Quick Navigation

Report Overview

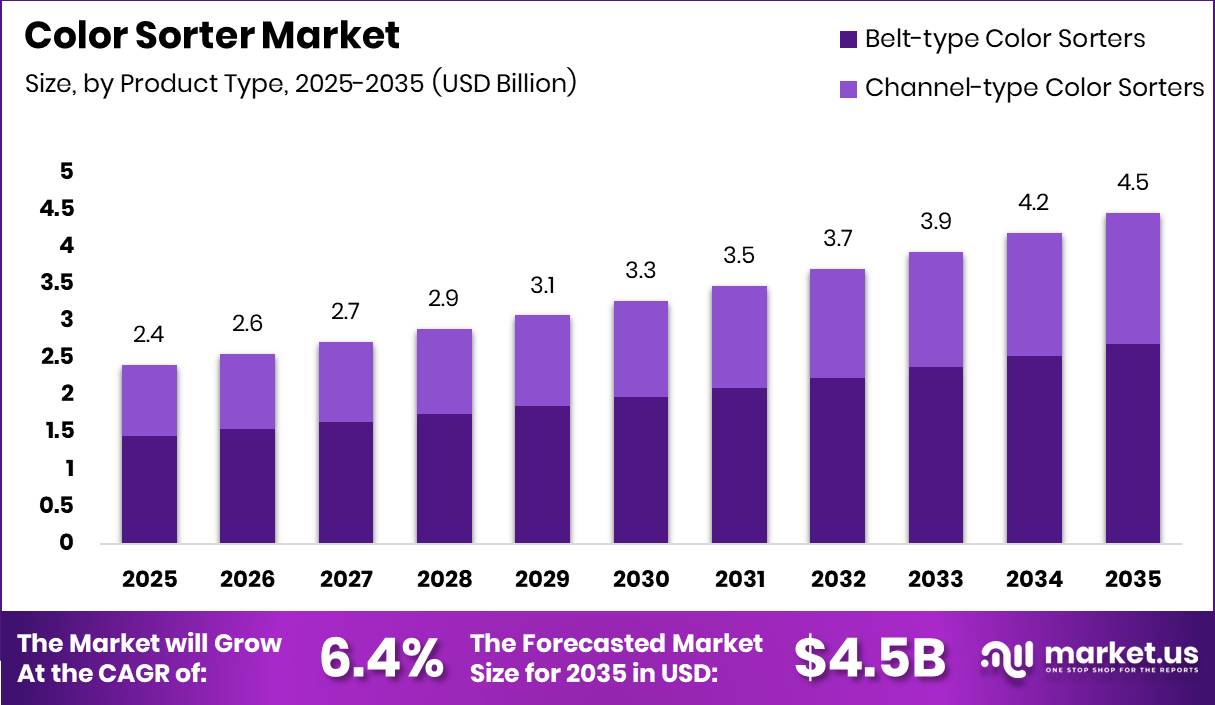

Global Color Sorter Market size is expected to be worth around USD 4.5 Billion by 2035 from USD 2.4 Billion in 2025, growing at a CAGR of 4.5% during the forecast period 2026 to 2035.

The color sorter market covers optical and sensor-based machines that separate products by color, shape, or spectral signature across food, agriculture, plastics, recycling, and mining. Systems range from belt-type and channel-type units to AI-enabled multispectral platforms. Buyers include grain processors, food manufacturers, recycling operators, and mining companies seeking consistent output quality and contaminant removal.

Key Takeaways

- Market size in 2025: USD 2.4 Billion

- Forecast market size by 2035: USD 4.5 Billion

- CAGR (2026 to 2035): 4.5%

- Dominant product type segment: Belt-type Color Sorters with 60.5% share

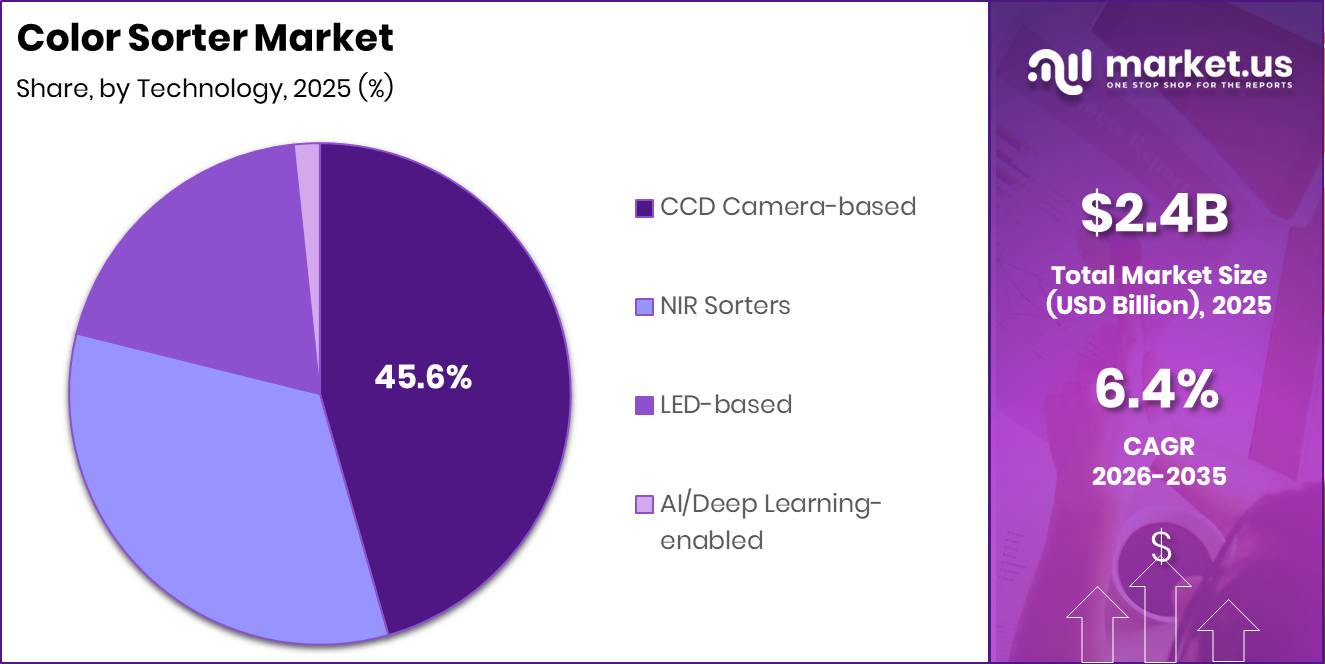

- Dominant technology segment: CCD Camera-based with 45.6% share

- Dominant application segment: Food with 55.6% share

- Dominant capacity segment: Medium Capacity with 50.6% share

- Dominant end-use industry segment: Agriculture with 35.6% share

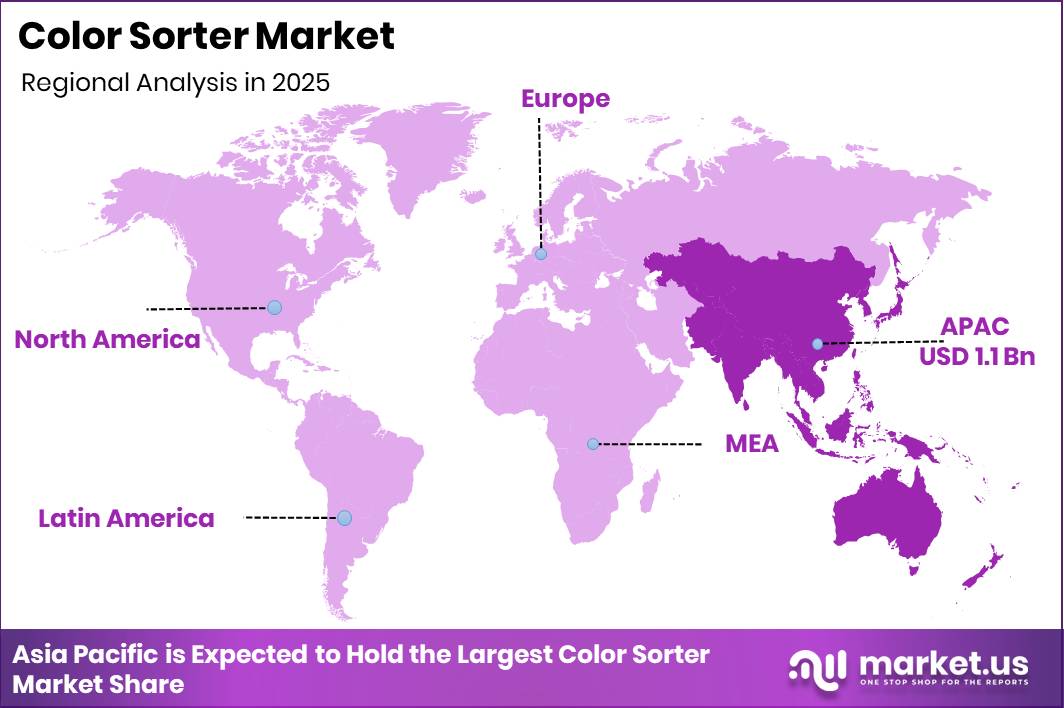

- Dominant region: Asia Pacific with 45.4% share, valued at USD 1.1 Billion

According to the Food and Agriculture Organization, approximately 1.3 billion tonnes of food produced for human consumption are lost or wasted globally each year. This volume represents roughly one-third of total global food production. Color sorting technology directly addresses this loss by removing defective and contaminated product before it enters distribution, making sorters a measurable tool for food recovery, not just quality control.

Food waste also generates approximately 3.3 billion tonnes of CO₂-equivalent greenhouse gas emissions per year, as reported by the FAO. This environmental cost strengthens the regulatory case for upstream sorting investment across food supply chains. Consequently, processors in export-oriented markets face compounding pressure from both food safety regulators and sustainability mandates, raising the priority of optical sorting within capital planning cycles.

Product Type Analysis

Belt-type Color Sorters dominates with 60.5% due to broad compatibility across food processing lines.

In 2025, Belt-type Color Sorters held a dominant market position in the By Product Type segment of the Color Sorter Market, with a 60.5% share. Belt-fed systems accommodate wet, sticky, and fragile materials that channel-type units cannot process reliably. This structural advantage keeps belt-type sorters as the default specification for food processors handling produce, frozen goods, and mixed grain streams.

Channel-type Color Sorters serve processors requiring high-throughput separation of free-flowing dry materials such as rice, pulses, and coffee. Their high-speed chute design supports faster feed rates per lane than belt alternatives. This makes channel-type units the preferred choice in large-scale grain and seed processing facilities where throughput volume outweighs flexibility requirements. In July 2025, Key Technology launched a belt-fed COMPASS optical sorter designed for wet, sticky, and fragile food products, expanding competitive options in the belt-type segment.

Technology Analysis

CCD Camera-based dominates with 45.6% due to proven accuracy and established integration across processing lines.

In 2025, CCD Camera-based technology held a dominant market position in the By Technology segment of the Color Sorter Market, with a 45.6% share. CCD systems deliver high-resolution color discrimination at commercially viable price points, giving processors a reliable entry into optical sorting without requiring specialist calibration expertise. This cost-performance balance keeps CCD the baseline specification across mid-tier food and grain processors globally.

NIR Sorters extend detection capability beyond visible color to identify material composition differences invisible to standard cameras. NIR is the preferred upgrade path for processors separating plastics by polymer type or detecting internal defects in food products. This technology unlocks sorting precision that color-only systems cannot match, making NIR a key differentiator for processors competing on export-grade output standards.

LED-based sorters offer lower energy consumption and longer component lifespan than earlier lamp-based illumination systems. Processors operating at scale benefit directly from reduced maintenance cycles and more stable illumination consistency across shifts. AI and Deep Learning-enabled systems represent the fastest-evolving sub-segment, using trained models to adapt detection thresholds in real time, while the remaining share is distributed across these three technology types.

Application Analysis

Food dominates with 55.6% due to strict quality and safety requirements across grain and produce processing.

In 2025, Food held a dominant market position in the By Application segment of the Color Sorter Market, with a 55.6% share. Data from the FAO shows industrialized countries lose or waste approximately 670 million tonnes of food annually, while developing countries lose or waste approximately 630 million tonnes. This scale of loss across both market tiers creates consistent capital justification for sorting technology at the processor level, regardless of geography.

Plastics sorting benefits directly from rising recycling infrastructure investment in North America and Europe. As per our research, plastics generation in the United States reached 35.7 million tons in municipal solid waste. This volume creates a measurable feedstock challenge for recyclers, where color sorters improve polymer separation accuracy and increase recovered material value, supporting the business case for optical sorting investment in waste management facilities.

Recycling applications are expanding as material recovery targets tighten globally. Data from the EPA shows PET plastic bottles and jars achieved a recycling rate of only 29.1% in the United States, signaling that the majority of this material stream remains unsorted and unrecovered. This gap represents a direct addressable volume for sorter vendors targeting the recycling sector. Mining and Others hold the remaining application share collectively.

Capacity Analysis

Medium Capacity dominates with 50.6% due to fit across the majority of commercial processing facilities.

In 2025, Medium Capacity held a dominant market position in the By Capacity segment of the Color Sorter Market, with a 50.6% share. Mid-scale processors represent the broadest buyer segment globally, operating facilities too large for entry-level units but unwilling to commit to high-capacity infrastructure without guaranteed volume. Medium-capacity sorters occupy this gap by delivering industrial-grade throughput within manageable capital and footprint constraints.

Low Capacity sorters serve smallholder cooperatives, artisan processors, and emerging-market buyers entering optical sorting for the first time. Their lower price threshold reduces the adoption barrier in markets where processing volumes fluctuate seasonally. High Capacity systems target large-scale commodity processors where throughput per hour directly determines return on capital, and these units hold the remaining capacity share collectively.

End-Use Analysis

Agriculture dominates with 35.6% due to its role as the primary feedstock source for color sorter applications.

In 2025, Agriculture held a dominant market position in the By End-Use Industry segment of the Color Sorter Market, with a 35.6% share. Figures from UNEP show that food lost or wasted consumes approximately 1.4 billion hectares of agricultural land annually, equivalent to roughly 28% of the world’s agricultural area. This land productivity loss reinforces the commercial urgency for precision sorting at the farm-gate and primary processing stages, where defect removal protects both yield value and downstream quality.

Food Processing represents the second-largest end-use segment, covering manufacturers converting raw agricultural inputs into packaged or exported products. This segment applies sorters at multiple points in the production line to meet branded product specifications and export compliance standards. Recycling, Mining, Plastics, and Others hold the remaining end-use share collectively, reflecting the market’s continued expansion beyond its agricultural origins.

Key Market Segments

By Product Type

- Belt-type Color Sorters

- Channel-type Color Sorters

By Technology

- CCD Camera-based

- NIR Sorters

- LED-based

- AI/Deep Learning-enabled

By Application

- Food

- Rice

- Wheat

- Pulses

- Nuts

- Fruits and Vegetables

- Plastics

- Recycling

- Mining

- Others

By Capacity

- Low Capacity

- Medium Capacity

- High Capacity

By End-Use Industry

- Agriculture

- Food Processing

- Recycling

- Mining

- Plastics

- Others

Regional Analysis

Asia Pacific Dominates the Color Sorter Market with a Market Share of 45.4%, Valued at USD 1.1 Billion

Asia Pacific holds the largest regional share at 45.4%, valued at USD 1.1 Billion, driven by the concentration of global grain, rice, and pulse processing in China, India, and Southeast Asia. These markets operate large-scale commodity processing infrastructure where consistent export-grade quality is directly tied to contract retention. This structural demand keeps capital investment in optical sorting equipment active across the region’s processing hubs.

North America represents a high-value regional market shaped by food safety compliance requirements and labor cost dynamics in food manufacturing. Based on FDA data, food waste in the United States is estimated at 30% to 40% of the food supply, and the country generated more than 63 million tons of food waste in commercial, institutional, and residential sectors in 2018. This waste intensity creates sustained demand for sorting solutions that prevent defective product from entering distribution networks.

Europe operates under a tightening regulatory framework that directly affects sorter adoption timelines and vendor qualification standards. Data from the European Commission shows that more than 58 million tonnes of food waste are generated annually in the EU, equal to 129 kg per inhabitant, with households accounting for 53% of that total. This waste profile, combined with EU circular economy targets, pushes processors to invest in sorting systems that improve both output quality and material recovery rates.

Latin America represents a structurally underserved regional market with a growing base of grain and coffee processors seeking quality certification for export. Brazil and Mexico anchor regional sorter demand through their commodity export volumes. However, high buyer capital expenditure hurdles and fragmented processing infrastructure slow adoption relative to the region’s actual addressable volume, creating a delayed but real entry window for vendors offering financing-linked or lease-based equipment models.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Drivers

Export-grade quality requirements for grains, pulses, nuts, seeds, tea, coffee, and dehydrated foods are expanding the commercial case for color sorters across multiple agricultural value chains. The FDA traceability framework reinforces this pressure by covering high-risk food categories including nut butters, fresh produce, cheeses, and seafood, requiring upstream processors to document stricter sorting discipline before products enter branded, private-label, or export channels.

Adoption is strongest in India, China, Southeast Asia, Turkey, Brazil, and the United States, where processors compete on reject minimization and shipment consistency. Once export premiums or avoided rejections exceed the combined cost of compressed air, maintenance, and financing, the sorter shifts from optional equipment to core plant infrastructure. This conversion dynamic is what makes food and nut-grain export quality a sustained demand engine rather than a cyclical one.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food safety compliance automation | +1.4% | North America core, EU, Japan, Korea, export-oriented APAC | Short term (≤ 2 years) |

| Labor cost substitution in sorting lines | +1.1% | North America core, EU, Gulf food hubs, China coastal, Australia | Short term (≤ 2 years) |

| Processed food and nut-grain export quality | +1.3% | India, China, Southeast Asia, Turkey, U.S., Brazil | Medium term (2-4 years) |

| AI and multispectral upgrade cycle | +0.9% | EU, North America, China, Japan premium lines | Medium term (2-4 years) |

| Plastics recycling and packaging circularity | +0.8% | EU core, U.K., North America selective, advanced APAC | Medium term (2-4 years) |

| Yield recovery and waste monetization | +0.7% | Global spill-over, strongest in large processors and packhouses | Long term (≥ 4 years) |

Restraints

Regulatory complexity slows color sorter adoption not because the technology is unwanted, but because food and export-chain buyers must verify that machinery, food-contact materials, and traceability processes remain compliant as plants modernize. The 2025 tightening of EU food-contact and recycled-plastics rules, including Regulation (EU) 2025/351 and pre-existing traceability obligations under Regulation (EU) 2022/1616, adds documentation and validation requirements around equipment interfaces, material declarations, and quality-control records.

These compliance demands are manageable for large multinationals but carry meaningful costs for smaller exporters. The result is not project cancellation but slower approvals, narrower approved-vendor lists, and a preference for established OEMs over challengers. This dynamic raises market-entry friction, dampens price competition, and delays conversion across EU, North American, and export-oriented Asian facilities, warranting an estimated 0.6 percentage-point deduction to CAGR over a 2 to 4 year horizon.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensor & camera cost inflation | -1.1% | Global; NA, EU, China-linked APAC | Short term (≤ 2 years) |

| High buyer CapEx hurdle | -0.9% | India, SEA, LATAM, Africa | Short term (≤ 2 years) |

| Tariff and localization friction | -0.8% | North America core, EU, APAC corridors | Medium term (2-4 years) |

| Integration skill shortage | -0.7% | North America, EU, emerging APAC | Medium term (2-4 years) |

| Compliance and validation burden | -0.6% | EU, North America, export-led APAC | Medium term (2-4 years) |

| Volatile food processor margins | -0.5% | Global; grain, nut, rice, pulses belts | Short term (≤ 2 years) |

Challenges

Color sorters operate across end markets where grading norms, export specifications, food safety tolerances, and recycled material purity expectations continue to tighten. Regulators and buyers are demanding better contaminant control, traceability, and standardized output quality across both agriculture and plastics recycling. In agriculture, rising trade-linked quality expectations increase pressure on processors to separate subtle visual defects more consistently than previous equipment generations allowed.

In plastics recycling, higher-quality sorted streams remain central to circular economy progress and recycled content execution. This evolving compliance environment creates a moving technical target for sorter vendors, who must repeatedly refine optical sensitivity, software recipes, and validation protocols to match changing downstream requirements. As a result, regulation and standards evolution functions as an ongoing adaptation cost for vendors rather than a one-time barrier to entry.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Skilled vision labor gap | -1.1% | APAC manufacturing hubs, North America, EU | Long term (≥ 4 years) |

| Sensor sourcing instability | -0.8% | APAC logistics corridors, EU industrial belt, US | Medium term (2-4 years) |

| Legacy line integration complexity | -1.0% | Asia grain belts, EU processors, emerging markets | Long term (≥ 4 years) |

| ROI variability by crop mix | -0.7% | India, Southeast Asia, Latin America, Africa | Medium term (2-4 years) |

| Digital uptime dependency | -0.6% | Smart plants in APAC, EU, North America | Medium term (2-4 years) |

| Quality compliance evolution | -0.5% | EU regulatory hubs, North America, export-oriented APAC | Long term (≥ 4 years) |

Opportunities

Retrofitting the global installed base of legacy color sorters with AI vision modules, cloud diagnostics, recipe libraries, and predictive maintenance subscriptions creates a recurring revenue layer on existing hardware. This model targets mid-tier processors that cannot justify complete line replacement but can justify retrofit tickets at roughly 15% to 25% of new-machine capital cost, provided payback stays under 24 months.

Attaching an annual software-and-service fee of 6% to 10% to only 15% to 20% of the addressable installed base could lift segment EBITDA margins by roughly 250 to 450 basis points. This same model could lower customer downtime by an estimated 10% to 18% and reduce field-service cost per unit by 12% to 20%. This means the white space in color sorting is not only new machine sales but monetization of the existing equipment base through software-led service contracts.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Mid-tier SaaS retrofits | +1.4% | North America, EU, India, ASEAN | Short term (≤ 2 years) |

| Emerging-market grain clusters | +2.2% | India, Sub-Saharan Africa, SE Asia | Medium term (2-4 years) |

| Recycling-grade expansion | +1.8% | EU, North America, Japan, Korea | Short term (≤ 2 years) |

| Protein & specialty crops | +1.6% | North America, EU, Australia, India | Medium term (2-4 years) |

| Outcome-based pricing | +1.1% | Global installed base | Short term (≤ 2 years) |

| Roll-up of local OEMs | +2.0% | India, China, Turkey, Brazil | Long term (≥ 4 years) |

Key Company Insights

Bühler Group brings 160 years of grain and food processing expertise to its SORTEX optical sorting business, supported by a service network covering more than 140 countries. In May 2025, the company launched the SORTEX AI700, an AI-powered sorter using deep-learning for impurity detection and allergen removal in oat processing. This global service reach creates a structural advantage that challengers with regional footprints cannot quickly replicate.

Tomra Systems ASA reported 2025 revenue of €1.32 billion and operates more than 91,900 installed reverse vending machines globally, according to its 2025 Annual Report. In September 2025, the company acquired C&C Consolidated Holdings (CLYNK), strengthening its collection and sorting solutions portfolio in North America. As per our research, approximately 27 million tons of plastic were landfilled in the United States alone, signaling that Tomra’s expanded recycling infrastructure directly addresses a large unrecovered material volume.

Key Players

- Bühler Group

- Satake Corporation

- Tomra Systems ASA

- Key Technology

- Hefei Meyer Optoelectronic Technology

- Anhui Jiexun Optoelectronic Technology

- Orange Sorting Machines

- Fowler Westrup

- Agrosaw

- SEA Optical Sorters

- Tomra Food

- Westrup A/S

- Anzai Manufacturing

- ArrowCorp Inc.

- GREEFA

- Other Key Players

Recent Developments

- June 2025 – Satake Corporation launched Pellet Sorter II, a new optical sorter for plastic pellets featuring 4K cameras and intelligent software for detecting speck damage and discoloration.

- October 2025 – Aegis Sortation launched TetraSort, a next-generation modular steerable wheel sorter engineered for high-speed logistics and parcel sorting applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.4 Billion |

| Forecast Revenue (2035) | USD 4.5 Billion |

| CAGR (2026-2035) | 4.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Belt-type Color Sorters, Channel-type Color Sorters); By Technology (CCD Camera-based, NIR Sorters, LED-based, AI/Deep Learning-enabled); By Application (Food [Rice, Wheat, Pulses, Nuts, Fruits and Vegetables], Plastics, Recycling, Mining, Others); By Capacity (Low Capacity, Medium Capacity, High Capacity); By End-Use Industry (Agriculture, Food Processing, Recycling, Mining, Plastics, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Bühler Group, Satake Corporation, Tomra Systems ASA, Key Technology, Hefei Meyer Optoelectronic Technology, Anhui Jiexun Optoelectronic Technology, Orange Sorting Machines, Fowler Westrup, Agrosaw, SEA Optical Sorters, Tomra Food, Westrup A/S, Anzai Manufacturing, ArrowCorp Inc., GREEFA, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |