Quick Navigation

Report Overview

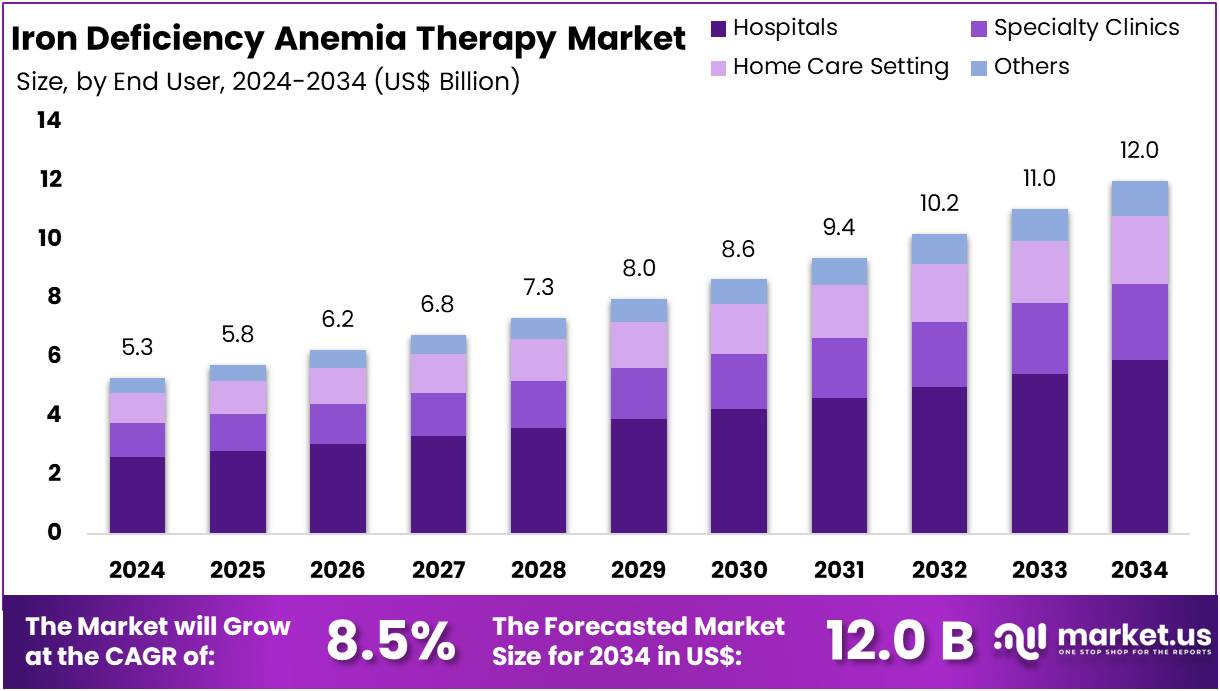

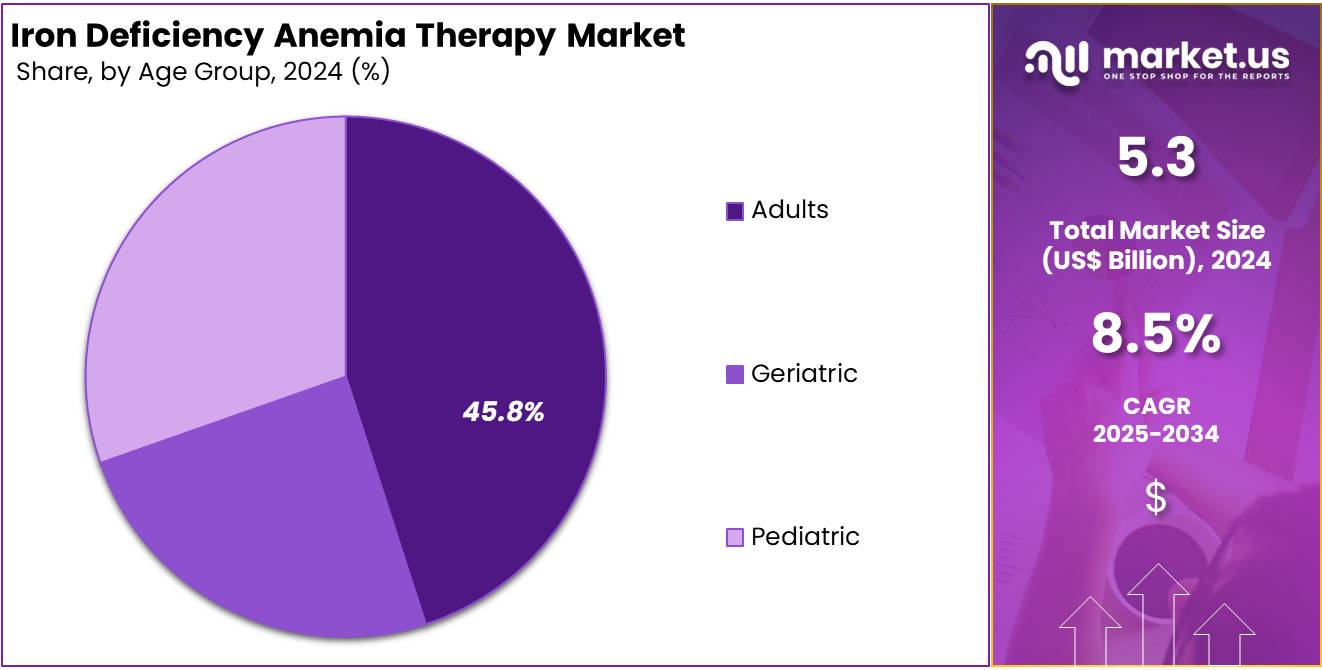

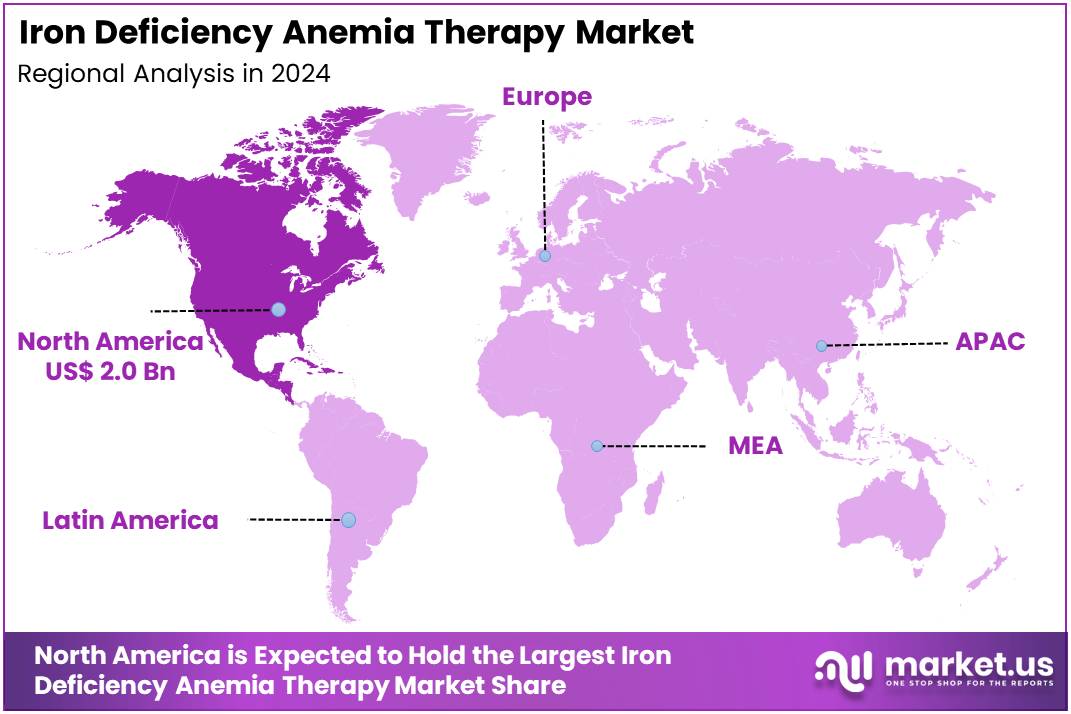

The Global Iron Deficiency Anemia Therapy Market Size is expected to be worth around US$ 12 Billion by 2034, from US$ 5.3 Billion in 2024, growing at a CAGR of 8.5% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 38.2% share and holds US$ 2.0 Billion market value for the year.

Iron Deficiency Anemia (IDA) therapy is witnessing robust growth due to its rising prevalence and evolving treatment technologies. According to the World Health Organization (WHO), iron deficiency affects nearly 30% of the global population. Vulnerable groups include children, pregnant women, and women of reproductive age. For instance, 40% of children aged 6–59 months and 37% of pregnant women are anemic. This high prevalence drives the need for efficient diagnostic methods and therapeutic interventions.

IDA poses serious health challenges and economic burdens. It impairs cognitive and physical development in children and reduces productivity in adults. For example, in pregnant women, IDA is linked to increased risks of low birth weight and preterm birth. These complications lead to higher healthcare costs. A study from Korea reported a 2.3-fold increase in IDA prevalence between 2002 and 2013, with a 2.8-fold rise in healthcare expenditures during the same period. Such trends stress the urgency of early treatment and preventive care.

The adoption of advanced diagnostic tools has also supported market growth. WHO recommends serum ferritin concentration as a key indicator to assess iron levels. This approach allows for early detection and targeted therapy. For example, population-based strategies using ferritin testing help reduce the delay in diagnosis, allowing faster therapeutic response and improved outcomes in at-risk individuals.

Technological advancements in treatment options are further boosting market expansion. Intravenous (IV) iron therapy has become essential, especially for patients intolerant to oral iron. For instance, in a study of 1,186 patients undergoing elective arthroplasty, IV iron reduced allogeneic blood transfusion (ABT) rates from 30.1% to 8.9% and shortened hospital stays from 10.7 to 8.4 days. Similarly, among 1,361 hip fracture patients, IV iron therapy decreased ABT rates and 30-day mortality (from 9.4% to 4.8%).

Global health policies are creating supportive environments for therapy adoption. The WHO aims to reduce anemia in women of reproductive age by 50% by 2025. These initiatives promote awareness, early detection, and access to care, contributing to broader therapy uptake. As countries align with WHO goals, public health programs are increasingly incorporating IDA screening and treatment protocols into routine care.

Athletes also represent a unique therapy segment. According to various studies, 15–35% of female and 3–11% of male endurance athletes experience iron deficiency. For example, a Japanese university study found that 47% of female athletes had low ferritin levels despite no anemia. Supplementing with 100 mg/day of elemental iron for up to 56 days has shown performance improvements ranging from 2% to 20%, demonstrating therapeutic benefits in non-clinical populations.

The IDA therapy market is growing due to widespread prevalence, health and economic consequences, improved diagnostics, treatment innovations, and strong global health initiatives. These factors are collectively driving demand for effective and scalable therapy options worldwide.

Key Takeaways

- The global Iron Deficiency Anemia Therapy market is projected to reach US$ 12 billion by 2034, up from US$ 5.3 billion in 2024.

- This growth reflects a robust CAGR of 8.5% during the forecast period spanning 2025 to 2034, indicating rising global demand for anemia treatments.

- In 2024, the Obstetrics and Gynecology segment led the therapy area category, accounting for over 29.8% of the total market share.

- Adult patients represented the largest share in the age group segment in 2024, contributing more than 45.8% to the global market value.

- Among end users, the Adults section dominated in 2024, securing a market share of more than 38.5% across therapy applications.

- North America emerged as the leading regional market in 2024, capturing over 38.2% share and recording a value of US$ 2.0 billion.

Therapy Area Analysis

In 2024, the Obstetrics and Gynecology section held a dominant market position in the Therapy Area Segment of the Iron Deficiency Anemia Therapy Market, and captured more than a 29.8% share. Experts attribute this lead to the high incidence of anemia during pregnancy. The demand is also supported by growing awareness about maternal health. Improvements in prenatal care services are another driving factor. Urban women, in particular, are increasingly accessing iron therapies during pregnancy to manage or prevent iron deficiency.

The Renal Diseases segment has also shown strong performance in the market. Patients with chronic kidney disease (CKD) are often diagnosed with iron deficiency anemia. This is due to low erythropoietin levels and chronic inflammation. Intravenous iron supplements are commonly used in dialysis treatment, boosting segment growth. Medical professionals note that better screening and treatment protocols for CKD have increased the use of targeted iron therapies in renal care settings.

Other key areas include Congestive Heart Failure (CHF), Oncology, and Inflammatory Bowel Disease (IBD). CHF patients often experience worsening symptoms due to anemia. This has led to a rise in iron-based interventions. In cancer care, iron therapies support patients receiving chemotherapy. Oncologists frequently combine iron with other agents to improve recovery. In IBD, blood loss and poor absorption drive demand for iron therapy. Experts also point to the Others category, which includes post-surgery care, as an area with growing therapeutic interest.

Age Group Analysis

In 2024, the Adults section held a dominant market position in the Age Group Segment of the Iron Deficiency Anemia Therapy Market, and captured more than a 45.8% share. According to analysts, this was due to a higher rate of diagnosis among adults. Adults are more proactive in managing their health. Factors such as poor diet, stress, and menstruation contributed to iron loss. This increased demand for iron supplements. The availability of various treatment options also helped boost market share.

Experts noted that working adults often seek timely medical care. This age group is also more likely to undergo routine check-ups. That leads to faster identification and treatment of anemia. Urbanization plays a role too. People in cities have better access to healthcare facilities and pharmacies. Moreover, oral and intravenous iron therapies are well-suited for adult use. All these factors combined to drive strong growth in this segment throughout the year.

In comparison, pediatric and geriatric groups showed lower market penetration. For children, treatment is often complex due to dosage limitations. Parents may also delay seeking care for minor symptoms. Among the elderly, other chronic conditions can complicate iron therapy. However, analysts expect these segments to grow in the coming years. New product formulations and increased awareness will help. But for now, the adult segment remains the leading contributor to market revenue and continues to set the pace for overall growth.

End User Analysis

In 2024, the Adults section held a dominant market position in the End User Segment of the Iron Deficiency Anemia Therapy Market, and captured more than a 38.5% share. This dominance was largely attributed to increased hospital visits for iron therapy among adults. Hospitals offered a full range of services, including diagnostic tools and advanced IV treatments. Their ability to manage complex anemia cases made them the preferred choice for many adult patients. This trend was consistent across both urban and semi-urban areas.

Specialty clinics followed closely behind hospitals. These centers focused on tailored care for adults dealing with chronic conditions like cancer or kidney disease. The personalized approach made these clinics a reliable choice for ongoing treatment. Patients appreciated the lower wait times and focused attention. These facilities also began offering outpatient infusion therapies. Their rise reflects the growing need for disease-specific iron deficiency care among the adult population.

The home care setting showed strong growth potential. Many adults shifted to at-home therapies for convenience and comfort. Oral iron supplements and IV therapy kits were increasingly available for home use. Insurance providers also began covering more home-based treatments. This shift supported patients with mobility issues or those seeking flexible care. While smaller, community health centers and wellness clinics played a growing role. They provided access to underserved areas and helped raise awareness about anemia therapy options.

Key Market Segments

By Therapy Area

- Obstetrics and Gynecology

- Renal Diseases

- Congestive Heart Failure (CHF)

- Oncology

- Inflammatory Bowel Disease

- Others

By Age Group

- Adults

- Geriatric

- Pediatric

By End User

- Hospitals

- Specialty Clinics

- Home Care Setting

- Others

Drivers

Rising Global Prevalence and WHO-Endorsed Intervention Strategies

The rising global prevalence of iron deficiency anemia (IDA) is a critical factor driving the demand for effective therapeutic interventions. According to the World Health Organization, in 2023, 30.7% of women of reproductive age and 35.5% of pregnant women globally were affected by anemia. Additionally, 39.8% of children aged 6–59 months had anemia in 2019. These high prevalence rates across vulnerable groups highlight the urgent need for targeted treatment options and preventive therapies.

To address this public health burden, the WHO has introduced multiple guidelines promoting iron supplementation. Daily iron intake is recommended for menstruating women and adolescent girls in regions with anemia prevalence exceeding 20%. Infants aged 6–23 months in areas with over 40% anemia prevalence are also advised to receive daily iron supplements. These recommendations create a continuous demand for iron-based therapies across different population segments, reinforcing market growth for IDA treatments.

Furthermore, antenatal care protocols include daily supplementation with 30–60 mg of iron and 400 µg of folic acid to reduce the risk of maternal anemia and poor birth outcomes. The WHO also stresses regular assessment and monitoring of iron status using ferritin concentration measurements. This emphasis on diagnostic screening and preventive supplementation further supports the expansion of therapeutic and diagnostic tools in the IDA therapy market.

Restraints

Limited Awareness and Underdiagnosis in Developing Regions

In many developing regions, the iron deficiency anemia (IDA) therapy market faces a major hurdle due to limited public awareness. Individuals often remain unaware of the symptoms and health risks associated with iron deficiency. As a result, early detection is rare, and patients typically seek medical help only when complications arise. This delay in diagnosis reduces the effectiveness of timely therapeutic interventions. Consequently, the market for IDA therapies remains underpenetrated in these regions, restricting its potential growth.

Underdiagnosis further compounds the challenge of limited awareness. Healthcare systems in developing countries often lack sufficient diagnostic infrastructure and trained personnel. As a result, iron deficiency anemia frequently goes unrecognized or is misdiagnosed as other general fatigue-related conditions. This diagnostic gap leads to missed opportunities for initiating proper treatment, particularly in high-risk groups such as women of reproductive age and children. Without a robust diagnostic framework, the uptake of IDA therapies remains slow.

In addition to healthcare limitations, cultural beliefs and socioeconomic factors also contribute to poor health-seeking behavior. In many rural or low-income communities, iron supplementation or anemia screening is not prioritized. Educational campaigns and public health outreach are often inadequate, leaving large population groups uninformed. This systemic neglect not only worsens health outcomes but also dampens commercial interest and investment in expanding IDA therapeutic services across these regions.

Opportunities

Increasing Adoption of Intravenous (IV) Iron Formulations Across Global Markets

The growing limitations of oral iron supplements have shifted clinical focus toward intravenous (IV) iron therapies. Oral supplements often lead to gastrointestinal discomfort, reduced patient adherence, and lower absorption rates. These challenges are particularly notable in individuals with chronic conditions such as chronic kidney disease (CKD) and inflammatory bowel disease (IBD). As a result, IV iron offers a more effective solution for rapid iron repletion. This rising preference is driving healthcare providers to adopt IV iron therapy in both inpatient and outpatient settings.

In developed countries, advanced healthcare infrastructure and strong reimbursement systems are enabling faster adoption of IV iron products. Hospitals and specialty clinics are increasingly prescribing these formulations due to their efficacy and faster onset of action. The prevalence of anemia-related complications in high-risk populations, such as oncology and nephrology patients, further amplifies this demand. Pharmaceutical companies can leverage this shift by investing in next-generation IV iron formulations with improved safety profiles and easier administration protocols.

Emerging markets are also witnessing a steady rise in the use of IV iron therapies. Rising healthcare awareness, increasing diagnostic rates, and expanding hospital networks are contributing to the growth. Governments and health organizations are working to reduce anemia burdens, especially among pregnant women and children. This policy support, combined with rising disposable incomes, creates a strong foundation for IV iron therapy expansion in regions like Asia-Pacific, Latin America, and parts of Africa.

Trends

Increasing Adoption of Home-Based Oral Iron Therapies

The iron deficiency anemia (IDA) therapy market is witnessing a rising preference for home-based treatment solutions. Patients are increasingly opting for oral iron supplements due to their ease of administration and reduced dependence on clinical settings. This trend is driven by the need to enhance treatment compliance and minimize the burden of frequent hospital visits. Oral therapies offer a practical solution, especially for elderly patients and individuals in remote locations, where access to healthcare services is limited or inconsistent.

This shift towards home healthcare aligns with broader global trends favoring outpatient and self-managed care. Health systems are under pressure to reduce costs, hospital admissions, and in-person consultations. As a result, therapy providers are re-evaluating their product portfolios to prioritize oral formulations. These formulations not only support patient convenience but also contribute to long-term disease management. In regions with aging populations, the demand for non-invasive and home-friendly therapies is expected to increase further in the coming years.

Manufacturers are responding by enhancing the palatability, bioavailability, and tolerability of oral iron supplements. Marketing strategies now emphasize patient-centric features such as once-daily dosing, fewer gastrointestinal side effects, and availability over the counter. This transformation is not only improving access to therapy but also opening new avenues for direct-to-consumer marketing. The trend is expected to shape future innovation in iron supplementation delivery systems.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 38.2% share and holds US$ 2.0 Billion market value for the year. This leading position is largely due to the region’s strong healthcare systems and early diagnosis practices. There is a high level of public awareness about iron deficiency anemia (IDA), especially among women and elderly patients. As a result, treatment uptake is widespread. Regular health checkups and proactive anemia screening have contributed significantly to market growth.

A wide range of iron therapies is available across the United States and Canada. Pharmaceutical manufacturers have ensured efficient distribution of both oral and intravenous iron products. The U.S. Food and Drug Administration (FDA) has supported this trend by approving newer and more effective formulations. These innovations are quickly adopted in clinical settings. Hospital and pharmacy networks are well-equipped to handle high demand, especially for injectable therapies used in chronic conditions.

Government-supported nutrition and health programs have further strengthened treatment access in underserved communities. Iron supplementation is often included in public health strategies, particularly for women and children. The presence of national initiatives focused on anemia management has driven therapy adoption. In addition, partnerships between public agencies and healthcare providers have improved outreach and patient compliance with prescribed therapies.

Chronic diseases such as chronic kidney disease and cancer are prevalent in the region. These conditions frequently require iron therapy, especially intravenous options. According to the CDC, iron deficiency remains the most common nutritional issue in the U.S. This has led to increased demand for targeted treatments. The aging population, which often suffers from malabsorption, is also contributing to higher usage of injectable iron formulations.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Iron Deficiency Anemia (IDA) therapy market includes both global pharmaceutical firms and niche biotech companies. AbbVie Inc. maintains a presence through its broad commercial network, though IDA is not its core focus. Its strength lies in acquisition strategies and biologic R&D, which may support future advancements in iron therapies. Akebia Therapeutics stands out with vadadustat, targeting anemia in CKD patients. Their focus on innovation and partnerships helps grow global access. AMAG Pharmaceuticals, now part of Covis Pharma, remains key in IV iron treatment via Feraheme.

CSL Vifor leads the IV iron therapy market globally, with products like Ferinject and Venofer. The company holds strong links with nephrologists and cardiologists. Its merger with CSL boosts research and international expansion. This positions it as a dominant player in the IDA space. Daiichi Sankyo focuses on both prescription and OTC iron products across Asia. Its R&D aims to enhance oral iron systems. These efforts may help increase patient adherence and create new market opportunities in IDA therapies.

Smaller firms and regional players also add competitive pressure in the IDA market. These companies often address localized treatment gaps or innovate around formulation and delivery. They target patients who struggle with standard oral or IV iron products. Their agility helps them respond to unmet needs more rapidly than large pharma companies. Together, these emerging players support broader access and add innovation to the space. The IDA therapy market continues to evolve, driven by advancements, partnerships, and a focus on underserved patient groups.

Market Key Players

- AbbVie Inc.

- Akebia Therapeutics

- AMAG Pharmaceuticals

- CSL Vifor

- Daiichi Sankyo Company

- Emcure Pharmaceuticals

- Ironic Biotech

- Johnson & Johnson

- Kye Pharmaceuticals

- Pharmacosmos Therapeutics

- Shield Therapeutics

- Teva Pharmaceuticals

Recent Developments

- In May 2023: Akebia Therapeutics entered into a licensing agreement with Medice Arzneimittel Pütter GmbH & Co. KG for the commercialization of Vafseo in Europe and Australia. Under the terms of the agreement, Medice agreed to pay Akebia $10 million upfront and up to $100 million in commercial milestones for the rights to Vafseo in these regions. This partnership followed the termination of a previous agreement with Otsuka Pharmaceutical, which had been valued at up to $865 million. Medice brings extensive expertise in nephrology and an established European dialysis business, positioning it well to support the launch and commercialization of Vafseo in these markets.

- In August 2023: American Regent, Inc., a Daiichi Sankyo Group company, announced results from the Phase 3 HEART-FID trial of INJECTAFER® for the treatment of iron deficiency in adult heart failure patients with reduced ejection fraction (HFrEF). The trial evaluated the efficacy and safety of INJECTAFER in this patient population. The results contributed to the understanding of INJECTAFER’s role in managing iron deficiency among heart failure patients.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 5.3 Billion |

| Forecast Revenue (2034) | US$ 12 Billion |

| CAGR (2025-2034) | 8.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Therapy Area (Obstetrics and Gynecology, Renal Diseases, Congestive Heart Failure (CHF), Oncology, Inflammatory Bowel Disease, Others), By Age Group (Adults, Geriatric, Pediatric), By End User (Hospitals, Specialty Clinics, Home Care Setting, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | AbbVie Inc., Akebia Therapeutics, AMAG Pharmaceuticals, CSL Vifor, Daiichi Sankyo Company, Emcure Pharmaceuticals, Ironic Biotech, Johnson & Johnson, Kye Pharmaceuticals, Pharmacosmos Therapeutics, Shield Therapeutics, Teva Pharmaceuticals |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |