Quick Navigation

- Report Overview

- Key Takeaways

- Therapy Type Analysis

- Therapy Area Analysis

- Patient Analysis

- Distribution Channel Analysis

- End-User Analysis

- Key Market Segments

- Drivers

- Restraints

- Opportunities

- Impact of Macroeconomic / Geopolitical Factors

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

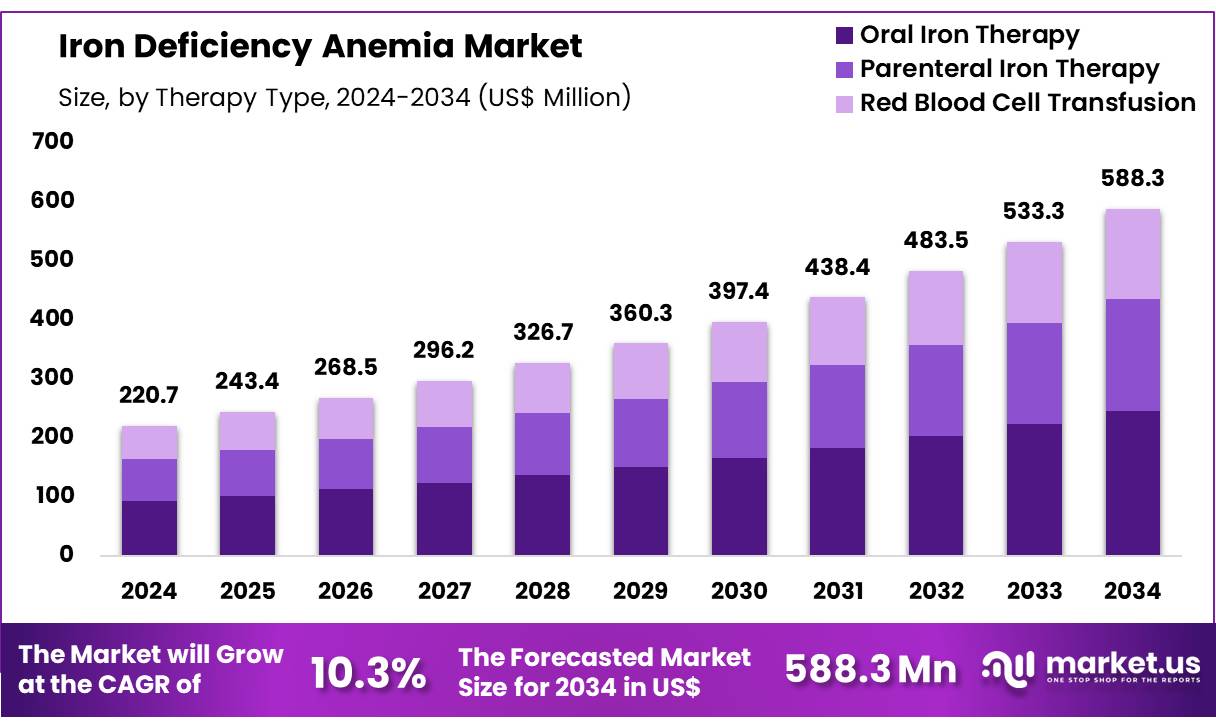

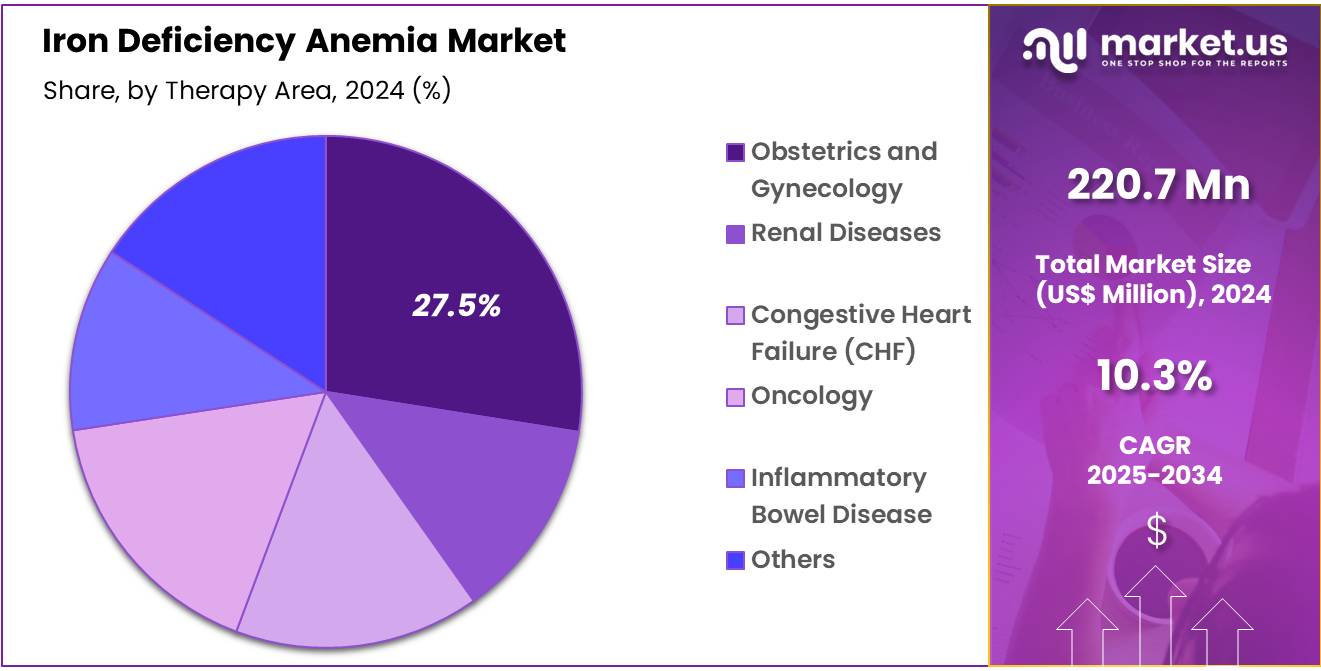

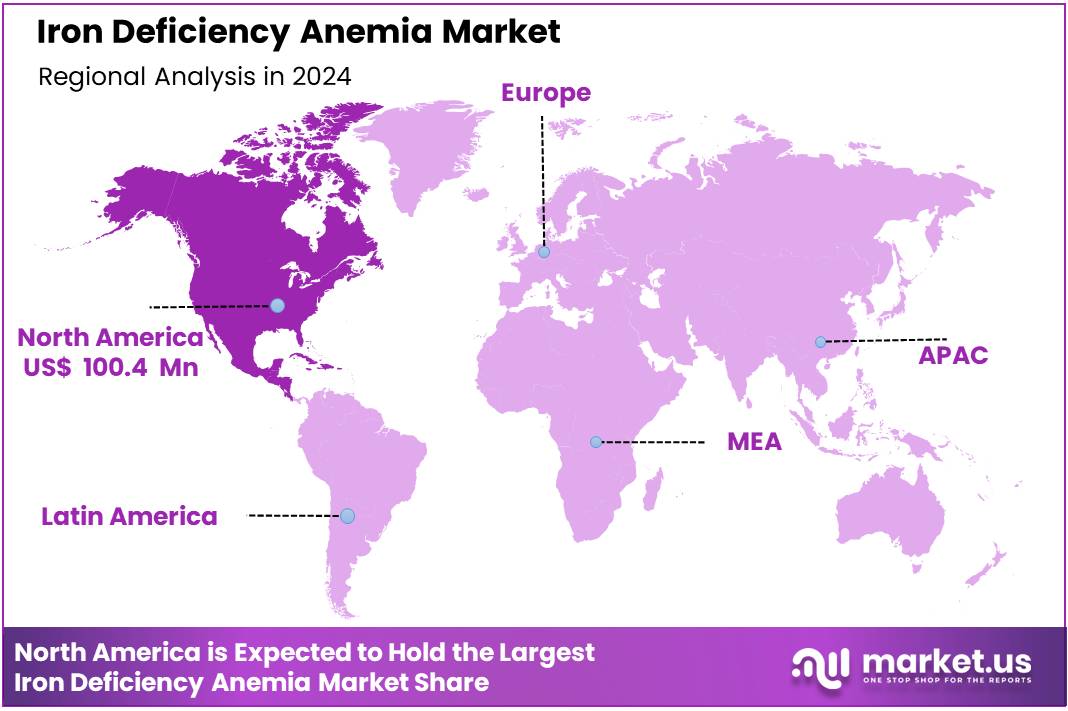

Global Iron Deficiency Anemia Market size is expected to be worth around US$ 588.3 million by 2034 from US$ 220.7 million in 2024, growing at a CAGR of 10.3% during the forecast period 2024 to 2034. In 2024, North America led the market, achieving over 45.5% share with a revenue of US$ 100.4 Million.

The Iron Deficiency Anemia Market is experiencing rapid growth, driven by advancements in telemedicine, remote patient monitoring, and wearable health technology. These devices use Adults, Geriatric, RFID, and IoT to enable real-time health data transmission, enhancing patient outcomes and reducing hospital visits.

Key product categories include wearable devices (smartwatches, ECG monitors), implantable devices (pacemakers, neurostimulators), and portable monitoring systems (glucometers, infusion pumps). The market is fueled by the increasing prevalence of chronic diseases, aging populations, and the shift toward home healthcare solutions.

Strategic initiatives by market players such as collaborations, partnerships, in the market is a major driving factor for the market. For instance, in December 2024, Nokia announced a new research initiative in collaboration with Fraunhofer Heinrich Hertz Institute (HHI) and Charité – Universitätsmedizin Berlin to explore the potential of wireless sensing technologies in medical applications.

The partnership aims to investigate how sub-terahertz (sub-THz) frequencies can be used to remotely detect human vital signs, paving the way for advanced non-invasive medical monitoring and diagnostic solutions. Sub-THz frequencies, ranging from 90 GHz to 300 GHz, possess unique properties that make them ideal for wireless sensing.

Functioning similarly to radar but with significantly higher precision, these frequencies enable highly accurate detection due to their small wavelengths and high bandwidth. Nokia Bell Labs, Fraunhofer HHI, and Charité are working together to develop sensing networks that leverage sub-THz frequencies for ultra-high-resolution spatial scans in hospital environments, allowing for continuous monitoring of patients’ vital signs.

Key Takeaways

- In 2024, the market for Iron Deficiency Anemia generated a revenue of US$ 220.7 million, with a CAGR of 10.3%, and is expected to reach US$ 588.3 million by the year 2034.

- The Therapy Type segment is divided into Oral Iron Therapy, Parenteral Iron Therapy and Red Blood Cell Transfusion, with Oral Iron Therapy taking the lead in 2024 with a market share of 41.9%.

- Considering Therapy Area, the market is divided into Obstetrics and Gynecology, Renal Diseases, Congestive Heart Failure (CHF), Oncology, Inflammatory Bowel Disease and Others, Obstetrics and Gynecology held a significant share of 27.5%.

- Furthermore, concerning the Patient, the market is segregated into Adults, Geriatric, Pediatric. The Adults segment stand out as the dominant segment, holding the largest revenue share of 45.9% in the Iron Deficiency Anemia market.

- Based on Distribution Channel, the market is bifurcated into Hospital Pharmacies, Retail Pharmacies, Online Pharmacies. Hospital Pharmacies holds the largest market share with 48.9%.

- By End-User, the market is classified into Hospitals, Specialty Clinics, Home Care Setting and Others. Hospitals held a major share of 38.7%.

- North America led the market by securing a market share of 45.5% in 2023.

Therapy Type Analysis

The Oral Iron Therapy segment dominated the Iron Deficiency Anemia (IDA) market with 41.9% market share, driven by its affordability, ease of administration, and widespread availability. Oral iron supplements, such as ferrous sulfate, ferrous gluconate, and ferric citrate, are commonly prescribed as the first-line treatment for mild to moderate anemia. This segment benefits from a high patient preference due to its non-invasive nature and over-the-counter accessibility. New product approvals and launches in the market is helping the market grow in the oral iron therapy segment.

For instance, in October 2020, The U.S. Food and Drug Administration (FDA) has approved oral ferric maltol for treating iron deficiency in adults. Ferric maltol is a non-salt formulation of ferric iron, offering an alternative to traditional salt-based oral iron therapies while reducing common gastrointestinal side effects.

This approval was supported by data from the AEGIS-H2H study, which demonstrated that oral ferric maltol was noninferior to intravenous iron therapy in increasing hemoglobin levels in patients with iron-deficiency anemia, without the need for hospital-based administration.

Therapy Area Analysis

The Obstetrics and Gynecology segment dominated the Iron Deficiency Anemia (IDA) market with 27.5% market share, primarily due to the high prevalence of anemia in pregnant women and menstruating females. Increased iron demand during pregnancy, blood loss during childbirth, and heavy menstrual bleeding are key factors driving the segment.

According to NCBI data, approximately 35.6% of women experienced maternal or fetal morbidity. Anemia was the most common pregnancy-related complication, affecting 62.3% of cases. Other complications included difficult labor (3%), postpartum hemorrhage (1.6%), preeclampsia (1.6%), and abortion or stillbirth (3.5%). Fetal complications primarily involved low birth weight (25.5%), followed by premature delivery (0.2%) and birth asphyxia (0.5%).

Governments and healthcare organizations actively promote iron supplementation programs to reduce maternal and neonatal complications, further fueling market growth. Renal Diseases is another significant segment, as chronic kidney disease (CKD) patients often develop anemia due to reduced erythropoietin production and iron deficiency. The Oncology and Inflammatory Bowel Disease (IBD) segments also contribute significantly due to treatment-related anemia and malabsorption issues.

Patient Analysis

The Adults segment dominates the Iron Deficiency Anemia (IDA) market with 45.9% market share, primarily due to the high prevalence of anemia among women of reproductive age, pregnant women, and individuals with chronic conditions such as kidney disease and inflammatory disorders. Lifestyle factors, poor dietary intake, and higher iron requirements contribute to the segment’s dominance.

The Geriatric segment is also growing, driven by age-related nutritional deficiencies, chronic illnesses, and reduced iron absorption. Pediatric cases, while significant, are often addressed through government-led supplementation programs and dietary interventions.

Distribution Channel Analysis

The Hospital Pharmacies led the Iron Deficiency Anemia (IDA) market with holding a major market share of 48.9%, driven by the high demand for prescription-based iron therapies, especially for severe anemia cases requiring parenteral iron therapy or red blood cell transfusions. Hospitals are primary treatment centers for patients with chronic conditions like renal diseases, oncology-related anemia, and severe pregnancy-related anemia, further contributing to this segment’s dominance.

The Retail Pharmacies segment holds a significant share, catering to patients with mild to moderate anemia who rely on over-the-counter (OTC) oral iron supplements. Meanwhile, the Online Pharmacies segment is experiencing rapid growth due to increasing e-commerce penetration, convenience, and discounts on iron supplements.

End-User Analysis

The Hospitals segment dominated the Iron Deficiency Anemia (IDA) market with 38.7% share, driven by the need for parenteral iron therapy, red blood cell transfusions, and specialized anemia management in severe cases.

Hospitals serve as primary treatment centers for patients with chronic kidney disease (CKD), cancer-related anemia, and obstetric complications, where intensive care and monitoring are essential. Specialty Clinics also hold a significant share, particularly in managing anemia related to renal diseases, oncology, and obstetrics & gynecology, offering targeted treatment solutions.

Key Market Segments

Therapy Type

- Oral Iron Therapy

- Parenteral Iron Therapy

- Red Blood Cell Transfusion

Therapy Area

- Obstetrics and Gynecology

- Renal Diseases

- Congestive Heart Failure (CHF)

- Oncology

- Inflammatory Bowel Disease

- Others

Patient

- Adults

- Geriatric

- Pediatric

Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

End-User

- Hospitals

- Specialty Clinics

- Home Care Setting

- Others

Drivers

Rising Prevalence of Iron Deficiency Anemia (IDA)

The increasing prevalence of iron deficiency anemia worldwide is a significant driver of the market. IDA is the most common nutritional disorder, affecting millions of people, particularly women of reproductive age, pregnant women, children, and individuals with chronic diseases such as chronic kidney disease (CKD) and inflammatory bowel disease (IBD).

According to the World Health Organization (WHO), anemia affects over 1.6 million people globally, with iron deficiency being the leading cause. Poor dietary habits, malnutrition, gastrointestinal disorders, and heavy menstrual bleeding further contribute to the rising cases.

In January 2022, the WHO acknowledged iron deficiency anemia (IDA) as the most prevalent nutritional deficiency worldwide, affecting 30% of the global population. While IDA is more common among children and women, adult men can also be vulnerable, depending on their socioeconomic status and overall health.

Additionally, the aging population and the rising prevalence of chronic diseases that cause blood loss or impair iron absorption are exacerbating the issue. As awareness about anemia increases, along with the need for effective treatment options, pharmaceutical companies are investing in innovative therapies, including novel intravenous iron formulations and better-tolerated oral supplements.

Governments and healthcare organizations are also promoting iron fortification programs, which further contribute to market growth by expanding access to iron therapies and driving demand for effective treatments.

Restraints

Side Effects and Safety Concerns of Iron Supplements

Despite the increasing demand for iron supplements and intravenous iron therapies, safety concerns and side effects associated with these treatments act as a major market restraint. Oral iron supplements, particularly ferrous salts like ferrous sulfate, can cause gastrointestinal side effects such as nausea, constipation, diarrhea, and stomach cramps, leading to poor patient adherence. Many patients discontinue their prescribed iron therapy due to these side effects, reducing treatment efficacy and limiting market growth.

Additionally, intravenous (IV) iron formulations, while more effective in treating severe IDA cases, are associated with risks such as hypersensitivity reactions, anaphylaxis, and oxidative stress-related complications. Regulatory agencies, including the FDA and EMA, have imposed strict guidelines and safety monitoring for IV iron therapies, which can slow down product approvals and commercialization.

These safety concerns create barriers for market penetration, making it crucial for pharmaceutical companies to develop better-tolerated formulations and educate healthcare providers and patients about appropriate dosing and management of side effects.

Opportunities

Technological Advancements in Iron Therapy

Advancements in drug delivery technologies and novel formulations present a significant opportunity for the iron deficiency anemia market. One of the most promising developments is the introduction of nano-formulated iron supplements and liposomal iron formulations, which enhance bioavailability and reduce gastrointestinal side effects compared to traditional ferrous salts. These formulations ensure better iron absorption with minimal irritation to the digestive tract, improving patient adherence.

Additionally, research into heme iron polypeptides offers another alternative with higher absorption rates and fewer side effects. In the intravenous (IV) segment, new-generation iron complexes such as ferric carboxymaltose and ferric derisomaltose allow for high-dose administration in a single infusion, reducing the need for multiple hospital visits. The growing use of artificial intelligence (AI) and machine learning in drug development is also facilitating faster research and clinical trials for innovative therapies.

Moreover, partnerships between biotech firms and pharmaceutical giants to develop novel oral and injectable iron products further create opportunities for expansion in emerging and developed markets. In July 2021, Sandoz, a global leader in generic and biosimilar medicines, has announced the immediate availability of generic Ferumoxytol in the U.S. This intravenous medication is used to treat iron deficiency anemia (IDA) and is a generic equivalent to AMAG Pharmaceuticals’ Feraheme (ferumoxytol injection).

It is approved for adult patients with IDA who cannot tolerate oral iron, have had an inadequate response to oral iron, or have chronic kidney disease. The global IV iron market exceeds $1 million and continues to expand.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly impact the Iron Deficiency Anemia (IDA) market, affecting drug availability, pricing, and access to care. Economic downturns, inflation, and healthcare budget cuts reduce affordability and limit government funding for anemia treatment programs, especially in low-income regions. Rising costs of raw materials and logistics further drive up drug prices, making iron therapies less accessible.

Geopolitical instability, including wars, trade restrictions, and supply chain disruptions, affects the manufacturing and distribution of iron supplements and IV iron formulations. For example, the Russia-Ukraine conflict and trade tensions between China and the U.S. have caused shortages of key pharmaceutical ingredients. Currency fluctuations also impact the affordability of imported iron therapies in developing countries.

Despite these challenges, global health organizations and governments are increasing investments in anemia awareness and fortification programs. This continued focus on public health initiatives is expected to support market growth, even amid economic and geopolitical uncertainties.

Latest Trends

Growing Preference for Intravenous Iron Therapy

Over the past few years, there has been an increasing shift toward intravenous (IV) iron therapy due to its higher efficacy and faster replenishment of iron stores compared to oral supplements. IV iron therapy is particularly beneficial for patients with chronic diseases such as chronic kidney disease (CKD), heart failure, and inflammatory bowel disease (IBD), where oral iron is poorly absorbed or not tolerated.

Newer formulations like ferric carboxymaltose and ferric derisomaltose allow for the administration of large doses in a single infusion session, reducing hospital visits and improving treatment adherence. This shift is further supported by recommendations from medical associations like the National Kidney Foundation and the American Gastroenterological Association, which endorse IV iron for patients with severe anemia. Additionally, the expansion of ambulatory and outpatient infusion centers is making IV iron therapy more accessible, fueling market growth.

Regional Analysis

North America is leading the Iron Deficiency Anemia Market

North America dominates the Iron Deficiency Anemia (IDA) market due to high healthcare spending, advanced treatment options, and increasing prevalence of chronic diseases like chronic kidney disease (CKD) and cancer-related anemia. The U.S. leads the region, with strong pharmaceutical R&D and widespread adoption of intravenous (IV) iron therapies along with new approvals and launches in the region.

In June 2023, Daiichi Sankyo, Inc. and American Regent, Inc., a subsidiary of the Daiichi Sankyo Group, announced today that the U.S. Food and Drug Administration (FDA) has approved INJECTAFER (ferric carboxymaltose injection) for the treatment of iron deficiency in adult patients with heart failure classified as New York Heart Association (NYHA) class II/III, aimed at improving exercise capacity.

The Europe region is second largest market

Europe holds a significant market share, driven by government initiatives, iron fortification programs, and advanced healthcare infrastructure. Countries like Germany, the U.K., and France see rising demand for IV iron formulations, particularly in pregnant women and elderly populations.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the market include AbbVie Inc., Akebia Therapeutics Inc., AMAG Pharmaceuticals Inc. (Covis Group S.à r.l.), Daiichi Sankyo Company, Pharmacosmos A/S, Sanofi S.A., Johnson & Johnson, Fresenius SE & Co. KGaA, CSL Vifor, Rockwell Medical, Inc., Akorn Operating Company LLC, Shield Therapeutics plc, AdvaCare Pharma, Otsuka Pharmaceutical Co., Ltd., Sun Pharmaceutical Industries Ltd., and Other key players.

AbbVie is a global biopharmaceutical company known for its research-driven approach to drug development. In the Iron Deficiency Anemia (IDA) market, AbbVie has a strong presence through its portfolio of anemia-related treatments, especially targeting patients with chronic kidney disease (CKD) and inflammatory conditions.

Akebia Therapeutics specializes in developing renal and anemia-related treatments. Its flagship product, Vafseo (vadadustat), is an oral hypoxia-inducible factor prolyl hydroxylase (HIF-PH) inhibitor designed to treat anemia associated with chronic kidney disease (CKD).

AMAG Pharmaceuticals was a key player in the IDA market before being acquired by Covis Group S.à r.l.. It developed and marketed Feraheme (ferumoxytol), an intravenous (IV) iron therapy approved for the treatment of IDA in adults with CKD. Feraheme provides a rapid, high-dose iron infusion with fewer hospital visits, making it a preferred option for patients with severe anemia.

Top Key Players

- AbbVie Inc.

- Akebia Therapeutics Inc.

- AMAG Pharmaceuticals Inc. (Covis Group S.à r.l.)

- Daiichi Sankyo Company

- Pharmacosmos A/S

- Sanofi S.A.

- Johnson & Johnson

- Fresenius SE & Co. KGaA

- CSL Vifor

- Rockwell Medical, Inc.

- Akorn Operating Company LLC

- Shield Therapeutics plc

- AdvaCare Pharma

- Otsuka Pharmaceutical Co., Ltd.

- Sun Pharmaceutical Industries Ltd.

- Other key players

Recent Developments

- In March 2024, CSL Vifor has announced that Health Canada has approved Ferinject (ferric carboxymaltose) for intravenous (IV) treatment of iron deficiency anemia in adults and pediatric patients aged one year and older when oral iron supplements are ineffective or not well tolerated. Additionally, it has been authorized for treating iron deficiency in adult patients with heart failure classified as New York Heart Association (NYHA) class II/III to enhance exercise capacity. With this approval, Ferinject is now authorized for marketing in 87 countries worldwide.

- In February 2023, the U.S. Food and Drug Administration (FDA) approved Jesduvroq (daprodustat) tablets as the first oral treatment for anemia caused by chronic kidney disease in adults undergoing dialysis for at least four months. Jesduvroq is not approved for use in patients who are not on dialysis.

- In July 2021, Sandoz, a global leader in generic and biosimilar medicines, today announced the immediate US availability of generic Ferumoxytol, an intravenous medicine used to treat iron deficiency anemia (IDA).

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 220.7 Million |

| Forecast Revenue (2034) | US$ 588.3 Million |

| CAGR (2025-2034) | 10.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2022 |

| Forecast Period | 2024-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Online Pharmacies Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Therapy Type (Oral Iron Therapy, Parenteral Iron Therapy and Red Blood Cell Transfusion), By Therapy Area (Obstetrics and Gynecology, Renal Diseases, Congestive Heart Failure (CHF), Oncology, Inflammatory Bowel Disease and Others), By Patient (Adults, Geriatric, Pediatric), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By End-User (Hospitals, Specialty Clinics, Home Care Setting and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | AbbVie Inc., Akebia Therapeutics Inc., AMAG Pharmaceuticals Inc. (Covis Group S.à r.l.), Daiichi Sankyo Company, Pharmacosmos A/S, Sanofi S.A., Johnson & Johnson, Fresenius SE & Co. KGaA, CSL Vifor, Rockwell Medical, Inc., Akorn Operating Company LLC, Shield Therapeutics plc, AdvaCare Pharma, Otsuka Pharmaceutical Co., Ltd., Sun Pharmaceutical Industries Ltd., and Other key players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |