Quick Navigation

Report Overview

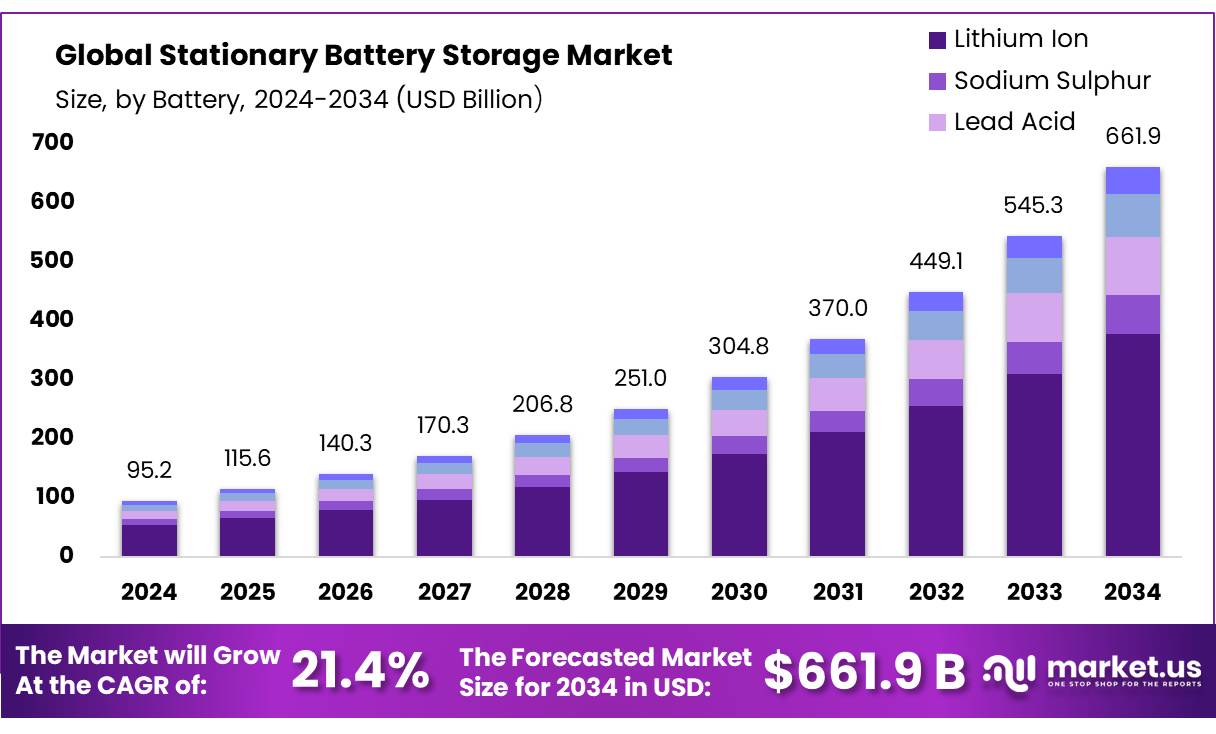

The Global Stationary Battery Storage Market size is expected to be worth around USD 661.9 Bn by 2034, from USD 95.2 Bn in 2024, growing at a CAGR of 21.4% during the forecast period from 2025 to 2034.

Stationary battery storage is utilized to store energy at a fixed location using rechargeable batteries. These systems are integral to the energy infrastructure, providing backup power, aiding in supply-demand balance, and facilitating the integration of renewable sources like solar and wind into the grid. Stationary batteries are designed for large-scale use in residential, business, and utility settings. They contribute to reducing energy costs, stabilizing the grid, and promoting a sustainable energy ecosystem.

The predominant technologies in this sector include lithium-ion, lead-acid, and flow batteries, each distinguished by its efficiency, lifespan, and cost-effectiveness. Technological Advancements in battery technology, especially in lead-acid, lithium-ion, and flow batteries, have improved their energy density, lifecycle, and safety features, leading to an expanded global deployment.

Lithium-ion batteries, known for their high energy density, excel in charge and discharge efficiency. This characteristic is increasingly significant as environmental concerns shift preferences from traditional vehicles to electric vehicles (EVs), particularly in developed nations like the U.S. and the UK. For example, the U.S. experienced a 7.3% increase in EV sales in 2024, reaching 1.3 million vehicles. This surge in EV usage indirectly boosts the stationary battery storage market due to the related demand for high-efficiency energy storage solutions.

A notable development occurred in March 2024 when ENGIE was authorized by Chile’s National Electricity Coordinator (CEN) to commence commercial operations at BESS Coya in the Antofagasta region, the largest battery energy storage system in Latin America. With a storage capacity of 638 MWh and an installed power of 139 MW, this facility leverages lithium battery technology to store energy from the adjacent Coya PV solar plant, which has a capacity of 180 MWac.

Key Takeaways

- The global stationary battery storage market is projected to grow from USD 95.2 billion in 2024 to USD 661.9 billion by 2034.

- The market is expected to expand at a CAGR of 21.4% from 2025 to 2034.

- Lithium-Ion batteries held a dominant 57.3% market share in 2024.

- Hydrogen and Ammonia Storage systems accounted for 32.2% of the market share in 2024.

- Grid Services dominated the market, holding a 56.3% share in 2024.

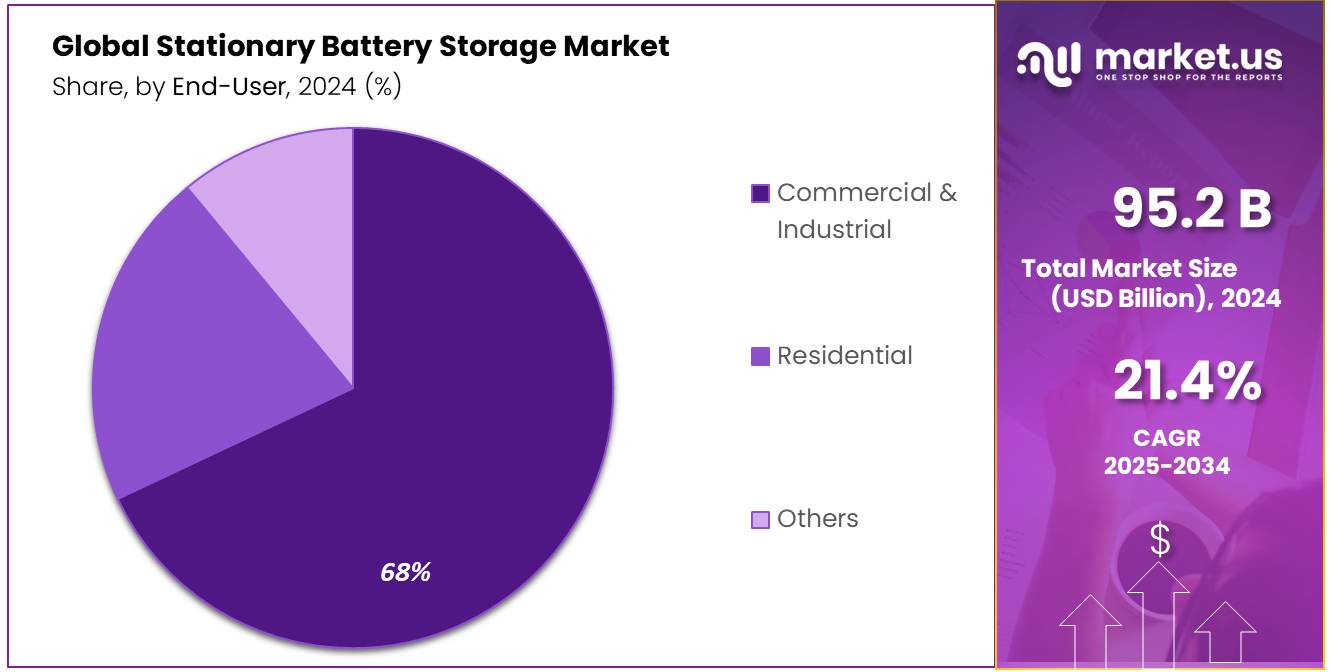

- The Commercial & Industrial sector captured the largest share, accounting for 68.2% in 2024.

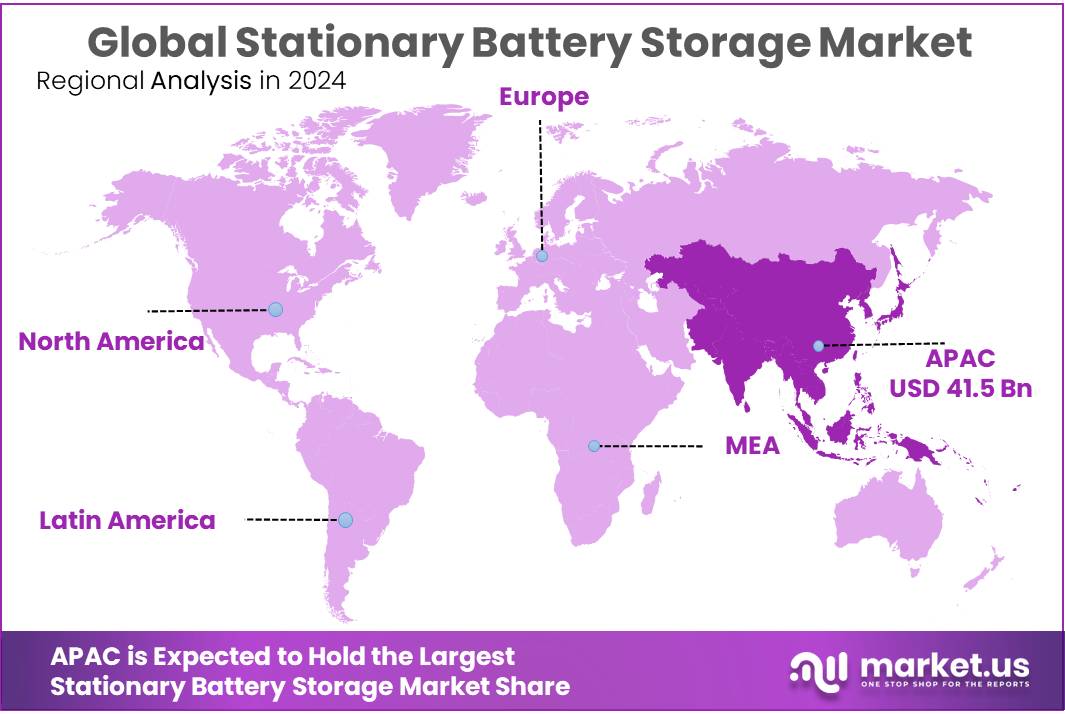

- The Asia-Pacific (APAC) region dominated the stationary battery storage market, holding a 43.6% market share in 2024, valued at approximately USD 41.5 billion.

By Battery

In 2024, Lithium-Ion batteries held a dominant position in the stationary battery storage market, capturing more than a 57.3% share. This significant market share is attributed to the widespread adoption of Lithium-Ion batteries in various applications, including grid storage and renewable energy integration. Lithium-Ion batteries are favored for their high energy density, long lifespan, and decreasing cost per kilowatt-hour, factors that drive their preference over other battery types.

As the demand for renewable energy sources continues to rise, the need for efficient and reliable energy storage solutions like Lithium-Ion batteries is expected to grow, further solidifying their position in the market. Looking ahead to 2025, the market is anticipated to witness continued growth driven by technological advancements and increased investments in energy storage solutions.

By Type of Energy Storage

In 2024, Hydrogen and Ammonia Storage systems held a dominant position in the stationary battery storage market, securing over a 32.2% share. This market segment benefits significantly from the push for greener energy solutions, as both hydrogen and ammonia are considered clean alternatives for energy storage, with the potential to reduce carbon footprints significantly.

These storage types are particularly pivotal in sectors where battery storage needs to exceed the typical capacity of Lithium-Ion systems, such as in large-scale renewable energy projects or industrial applications. With the ongoing advancements in technology and an increasing focus on sustainable energy practices, the market share for hydrogen and ammonia storage solutions is expected to maintain a strong growth trajectory into 2025. This growth is likely fueled by investments in infrastructure to support these technologies and the development of more efficient ways to store and utilize hydrogen and ammonia energy.

By Application

In 2024, Grid Services held a dominant market position in the stationary battery storage market, capturing more than a 56.3% share. This substantial market share reflects the critical role of stationary battery storage in managing grid stability, balancing supply and demand, and enhancing the integration of renewable energy sources. The ability of these storage systems to provide essential services such as load leveling, peak shaving, and frequency regulation has made them invaluable in modern energy infrastructures.

As renewable energy adoption increases, the demand for grid services that can handle intermittent energy supplies continues to grow. Looking ahead to 2025, the importance of grid services is expected to remain high, driven by further investments in renewable energy and the ongoing need for efficient grid management solutions.

By End-User

In 2024, the Commercial & Industrial sectors held a dominant position in the stationary battery storage market, capturing more than a 68.2% share. This significant share underscores the crucial role that stationary battery storage plays in these sectors, particularly for energy management and operational efficiency. Businesses in these sectors increasingly rely on battery storage solutions to provide emergency backup, enhance energy security, and optimize electricity costs through peak-shaving strategies.

Moreover, the shift towards sustainability and the integration of renewable energy sources continue to drive the adoption of battery storage systems within commercial and industrial settings. As we move into 2025, the trend towards digitalization and smart infrastructure is expected to further boost the demand for sophisticated battery storage systems, ensuring that this segment maintains a strong market presence.

Key Market Segments

By Battery

- Lithium Ion

- LFP

- NMC

- Others

- Sodium Sulphur

- Lead Acid

- Flow Battery

- Others

By Type of Energy Storage

- Hydrogen and Ammonia Storage

- Gravitational Energy Storage

- Compressed Air Energy Storage

- Liquid Air Storage

- Thermal Energy Storage

By Application

- Grid Services

- Behind the Meter

- Off Grid

- Others

By End-User

- Residential

- Commercial & Industrial

- Others

Drivers

Government Support for Renewable Energy Integration

One of the major driving factors for the growth of the stationary battery storage market is the substantial government support for renewable energy sources. As countries worldwide aim to reduce carbon emissions and enhance energy security, numerous governments have implemented policies and incentives to promote the integration of renewable energy into their national grids. For example, the United States Department of Energy has been actively funding projects and technologies that facilitate the adoption of renewable energy, including solar and wind, through various grants and tax incentives.

These initiatives are designed to make renewable energy projects more economically viable and competitive against traditional energy sources. For instance, in Germany, the Federal Ministry for Economic Affairs and Energy provides various funding programs to support energy storage systems coupled with renewable energy installations. These programs not only promote the use of renewable energy but also stabilize the grid during variable energy production levels.

Furthermore, in China, the government’s commitment to renewable energy is reflected in its 14th Five-Year Plan, which emphasizes green energy sectors as a part of its economic development strategy. This policy framework encourages the deployment of large-scale battery storage systems to manage the intermittency of renewable energy sources effectively.

Such government-backed initiatives and financial incentives are critical enablers, fostering a conducive environment for the expansion and scalability of battery storage solutions. They help lower the investment risks and provide a clearer path toward profitability for projects involving renewable energy storage. This supportive legislative landscape is crucial in driving forward the adoption and development of stationary battery storage systems as pivotal components in the global transition to sustainable energy.

Restraints

High Initial Investment Costs

A major restraining factor for the adoption of stationary battery storage systems is the high initial investment costs associated with deploying these technologies. While the benefits of battery storage, such as enhanced grid stability and renewable integration, are widely recognized, the upfront cost remains a significant barrier for many businesses and utility providers.

The cost of battery storage systems primarily comprises the batteries themselves, along with associated hardware, installation, and operational maintenance expenses. For example, current market analyses suggest that the total cost for deploying a medium-scale lithium-ion battery storage system can range significantly depending on capacity and specific technology used. This high cost can deter especially smaller utilities or commercial entities from investing in these systems.

Governments and industry bodies have recognized this challenge and are working to mitigate it through various financial incentives and support programs. For instance, the European Union has established funds and grants specifically aimed at reducing the capital expenditure for green energy projects, including battery storage. These financial aids are intended to lower the barrier to entry and accelerate the deployment of energy storage solutions across the continent.

Despite these efforts, the initial cost is still a substantial hurdle, impacting the decision-making process for potential adopters of the technology. Overcoming this obstacle is crucial for the wider acceptance and implementation of stationary battery storage solutions, particularly in regions where financial support from the government is less robust or non-existent.

Opportunity

Expansion into Emerging Markets

A significant growth opportunity for the stationary battery storage market lies in its expansion into emerging markets. These regions are rapidly industrializing and urbanizing, presenting a robust demand for reliable and efficient energy solutions. As these economies grow, so does the strain on their energy infrastructures, which are often unable to meet the increasing energy demands reliably without modernization.

Emerging markets, particularly in Asia, Africa, and South America, are experiencing a surge in energy consumption due to their growing middle classes and expanding industrial sectors. For instance, countries like India and Brazil are implementing aggressive renewable energy integration plans. These plans are part of broader national strategies to ensure sustainable growth, which include significant investments in solar and wind capacities. The integration of renewable sources increases the need for effective energy storage solutions to manage supply variability and ensure stability of the grid.

Governments in these regions are supporting the adoption of energy storage technologies through various incentives such as tax breaks, subsidies, and favorable regulations. For example, India’s National Energy Storage Mission aims to promote the creation of a sustainable ecosystem for energy storage in the country, recognizing its critical role in both energy security and renewable integration.

The combination of increasing energy demand, favorable government policies, and the critical need for grid modernization presents a lucrative opportunity for the growth of the stationary battery storage market in emerging economies. Companies that can navigate these markets’ regulatory and operational challenges, possibly through partnerships with local firms or direct investment in local operations, stand to gain considerably.

Trends

Integration of AI and IoT Technologies in Stationary Battery Storage

One of the latest trends in the stationary battery storage market is the integration of artificial intelligence (AI) and the Internet of Things (IoT) technologies. This trend is revolutionizing how battery storage systems operate, making them smarter and more efficient. AI algorithms optimize the charging and discharging processes to extend the life of the battery and maximize energy efficiency. IoT, on the other hand, enables real-time monitoring and management of battery systems, ensuring optimal performance and preventing maintenance issues before they become critical.

This technology integration addresses some of the most pressing challenges in energy storage, such as improving cost-efficiency and operational reliability. For example, AI can predict energy usage patterns and automatically adjust storage usage, reducing reliance on grid-supplied electricity during peak demand times, which lowers energy costs. Similarly, IoT devices can send instant alerts about system performance anomalies, allowing for immediate troubleshooting, which minimizes downtime and maintenance costs.

Governments are also recognizing the potential of these technologies in enhancing energy security and sustainability. Initiatives such as the Smart Grids Innovation Network (SGIN) in Canada and the Smart Grids Infrastructure program in the European Union promote the adoption of smart technology in energy infrastructures. These programs support research and deployment of AI and IoT in energy systems, including stationary battery storage.

As AI and IoT technologies continue to evolve, their application in stationary battery storage is expected to become more widespread, offering significant improvements in energy management and efficiency. This not only benefits the energy sector but also contributes to broader economic and environmental goals.

Regional Analysis

In the stationary battery storage market, the Asia-Pacific (APAC) region has emerged as a dominant player, capturing a significant 43.6% market share, valued at approximately $41.5 billion. This strong position is driven by the rapid industrialization and urbanization across major economies such as China, India, and South Korea, where there is a growing demand for reliable and efficient energy storage solutions. These countries are aggressively integrating renewable energy sources into their power grids to meet rising energy demands and environmental targets, further boosting the need for advanced battery storage systems.

China leads the APAC region in terms of market share and technological advancements in battery storage. The Chinese government’s commitment to renewable energy and the reduction of carbon emissions has resulted in substantial investments in battery storage solutions. Similarly, India is experiencing significant growth in this sector, supported by government initiatives aimed at enhancing energy security and achieving ambitious renewable energy goals. South Korea, on the other hand, is not only a large consumer of stationary battery storage solutions but also a leading innovator and manufacturer of advanced battery technologies.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BYD: BYD stands out in the stationary battery storage market as a leading Chinese manufacturer known for its comprehensive range of rechargeable batteries. The company has made significant inroads into the renewable energy storage sector, leveraging its expertise in battery technology to support large-scale energy storage projects. BYD’s commitment to innovation and sustainability helps it maintain a competitive edge in both domestic and international markets.

CATL: Contemporary Amperex Technology Co. Limited (CATL) is a global leader in the production of lithium-ion batteries for energy storage solutions. Based in China, CATL supplies batteries that are crucial for electric vehicles and stationary storage systems. The company’s focus on research and development has positioned it as a key player in driving forward the energy storage technology, which supports the expansion of renewable energy implementations.

Duracell: Renowned for its long-standing reputation in battery manufacturing, Duracell has also carved a niche in the stationary battery storage market. The company offers reliable battery solutions for both residential and commercial applications, emphasizing durability and efficiency. Duracell continues to innovate to meet the evolving demands of the energy storage market, ensuring high performance and safety in its products.

Durapower: Durapower excels in the stationary battery storage market by specializing in advanced battery technology solutions for a range of applications, including industrial and renewable energy sectors. The company focuses on delivering high-quality, durable battery systems that offer superior performance and longevity, catering to the growing demand for efficient energy storage.

Top Key Players

- BYD

- CATL

- Duracell

- Durapower

- Exide Technologies

- GS Yuasa

- Hitachi

- Hoppecke Batteries

- Johnson Controls

- Leclanche

- LG

- Panasonic

- Panasonic Corporation

- Philips

- Samsung SDI

- Siemens

- SK Innovation

- Tesla

- Toshiba Corporation

- Varta

Recent Developments

In 2023, BYD delivered 22 gigawatt-hours (GWh) of batteries for energy storage purposes, representing a 57% increase from the previous year.

In 2023 CATL alone, the company’s deliveries for stationary storage systems soared by 46.8% to 69 gigawatt-hours (GWh), significantly outperforming its growth in the electric vehicle (EV) battery sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 95.2 Bn |

| Forecast Revenue (2034) | USD 661.9 Bn |

| CAGR (2025-2034) | 21.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Battery (Lithium Ion (LFP, NMC, Others), Sodium Sulphur, Lead Acid, Flow Battery, Others), By Type of Energy Storage (Hydrogen and Ammonia Storage, Gravitational Energy Storage, Compressed Air Energy Storage, Liquid Air Storage, Thermal Energy Storage), By Application (Grid Services, Behind the Meter, Off Grid, Others), By End-User ( Residential, Commercial And Industrial, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | BYD, CATL, Duracell, Durapower, Exide Technologies, GS Yuasa, Hitachi, Hoppecke Batteries, Johnson Controls, Leclanche, LG, Panasonic, Panasonic Corporation, Philips, Samsung SDI, Siemens, SK Innovation, Tesla, Toshiba Corporation, Varta |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |