Quick Navigation

Report Overview

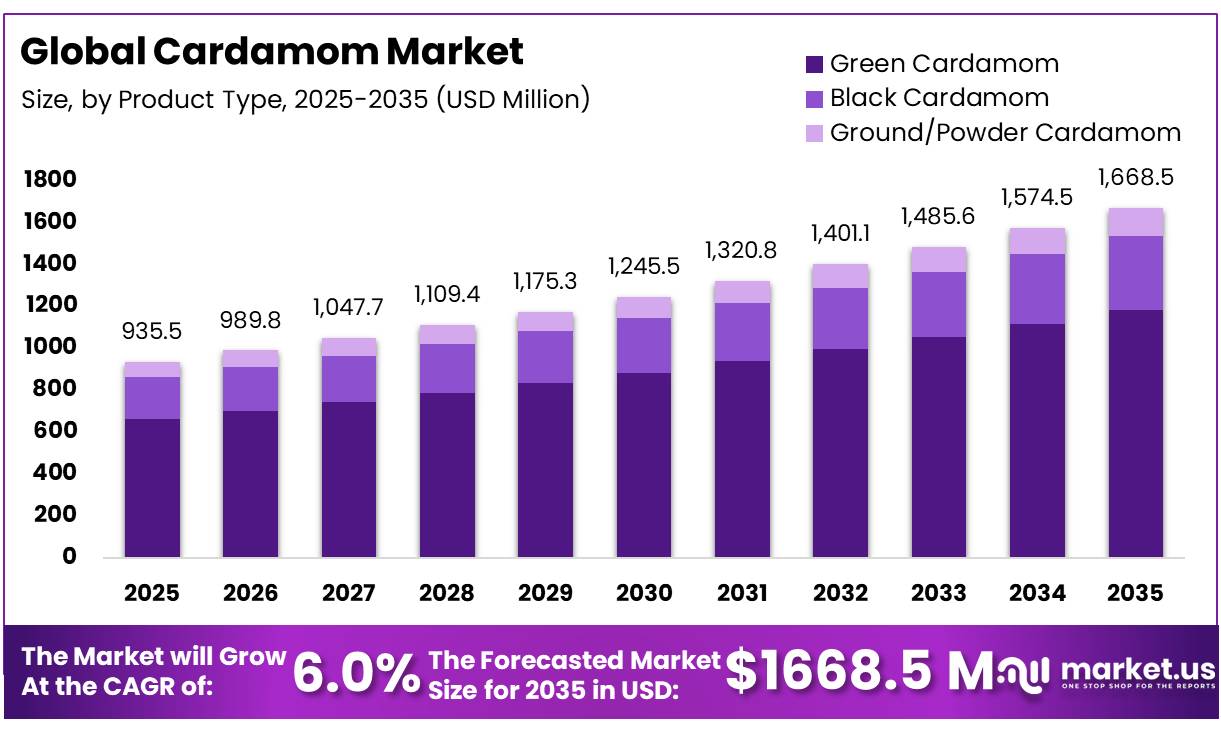

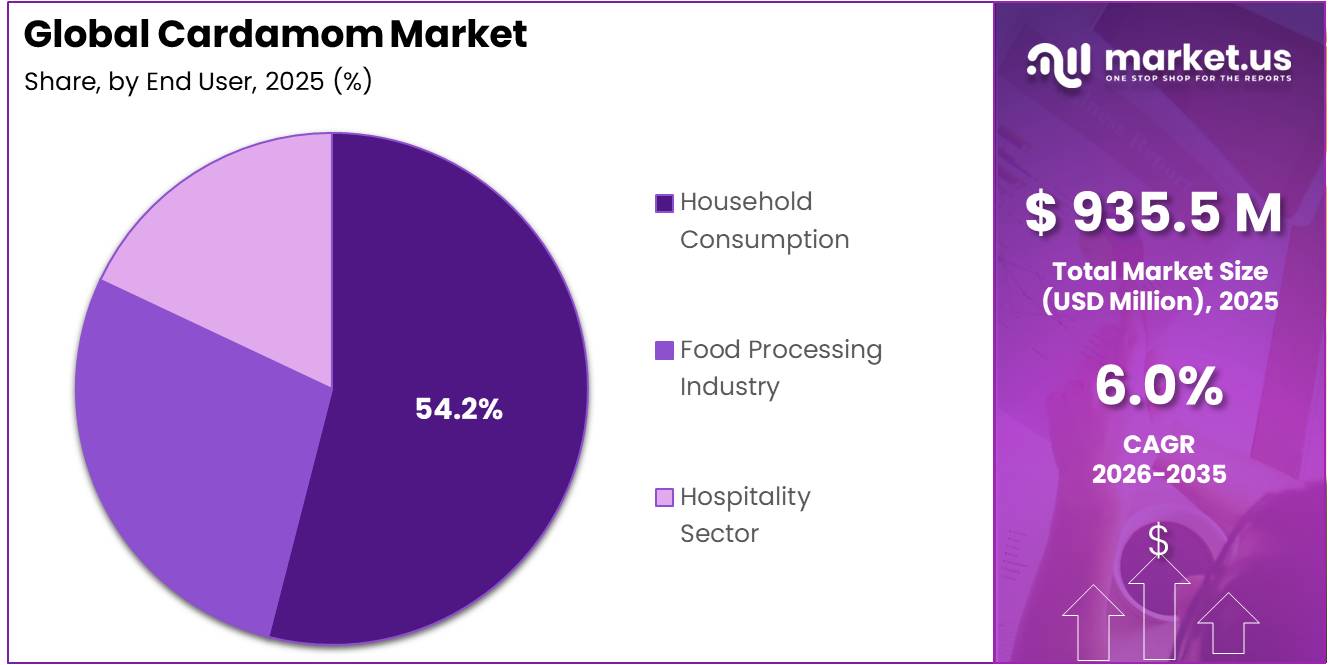

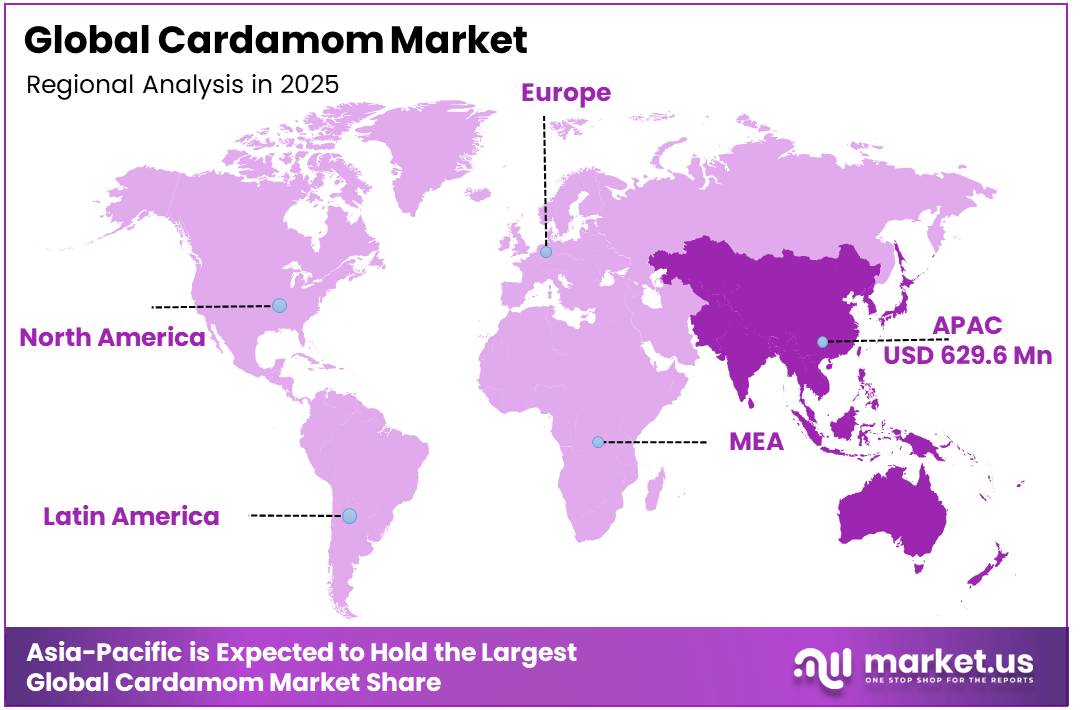

In 2025, the Global Cardamom Market was valued at USD 935.5 million, and between 2026 and 2035, this market is estimated to register a CAGR of 6.0%, reaching about USD 1668.5 million by 2035. In 2025, Asia Pacific led the market, achieving over 67.3% share with a revenue of USD 629.6 Million.

The cardamom market is expanding due to rising global demand for natural spices and increasing use in pharmaceuticals and cosmetics. The spice is a key ingredient in premium beverage applications, specialty confectionery, and traditional baking lines. Growing consumer awareness regarding antioxidant and digestive health benefits is supporting demand from the nutraceutical industry.

- According to the Centre for the Promotion of Imports from developing countries (CBI), Germany imported approximately 683 tonnes of cardamom valued at €5.8 million in 2023, with around 97% of imports originating from developing countries, highlighting the country’s strong dependence on international spice-producing regions for cardamom supply.

Key Takeaways

- The global cardamom market was valued at USD 935.5 Million in 2025.

- The market is projected to grow at a CAGR of 6.0% and is estimated to reach USD 1668.5 Million by 2035.

- On the basis of product type, green cardamom dominated the market, constituting 71.1% of the total market share.

- Based on the nature type, conventional cardamom led the market, comprising 82.3% of the total market share.

- Based on the form, whole pods held a major share in the cardamom market, accounting for 63.2% of the total market.

- Among the applications, the food & beverages segment was the most considerable within the market, accounting for 58.5% of the total revenue.

- Among the distribution channels, supermarkets/hypermarkets held a major share in the market, comprising 36.1% of the total distribution.

- Among the end-users, household consumption was the most considerable within the market, accounting for 54.2% of the market share.

- In 2025, the Asia-Pacific was the most dominant region in the cardamom market, accounting for 67.3% of the total global consumption.

The cardamom market is driven by a convergence of supply disruption and shifting trade geography. Widespread crop failures in Guatemala have created a persistent gap in global supply, repositioning India as the primary international provider across major import corridors. This supply tightening has driven e-auction prices for premium-grade cardamom upward at regulated domestic trading centers. Smallholders, who form the foundational layer of India’s production base, continue to face rising cultivation costs and remain highly vulnerable to erratic monsoon patterns that can materially alter yield outcomes within a single growing season.

In response, the Indian government has moved to consolidate this competitive opportunity at the policy level, with the Spices Board of India launching the SPICED initiative under the Ministry of Commerce and Industry directly targeting cardamom productivity improvement, post-harvest quality upgrades, and value-added export development across the supply chain.

Cardamom Market Segmentation

Product Type Analysis

Green Cardamom represents dominant Segment in the Market.

In 2025, the green cardamom category dominated the market, accounting for 71.1%. This dominance is fueled by ingrained consumer culinary heritage in major consuming countries and extensive structural purchasing networks in destination economies.

Green cardamom is an important spice in international trade due to its strong aroma, bright green color, and wide use in food, beverages, and pharmaceutical products. It is especially popular in Middle Eastern countries, where premium green cardamom is commonly used in traditional coffee preparations. Global trade is supported by quality standards based on pod size, color, and moisture content, helping maintain product consistency and value. Premium-grade cardamom often receives higher prices, encouraging quality-focused cultivation.

Nature Type Analysis

Conventional Cardamom Yields Bulk Volumes Across Commercial Sectors.

The Conventional cardamom category dominated the market in 2025, accounting for 82.3% of the total, because to existing infrastructure, consistent high-density yields, and cost-effective pricing for mass consumption. Conventional networks serve as the crucial backbone of world trade, transporting vast volumes of goods from rural agricultural farms directly to major wholesale purchasers. Industrial food processors, international beverage blenders, and commercial spice packagers all employ standard lots to keep raw material costs under control and retail customer pricing steady.

Organic cardamom will reach significant valuation milestones from 2026 to 2035 as a result of clean-label agricultural certification. This growth is being spurred by the European Food Safety Authority’s tightening of maximum residue limits for chemical pesticides, disrupting conventional trade. Furthermore, a steady shift in customer preference for transparent supply chains and non-GMO products drives spice handlers to invest directly in organic farming networks, bio-fertilizer research, and third-party certifications in order to acquire high-margin retail areas.

Form Analysis

Whole Pods Dominate the Supply Chain Through Flavor Preservation.

In 2025, the whole pods sector dominated the market with a 63.2% share. The unmilled cardamom capsule’s inherent physical structural stability, which naturally shields essential oils from quick oxidation and environmental deterioration during long-distance transit, is what drives its dominance. Whole pods are the major trading currency in international spice auctions, giving purchasers a clear visual way to judge quality based on pod diameter, color saturation, and physical cleanliness.

The key wholesale importers in Saudi Arabia, the United Arab Emirates, and India prioritize bulk procurement of whole pods to carry out internal quality grading before downstream processing or local packing happens. Technically, this leadership is maintained because the cardamom capsule’s fibrous outer shell acts as a natural barrier, preserving volatile chemicals such as 1,8 cineole.

Cardamom oil and extracts are the fastest-growing, with significant milestones expected to be reached between 2026 and 2035. This shift minimizes laborious pod cleaning and waste in food processing by utilizing automated, closed-loop liquid dosing systems. Advanced supercritical carbon dioxide extraction generates solvent-free oleoresins, maintaining complete flavor homogeneity.

Application Analysis

Cardamom Are Mostly Utilized in the Food & Beverages Sector.

In 2025, the food and beverage segment dominated the market, accounting for 58.5%. This domination stems from cardamom’s strong structural integration into worldwide culinary traditions, commercial beverage formulations, and mass-market consumer snack manufacturing processes. The food and beverage application sector is the principal volume engine for the whole cardamom supply chain, consuming massive amounts of spice lots from several sub-categories on a daily basis. The rapid global expansion of industrial spice-mix manufacturing networks and commercial hospitality channels adds to this enormous market depth.

The pharmaceuticals segment is the fastest-growing application vector. Over the forecast period, as global medical research confirms the spice’s therapeutic properties, the medical application segment will absorb a significant portion of specialized cardamom extracts, establishing a high-value market alongside traditional food channels. This growth is being driven by an increasing amount of clinical research proving the usefulness of cardamom components in reducing gastrointestinal inflammation, regulating blood pressure, and providing strong antioxidant defense.

Distribution Channel Analysis

Supermarkets and Hypermarkets Lead Volume Distribution Worldwide.

In 2025, supermarkets and hypermarkets dominated the market, accounting for 36.1%. This dominance stems from their wide store network, strong product visibility, trusted branded packaging, and easy consumer access in urban and semi-urban areas. These retail formats allow buyers to compare different cardamom grades, pack sizes, and prices in one place. Their organized shelf placement and regular household footfall make them a preferred channel for both premium whole pods and standard packaged cardamom products.

Online Retail is the fastest-growing segment in the Cardamom Market as this segment is experienced strong growth as consumers increasingly turned to e-commerce platforms for purchasing spices and food ingredients. Online retail channels offer greater convenience, wider product selection, competitive pricing, and direct access to premium and specialty cardamom products. Spice manufacturers and retailers have also expanded their digital presence to strengthen customer reach and improve product accessibility.

End User Analysis

Cardamom Are Mostly Utilized in the Household Consumption Sector.

In 2025, the household consumption sector dominated the market, accounting for 54.2%, due to the extensive use of cardamom in everyday cooking, beverages, bakery products, desserts, and traditional food preparations across various regions. Consumers continued to prefer cardamom for its distinctive aroma, flavor, and versatility in both sweet and savory applications. The growing popularity of home cooking, premium spices, and natural flavoring ingredients further supported demand from household users. In addition, increasing consumer awareness regarding the culinary value of cardamom encouraged regular usage in tea, coffee, confectionery products, and homemade recipes.

The food processing industry is the fastest-growing end-user segment, with large industrial consumption milestones expected between 2026 and 2035 as commercial food manufacturing continues to automate globally. According to analysis, by 2035, mass-market food manufacturers would increase industrial cardamom procurement to feed high-speed production lines, hence growing the commercial B2B spice sector.

Key Market Segments

By Product Type

- Green Cardamom

- Black Cardamom

- Ground/Powder Cardamom

By Nature Type

- Conventional

- Organic

By Form

- Whole Pods

- Powdered Form

- Oil & Extracts

By Application

- Food & Beverages

- Bakery & Confectionery

- Pharmaceuticals

- Personal Care & Cosmetics

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Traditional Retail Stores

- Online Retail

- Specialty Stores

By End User

- Household Consumption

- Food Processing Industry

- Hospitality Sector

Driver Analysis

Export diversification through USA-UAE-Bangladesh-Saudi trade corridors

India’s spices export basket remains highly diversified by destination, with the USA accounting for 14% of total spice export earnings, China 12%, UAE 9%, Bangladesh 8%, and Saudi Arabia 5%, while the top destinations together contribute more than 85% of export earnings. Even though these figures are for the broader spices complex rather than cardamom alone, they are strategically important because cardamom export demand typically scales through the same importer-distributor architecture, especially through Gulf redistribution hubs and South Asian consumption corridors where whole spice trading remains channel-driven.

This widens the addressable market beyond domestic Indian consumption and lowers dependence on any single geography; commercially, it supports better shipment continuity, greater bargaining power for exporters with mixed spice portfolios, and stronger sell-through for premium and reprocessed cardamom formats, adding an estimated 1.4 percentage points to forward growth as channel density improves.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Indian auction-price strength lifting farm realizations and replanting economics | +1.9% | India core, Gulf-linked export routes, South Asia spill-over | Short term (≤ 2 years) |

| Export diversification through USA-UAE-Bangladesh-Saudi trade corridors | +1.4% | India core, Middle East, North America, South Asia | Medium term (2-4 years) |

| Nepal large-cardamom supply expansion increasing category depth | +1.2% | Nepal core, India border trade, South Asia, selective EU/Asia importers | Medium term (2-4 years) |

| EU pesticide-residue enforcement accelerating compliance-led premiumization | +0.8% | EU core, India exporters, re-export hubs in Gulf | Short term (≤ 2 years) |

| Climate-resilient cultivation and water-soil management reducing yield volatility | +1.1% | Nepal Himalaya belt, South India high ranges, broader producer zones | Long term (≥ 4 years) |

| Formal auction infrastructure improving market transparency and inventory turnover | +0.9% | India core, trader networks serving Gulf and domestic wholesale markets | Short term (≤ 2 years) |

Restraint Analysis

EU residue risk

The sharpest commercial restraint is export-market residue non-compliance, because even a limited number of official alerts can amplify buyer caution across the whole origin: the EU Rapid Alert System recorded Notification 2025.4636 for multiple pesticide residues in cardamom from India on 20 June 2025, while parallel official trade-policy tracking indicates the EU is discussing tightening profenofos maximum residue levels for cardamom and related spices to a limit of determination near 0.01-0.02 mg/kg from late 2026 or early 2027, which effectively narrows tolerance bands for exporters.

In practice, this increases pre-shipment testing frequency, raises rejection and rerouting risk, extends shipment release times, and forces exporters to segregate compliant and non-compliant lots more aggressively, compressing margins for smaller merchants that lack direct farm traceability or in-house quality systems; the result is a modeled 1.8 percentage-point drag on CAGR as some EU-bound volumes are discounted, delayed, or redirected to lower-yield channels.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU residue risk | -1.8% | EU core, India export base, Gulf re-export hubs | Short term (≤ 2 years) |

| Weather-yield volatility | -1.6% | South India core, Nepal belt, APAC supply corridors | Medium term (2-4 years) |

| Auction price swings | -1.2% | India core, domestic trade hubs, Gulf-linked buyers | Short term (≤ 2 years) |

| Post-harvest bottlenecks | -1.1% | India origin clusters, NE India, Nepal border trade | Medium term (2-4 years) |

| Productivity dependence on schemes | -0.9% | India core, smallholder belts, FPO channels | Long term (≥ 4 years) |

| Export compliance overhead | -0.8% | India exporters, EU, North America, Middle East | Short term (≤ 2 years) |

Opportunity Analysis

GI-linked cardamom premiumization is an opportunity because the category has not yet fully converted origin identity into systematic price capture, despite public policy already creating the enabling rails: the SPICED scheme explicitly includes promoting exportable surplus of GI and other spices from the North East, along with organic certification, care-and-cure support, and post-harvest quality improvement.

That means the institutional groundwork exists, but the upside remains underexploited at commercial scale; firms that translate GI status into verifiable batch-level storytelling, QR-linked traceability, estate grading, and premium channel placement in GCC gourmet retail, EU specialty stores, and high-end HoReCa can lift average realization by an estimated 12-18% on selected lots, expand premium-grade sell-through, and create a differentiated shelf proposition that is much harder for generic bulk suppliers to match

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Branded retail formats | +1.8% | India core, Gulf, UK, North America ethnic channels | Short term (≤ 2 years) |

| GI premium exports | +1.4% | India core, EU niche, GCC premium retail, NE India spill-over | Medium term (2-4 years) |

| Residue-clean supply chains | +1.6% | EU core, UK, North America, Japan | Short term (≤ 2 years) |

| FPO-led processing scale | +1.3% | South India core, NE India, APAC supply corridors | Medium term (2-4 years) |

| Extracts and oleoresins | +1.1% | India processing hubs, EU food industry, North America flavors | Long term (≥ 4 years) |

| India-Nepal portfolio play | +0.9% | South Asia core, Gulf re-export hubs, selective EU buyers | Medium term (2-4 years) |

Challenges Analysis

Market concentration risk

Market concentration risk is an enduring challenge because cardamom trade is still heavily dependent on a limited set of origins and a relatively narrow pool of destination markets, making the sector vulnerable to correlated shocks rather than diversified exposure: India and Nepal dominate small and large cardamom supply, and official trade statistics indicate that a handful of countries such as the USA, key EU states, Gulf economies and some South Asian neighbors—account for the bulk of India’s spice export earnings, with small cardamom constituting about 9% of the total spice-export value in 2025–26.

Strategically, firms must pursue origin diversification (within and beyond South Asia), destination diversification into emerging markets, and the development of more flexible product portfolios that can be redirected across geographies; executing such a diversification plan typically requires several planning cycles and non-trivial M&A or JV activity, which is why market concentration risk imposes an estimated 0.7 percentage-point drag on the market’s maximum attainable CAGR over the long term as risk buffers absorb capital and management bandwidth that could otherwise fuel aggressive volume expansion.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Climate–yield variability | -1.4% | South India core, Nepal belt, APAC hills | Long term (≥ 4 years) |

| Income & price volatility | -1.2% | India core, Guatemala, South Asia traders | Medium term (2-4 years) |

| Compliance–logistics complexity | -1.0% | India exporters, EU, Gulf, East Asia | Medium term (2-4 years) |

| Extension & skills gap | -0.9% | India and Nepal smallholders, NE India | Long term (≥ 4 years) |

| Post-harvest capability spread | -0.8% | India origin clusters, Nepal, APAC corridors | Medium term (2-4 years) |

| Market concentration risk | -0.7% | India export base, key destination hubs | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Risk Assessment in West Asian Conflict Realignment and Trade Corridor Bottlenecks.

Geopolitical tensions in West Asia are creating pricing, logistics, and payment-related pressure on the global cardamom market. Gulf countries remain among the most important destination markets for Indian cardamom, with nutmeg, mace, and cardamom exports from India valued at USD 295.5 million and nearly 70.5% shipped to the Gulf region. This high exposure makes Indian exporters sensitive to freight disruption, higher insurance costs, delayed vessel movement, and weaker buyer confidence in markets such as the UAE, Saudi Arabia, Qatar, and Iran. Recent trade reports also indicate that cardamom prices corrected from around ₹2,800 per kg to nearly ₹2,400 per kg after the West Asia crisis affected export demand and movement.

At the same time, India has gained a supply-side opportunity because Guatemala, one of the major competing origins, faced nearly 50% crop loss due to adverse weather and pest-related issues. This shortage has shifted part of global demand toward Indian cardamom, especially for premium green pods used in Gulf and European markets. However, the benefit from tight global supply is being partly limited by West Asia-linked shipping delays, payment uncertainty, and rising logistics costs. As a result, farmers, traders, exporters, and spice processors are facing a mixed market situation where stronger global demand is being balanced by trade corridor risks and short-term price volatility.

Regional Analysis

Asia Pacific Held the Largest Share of the Cardamom Market.

The Asia-Pacific area commands 67.3% of the global cardamom market, making it the world’s largest and fastest-growing territory. According to regional distribution data and demographic tracking matched with the World Population Review, this large spatial concentration sets global trade benchmarks. The dominance is further supported by extensive agricultural footprints and large consumer populations in key hubs such as India and Sri Lanka. These hubs support huge domestic culinary networks while also driving international export pipelines. This focused market architecture ensures that localized production cycles and regional trade updates have a direct impact on global wholesale commodity quantities.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The cardamom market is characterized by an asymmetric, highly consolidated oligopolistic framework at the export, processing, and multi-national distribution levels, as opposed to a highly fragmented structure at the agricultural baseline. This distinct dual-market behaviour means that, while tens of thousands of independent smallholder farmers in India, Guatemala, and Sri Lanka drive raw agricultural output, a small group of consolidated international spice houses, enterprise food processors, and national trading syndicates control the primary market share of international distribution channels.

The complete reliance of baseline smallholders on changeable local weather patterns such as the recent monsoon changes in India and major crop failures in Guatemala regularly results in large supply shocks. Because these disorganized smallholders absorb around 70-80% of upstream production costs, any structural crop loss results in a high-stakes scramble for physical inventory at centralized trading hubs such as India’s Vandanmedu e-auction center. This fragmentation enables consolidated oligopolistic buyers to employ their vast cash to acquire premium bold grades during supply gluts, so boosting their long-term market share supremacy while leaving small-scale producers vulnerable to localized financial hazards.

The Major Players In The Industry

- McCormick & Company

- Olam Group

- Synthite Industries

- Nedspice Group

- Cardex S.A.

- Mane KANCOR

- MAS Enterprises Ltd.

- Royal Spices

- Everest Spices

- MDH Spices

- DS Group

- Frontier Co-op

- Bart Ingredients

- Spice Jungle

Key Development

- In November 2025, DS Group’s Catch Salt & Spices brand expanded its product portfolio in Uttar Pradesh, India launching a premium “Origins” range and broadening its whole spices line to include Big Cardamom alongside Red Chilli, Bay Leaf, and Garam Masala, while targeting rural distribution and quick commerce expansion.

- In September 2025, Olam Group reported $33.7 billion in revenue and strengthened its cardamom business through ofi. The company signed a partnership with SASI and MOVE-ComCashew, agreed to divest its 64.57% stake in Olam Agri, and expanded its global reach across 60+ countries and 20,000+ customers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$935.5 Mn |

| Forecast Revenue (2035) | US$1668.5 Mn |

| CAGR (2026-2035) | 6.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Green Cardamom, Black Cardamom, Ground/ Powder Cardamom), By Nature Type (Conventional, Organic),By Form (Whole Pods, Powdered Form, Oil & Extracts), By Application (Food & Beverages, Bakery & Confectionery, Pharmaceuticals, Personal Care & Cosmetics, Others), By Distribution Channel (Supermarkets/ Hypermarkets, Traditional Retail Stores, Online Retail, Specialty Stores), By End User (Household Consumption, Food Processing Industry, Hospitality Sector) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | McCormick & Company, Olam Group, Synthite Industries, Nedspice Group, Cardex S.A., Mane KANCOR, MAS Enterprises Ltd., Vandanmedu Green Gold Cardamom Producer Company, Royal Spices, Everest Spices, MDH Spices, DS Group, Frontier Co-op, Bart Ingredients, Spice Jungle. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |