Quick Navigation

Report Overview

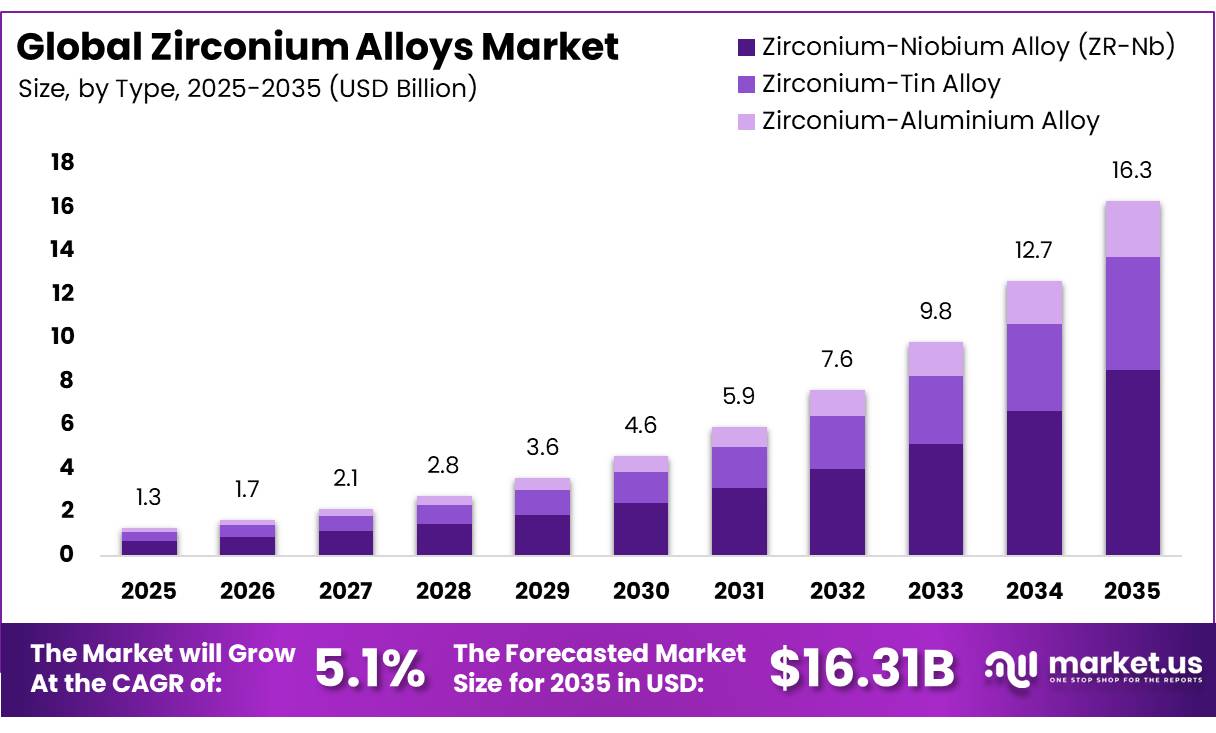

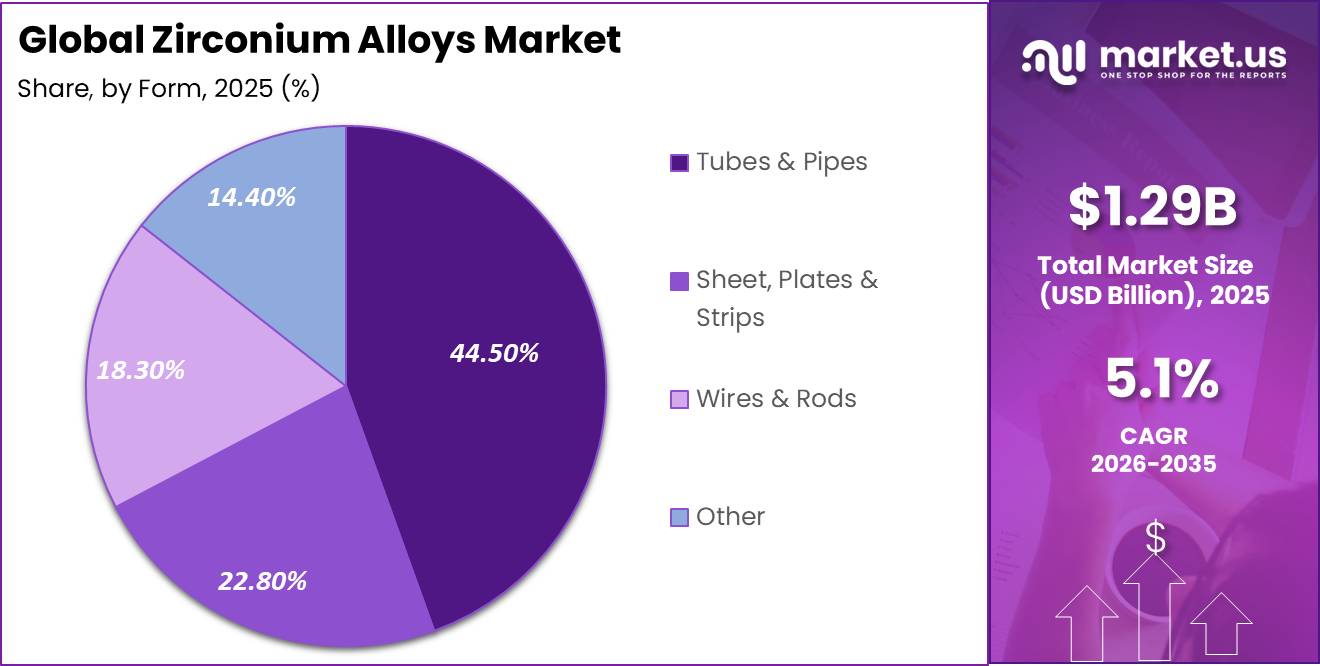

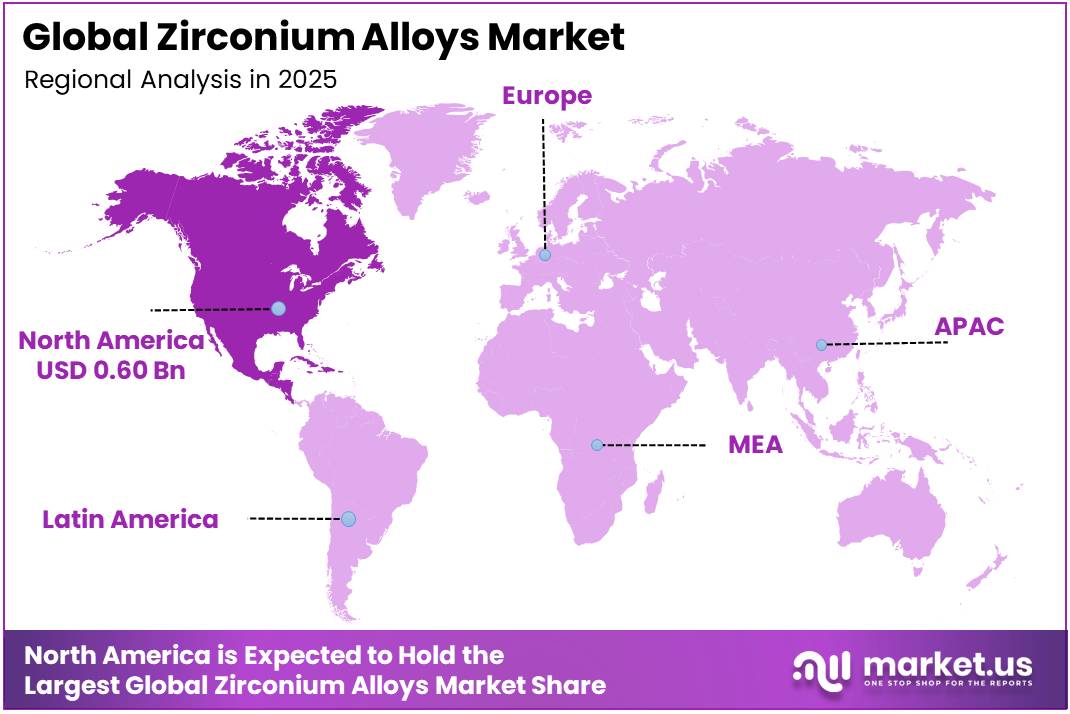

In 2025, the Global Zirconium Alloys Market was valued at USD 1.3 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.1%, reaching about USD 16.3 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 46.5% share, holding USD 0.60 billion in revenue.

The zirconium alloys market is a high performance manufacturing segment focused on zirconium niobium, zirconium tin, and zirconium aluminium alloys made into tubes, pipes, sheets, plates, strips, wires, and rods. These alloys are valued where corrosion resistance, neutron transparency, and dimensional stability are critical. World Nuclear Association states that zirconium alloy tubes are the main cladding material for nuclear fuel assemblies, making nuclear power the core demand base.

- The International Atomic Energy Agency (IAEA) Power Reactor Information System showed 417 nuclear power reactors in operation, 379,700 megawatts electric of installed capacity, and 77 reactors under construction as of 7 July 2026. This reactor base supports demand for cladding tubes, structural fuel components, and high specification zirconium alloy products.

Key Takeaways

- The global Zirconium Alloys Market was valued at USD 1.3 billion in 2025.

- The global Market is projected to grow at a CAGR of 5.1% and is estimated to reach USD 16.3 billion by 2035.

- On the basis of Type, Zirconium-Niobium Alloy (Zr-Nb) dominated the market, constituting 52.50% of the total market share.

- Based on Form, Tubes & Pipes led the Zirconium Alloys Market with a substantial market share of 44.50%.

- Based on End User, Nuclear Power held the leading position in the market, comprising 36.60% of the total market share.

- Among the Regions, Asia Pacific was the most dominant region in the Zirconium Alloys Market, accounting for 46.50% of the total global consumption.

Raw material security remains important for producers. The United States Geological Survey (USGS) reported that, in 2025, United States imports of zirconium ores and concentrates were 16,000 metric tons by zirconium dioxide content, while zirconium wrought imports reached 380 metric tons. For 2021 to 2024, zirconium ores and concentrates came mainly from South Africa at 48%, Australia at 35%, and Senegal at 15%, showing concentrated mineral sourcing.

Growth opportunities are supported by reactor life extension, advanced reactors, and local nuclear supply chain programs. On 10 March 2026, the European Commission presented a Small Modular Reactors strategy, stating that European Union Small Modular Reactor capacity could reach between 17 gigawatts and 53 gigawatts by 2050. It also estimated about €241 billion of nuclear investment needs by 2050. These initiatives support long term demand for qualified zirconium alloy manufacturing. In aerospace, defence, chemical processing, and healthcare, demand is more selective, but it supports premium alloy forms where corrosion resistance, biocompatibility, and fabrication quality are required alongside nuclear grade tube demand globally.

Type Analysis

Zirconium-Niobium Alloy dominates with 52.50% due to its strong use in nuclear-grade applications.

In 2025, Zirconium-Niobium Alloy (ZR-Nb) held a dominant market position, capturing more than a 52.50% share of the zirconium alloys market by type. In the June 2025 market view, this segment led because Zirconium-Niobium Alloy is widely preferred in nuclear power applications where corrosion resistance, strength, and stability under demanding operating conditions are important. Its use remained strong in fuel cladding, reactor components, and other high-performance industrial applications that require reliable alloy behavior.

Zirconium-Tin Alloy emerged as the growing segment. Its growth was supported by continued demand in nuclear and industrial uses where durability, fabrication performance, and resistance to harsh environments are important.

Form Analysis

Tubes & Pipes dominate with 44.50% due to their key role in reactor and industrial systems.

In 2025,Tubes & Pipes held a dominant market position, capturing more than a 44.50% share of the zirconium alloys market by form. In the June 2025 market view, this segment led because zirconium alloy tubes and pipes are widely used in nuclear power, chemical processing, and high-performance industrial systems. Their strong demand was supported by corrosion resistance, dimensional stability, and suitability for applications requiring safe material performance under pressure and heat.

Sheet, Plates & Strips emerged as the growing segment. Their growth was supported by rising use in fabrication, structural components, chemical equipment, and specialized manufacturing applications where flat alloy forms are needed for forming, joining, and precision design.

End User Analysis

Nuclear Power dominates with 36.60% due to its strong demand for zirconium alloy components.

In 2025, Nuclear Power held a dominant market position, capturing more than a 36.60% share of the zirconium alloys market by end user. In the June 2025 market view, this segment led because zirconium alloys are widely used in nuclear fuel cladding, reactor assemblies, and related components. Their demand remained strong as nuclear operators required materials with corrosion resistance, strength, and stable performance in high-temperature environments.

Aerospace & defence emerged as the growing segment. Its growth was supported by demand for lightweight, durable, and corrosion-resistant alloy materials used in specialized components where performance, reliability, and material quality are important.

Key Market Segments

By Type

- Zirconium-Niobium Alloy (ZR-Nb)

- Zirconium-Tin Alloy

- Zirconium-Aluminium Alloy

By Form

- Tubes & Pipes

- Sheet, Plates & Strips

- Wires & Rods

- Other

By End User

- Nuclear Power

- Aerspace & defence

- Chemical Processing

- Medical and Healthcare

Driver Analysis

Long-cycle reactor pipeline and replacement fuel backlog

The final driver is the long-duration nature of the installed and emerging reactor base, which converts today’s construction wave into a durable replacement-fuel market rather than a short-cycle capital goods spike. Current world reactor statistics show about 440 operating reactors across 31 countries, generating about 2667 TWh in 2024, while over the last 20 years retirements and start-ups have been broadly balanced; this means new-build activity is adding to an already large installed base that will continue purchasing zirconium alloy components through routine reload cycles. For zirconium alloy suppliers, the installed fleet matters nearly as much as new plants because recurring reload demand is steadier, more forecastable, and usually higher margin after qualification.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nuclear new-build cladding demand expansion | +2.4% | China core, India core, Turkey, Egypt, South Korea, Eastern Europe spill-over | Medium term (2-4 years) |

| Life-extension and higher burnup fuel economics | +1.7% | North America core, EU core, Japan selective, South Korea | Short term (≤ 2 years) |

| Accident-tolerant fuel coatings and premium tube upgrades | +1.3% | US core, France, Central Europe, China pilot programs | Short term (≤ 2 years) |

| Asia-centered conversion and fabrication localization | +1.1% | China core, India, Russia-linked supply chains, Southeast Asia spill-over | Medium term (2-4 years) |

| Hafnium separation and nuclear-grade purity barriers | +0.9% | Global, with strongest effect in North America, EU, China | Long term (≥ 4 years) |

| Long-cycle reactor pipeline and replacement fuel backlog | +0.8% | Asia broad-base, Middle East, UK, Eastern Europe | Long term (≥ 4 years) |

Restraint Analysis

Concentrated zircon mineral supply

In practical terms, this concentration means that any port congestion, mining-license renegotiation, or local environmental enforcement in one of the top four producers can tighten feedstock availability and force alloy processors to pay spot premiums of 8–15% above long-term contract benchmarks, squeezing EBITDA margins by 150–250 basis points on fuel-cladding and chemical-equipment orders.

For utilities and reactor vendors, this raises delivered component costs at exactly the time when regulators and policymakers push for competitive electricity tariffs and low-carbon generation, leading to delayed procurement decisions and more aggressive price negotiation. Over a 2–4 year horizon, this recurring raw-material risk justifies a roughly -2.1 percentage-point drag on zirconium alloys market CAGR as projects are re-phased, safety stocks are raised, and some non-critical applications migrate to alternative alloys where supply is more geographically diversified.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concentrated zircon mineral supply | -2.1% | Australia, South Africa, China, APAC corridors, global importers | Medium term (2-4 years) |

| Nuclear-grade hafnium separation cost burden | -1.6% | North America core, EU, China, Russia-linked supply chains | Long term (≥ 4 years) |

| Nuclear project delay and financing risk | -1.4% | EU, North America, Japan, emerging Middle East | Medium term (2-4 years) |

| Environmental and radiation regulatory tightening | -1.2% | EU core, North America core, select Asian markets | Long term (≥ 4 years) |

| Competing non-nuclear zirconium uses crowding supply | -1.1% | Global ceramics, chemicals, foundry hubs (APAC, EU) | Short term (≤ 2 years) |

| Price volatility and long lead-time inventory risk | -0.9% | Global, with highest impact on smaller processors | Short term (≤ 2 years) |

Opportunity Analysis

Strategic M&A roll-up of dispersed zirconium value-chain assets

If a handful of strategic buyers deploy, for example, USD 1–2 billion of cumulative acquisition capital over the next 8–10 years to assemble portfolios of mines, conversion plants, alloy foundries, and recycling facilities, they could realize synergies from logistics optimization, cross-selling, and unified R&D roadmaps enhancing product differentiation.

Consolidation would also strengthen negotiating power with large nuclear and industrial customers, potentially expanding margins by 200–300 basis points and stabilizing pricing through longer-tenor contracts, thus capturing upside not reflected in current independent-player projections. In aggregate, such a roll-up strategy could add around +0.9 percentage points to market CAGR by 2035, driven not by new end-use growth alone but by improved capital efficiency, margin capture, and accelerated deployment of innovations such as recycling and advanced alloys backed by stronger balance sheets.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Advanced zirconium alloys for aerospace and implants | +1.6% | North America, EU, Japan, APAC high-tech hubs | Medium term (2-4 years) |

| Closed-loop zirconium recycling and circular feedstock | +1.4% | EU core, North America core, China, Japan | Medium term (2-4 years) |

| Service-centric nuclear alloy lifecycle and performance contracts | +1.2% | US, France, UK, South Korea, China pilot | Short term (≤ 2 years) |

| Regionalized zirconium alloy hubs for SMRs and AMRs | +1.1% | APAC emerging (India, ASEAN), Middle East, Eastern Europe | Long term (≥ 4 years) |

| Specialty zirconium alloys for electronics, displays, and hydrogen | +1.0% | APAC electronics corridors, EU, US West Coast | Medium term (2-4 years) |

| Strategic M&A roll-up of dispersed zirconium value-chain assets | +0.9% | Global, focus on Australia, South Africa, EU, US | Long term (≥ 4 years) |

Challenges Analysis

Multi-stage alloy production complexity

Multi-stage alloy production complexity imposes continuous friction because zirconium alloy manufacturing spans at least five major stages—mining and concentration of heavy minerals, separation of zircon, separation of zirconium from hafnium and production of sponge, production of alloy ingots, and production of tubes—with each stage often located at separate facilities and frequently in different countries, creating cumulative operational risk and longer cycle times.

On an operational level, the total lead time from ore extraction to nuclear-grade tubes can easily reach 6–12 months, with each hand-off introducing potential delays of 5–15 days due to scheduling, transport, and quality checks, and yield losses at each stage compounding into non-trivial scrap and rework costs. This complexity forces firms to carry higher work-in-progress inventories, tying up working capital equal to several months of sales and raising interest and storage costs; it also amplifies the impact of any disruption in one stage, as downstream plants may run underutilized while upstream bottlenecks are cleared.

Strategically, companies must invest in better integration, digital tracking, and process optimization across this chain, but even with incremental improvements, multi-stage complexity is likely to impose about -1.5 percentage points of friction drag on potential CAGR over the long term, because the physics and chemistry of zirconium purification and alloying cannot be radically simplified without compromising nuclear-grade properties.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Multi-stage alloy production complexity | -1.5% | Global production hubs, APAC processing corridors | Long term (≥ 4 years) |

| Concentrated logistics and port exposure | -1.3% | Australia, South Africa, China, global importers | Medium term (2-4 years) |

| Nuclear-grade QA and certification load | -1.1% | North America, EU, Russia-linked, Asia nuclear hubs | Long term (≥ 4 years) |

| Specialized metallurgical and nuclear talent gap | -1.0% | EU, North America, Japan, emerging APAC | Long term (≥ 4 years) |

| Environmental footprint and process-intensity pressure | -0.9% | EU regulatory hubs, North America, Australia, South Africa | Medium term (2-4 years) |

| Demand forecasting and product-mix complexity | -0.8% | Global multi-industry suppliers | Short term (≤ 2 years) |

Geopolitical Impact Analysis

Nuclear Fuel Localization and Strategic Mineral Security Are Reshaping Zirconium Alloys Supply

The zirconium alloys market is increasingly influenced by geopolitical shifts because its major demand is connected with nuclear power, aerospace and defence, chemical processing, and high-grade manufacturing supply chains. In January 2026, the United States Department of Energy announced US$2.7 billion to strengthen domestic enrichment services over the next ten years, including low-enriched uranium and high-assay low-enriched uranium supply.

Trade restrictions are also changing procurement strategies. The United States Nuclear Regulatory Commission stated that the Prohibiting Russian Uranium Imports Act was signed on 13 May 2024, bans certain uranium products from Russia, and terminates on 31 December 2040. The ban became effective on 11 August 2024, while waivers must end no later than 1 January 2028. Such policies are pushing nuclear supply chains toward trusted suppliers, longer contracts, and stronger material traceability.

- The United States Geological Survey reported world zirconium reserves of more than 70,000 thousand metric tons by zirconium dioxide content, with Australia listed at 55,000 thousand metric tons and South Africa at 5,900 thousand metric tons. This shows that zirconium resource access is not evenly distributed, making mining policy, logistics, and export stability important for alloy manufacturers.

In Europe, nuclear policy is also creating long-term supply opportunities. The European Commission stated that European Union nuclear installed capacity is projected to grow from 98 gigawatts electric in 2025 to around 109 gigawatts electric by 2050. It also noted that decarbonised sources are expected to generate over 90% of European Union electricity in 2040. These trends support demand for certified zirconium alloy tubes, pipes, sheets, and rods, while geopolitical uncertainty encourages regional qualification and diversified sourcing.

Regional Analysis

In 2025, Asia Pacific dominated the global Zirconium Alloys Market, accounting for approximately 46.5% of total global consumption, thanks to its large and rapidly expanding nuclear energy fleet, deeply integrated industrial manufacturing ecosystem, and high concentration of aerospace and defense production.

Similarly Similarly, Japan and South Korea make significant contributions through advanced manufacturing capabilities and the continued operation of their existing nuclear fleets, particularly in the production of high-grade zirconium alloy tubes and precision-engineered components for nuclear and industrial use. India is emerging as an increasingly important contributor, with its domestic nuclear expansion program, growing aerospace and defense sector, and expanding chemical processing industry all driving up zirconium alloy consumption year after year.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

To remain competitive in an increasingly demanding global market, zirconium alloy manufacturers focus on improving technological differentiation, production scale efficiency, and supply chain integration. Continuous material innovation is a top priority, including the creation of advanced zirconium alloy grades with improved corrosion resistance, higher radiation tolerance, and increased mechanical strength to meet the changing performance requirements of next-generation nuclear reactors and high-performance industrial applications.

Framatome, TVEL Fuel Company (Rosatom), Leading manufacturers benefit from vertical integration with zircon sand mining operations and hafnium separation facilities, which helps them secure raw material stability and improve cost control in the face of volatile input prices and geographically concentrated supply sources. Strategic capacity expansion, particularly in Asia Pacific and North America, enables alignment with concentrated demand in the nuclear energy, aerospace and defense, and chemical processing industries.

Market Key Players

- Framatome (formerly Areva NP)

- ATI Inc. (Allegheny Technologies)

- State Nuclear Baoti Zirconium Industry Co. (SNZ)

- Westinghouse Electric Company

- Orano (formerly Areva Mines)

- Chepetsky Mechanical Plant (CMP JSC)

- CNNC Jinghuan Zirconium Industry Co., Ltd.

- Liaoning Huagao New Material Co., Ltd.

- Nuclear Fuel Complex (NFC)

- Luxfer Group

- VDM Metals GmbH

- Guangdong Orient Zirconic Ind. Sci. & Tech.

- American Elements

- C. Starck (Materion)

- Aviva Metals Inc.

Key Development

- In March 2026, Liaoning Huagao New Material Co., Ltd. signed a three-year agreement with Framatome to supply nuclear-grade zirconium sponge from 2026 to 2028, supporting its role in the global nuclear materials supply chain.

- In March 2026, TVEL Fuel Company and Chepetsky Mechanical Plant advanced accident-tolerant fuel work after completing pilot operation of chromium-coated zirconium cladding at Rostov NPP Unit 2.

- In April 2026, Westinghouse Electric Company updated its AP1000 design reference with the U.S. NRC, supporting future reactor deployment and long-term demand for zirconium alloy fuel cladding.

- In 2026, Framatome moved ahead with licensing and industrialization of its PROtect chromium-coated cladding, aimed at improving fuel performance and safety in nuclear reactors.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.29 Bn |

| Forecast Revenue (2035) | USD 16.31 Bn |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Zirconium-Niobium Alloy (Zr-Nb), Zirconium-Tin Alloy, and Zirconium-Aluminium Alloy), By Form (Tubes & Pipes, Sheet, Plates & Strips, Wires & Rods, and Others), By End User (Nuclear Power, Aerospace & Defence, Chemical Processing, and Medical & Healthcare) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Framatome (formerly Areva NP), ATI Inc. (Allegheny Technologies), State Nuclear Baoti Zirconium Industry Co. (SNZ), Westinghouse Electric Company, Orano (formerly Areva Mines), Chepetsky Mechanical Plant (CMP JSC), CNNC Jinghuan Zirconium Industry Co., Ltd., Liaoning Huagao New Material Co., Ltd., Nuclear Fuel Complex (NFC), Luxfer Group, VDM Metals GmbH, Guangdong Orient Zirconic Ind. Sci. & Tech., American Elements, H.C. Starck (Materion), and Aviva Metals Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |