Quick Navigation

Report Overview

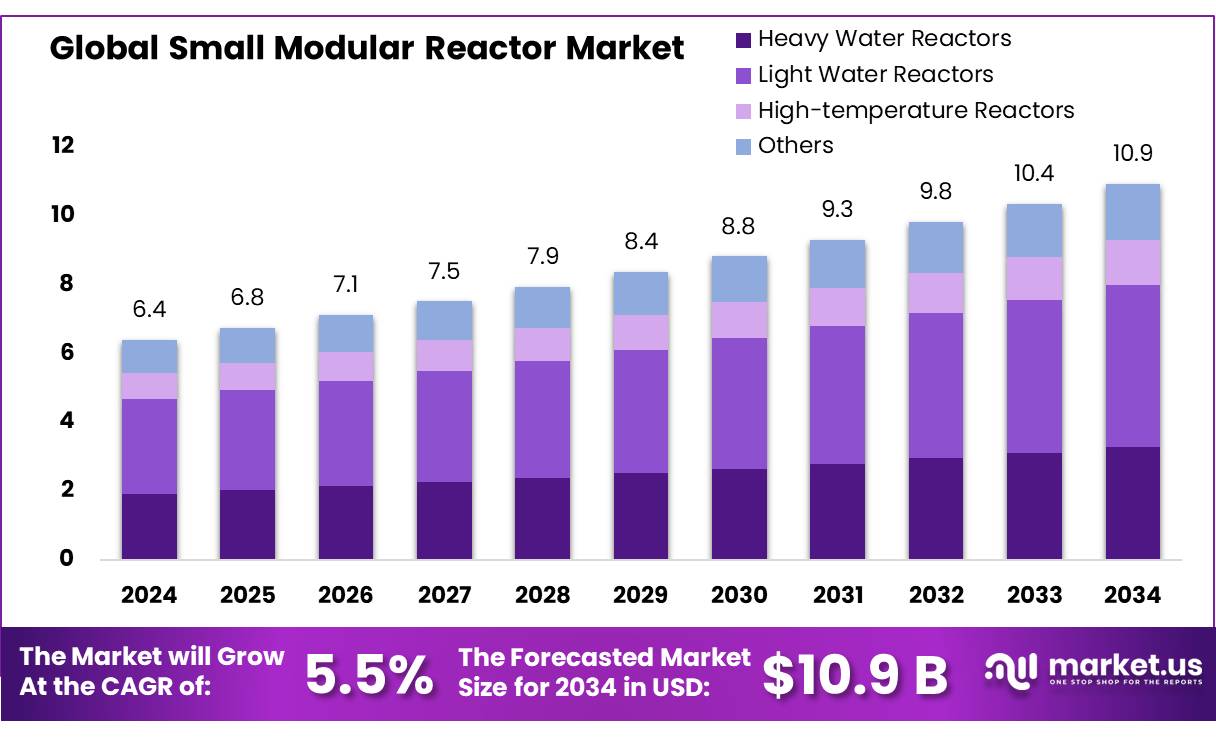

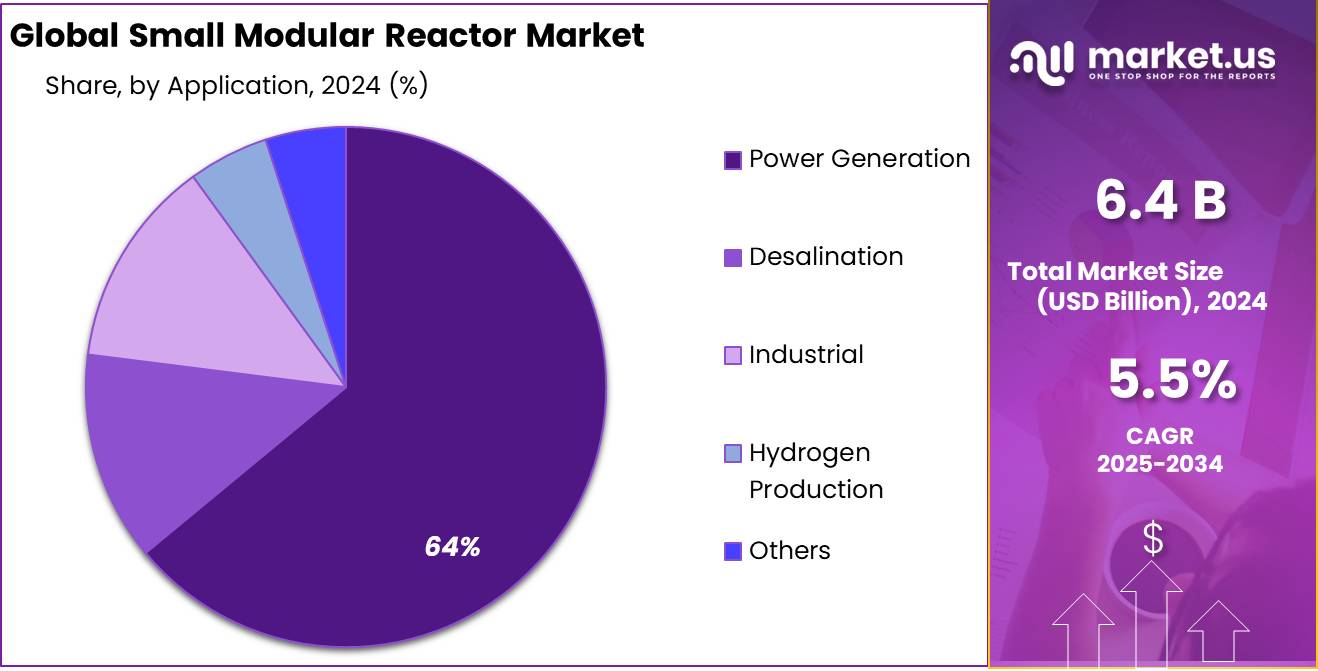

The Global Small Modular Reactor Market size is expected to be worth around USD 10.9 Bn by 2034, from USD 6.4 Bn in 2024, growing at a CAGR of 5.5% during the forecast period from 2025 to 2034.

The expansion of the Small Modular Reactor (SMR) market is primarily driven by their ability to offer a flexible and cost-efficient alternative for nuclear power generation. These reactors are designed for factory construction and are transported to installation sites, which significantly reduces the construction duration and expenses relative to traditional large-scale reactors. Additionally, Small Modular Reactor come equipped with advanced safety features, such as passive safety systems, and can be installed in remote or small-grid areas where larger facilities are impractical.

The Small Modular Reactor sector is marked by the active involvement of both established nuclear technology companies and dynamic new entrants. Key industry players include Rolls-Royce in the UK, NuScale Power in the USA, and Rosatom in Russia, all of which are at the forefront of Small Modular Reactor development and deployment. As of 2025, there are more than 70 Small Modular Reactor designs in various stages of progress globally, with numerous projects nearing the construction stage or having already achieved design certification from regulatory authorities.

Government support is crucial in driving the development of the Small Modular Reactor market. In the United Kingdom, for instance, the government has committed substantial funds to Small Modular Reactor research and development as a component of its comprehensive “Green Industrial Revolution” ten-point plan. In a similar vein, the Canadian government is vigorously promoting the advancement of Small Modular Reactors through its detailed Small Modular Reactor Action Plan, working in cooperation with several provincial governments and the private sector. These initiatives underscore the strategic role of national policies in facilitating the growth and adoption of Small Modular Reactor technologies across different regions.

Key Takeaways

- Small Modular Reactor Market is projected to grow from USD 6.4 billion in 2024 to USD 10.9 billion by 2034, with a CAGR of 5.5% during the forecast period from 2025 to 2034.

- Light Water Reactors captured a 43.3% share of the market in 2024, valued for their proven technology and reliability, primarily using ordinary water as coolant and moderator.

- Grid Connected SMRs dominated the market with a 67.4% share in 2024, integrating seamlessly with existing grid infrastructure, thereby enhancing their attractiveness for expanding regional energy capacities.

- Multi Module Power Plant configurations led the market with a 58.5% share in 2024, appreciated for their scalability and flexibility in energy output adjustment based on demand without extensive downtime.

- Water-Cooled Reactors held a 56.3% market share in 2024, preferred for their reliability and extensive global deployment, using water as both coolant and moderator.

- The 101-300 MW capacity segment of SMRs held a 47.4% market share in 2024, favored for balancing scalability with manageability, suitable for larger grid systems and diverse energy strategies.

- Power Generation was the dominant application, occupying a 64.2% market share in 2024, driven by the need for stable and reliable energy sources supporting ongoing industrial and residential sector growth.

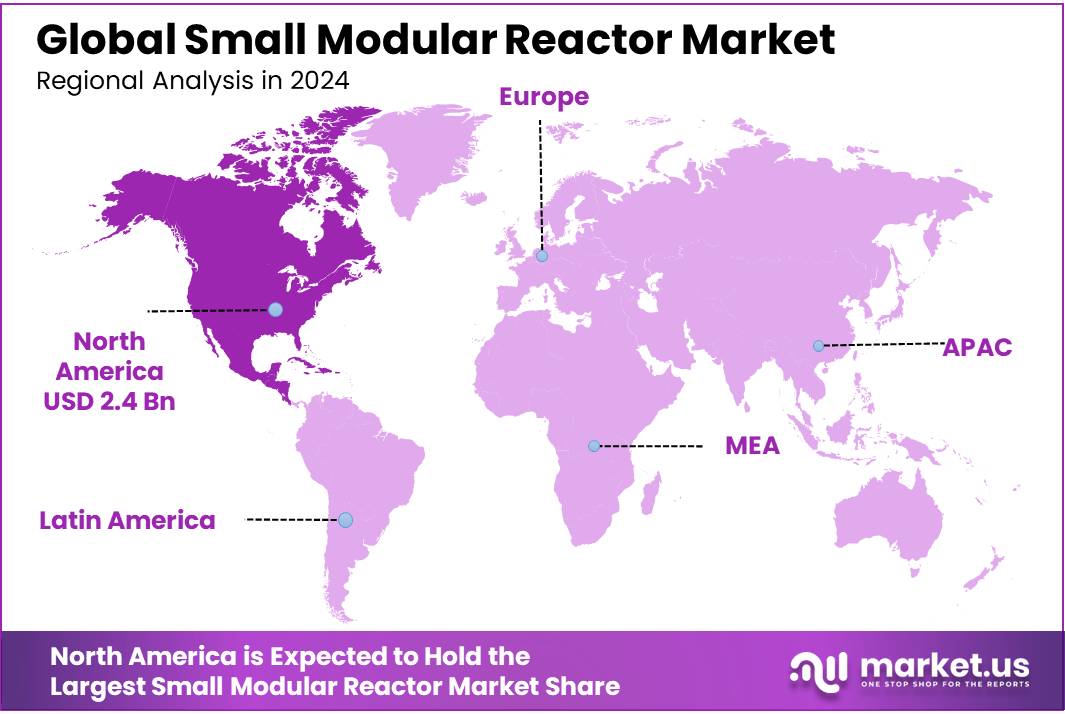

- North America was the leader in the SMR market, holding a 38.3% share, valued at approximately $2.4 billion in 2024.

By Product Type

In 2024, Light Water Reactors held a dominant market position, capturing more than a 43.3% share of the small modular reactor market. This type of reactor is favored for its proven technology and reliability, which are crucial in the nuclear energy sector. Light Water Reactors (LWRs) utilize ordinary water as a coolant and neutron moderator. This design simplicity and operational familiarity make them a preferred choice for many new nuclear projects around the world, especially in markets that are just beginning to adopt nuclear energy solutions.

The appeal of LWRs also lies in their safety features and the extensive global experience in managing such reactors, which reduces the perceived risks associated with nuclear power. Moving into 2025, the market is expected to see continued interest in LWRs, driven by global energy demands and the push for low-carbon technologies. The ongoing development and licensing of new LWR designs are likely to further solidify their market share, attracting investments from both public and private sectors.

By Connectivity

In 2024, Grid Connected small modular reactors (SMRs) held a dominant market position, capturing more than a 67.4% share. This segment benefits greatly from the ability to integrate seamlessly with the existing power grid infrastructure, making it a highly attractive option for regions looking to expand their energy capabilities without the need for extensive new infrastructure. Grid-connected SMRs provide a stable and reliable source of power that can support the base load while complementing intermittent renewable energy sources like solar and wind.

The scalability of grid-connected SMRs also allows for gradual energy capacity increases, which is particularly appealing in densely populated or rapidly industrializing areas. As we look towards 2025, the adoption of grid-connected SMRs is expected to continue growing. This growth is supported by advancements in modular technology, which reduce both construction times and costs, further enhancing the appeal of this connectivity type. Moreover, regulatory frameworks are increasingly becoming favorable for nuclear energy, recognizing its role in achieving carbon neutrality goals, thus pushing the demand for grid-connected SMRs even higher.

By Deployment

In 2024, Multi Module Power Plant configurations within the small modular reactor (SMR) market held a dominant market position, capturing more than a 58.5% share. These types of plants are particularly valued for their high scalability and flexibility, allowing energy output to be adjusted based on current demand without the need for extensive downtime or retrofitting. Multi Module Power Plants are composed of several small reactors that can collectively provide a significant power capacity, which is an attractive feature for regions needing reliable, continuous power supply.

The design of these plants also enhances safety and operational efficiency, as individual modules can be serviced without interrupting the overall power supply. Looking forward to 2025, the market for Multi Module Power Plants is expected to expand further. This growth will be driven by ongoing technological improvements that reduce the risk and cost associated with nuclear energy. Additionally, as governments and private sectors seek more resilient and stable energy solutions in the face of increasing energy demands and climate change pressures, Multi Module Power Plants are poised to become an increasingly common sight in the global energy landscape.

By Reactor Type

In 2024, Water-Cooled Reactors held a dominant market position in the small modular reactor (SMR) landscape, capturing more than a 56.3% share. These reactors, which use water as a coolant and moderator, are a cornerstone in the nuclear industry due to their proven technology and extensive deployment worldwide. The reliability and safety record of water-cooled reactors make them a preferred choice for many nations looking to diversify their energy mix with nuclear power.

The versatility of water-cooled reactors, suitable for both electricity generation and industrial heat applications, contributes to their broad market appeal. As we move into 2025, the demand for water-cooled SMRs is anticipated to grow. This is driven by increasing energy needs and a shift towards low-carbon energy sources to combat climate change. Innovations in reactor design are also expected to enhance their efficiency and safety, ensuring that water-cooled reactors remain a staple in both existing and emerging nuclear markets.

By Power Generation Capacity

In 2024, the 101-300 MW power generation capacity segment of small modular reactors (SMRs) held a dominant market position, capturing more than a 47.4% share. This range is particularly favored for its balance between scalability and manageability, making it ideal for utilities that require flexibility in their energy production capacities. Reactors within this output range are capable of supporting larger grid systems and can be effectively integrated as part of a diverse energy strategy, complementing renewable sources such as wind and solar.

The 101-300 MW SMRs are seen as a versatile solution for meeting mid-level power demands in both urban and industrial settings. They are small enough to be built and financed more feasibly than larger nuclear facilities, yet powerful enough to make a significant contribution to national grids. Looking ahead to 2025, the demand for this power capacity range is expected to grow as countries continue to invest in nuclear technologies that offer stable, low-carbon energy without the geographical or natural resource constraints associated with many types of renewable energy.

By Application

In 2024, Power Generation held a dominant market position in the small modular reactor (SMR) sector, capturing more than a 64.2% share. This application of SMRs has gained considerable traction due to the increasing demand for stable and reliable energy sources that can support the continuous growth of both industrial and residential sectors. Power generation through SMRs offers a compelling advantage by providing consistent electricity without the intermittency issues associated with many renewable resources.

SMRs in power generation are particularly appealing in regions where energy security is a priority or where grid infrastructure may not support large-scale nuclear plants. As we advance into 2025, the use of SMRs for power generation is expected to expand further. This expansion is fueled by ongoing advancements in nuclear technology, improved safety measures, and more streamlined regulatory processes, making nuclear a more accessible option for meeting global energy needs sustainably and efficiently.

Key Market Segments

By Product Type

- Heavy Water Reactors

- Light Water Reactors

- High-temperature Reactors

- Others

By Connectivity

- Off Grid

- Grid Connected

By Deployment

- Single Module Power Plant

- Multi Module Power Plant

By Reactor Type

- Water-Cooled Reactors

- Liquid Metal-Cooled Fast Neutron Spectrum Reactors

- Molten Salt Reactors

- High-Temperature Gas-Cooled Reactors

- Others

By Power Generation Capacity

- <25 MW

- 25-100 MW

- 101-300 MW

- >300 MW

By Application

- Power Generation

- Desalination

- Industrial

- Hydrogen Production

- Others

Drivers

Government Support and Regulatory Approval

One of the major driving factors for the growth of the Small Modular Reactor (SMR) market is the significant support and regulatory approvals provided by governments worldwide. For example, the U.S. Department of Energy has been a strong proponent of SMRs, providing funding and support to accelerate their development and deployment.

In a recent announcement, the U.S. Department of Energy revealed its commitment to investing $3.2 billion from the Infrastructure Law to support advanced nuclear technologies, which include SMRs. This substantial financial backing aims to enhance the feasibility and speed of SMR deployment across the United States, targeting both domestic energy needs and international market opportunities.

Furthermore, the Canadian government has also shown a strong commitment to advancing SMR technology. Natural Resources Canada released the “SMR Action Plan” which outlines a comprehensive strategy to develop the country’s SMR industry, reflecting collaboration between the government, industries, and other stakeholders. The action plan supports various stages of SMR development from research and innovation to demonstration and commercialization, emphasizing Canada’s role in leading global efforts towards cleaner energy alternatives.

These government initiatives are crucial as they not only provide financial aid but also help in establishing a robust regulatory framework that accelerates licensing processes for new reactors. Simplifying and expediting regulatory approval processes are essential for the development and deployment of SMRs, ensuring that these new nuclear technologies can be brought to market efficiently and safely.

Restraints

High Initial Capital Costs

One significant restraining factor in the development and deployment of Small Modular Reactors (SMRs) is their high initial capital costs. Despite the potential for lower overall operational and maintenance costs compared to traditional nuclear power plants, the initial expenses associated with the development, licensing, and construction of SMRs can be prohibitively high. These costs often deter investors and delay the financial backing needed to launch such projects.

For instance, a report by the International Energy Agency (IEA) highlights that the cost of constructing a traditional nuclear power plant ranges from $6 billion to $9 billion, and while SMRs are designed to be more cost-effective in the long run due to their modular nature, the upfront capital required remains substantial. The IEA suggests that overcoming financial hurdles is crucial for the wider adoption and success of SMRs.

Governments and international bodies recognize these financial challenges and are implementing measures to mitigate them. For example, the European Union, through its Euratom Research and Training Programme, has earmarked significant funds specifically for research into nuclear safety, including SMRs. This funding aims to reduce the financial risk associated with the nuclear research and development phase, making the subsequent steps of licensing and construction more feasible for investors.

Moreover, collaborative international efforts, like those led by the World Nuclear Association, aim to standardize and streamline the design and approval processes for SMRs. By promoting regulatory harmony and reducing the unpredictability of licensing durations and costs, these initiatives can substantially lower the initial financial barriers associated with SMRs.

Opportunity

Expanding Renewable Integration

A significant growth opportunity for Small Modular Reactors (SMRs) lies in their potential to enhance the integration of renewable energy sources into the power grid. As countries increase their reliance on renewables like solar and wind, which are intermittent by nature, the need for stable and reliable power sources to balance the grid becomes crucial. SMRs, with their smaller and more flexible operational capacities, are ideally suited to complement these fluctuations in renewable energy supply.

According to a study by the World Nuclear Association, SMRs can be ramped up or down quickly compared to traditional nuclear power plants, making them an excellent partner for balancing grid stability as renewable penetration increases. This operational flexibility not only helps in maintaining a steady electricity supply but also in enhancing the overall efficiency of the power system.

Furthermore, governments worldwide are recognizing the role of SMRs in achieving their carbon neutrality goals. For instance, the U.S. Department of Energy has launched initiatives like the Advanced Reactor Demonstration Program, which supports projects focused on demonstrating the capabilities of SMRs to integrate with renewables. The program aims to prove the economic and technical viability of these reactors in the context of modern and future energy landscapes that heavily feature renewable technologies.

These initiatives are accompanied by financial incentives and regulatory support, aiming to drive down costs and accelerate the commercialization of SMRs. By seizing this opportunity to bridge the gap between renewable energy supply and demand, SMRs not only position themselves as essential components of sustainable energy strategies but also open new markets for nuclear technology that were previously unexplored due to the limitations of larger reactors.

Trends

Enhanced Safety Features and Automation

A prominent trend in the development of Small Modular Reactors (SMRs) is the focus on enhancing safety features and incorporating advanced automation technologies. These innovations are driving interest and acceptance of SMRs by addressing traditional concerns associated with nuclear power, such as safety risks and human error.

Modern SMRs are being designed with passive safety systems that require no active intervention to maintain safe conditions in the event of an operational anomaly. For example, some models feature natural circulation cooling systems that eliminate the need for mechanical pumps, reducing the likelihood of failure and the impact of external power outages. These passive safety features are becoming a standard expectation in new reactor designs and are critical in gaining regulatory and public approval.

Moreover, automation in SMRs is set to revolutionize how these plants are operated. By integrating digital technologies, SMRs can achieve higher operational efficiencies and precision. Automation extends to monitoring systems that continuously check the reactor’s status and automatically adjust settings to optimize performance and safety. This not only reduces the operational burden but also enhances the reactors’ safety profile.

Governmental bodies and regulatory agencies are supporting these advancements through funding and policy frameworks. For instance, the International Atomic Energy Agency (IAEA) provides guidelines and support for incorporating advanced safety and automation features in nuclear reactor designs. Their initiatives help standardize safety features across the industry, promoting a global shift towards more secure nuclear energy solutions.

Regional Analysis

In the small modular reactor (SMR) market, North America holds a commanding position, dominating the regional landscape with a 38.3% market share, valued at approximately $2.4 billion. This robust market presence is driven by a combination of advanced technological infrastructure, strong governmental support, and a well-established nuclear industry. The United States and Canada are at the forefront of SMR development, with both countries actively investing in research and pilot projects to test the viability and efficiency of SMRs.

The U.S. Department of Energy has been particularly proactive, allocating substantial funds to support the commercialization of SMRs. Initiatives such as the Advanced Reactor Demonstration Program are pivotal, aimed at bringing novel nuclear technologies to market within the next decade. This program not only accelerates the development of SMRs but also ensures that North America remains at the cutting edge of nuclear technology.

Canada’s approach involves collaboration with various stakeholders to establish a conducive environment for SMR deployment, highlighted by its comprehensive SMR Action Plan which lays a strategic roadmap for the development of the industry. The Canadian government’s endorsement of SMRs as a key component of its clean energy strategy further underscores the region’s commitment to these technologies.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Brookfield Asset Management has leveraged its extensive capital resources and investment expertise to become a significant player in the SMR market. By focusing on sustainable and renewable energy projects, including nuclear technologies, Brookfield is positioning itself to meet the growing demand for clean energy solutions worldwide.

Fluor Corporation is actively involved in the development and deployment of SMRs, capitalizing on its extensive engineering and construction experience. The company plays a crucial role in delivering turnkey solutions for SMR projects, ensuring compliance with stringent safety and quality standards.

General Atomics brings its pioneering spirit to the SMR sector, focusing on innovative nuclear technologies. Known for its advanced reactor designs and nuclear research, the company is pushing the boundaries of what’s possible in nuclear energy with a strong commitment to enhancing reactor safety and efficiency.

General Electric Company, through its partnership with Hitachi in nuclear energy, is driving the SMR industry forward with its scalable solutions. GE’s expertise in power generation technology helps tailor SMR designs to be more efficient and adaptable to various energy needs.

Top Key Players

- Brookfield Asset Management

- Fluor Corporation

- General Atomics

- General Electric Company

- Holtec International

- Mitsubishi Heavy Industries Ltd.

- Moltex Energy

- NuScale Power, LLC.

- Rolls-Royce plc

- TerraPower, LLC.

- Terrestrial Energy Inc.

- ULTRA SAFE NUCLEAR

- Westinghouse Electric Company LLC

- X Energy LLC

Recent Developments

Brookfield Asset Management has made significant strides in the Small Modular Reactor (SMR) sector through strategic acquisitions, notably partnering with Cameco Corporation to acquire Westinghouse Electric Company for $8.2 billion in November 2023.

In 2024, Fluor Corporation significantly advanced its position in the Small Modular Reactor (SMR) sector through a major contract for Phase 2 of the front-end engineering and design (FEED) work on the SMR project in Doicesti, Romania.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.4 Bn |

| Forecast Revenue (2034) | USD 10.9 Bn |

| CAGR (2025-2034) | 5.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Heavy Water Reactors, Light Water Reactors, High-temperature Reactors, Others), By Connectivity (Off Grid, Grid Connected), By Deployment (Single Module Power Plant, Multi Module Power Plant), By Reactor Type (Water-Cooled Reactors, Liquid Metal-Cooled Fast Neutron Spectrum Reactors, Molten Salt Reactors, High-Temperature Gas-Cooled Reactors, Others), By Power Generation Capacity (<25 MW, 25-100 MW, 101-300 MW, >300 MW), By Application (Power Generation, Desalination, Industrial, Hydrogen Production, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Brookfield Asset Management, Fluor Corporation, General Atomics, General Electric Company, Holtec International, Mitsubishi Heavy Industries Ltd., Moltex Energy, NuScale Power, LLC., Rolls-Royce plc, TerraPower, LLC., Terrestrial Energy Inc., ULTRA SAFE NUCLEAR, Westinghouse Electric Company LLC, X Energy LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |