Quick Navigation

Report Overview

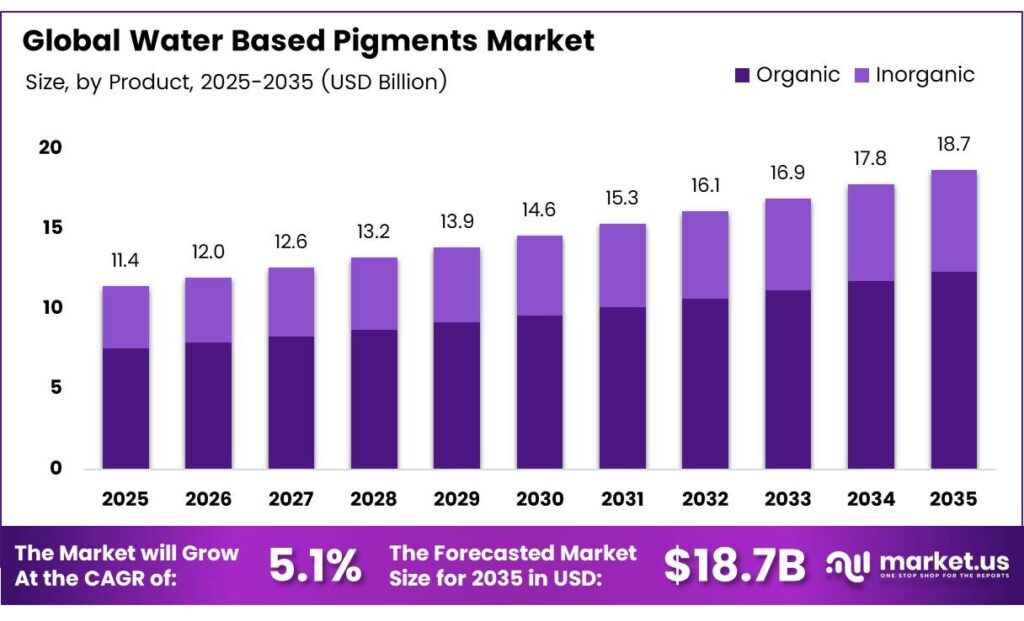

The Global Water-Based Pigments Market size is expected to be worth around USD 18.7 billion by 2035 from USD 11.4 billion in 2025, growing at a CAGR of 5.1% during the forecast period 2026 to 2035.

Water-based pigments are colorant systems dispersed in aqueous carriers, used across paints, coatings, printing inks, and textiles. They replace solvent-borne systems by eliminating toxic organic carriers. This shift responds to environmental mandates and occupational health requirements that now define procurement decisions in major industrial markets.

Organic pigments hold 59.4% of the product segment, reflecting buyer preference for higher chroma and brightness in applications where visual impact determines brand equity. Inorganic alternatives remain relevant in industrial and high-durability applications, but the product mix is shifting toward organic variants as color performance requirements rise.

Water-based gravure inks reduce VOC emissions by 70% compared to traditional oil-based gravure inks. This reduction is not marginal — it places water-based systems below the regulatory threshold in most major markets, removing a key barrier to specification approval in packaging and flexible film printing.

Quinacridone water-based pigment ink achieves a viscosity of 6.81 cP and a particle size below 5 µm. These properties confirm that water-based formulations now meet technical performance thresholds previously dominated by solvent systems, closing the argument that performance must be sacrificed for compliance.

Key Takeaways

- The Global Water-Based Pigments Market was valued at USD 11.4 billion in 2025 and is forecast to reach USD 18.7 billion by 2035 at a CAGR of 5.1% during the forecast period 2026 to 2035.

- By Product, Organic pigments lead with a 59.4% share in 2025.

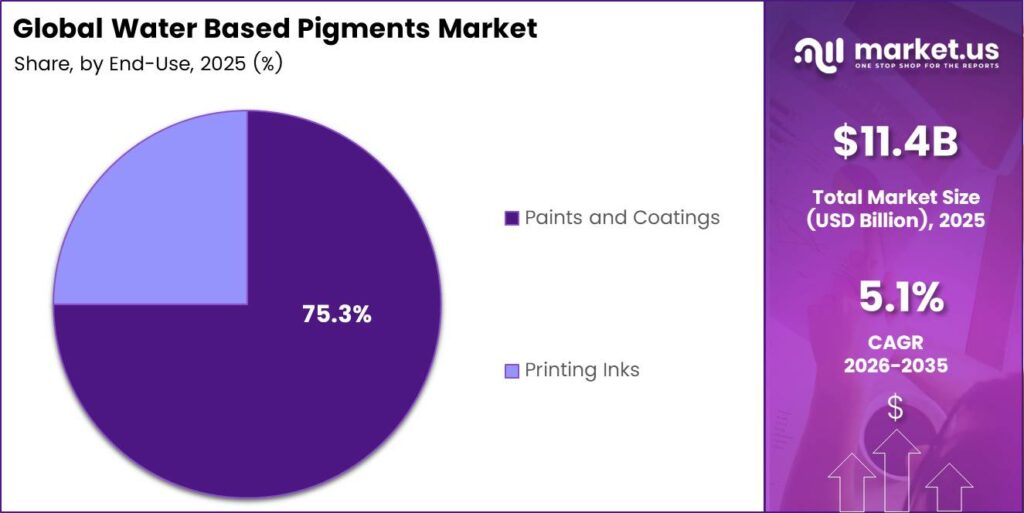

- By End-Use, Paints and coatings dominate with a 75.3% share in 2025.

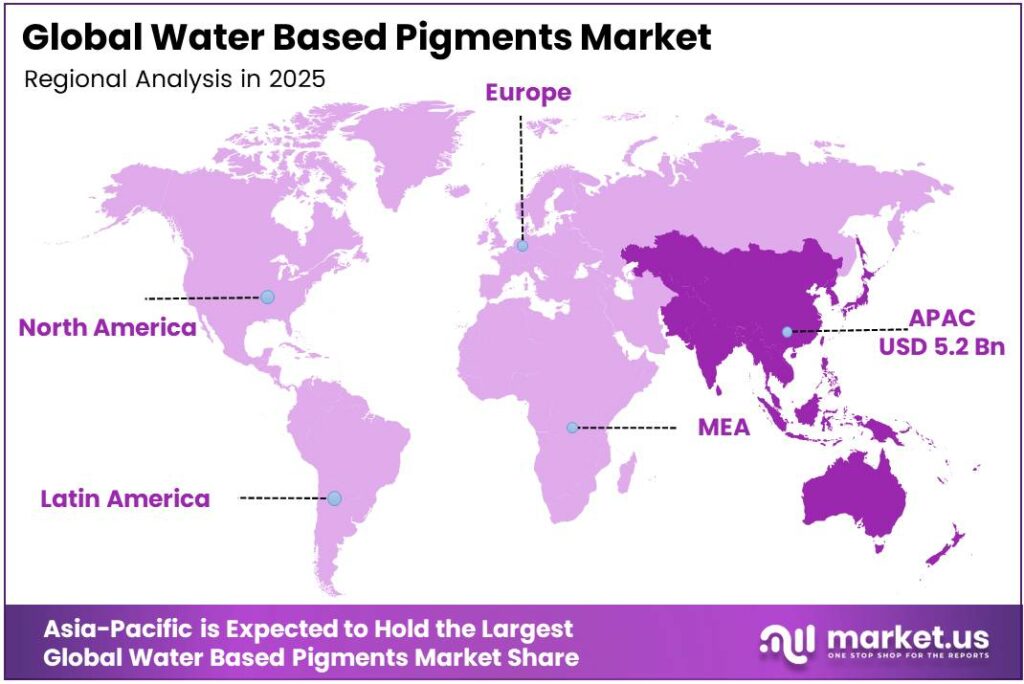

- Asia-Pacific holds the largest regional share at 45.8%, valued at USD 5.2 billion in 2025.

Product Analysis

Organic dominates with 59.4% due to superior chroma and brightness performance.

In 2025, Organic held a dominant market position in the By Product segment of the Water-Based Pigments Market, with a 59.4% share. Brand owners in packaging and consumer goods specify organic pigments because color saturation directly affects shelf visibility and purchase behavior. This buyer-driven preference entrenches organic variants as the default specification across high-value end-uses.

Inorganic pigments carry a structural cost advantage in industrial and exterior durability applications. Iron oxides and titanium dioxide deliver heat stability and lightfastness that organic alternatives cannot replicate at equivalent cost. However, inorganic systems face substitution pressure in interior architectural applications where health-focused formulation standards increasingly favor lower-metal-content alternatives.

End-Use Analysis

Paints and Coatings dominate with 75.3% due to regulatory-driven reformulation across architectural segments.

In 2025, Paints and Coatings held a dominant market position in the By End-Use segment of the Water-Based Pigments Market, with a 75.3% share. Mandatory VOC limits in residential construction across North America and Europe force paint manufacturers to replace solvent-borne pigment systems. This compliance-driven reformulation cycle sustains high and predictable volume off-take from pigment suppliers.

Printing Inks serve as the fastest-evolving end-use within the water-based system shift. Flexible packaging converters face retailer sustainability mandates that now require low-emission ink certification. Converters who adopt water-based gravure and flexographic inks gain preferential access to consumer goods supply chains, creating a structural pull on pigment ink demand independent of broader economic cycles.

Key Market Segments

By Product

- Organic

- Inorganic

By End-Use

- Paints and Coatings

- Printing Inks

Emerging Trends

Circular Economy Principles and Smart Coating Functionality Reshape Water-Based Pigment Development

Pigment manufacturers now source raw materials under circular economy frameworks, prioritizing bio-based and recycled-content inputs. This shift responds to procurement teams in fast-moving consumer goods who require full supply chain sustainability disclosures. Suppliers unable to document material origin lose specification access in sustainability-governed procurement cycles.

Smart coating integration represents a structural product evolution. Formulators embed functional properties — thermal response, UV activation, and conductivity — directly into water-based pigment systems. Solvent-based rotogravure inks contain 40–80% solvent, while water-based alternatives contain only 0–5%. This gap confirms that water-based systems create the formulation space needed for functional additive integration without solvent interference.

High-chroma specialty effect pigments and AI-driven formulation tools are converging to compress product development cycles. Manufacturers use machine learning models to predict dispersion stability and color matching outcomes before physical trials. This reduces time-to-market for new shades and cuts reformulation costs — a competitive differentiator as brand owners accelerate seasonal color refreshes.

Drivers

Regulatory Pressure and Sustainable Packaging Needs Accelerate Adoption of Low-VOC Water-Based Pigment Systems

Environmental regulators in North America, Europe, and parts of Asia now enforce strict VOC emission ceilings for industrial coatings and printing applications. Paint and ink manufacturers must reformulate or exit regulated markets. Water-based pigment systems offer the primary compliant pathway, making regulatory alignment a non-negotiable commercial requirement rather than an optional upgrade.

Packaging converters face sustainability mandates from global consumer goods brands specifying low-emission printing inputs. Adhesion values in water-based ink systems improved from 70.19% to 95% with ADH crosslinker addition. This performance gain demonstrates that water-based systems now match functional benchmarks previously held only by solvent-based alternatives, removing the performance objection from adoption decisions.

Architectural paint manufacturers cite indoor air quality as a primary driver of reformulation investment. Health-conscious buyers — particularly in residential and healthcare construction — actively select low-VOC paints, creating demand that flows directly to water-based pigment suppliers. This consumer-level preference embeds water-based specifications into builder and contractor procurement standards across mature markets.

Restraints

Substrate Compatibility Gaps and Higher Formulation Costs Limit Water-Based Pigment Penetration in Industrial Applications

Water-based pigment systems face adhesion and wetting failures on hydrophobic substrates, including polyolefin films and certain metal surfaces. These compatibility limitations exclude water-based products from fast-growing flexible packaging segments using untreated polypropylene and polyethylene. Converters serving these substrates remain locked into solvent-based systems until surface treatment or primer technologies close the adhesion gap.

Formulation costs for water-based pigments exceed solvent-based equivalents due to more complex dispersant chemistry and stabilization requirements. A sheep-wool protein hydrolysate dispersant reduced yellow iron oxide particle size to 841.6 nm, versus 875.2 nm without dispersant — illustrating the precision engineering required to achieve stability.

Drying speed remains a limiting factor in high-throughput industrial printing. Water evaporation rates are slower than solvent flash-off, creating bottlenecks on high-speed gravure and flexographic lines. Manufacturers investing in dryer infrastructure upgrades face capital outlay that delays adoption payback, particularly in developing markets where press modernization budgets are constrained.

Growth Factors

Digital Textile Printing, Bio-Based Formulations, and Nanopigment Innovation Open New Revenue Channels for Water-Based Systems

Digital textile printing adoption creates direct volume demand for water-based inkjet pigment dispersions. Inkjet pigment dispersions are optimized at particle sizes of 10–400 nm, preferably 50–150 nm, for stability and jetting performance. Pigment suppliers who master this particle size control window access a textile printing market where conventional dye systems face environmental and wastewater treatment restrictions.

Bio-based and biodegradable pigment formulations address procurement requirements from brands with formal net-zero commitments. This segment creates a premium pricing opportunity because buyers accept higher input costs when sustainability credentials deliver regulatory risk reduction.

Urbanization in Southeast Asia, South Asia, and Sub-Saharan Africa expands construction activity and, consequently, architectural coating consumption. Water-based pigment suppliers entering these markets through local distribution partnerships capture volume at the base of adoption curves — before domestic producers establish formulation capability.

Regional Analysis

Asia-Pacific Dominates the Water-Based Pigments Market with a Market Share of 45.8%, Valued at USD 5.2 Billion

Asia-Pacific holds 45.8% of the global Water Based Pigments Market, valued at USD 5.2 billion in 2025. China’s construction output and India’s packaging sector create the two largest end-use consumption pools within the region. Local regulatory tightening on VOC emissions in Chinese manufacturing zones further accelerates the replacement of solvent-based systems at scale.

North America benefits from a mature regulatory infrastructure enforcing low-VOC specifications across architectural, industrial, and packaging coatings. The U.S. EPA’s National Emission Standards and state-level California Air Resources Board rules create non-negotiable compliance floors. These mandates establish a structural demand base for water-based pigment systems that persists independent of broader construction cycle fluctuations.

Europe operates under REACH chemical restrictions and EU Ecolabel criteria that directly influence pigment selection in coatings and inks. Formulators serving European markets reformulate proactively to maintain market access. Germany and France anchor industrial coating demand, while Scandinavian markets lead adoption of bio-based and circular-economy-aligned pigment specifications that set early benchmarks for the broader region.

The Middle East and Africa region remains at an earlier adoption stage, with infrastructure-led construction in GCC countries driving primary coatings demand. Regulatory frameworks for VOC emissions are less developed than in Western markets, which slows mandatory reformulation timelines. However, multinational paint brands entering GCC markets bring global water-based formulation standards that gradually establish local specification norms.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Northwest Dispersions positions itself as a specialist in custom aqueous pigment dispersions, targeting formulators who require precise particle size and rheological control. This specialization allows Northwest Dispersions to serve niche but high-margin accounts in inkjet and digital printing — segments where off-the-shelf dispersion products fail performance specifications and where switching costs protect incumbents.

LANXESS leverages its integrated inorganic pigment production — particularly iron oxide — to offer a cost-stable supply across construction and industrial coating markets. Vertical integration from raw material to finished dispersion gives LANXESS pricing discipline that pure-play formulators cannot replicate. This structural advantage becomes particularly valuable when raw material markets tighten, and spot procurement costs rise for competitors.

Chromatech Incorporated concentrates on color dispersion systems for the plastics and coatings industries, with a product range oriented toward consistent batch-to-batch color matching. Consistency is the core value proposition in markets where production line color variance generates costly rework. Chromatech’s technical service infrastructure reinforces customer retention by embedding its color-matching protocols into customer quality control procedures.

Huntsman Corporation brings a multi-chemistry platform to water-based pigment applications, drawing on its textile, coating, and performance products divisions. This cross-divisional resource base enables Huntsman to develop integrated formulation solutions — combining pigment, binder, and additive systems — that single-product competitors cannot offer. The bundled solution model creates higher account value and reduces exposure to commodity price competition.

Key Players

- Northwest Dispersions

- LANXESS

- Chromatech Incorporated

- Huntsman Corporation

- Proquimac

- Clariant AG

Recent Developments

- In 2025, LANXESS announced it would showcase Bayferrox Scopeblue reduced-carbon pigments, low-VOC additives, and microbial-control solutions at American Coatings. It launched Scopeblue micronized yellow iron-oxide pigments with a lower product carbon footprint vs. regular Bayferrox grades. It also markets Levanyl / Levanox water-based pigment dispersions for paints, inks, paper, synthetic leather, wood preservatives, etc.

- In 2025, Huntsman is related more through coatings/additives/specialty amines than current pigment manufacturing; its pigment & additives business was separated as Venator. Huntsman opened an expanded Performance Products facility in Hungary, serving the polyurethane, coatings, metalworking, and electronics industries.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 11.4 Billion |

| Forecast Revenue (2035) | USD 18.7 Billion |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Organic, Inorganic), By End-Use (Paints and Coatings, Printing Inks) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Northwest Dispersions, LANXESS, Chromatech Incorporated, Huntsman Corporation, Proquimac, Clariant AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |