possibility of China restricting pork imports from the region. This concern arose in response to EU-imposed anti-subsidy duties on Chinese electric vehicles, leading Chinese firms to request an anti-dumping investigation into EU pork imports. In 2023, China imported $6 billion worth of pork, over half of which came from the EU.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1113 Billion |

| Forecast Revenue (2033) | USD 1481.0 Billion |

| CAGR (2024-2032) | 2.9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2016-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Beef, Mutton, Pork, Poultry, Others), By Form (Canned, Fresh/Chilled, Frozen, Processed), By Process (Fresh, Processed, Frozen, Cured, Smoked), By Source (Commercial, Artisanal, Organic, Local, Wild-Caught), By Distribution Channel (Convenience Stores, Online Channel, Supermarkets and Hypermarkets, Others) |

| Regional Analysis | North America – The US, Canada, Rest of North America, Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America – Brazil, Mexico, Rest of Latin America, Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa |

| Competitive Landscape | Al Aali Exports Pvt. Ltd, Allanasons Private Limited, BRF S.A, Cargill, Cloverdale Foods, Danone, Farm Suzanne Pvt limited, HMA Agro Industries Limited, Hormel Foods, JBS S.A., Maple Leaf Foods, Marfrig, Mark International Food Stuff Pvt. Ltd, Mirha Exports Pvt. Ltd, MK Overseas Private Limited, Moy Park, Perdue Farms, Pilgrim’s Pride, Sanderson Farms, Smithfield Foods, Suguna Foods Private Limited, Tyson Foods, VH Group, Vion Food Group |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |