Quick Navigation

Report Overview

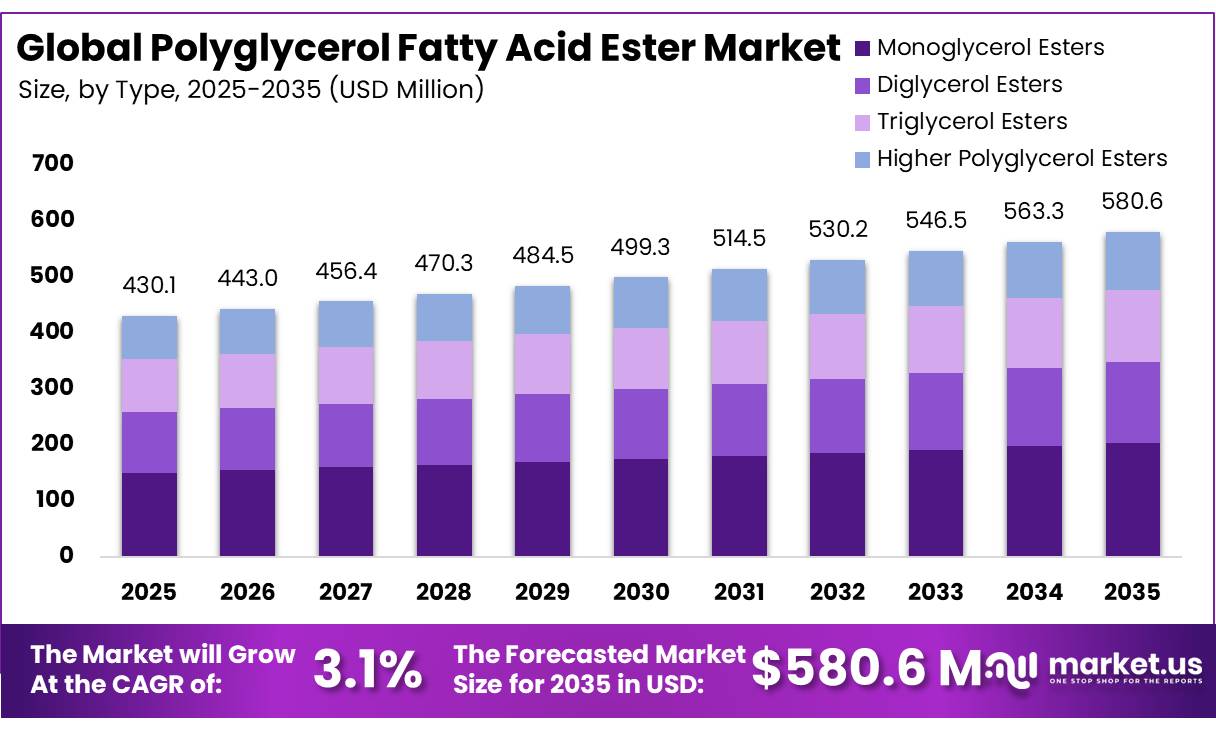

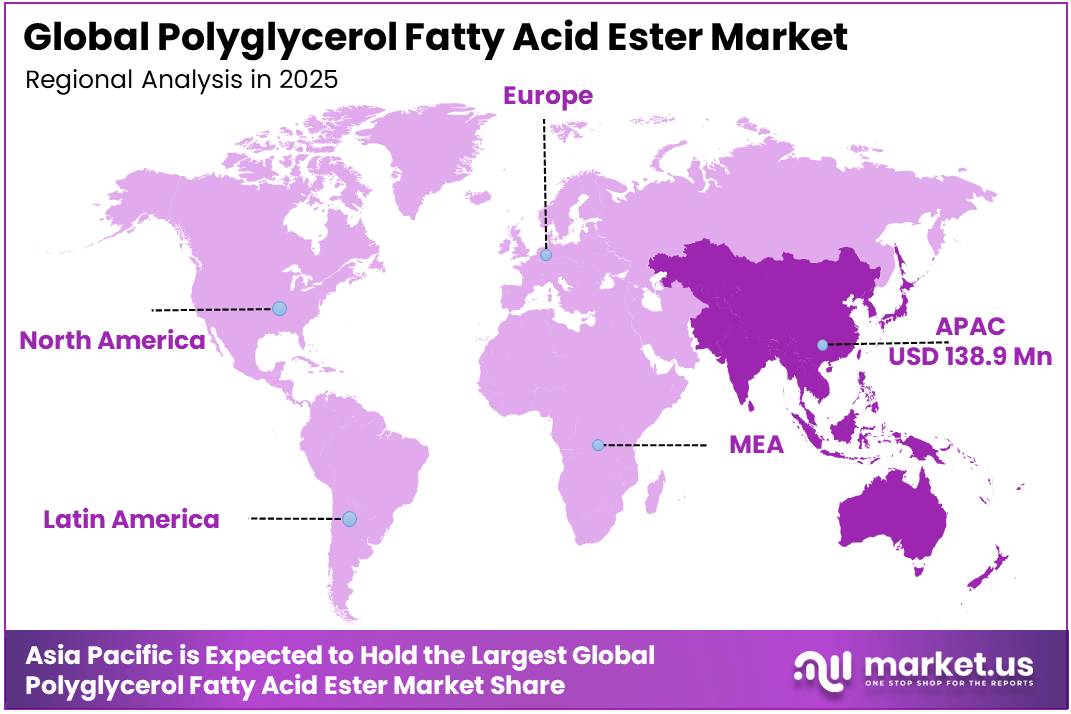

In 2025, the Global Polyglycerol Fatty Acid Ester Market was valued at USD 430.1 million, and between 2026 and 2035, this market is estimated to register a CAGR of 3.1%, reaching about USD 580.6 million by 2035. In 2025, Asia Pacific led the market, achieving over 32.3% share with a revenue of USD 138.9 Million.

Polyglycerol Fatty Acid Ester is a non-ionic emulsifier produced through the esterification of polyglycerol with fatty acids. It is widely used in the food industry to improve texture, stability, aeration, and shelf life in products such as bakery items, dairy products, confectionery, beverages, and processed foods.

- According to the FAO/JECFA specifications published in 2025, the polyglycerol component of the additive is required to contain at least 70% combined diglycerols, triglycerols, and tetraglycerols. Polyglycerols equal to or higher than heptaglycerol must not exceed 10%, while free fatty acids must remain at or below 6%, calculated as oleic acid.

Key Takeaways

- The Global Polyglycerol Fatty Acid Ester Market was valued at USD 430.1 million in 2025.

- The market is projected to grow at a CAGR of 3.1% during the forecast period and is estimated to reach approximately USD 580.6 million by 2035.

- In 2025, Monoglycerol Esters held the dominant position within the type segment, accounting for 35.0% of the global market share, driven by their extensive use as emulsifiers and stabilizers in a wide range of food and industrial formulations.

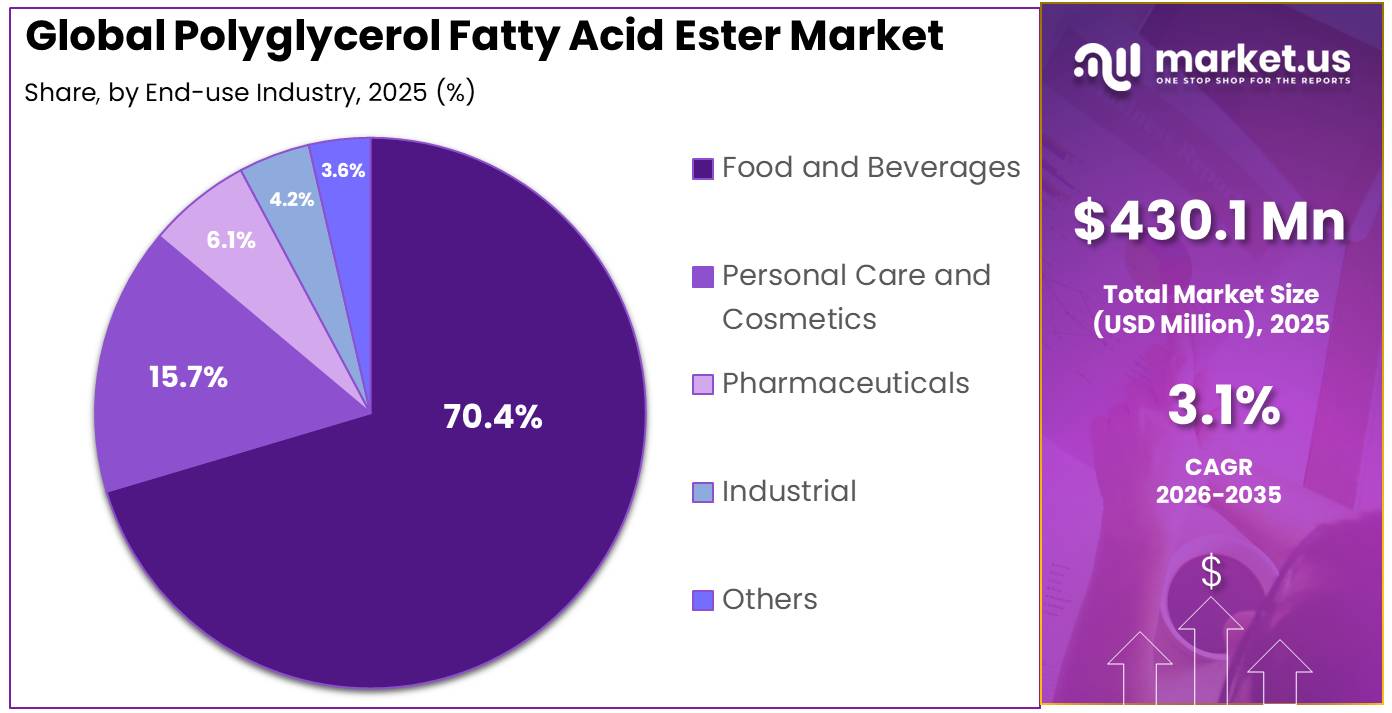

- In 2025, the Food and Beverages segment emerged as the largest end-use industry, capturing 70.4% of the total market share, owing to the growing utilization of polyglycerol fatty acid esters in bakery and processed foods.

- In 2025, Vegetable Oil-based products dominated the market by source, representing 65.0% of the overall market share, supported by increasing consumer preference for plant-derived ingredients and the rising demand for sustainable raw materials.

- In 2025, Liquid Solutions accounted for the largest share of the market by form, holding 55.0% of total revenue, due to their ease of handling, efficient blending characteristics, and broad applicability across multiple end-use industries.

- In 2025, Asia Pacific maintained its leadership position in the global market, securing 32.3% of the total market share supported by strong food manufacturing activity and increasing consumption of specialty ingredients across the region.

The ingredient has gained significant importance as food manufacturers increasingly focus on clean-label formulations, product consistency, and enhanced processing efficiency. Its versatility and compatibility with a broad range of ingredients have made it a valuable component in modern food manufacturing processes.

Government agencies and food safety authorities have also supported the use of approved food emulsifiers through established regulatory frameworks. Organizations such as the European Food Safety Authority (EFSA) and the U.S. Food and Drug Administration (FDA) continue to evaluate and regulate food additives to ensure product safety and quality. These regulatory systems provide manufacturers with confidence in the use of emulsifiers across large-scale food production.

The market is expected to emerge from rising demand for premium bakery products, plant-based foods, functional beverages, and clean-label formulations. According to the OECD-FAO Agricultural Outlook, global agricultural and food consumption is expected to continue expanding steadily through the coming decade, supporting long-term growth in food ingredient demand. As food manufacturers focus on product innovation, formulation efficiency, and consumer-driven quality improvements, polyglycerol fatty acid esters are expected to remain an important ingredient supporting the evolution of the global food and beverage industry.

Polyglycerol Fatty Acid Ester Market Segmentation

Type Analysis

Monoglycerol Esters dominate the market due to their extensive use in food emulsification applications

In 2025, Monoglycerol Esters held a dominant market position, capturing a 35.0% share, due to their widespread application as an emulsifier and stabilizer in food and beverage products. Manufacturers commonly utilize monoglycerol esters in bakery products, confectionery, dairy items, and processed foods to improve texture, enhance product stability, and extend shelf life. Growing demand for high-quality convenience foods and premium food products further strengthened the segment’s position.

Diglycerol Esters is the fastest-growing segment experienced increasing demand due to its enhanced emulsification properties and growing use in specialized food formulations. Food manufacturers increasingly adopted diglycerol esters in products requiring improved stability, texture control, and fat dispersion. The ability of diglycerol esters to support product consistency and formulation flexibility contributed to their growing adoption across food manufacturing operations, making the segment one of the fastest-expanding categories within the market during 2025.

End-Use Industry Analysis

Food and Beverages dominates market driven by extensive use in processed food formulations.

In 2025, Food and Beverages held a dominant market position, capturing a 70.4% share of the market by end-use industry due to the widespread use of polyglycerol fatty acid esters as emulsifiers, stabilizers, and texture enhancers in a variety of food products. Manufacturers extensively utilized these ingredients in bakery products, dairy items, confectionery, beverages, sauces, and processed foods to improve consistency, shelf life, and overall product quality. The growing consumption of convenience foods and the increasing demand for premium food products further supported segment growth.

- In February 2026, Codex electronic working group document CX/FA 26/56/7 proposed lowering the maximum permitted level of INS 475 in dairy-based desserts from 5,000 mg/kg to 2,000 mg/kg and in fruit-based desserts from 5,000 mg/kg to 100 mg/kg.

Personal Care and Cosmetics is the fastest-growing segment in the market by end-use industry. The segment experienced strong growth as manufacturers increasingly incorporated polyglycerol fatty acid esters into skincare, haircare, and cosmetic formulations. These ingredients are valued for their emulsifying properties, helping improve product texture, stability, and application performance. Growing consumer interest in premium personal care products and multifunctional cosmetic formulations supported wider adoption across the industry.

Source Analysis

Vegetable Oil-based dominates market due to strong demand for plant-derived ingredients

In 2025, Vegetable Oil-based held a dominant market position, capturing more than a 65.0% share of the market due to the widespread availability of vegetable-derived raw materials and their extensive use in food, personal care, and pharmaceutical applications. Manufacturers increasingly preferred vegetable oil-based polyglycerol fatty acid esters because they align with growing consumer demand for plant-based and sustainably sourced ingredients. These products are commonly utilized in food emulsification, texture enhancement, and formulation stabilization, making them a preferred choice across large-scale manufacturing operations.

- In May 2025, the USDA projected global vegetable-oil production at 5 million metric tons for 2025/26, while consumption was expected to reach 228.9 million metric tons, with food applications accounting for 72% of total use.

Synthetic-based is the fastest-growing segment in the Polyglycerol Fatty Acid Ester Market by source. The segment experienced notable growth due to increasing demand for specialized formulations that require precise performance characteristics and enhanced functionality. Manufacturers adopted synthetic-based polyglycerol fatty acid esters in applications where consistency, stability, and controlled formulation properties are critical. The segment also benefited from ongoing product innovation across food processing, personal care, and industrial applications, where tailored ingredient solutions are becoming increasingly important.

Form Analysis

Liquid Solutions dominates the market due to ease of use and formulation flexibility

In 2025, Liquid Solutions held a dominant market position, capturing more than a 55.0% share of the Polyglycerol Fatty Acid Ester Market by form. The segment maintained its leadership due to its ease of handling, efficient mixing properties, and compatibility with a wide range of food, personal care, and pharmaceutical formulations. Manufacturers preferred liquid solutions because they can be easily incorporated into production processes, ensuring uniform distribution and consistent product quality. The form is particularly suitable for large-scale food processing applications where operational efficiency and formulation accuracy are critical.

- Codex provisions applicable in 2025 allowed the additive at levels up to 20,000 mg/kg in soybean-based beverages and oil-in-water fat emulsions, 8,000 mg/kg in cream analogues, 6,000 mg/kg in processed cream products, and 5,000 mg/kg in beverage whiteners and flavoured drinks.

Powder and Solid is the fastest-growing segment in the Polyglycerol Fatty Acid Ester Market by form. The segment experienced strong growth due to its longer shelf life, convenient storage characteristics, and ease of transportation. Manufacturers increasingly adopted powder and solid forms for applications requiring precise dosing and improved product stability during storage. The segment also benefited from growing demand across food processing and specialty ingredient applications where dry formulations are preferred for operational and logistical reasons.

Key Market Segments

By Type

- Monoglycerol Esters

- Diglycerol Esters

- Triglycerol Esters

- Higher Polyglycerol Esters

By End-Use Industry

- Food and Beverages

- Personal Care and Cosmetics

- Pharmaceuticals

- Industrial

- Others

By Source

- Vegetable Oil-based

- Synthetic-based

- Animal Fat-based

By Form

- Liquid Solutions

- Powder and Solid

- Formulated Blends

Driver Analysis

Dairy and whipped/fat-system optimization sustains specialty ester demand

The regulatory record itself points to one of the clearest functional demand pockets: U.S. regulation specifically recognizes polyglycerol esters of fatty acids for emulsifier use in dry whipped topping base, confirming continued relevance in aerated fat-and-water systems where stability, whipping performance, and dispersion quality are monetizable processing outcomes rather than cosmetic attributes.

On the demand side, Eurostat reports the EU dairy chain at very large scale, with 2024 raw milk production estimated at 161.8 million tonnes and drinking milk output at 21.9 million tonnes, while the European Commission’s dairy data portal continues to show a production base around 150 million tonnes annually; that scale supports steady demand for specialty stabilizers and emulsifiers in cream analogues, recombined systems, desserts, toppings, and fat-structured dairy formulations.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processed bakery and tortilla output scaling raises emulsifier pull-through | +1.6% | North America core, EU bakery belts, APAC urban corridors | Short term (≤ 2 years) |

| Dairy and whipped/fat-system optimization sustains specialty ester demand | +1.3% | EU core, North America core, selected APAC dairy processors | Short term (≤ 2 years) |

| EU 2023 purity tightening shifts share toward high-spec compliant suppliers | +1.1% | EU core, UK alignment spill-over, export hubs serving Europe | Medium term (2-4 years) |

| Codex and multi-jurisdiction approvals widen formulation optionality in export foods | +0.9% | EU, North America, Asia export corridors, Middle East/Africa import markets | Medium term (2-4 years) |

| Clean-label reformulation pressure favors low-dose functional emulsifier systems | +0.8% | EU reformulation-led markets, North America packaged foods, APAC premium foods | Medium term (2-4 years) |

| Higher-value texture control in confectionery, fillings, and compound fats expands mix premiumization | +0.7% | EU confectionery clusters, North America, APAC industrial foods | Long term (≥ 4 years) |

Restraint Analysis

Tightening food additive standards (FSSAI, EU, FDA)

This restraint originates from the progressive tightening and harmonization of food product and food additive standards by major regulators such as FSSAI in India, the European Commission, and the United States FDA, which are increasing the documentation and testing burden on emulsifiers like polyglycerol fatty acid esters used in beverages, bakery, confectionery, and nutrition products.

For producers, this translates into incremental regulatory compliance OPEX of roughly 2–3% of sales, plus a delay of 1–2 years in commercialization of novel Baobab‑based PGFE grades in high‑margin categories such as fortified beverages and plant‑based dairy analogues, which compresses near‑term margin uplift by 150–250 basis points and pushes CapEx payback for new lines out from 5–6 years to 7–8 years.

At a portfolio level, the stricter regulatory filters effectively cap SKU innovation throughput at perhaps 50–60% of planned launches in 2026–2028, forcing producers to allocate R&D budgets away from Baobab‑specific variants toward already‑approved generic vegetable oil‑derived PGFEs, so the restraint removes around 2 percentage points from the baseline CAGR via slower volume ramp‑up in regulated food categories and higher unit compliance cost embedded in price negotiations with FMCG customers.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening food additive standards (FSSAI, EU, FDA) | -2.0% | India core, EU, North America | Medium term (2–4 years) |

| Volatile Baobab seed oil and vegetable oil input prices | -1.5% | Sub-Saharan Africa, EU, APAC corridors | Short to medium term (≤ 4 years) |

| SPS and customs barriers on Baobab inputs | -1.2% | EU, North America, GCC | Medium term (2–4 years) |

| Limited manufacturing scale and CapEx friction | -1.0% | Global emerging corridors | Long term (≥ 4 years) |

| Slow regulatory approvals for novel uses | -0.8% | EU, North America, India | Long term (≥ 4 years) |

| Sustainability and traceability compliance costs | -0.7% | EU, UK, premium APAC | Medium to long term (≥ 3 years) |

Opportunity Analysis

Expansion into non‑food industrial applications

The upside scenario assumes targeted development of PGFE grades tailored for high‑margin categories skin‑care creams, sunscreens, crop protection emulsions and industrial cleaners where penetration could reach 10–15% of new product launches between 2026 and 2035 in North America, EU and East Asia as manufacturers seek more biobased and regulation‑friendly emulsifiers in response to tightening chemical safety rules.

If PGFE capture in non‑food applications reaches even 5% of the broader specialty ingredients volume pool by 2035, this could represent incremental annual demand growth of 3–4% in those segments, translating into roughly 1.5 percentage points of upside CAGR for the overall PGFE market as industrial revenue shares rise from single digits towards 20–25% over the forecast period. Unit economics are attractive because industrial PGFE grades can achieve operating margins of 30–35% due to higher price points, specialized performance claims and lower price sensitivity, and this diversification reduces revenue volatility compared with the baseline, which is tied largely to food processing cycles and food price indices tracked by FAO.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Clean-label PGFE reformulation platforms | +2.0% | EU, UK, North America core | Medium term (2-4 years) |

| Sustainable, agri-linked PGFE sourcing models | +1.8% | APAC emerging, Latin America, Africa | Long term (≥ 4 years) |

| Expansion into non-food industrial applications | +1.5% | North America, EU, East Asia | Medium term (2-4 years) |

| Localization with fast-growing food processing hubs | +2.3% | APAC emerging, India, MENA | Short term (≤ 2 years) |

| Regulatory-driven premium compliance segment (EU E-475/E-476) | +1.7% | EU, UK, EEA | Short term (≤ 2 years) |

| Functional nutrition and pharma-grade PGFE systems | +1.9% | North America, EU, Japan, South Korea | Long term (≥ 4 years) |

Challenges Analysis

Oil feedstock volatility

The dominant structural challenge is the cost and availability volatility of the underlying vegetable-oil and fatty-acid feedstocks used in polyglycerol fatty acid ester production, because the market is still tied to broader oilseed and vegetable-oil cycles rather than a fully insulated specialty-chemicals supply base. USDA’s 2026 outlook shows soybean oil prices remaining elevated relative to global benchmarks, while FAO’s 2026 oilseed and oilmeal indices continue to rise, indicating a persistently tight input environment that can add roughly 180 to 260 basis points of raw-material inflation to a producer’s unit cost stack during adverse procurement windows.

That translates into an estimated -1.2% CAGR friction drag because formulators face higher working-capital needs, more frequent price resets, and narrower conversion margins, especially in APAC processing hubs and EU import-reliant plants where crude-oil substitution is constrained by specification requirements. Over the next 12 to 18 months, mitigation depends on dual-sourcing, longer-duration supply contracts, and higher inventory coverage, but the sector cannot fully normalize until feedstock markets stabilize and supplier concentration is reduced.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Oil feedstock volatility | -1.2% | Global, APAC supply hubs, EU processors | Short term (≤ 2 years) |

| Traceability compliance load | -0.8% | EU regulatory hubs, North America, export markets | Medium term (2-4 years) |

| Reactor yield variability | -0.9% | Global manufacturing clusters, APAC, EU | Medium term (2-4 years) |

| Specialty talent scarcity | -0.6% | North America, EU, APAC chemical hubs | Long term (≥ 4 years) |

| Trade corridor congestion | -0.7% | APAC logistics corridors, EU import lanes, Middle East transshipment | Short term (≤ 2 years) |

| Energy cost instability | -0.8% | EU, APAC, high-cost industrial zones | Medium term (2-4 years) |

Geopolitical Impact Analysis

Global Conflicts Impacting Supply Chains and Food Ingredients

The ongoing Russia–Ukraine war and tensions in the Middle East have influenced the Polyglycerol Fatty Acid Ester (PGFE) market by affecting global supply chains, raw material availability, and food manufacturing costs. PGFE production depends on vegetable oils, fatty acids, and other food-grade ingredients that are traded internationally. Disruptions in agricultural commodity markets and transportation networks have created cost pressures for manufacturers operating across the food ingredient value chain. Supply uncertainties and logistics disruptions led food manufacturers to seek alternative sourcing strategies, resulting in fluctuations in raw material prices.

At the same time, instability in the Middle East has contributed to higher freight and shipping costs across key international trade routes. Food ingredient manufacturers have faced longer delivery times and increased transportation expenses, affecting procurement and inventory planning. Despite these challenges, demand for processed and packaged foods has remained resilient across major markets. As food companies continue focusing on supply chain diversification and ingredient security, the PGFE market is adapting through broader sourcing networks and improved operational strategies.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Polyglycerol Fatty Acid Ester Market.

Asia-Pacific dominated the market in 2025, accounting for 32.3% of the global market share. The region’s leadership is primarily supported by its large food processing industry, growing consumption of packaged foods, and expanding production of bakery, dairy, and confectionery products. Countries across the region have witnessed rising demand for processed and convenience foods due to urbanization, changing dietary habits, and increasing disposable incomes. Polyglycerol fatty acid esters are widely utilized in these applications to improve texture, stability, emulsification, and shelf life.

Europe represents a significant market driven by a mature food processing sector and stringent food quality standards. The region continues to see demand for emulsifiers in bakery, dairy, confectionery, and specialty food applications. North America also maintains a strong presence due to high consumption of processed foods and ongoing product innovation by food manufacturers. Latin America and the Middle East & Africa are emerging markets where growing urban populations and expanding food manufacturing activities are creating new opportunities for food ingredient suppliers.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global Polyglycerol Fatty Acid Ester (PGFE) Market exhibits a moderately consolidated market structure, with a limited number of multinational specialty ingredient manufacturers accounting for a significant portion of global production and supply. The market is characterized by strong competition based on product quality, formulation expertise, regulatory compliance, manufacturing capabilities, and long-term customer relationships within the food, personal care, and pharmaceutical industries. Entry barriers are relatively moderate due to the technical requirements associated with food-grade ingredient manufacturing and compliance with international food safety standards.

Key players like ocus on expanding specialty emulsifier offerings and improving product performance to address evolving customer requirements across food and non-food applications. Strategic investments in research and development, sustainable sourcing initiatives, and manufacturing efficiency continue to shape the competitive landscape. The growing demand for high-performance emulsifiers in bakery, dairy, confectionery, and personal care formulations is encouraging leading companies to strengthen their market positions through innovation and customer-focused solutions.

The Major Players in The Industry

- Lonza Group AG

- Croda International Plc

- Clariant AG

- DuPont de Nemours, Inc.

- Riken Vitamin Co., Ltd.

- Sakamoto Yakuhin Kogyo Co., Ltd.

- Spiga Nord S.p.A.

- Mohini Organics Pvt. Ltd.

- Kasco Chemtech Pvt. Ltd.

- ABITEC Corporation

- Stepan Company

- Evonik Industries AG

- BASF SE

- Kao Corporation

- Mitsubishi Chemical Group Corporation

- Others

Key Development

- In May 2026, Sakamoto Yakuhin Kogyo strengthened its polyglycerol fatty acid ester position through emulsifier portfolio expansion. Serving bakery, dairy, and confectionery sectors, the company expanded globally, improving product availability and meeting formulation requirements.

- In April 2026, Mitsubishi Chemical advanced its specialty ingredients through innovation, sustainability, and process optimization. They enhanced food, healthcare, and industrial functionality while strengthening collaborations, improving operational efficiency, and reinforcing its market position.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 430.1 Mn |

| Forecast Revenue (2035) | USD 580.6 Mn |

| CAGR (2026-2035) | 3.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Monoglycerol Esters, Diglycerol Esters, Triglycerol Esters, and Higher Polyglycerol Esters), By End-Use Industry (Food and Beverages, Personal Care and Cosmetics, Pharmaceuticals, Industrial, and Others), By Source (Vegetable Oil-based, Synthetic-based, and Animal Fat-based), and By Form (Liquid Solutions, Powder and Solid, and Formulated Blends) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Lonza Group AG, Croda International Plc, Clariant AG, DuPont de Nemours, Inc., Riken Vitamin Co., Ltd., Sakamoto Yakuhin Kogyo Co., Ltd., Spiga Nord S.p.A., Mohini Organics Pvt. Ltd., Kasco Chemtech Pvt. Ltd., ABITEC Corporation, Stepan Company, Evonik Industries AG, BASF SE, Kao Corporation, Mitsubishi Chemical Group Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |