Quick Navigation

Report Overview

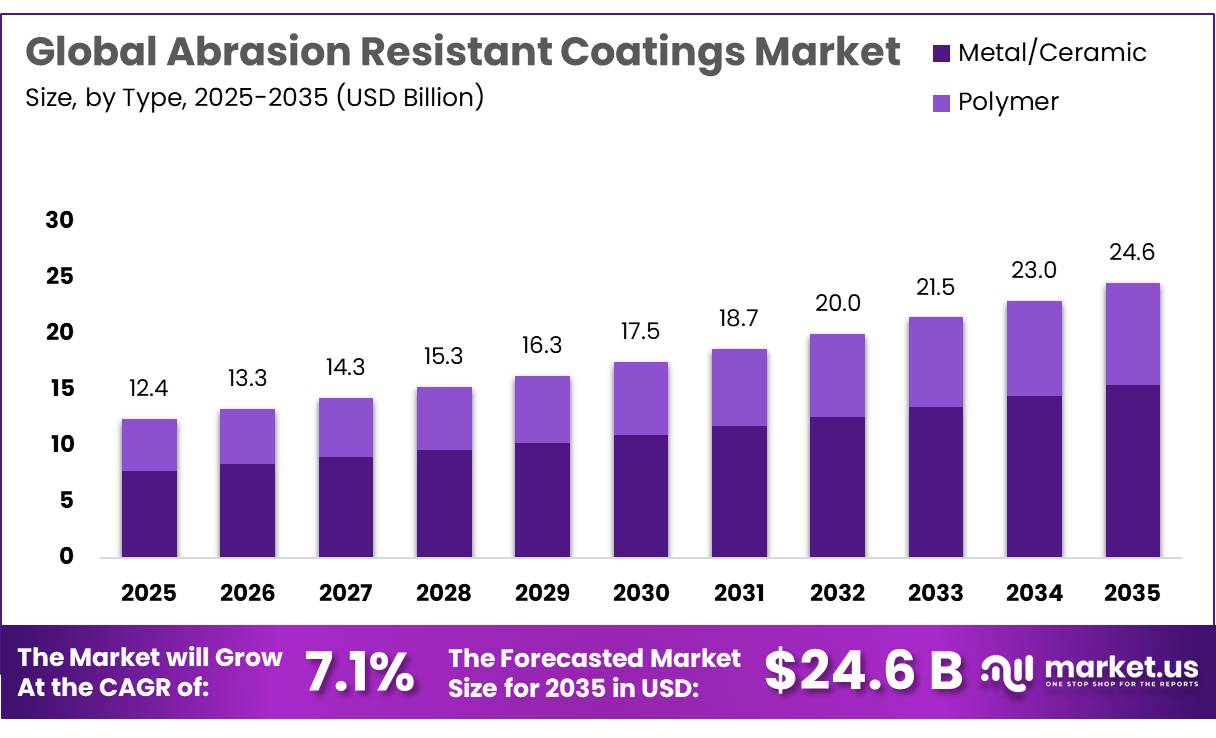

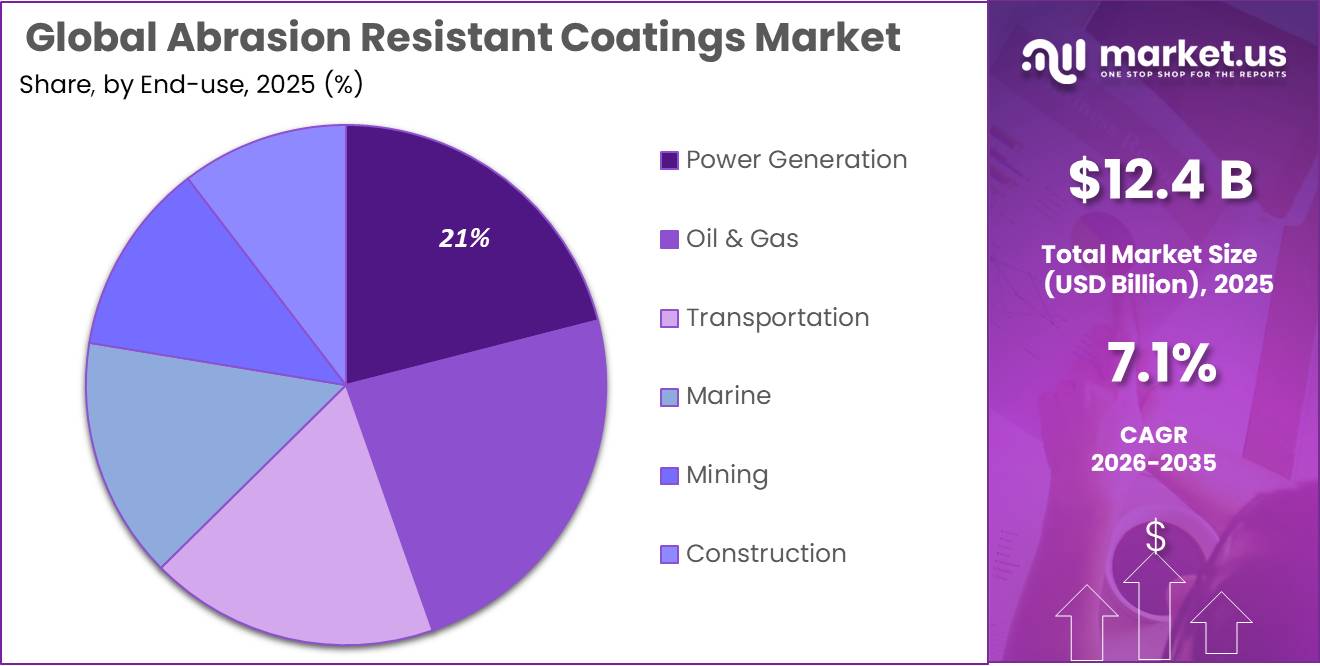

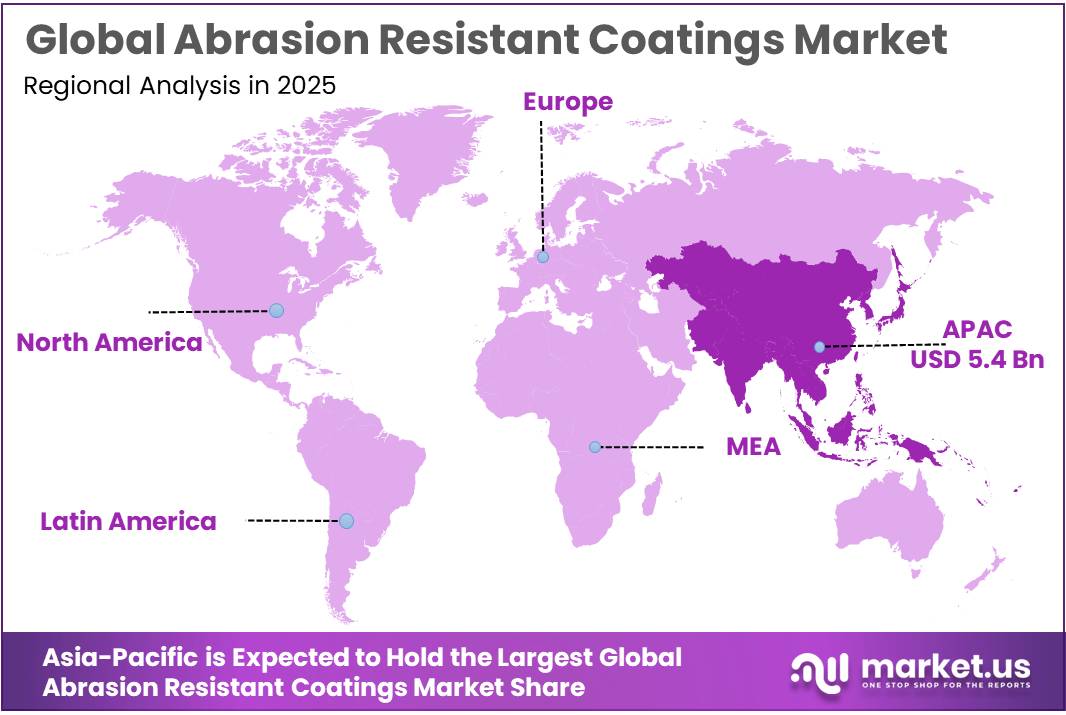

The Global Abrasion Resistant Coatings Market size is expected to be worth around USD 24.6 Billion by 2035, from USD 12.4 Billion in 2025, growing at a CAGR of 7.1% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 43.7% share, holding USD 5.4 Billion revenue.

Abrasion-resistant coatings are protective systems used on metals, concrete, plastics and equipment surfaces to reduce wear from friction, particles, impact and cleaning cycles. Industrial demand is supported by heavy-use sectors such as food processing, automotive, marine, construction, mining and general manufacturing, where coating failure can raise downtime and replacement costs. In food and beverage manufacturing, the need is clear: U.S. food and beverage processors accounted for 16.8% of manufacturing sales, 15.4% of manufacturing employment, and 1.7 million workers in 2021, with 42,708 establishments in 2022, creating a broad installed base for durable, cleanable, abrasion-resistant surfaces.

The industrial scenario is shaped by hygiene, productivity, and sustainability. Abrasion resistant coatings are used on conveyors, chutes, mixers, floors, valves, tanks, blades, vehicle surfaces, glass, architectural aluminum, and galvanized steel. In food plants, coatings help resist washdowns, cleaning cycles, and particle abrasion, supporting contamination control and lower maintenance. The broader pressure is also supported by food-system efficiency targets: the UN reported that about 19% of food available to consumers was wasted in 2022, equal to 1.05 billion metric tons, while food loss and waste generated 8–10% of global greenhouse gas emissions.

Demand is being supported by public infrastructure renewal and stricter durability expectations. In the U.S., the Bipartisan Infrastructure Law authorizes about US$1.2 trillion in infrastructure spending, including programs for roads, bridges, ports, rail and water systems, while the FHWA Bridge Formula Program is designed to replace, rehabilitate, preserve, protect and construct highway bridges. In Europe, the Net-Zero Industry Act targets EU clean-technology manufacturing capacity of at least 40% of annual deployment needs by 2030, supporting advanced coatings for renewable, battery, hydrogen and industrial equipment.

Environmental regulation is also reshaping product development. The U.S. EPA finalized enforceable drinking-water limits of 4.0 ppt for PFOA and PFOS, while the EU Ecolabel for paints and varnishes covers decorative paints, varnishes, performance coatings and water-based aerosol spray paints, emphasizing reduced hazardous substances, lower VOCs and high performance. This is pushing suppliers toward low-VOC, powder, waterborne and PFAS-free abrasion-resistant technologies.

3M Company remains relevant through abrasion-resistant films and automotive/architectural protection systems. In 2025, 3M’s Safety & Security Window Film Safety S70 technical sheet described a 7-mil optically clear, shatter-resistant and abrasion-resistant film, while its Ultra S800 sheet specified an 8-mil abrasion-resistant film for interior windows and doors. 3M’s October 2025 Crystalline automotive film bulletin also described multilayered optical films with an abrasion-resistant coating.

Key Takeaways

- Abrasion Resistant Coatings Market size is expected to be worth around USD 24.6 Billion by 2035, from USD 12.4 Billion in 2025, growing at a CAGR of 7.1%.

- Metal/Ceramic held a dominant market position, capturing more than a 62.9% share.

- Oil & Gas held a dominant market position, capturing more than a 23.6% share.

- Asia-Pacific region holds a leading position in the moisture curing adhesives market, accounting for a dominant 43.7% share with a market value of around USD 5.4 billion.

By Type Analysis

Metal/Ceramic coatings lead with 62.9% driven by high durability and strong resistance in heavy-duty use

In 2025, Metal/Ceramic held a dominant market position, capturing more than a 62.9% share. This strong hold comes from their ability to handle extreme wear, high temperatures, and harsh operating conditions better than most other coating types. Industries like mining, oil & gas, power generation, and manufacturing rely heavily on these coatings to protect equipment from constant friction and corrosion. Metal and ceramic-based coatings are widely used on machinery parts, pipelines, and industrial tools because they extend service life and reduce maintenance needs. Their performance in tough environments makes them a preferred choice, even if the initial cost is slightly higher.

By End-Use Analysis

Oil & Gas leads with 23.6% driven by harsh operating conditions and high equipment wear

In 2025, Oil & Gas held a dominant market position, capturing more than a 23.6% share. This strong presence is mainly due to the tough environments in which this industry operates. Equipment used in oil drilling, pipelines, and refineries is constantly exposed to sand, chemicals, pressure, and extreme temperatures. Because of this, abrasion resistant coatings are widely used to protect metal surfaces from damage and extend the life of critical assets. These coatings help reduce frequent repairs and downtime, which is very important in an industry where operational delays can be costly.

Key Market Segments

By Type

- Metal/Ceramic

- Oxide

- Carbide

- Nitride

- Others

- Polymer

- Epoxy

- Polyurethane

- Fluoropolymer

- Polyester

- Others

By End-Use

- Power Generation

- Oil & Gas

- Transportation

- Marine

- Mining

- Construction

- Others

Emerging Trends

Shift Toward High-Durability Coatings to Reduce Food Processing Losses

One of the latest trends in abrasion resistant coatings is the growing shift toward high-durability and long-life coatings in food processing equipment. A large portion of food loss is still linked to poor handling, damaged machinery, and inefficient processing systems. According to global estimates, nearly one-third of food produced worldwide is lost or wasted, which equals hundreds of millions of tonnes every year

In 2025–2026, food processing companies are increasingly adopting advanced abrasion resistant coatings on conveyors, mixers, and pipelines to reduce wear and avoid contamination. When surfaces wear out, they create rough edges that trap food particles, leading to hygiene issues and product loss. Governments and global bodies are also pushing for better food handling practices under sustainability goals like SDG 12.3, which focuses on reducing food waste.

Increasing Use of Coatings to Improve Storage and Post-Harvest Efficiency

Another key trend is the rising use of abrasion resistant coatings in storage and post-harvest systems. A significant share of food losses happens after harvest due to poor storage conditions, handling, and transport issues. In many developing regions, post-harvest losses can reach up to 40% during storage and handling stages, especially in grains and perishable products. This highlights the need for better infrastructure and surface protection.

To address this, industries are applying abrasion resistant coatings inside silos, storage bins, and transport systems to reduce friction and material sticking. These coatings help maintain smooth flow, prevent buildup, and reduce contamination risks. Governments and organizations like FAO are encouraging improvements in storage infrastructure to reduce losses and improve food security. By 2026, this trend is becoming more practical, especially in regions investing in modern agricultural systems.

Drivers

Rising Need to Reduce Food Loss During Processing and Transport

One of the key driving factors for abrasion resistant coatings is the growing need to reduce food loss across processing and supply chains. A large amount of food gets wasted due to damage in handling equipment, pipelines, and storage systems where constant friction causes wear and tear. According to the Food and Agriculture Organization, nearly 13% of food is lost between harvest and retail, which equals about 1.3 billion tonnes every year. This loss is not just about food—it also means wasted water, energy, and labor.

To address this, food processing industries are focusing on improving equipment durability. Abrasion resistant coatings are now widely used in mixers, conveyors, silos, and pipelines to reduce surface damage and contamination risks. Governments are also supporting this shift under global targets like SDG 12.3, which aims to cut food waste by half by 2030. In 2025–2026, many food companies are upgrading their infrastructure with protective coatings to ensure smoother operations and less product loss.

Increasing Focus on Hygiene and Equipment Life in Food Industries

Another major driver is the rising focus on hygiene and longer equipment life in food manufacturing. When surfaces wear out, they can develop cracks and rough areas where bacteria can grow, leading to contamination risks. According to the United Nations Environment Programme, about 19% of food available to consumers is wasted globally, with a large share linked to quality and handling issues.

To improve food safety, industries are investing in abrasion resistant coatings that keep surfaces smooth and easy to clean. These coatings help reduce buildup, prevent corrosion, and maintain hygienic conditions in processing plants. Governments are also tightening food safety regulations, encouraging companies to adopt better materials and technologies. By 2026, food manufacturers are increasingly choosing coatings that not only protect equipment but also support strict hygiene standards.

Restraints

High Cost of Maintenance and Replacement Limits Adoption

One of the biggest restraining factors for abrasion resistant coatings is the high cost involved in maintenance, reapplication, and replacement over time. These coatings are designed to protect equipment, but in industries like food processing, constant friction, cleaning, and chemical exposure still wear them down. This creates a recurring cost burden for companies. The challenge becomes more visible when we look at how much food is already lost due to inefficiencies. According to the Food and Agriculture Organization, nearly 1.3 billion tonnes of food are lost or wasted every year, which is about one-third of total global food production.

To reduce such losses, industries invest in better equipment and coatings, but the high upfront and lifecycle costs often slow down adoption. In 2025–2026, many small and mid-sized food processors still hesitate to use advanced coatings because they require periodic reapplication and skilled handling. Government programs under sustainability goals like SDG 12 encourage reducing food loss, but they do not always cover the cost burden faced by industries.

Performance Degradation in Harsh Cleaning and Food Environments

Another key restraint is the gradual performance loss of coatings in real-world food processing conditions. Food industries require frequent cleaning using water, chemicals, and high-pressure systems to maintain hygiene. Over time, this cleaning process reduces the effectiveness of abrasion resistant coatings, leading to surface damage and contamination risks. Studies show that in developing regions, more than 40% of food losses occur during post-harvest and processing stages, often linked to poor handling and infrastructure issues.

This puts pressure on coatings to perform consistently in demanding environments, which is not always easy. If coatings degrade quickly, they fail to protect equipment, leading to higher wear and possible food contamination. Governments and food safety authorities are also tightening hygiene standards, which means coatings must meet strict durability and safety requirements.

Opportunity

Growing Investment in Food Processing Infrastructure Creating New Opportunities

One major growth opportunity for abrasion resistant coatings is the increasing investment in food processing and handling infrastructure across the world. A large amount of food is still lost due to damage in equipment, pipelines, and storage systems. According to the Food and Agriculture Organization, about 13.3% of global food production—around 1.31 billion tonnes—is lost between harvest and retail. This clearly shows the need for stronger, more durable systems that can handle food without causing damage or contamination.

As governments and industries work toward reducing these losses, they are investing in better processing equipment, storage units, and transportation systems. Programs linked to global goals like SDG 12.3 are encouraging countries to upgrade infrastructure and reduce waste. In 2025–2026, food companies are increasingly using abrasion resistant coatings on conveyors, mixers, silos, and pipelines to reduce wear and improve efficiency. These coatings help equipment last longer, reduce breakdowns, and maintain smooth operations.

Rising Focus on Reducing Food Waste and Improving Efficiency

Another strong opportunity comes from the global push to reduce food waste and improve supply chain efficiency. The United Nations Environment Programme reported that around 1.05 billion tonnes of food were wasted in 2022, which is nearly 19% of food available to consumers. This massive waste is pushing industries to adopt better technologies that can protect food quality during processing and transport.

Abrasion resistant coatings are becoming more important as they help maintain clean, smooth surfaces that reduce contamination and product loss. Governments are also encouraging industries to adopt efficient and sustainable systems through environmental policies and food safety regulations. In 2026, food manufacturers are focusing more on reducing waste not just at the consumer level, but also during production and handling. Coatings that reduce equipment wear and improve hygiene directly support this goal.

Regional Insights

Asia-Pacific dominates with 43.7% (USD 5.4 Bn) driven by rapid industrial growth and strong packaging demand

The Asia-Pacific region holds a leading position in the moisture curing adhesives market, accounting for a dominant 43.7% share with a market value of around USD 5.4 billion. This strong presence is mainly supported by rapid industrialization, growing construction activity, and the expanding packaging sector across countries like China, India, Indonesia, and Southeast Asia.

The region benefits from a large manufacturing base and increasing demand from automotive, electronics, and infrastructure industries, which heavily rely on high-performance adhesive solutions. In 2025, Asia-Pacific continued to show strong consumption patterns, supported by the growth of end-use sectors and rising urban development projects.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

3M Company remains a strong player in the moisture curing adhesives market through its diversified industrial adhesives and sealants portfolio. In 2025, the company reported USD 24.9 billion in total sales, with steady 1.5% annual growth and operating margins near 18.6%. Its adhesive technologies are widely used across automotive, construction, and packaging sectors. With operations in 70+ countries and thousands of bonding solutions, 3M benefits from scale, innovation, and consistent demand across industrial and consumer applications.

Arkema Group is a major contributor to the moisture curing adhesives segment through its Bostik division, which focuses on advanced bonding solutions. The company reported approximately €9.5 billion in revenue in 2024 and operates in 55 countries with over 21,150 employees. Arkema also runs 17 research centers and 157 production sites, supporting innovation in high-performance adhesives.

Top Key Players Outlook

- 3M Company

- Akzo Nobel N.V.

- Arkema Group

- ASB Industries

- Bodycote

- EM Coatings

- Hardide Coatings

- Jotun

- NEI Corporation

- PPG Industries

- Praxair S.T. Technology, Inc.

- SDC Technologies

Recent Industry Developments

Moving into 2026, Hardide Coatings continues to show strong momentum, with Q1 FY2026 revenue reaching £1.8 million, nearly 40% higher year-on-year, along with new order intake of around £1.75 million from a major energy client.

In 2025, Arkema Group continued to play a strong role in the abrasion resistant coatings space through its Coating Solutions and Advanced Materials segments, which are widely used in industrial, automotive, and infrastructure applications. The company reported total revenue of around €9.1 billion in 2025, with an EBITDA of €1.25 billion and a margin of 13.8%, showing stable performance despite a challenging market environment

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 12.4 Bn |

| Forecast Revenue (2035) | USD 24.6 Bn |

| CAGR (2026-2035) | 7.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Metal/Ceramic, Polymer), By End-Use (Power Generation, Oil And Gas, Transportation, Marine, Mining, Construction, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | 3M Company, Akzo Nobel N.V., Arkema Group, ASB Industries, Bodycote, EM Coatings, Hardide Coatings, Jotun, NEI Corporation, PPG Industries, Praxair S.T. Technology, Inc., SDC Technologies |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |