Quick Navigation

Report Overview

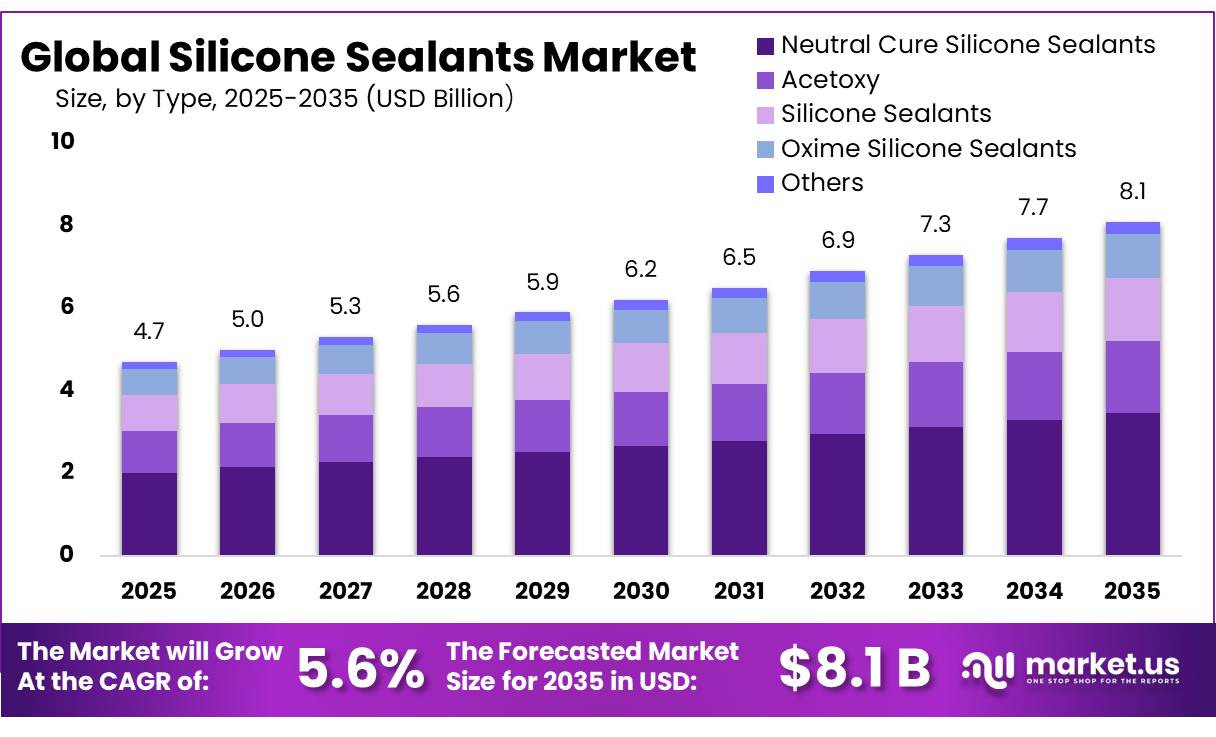

The Global Silicone Sealants Market size is expected to be worth around USD 8.1 Billion by 2035, from USD 4.7 Billion in 2025, growing at a CAGR of 5.6% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 46.80% share, holding USD 2.1 Billion revenue.

Silicone sealants are used to seal joints, gaps, façades, glass, metal, concrete, bathrooms, electronics, vehicles, and industrial equipment because they stay flexible, resist UV, handle temperature changes, and give long service life. In 2025–2026, the industry is being supported mainly by construction, renovation, energy-efficient buildings, EVs, electronics, and infrastructure spending.

Key Takeaways

- Silicone Sealants Market size is expected to be worth around USD 8.1 Billion by 2035, from USD 4.7 Billion in 2025, growing at a CAGR of 5.6%.

- Neutral Cure Silicone Sealants held a dominant market position, capturing more than a 42.80% share of the Silicone Sealants market.

- Room Temperature Vulcanizing (RTV) held a dominant market position, capturing more than a 66.20% share of the Silicone Sealants market.

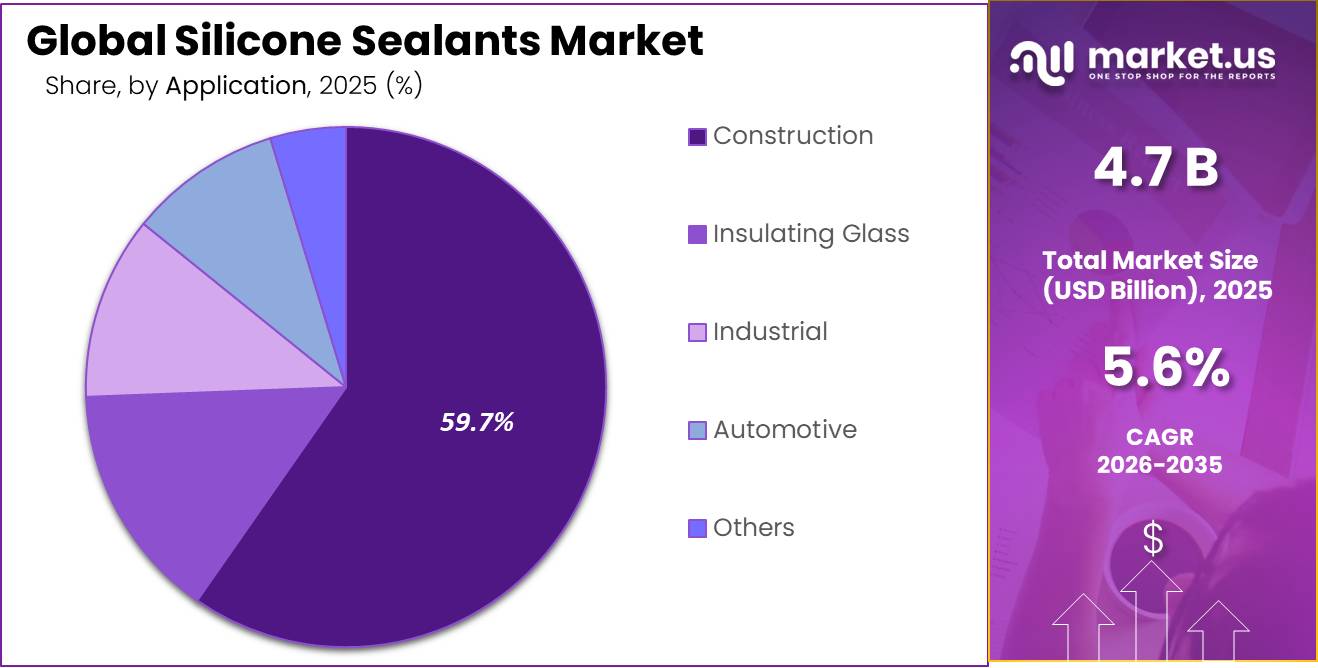

- Construction held a dominant market position, capturing more than a 59.70% share of the Silicone Sealants market.

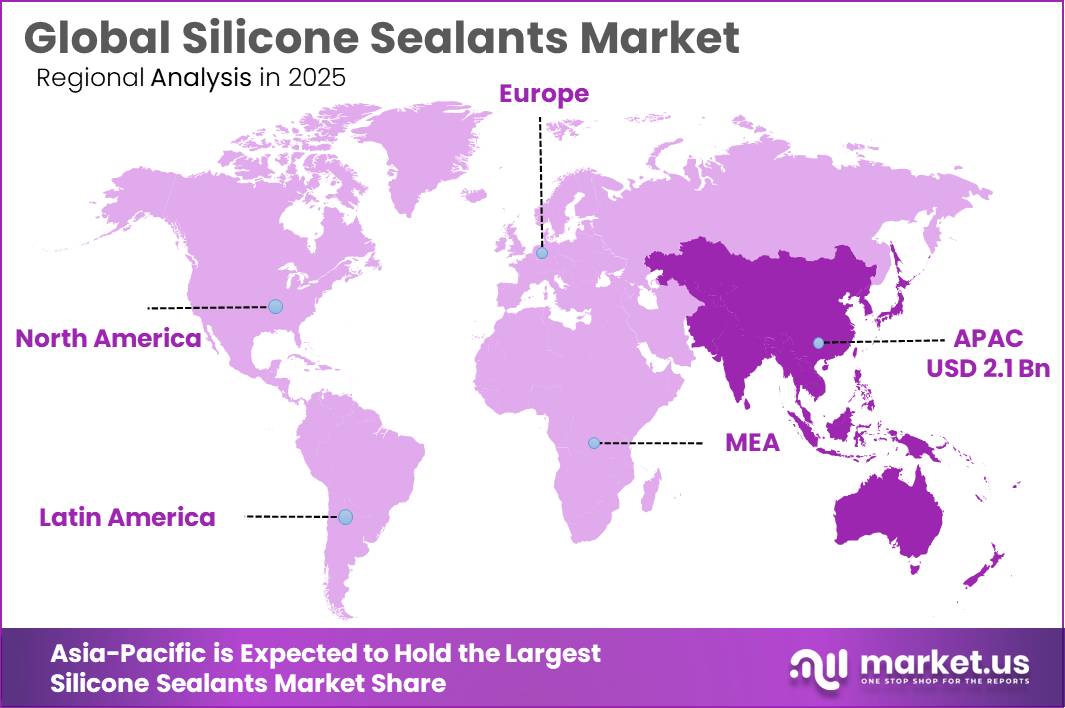

- Asia-Pacific held the dominant position in the Silicone Sealants market, accounting for more than 46.80% of the global market and reaching a value of USD 2.1 Billion.

In the U.S., construction spending reached an annual rate of USD 2,172.4 billion in April 2026, while first-four-month spending was USD 657.2 billion, showing a large base of sealant-consuming projects. EV growth is also important because silicone sealants are used in batteries, sensors, electronics protection, and thermal management; IEA reported electric car sales exceeded 20 million units in 2025, equal to 25% of global car sales.

The industrial scenario remains positive as construction activity continues to support sealant consumption. In the U.S., construction spending reached an annual rate of USD 2,172.4 billion in April 2026, 0.9% higher than April 2025, showing steady demand from residential, commercial and public building work. Silicone sealants benefit from this trend because they are used in façade weatherproofing, structural glazing, expansion joints and repair work.

Key growth drivers include rising urban construction, stricter building energy rules, renovation of older buildings, and higher demand for low-VOC, durable and climate-resistant materials. The EU Energy Performance of Buildings Directive, adopted in 2024, is pushing renovation and efficiency upgrades, while the IEA notes that residential buildings make up about 70% of building energy demand, creating long-term scope for insulation, window sealing and façade improvement products.

Huntsman International LLC is more connected to the broader adhesives, polyurethane, coatings, sealants, and construction-material ecosystem. Its 2025 annual filing notes applications in coatings, adhesives, sealants and elastomers, while its construction portfolio supports flooring, roofs, walls, façades, doors, windows, roads, bridges, and pipes. Huntsman reported USD 5.683 billion revenue in 2025, compared with USD 6.036 billion in 2024, reflecting softer construction and industrial demand.

By Type Analysis

Neutral Cure Silicone Sealants dominate with 42.80% share due to strong weather resistance and broad construction compatibility.

In 2025, Neutral Cure Silicone Sealants held a dominant market position, capturing more than a 42.80% share of the Silicone Sealants market. This leadership was supported by their ability to cure without releasing acidic by-products, making them highly suitable for sensitive substrates such as metals, coated surfaces, natural stone, plastics, and modern façade materials. Compared with conventional curing technologies, neutral cure formulations offer lower corrosion risk and better long-term adhesion, which has increased their use across commercial construction, glazing, industrial assembly, and infrastructure projects.

By Technology Analysis

Room Temperature Vulcanizing (RTV) dominates with 66.20% share due to easy application and strong performance across construction and industrial uses.

In 2025, Room Temperature Vulcanizing (RTV) held a dominant market position, capturing more than a 66.20% share of the Silicone Sealants market. The segment maintained its leadership because of its ability to cure at normal ambient conditions without requiring additional heat or specialized processing equipment. This characteristic made RTV silicone sealants highly practical for large-scale construction activities, industrial assembly operations, glazing systems, automotive sealing, and general maintenance applications.

By Application Analysis

Construction dominates with 59.70% share due to growing demand for durable, weather-resistant, and long-life sealing solutions.

In 2025, Construction held a dominant market position, capturing more than a 59.70% share of the Silicone Sealants market. The segment maintained its leadership due to the extensive use of silicone sealants across residential, commercial, and infrastructure development projects. Silicone sealants became a preferred material for construction applications because of their strong adhesion, flexibility, and ability to maintain performance under changing environmental conditions. These properties made them widely suitable for sealing joints, glazing systems, façades, windows, doors, roofing structures, and expansion gaps.

Key Market Segments

By Type

- Neutral Cure Silicone Sealants

- Acetoxy

- Silicone Sealants

- Oxime Silicone Sealants

- Others

By Technology

- Room Temperature Vulcanizing (RTV)

- Thermoset or Heat Cured

- Pressure Sensitive

- Radiation Cured

By Application

- Construction

- Insulating Glass

- Industrial

- Automotive

- Others

Emerging Trends

Growing Use of Low-VOC and Food-Safe Silicone Sealants in Modern Food Infrastructure

One of the latest trends shaping the Silicone Sealants market is the increasing adoption of low-VOC (low volatile organic compound) and food-safe silicone solutions across food processing and storage facilities. Food manufacturers are upgrading plants to improve hygiene, reduce maintenance requirements, and support long-term environmental goals.

Governments and regulatory agencies are encouraging modern food infrastructure through sustainability and food safety initiatives linked to reduced emissions and improved operational performance. As a result, manufacturers are introducing advanced silicone formulations designed for cleaner indoor environments and long service life. This shift toward low-emission and food-compatible sealing materials is emerging as an important trend supporting long-term market expansion in industrial and food-related construction applications.

Expansion of Cold Chain and Hygienic Facility Construction Supporting Advanced Silicone Sealant Adoption

Food organizations continue highlighting the need to reduce losses across the supply chain. FAO estimates show that improving storage and preservation infrastructure remains essential because food loss continues to affect global efficiency and resource use. Government-backed food modernization programs and sustainability initiatives are encouraging investment in refrigerated warehouses, processing centers, and packaging facilities.

Silicone sealants are increasingly selected for these projects because they maintain performance under temperature variation and reduce repair frequency. The growing emphasis on sustainable facility construction and efficient food handling is creating stronger demand for next-generation sealing materials across industrial applications. This trend is expected to continue as industries focus on reducing waste, extending asset life, and improving food safety standards globally.

Drivers

Growth in Food Processing and Hygienic Infrastructure Demand Supporting Silicone Sealants

One of the major driving factors for the Silicone Sealants market is the rapid expansion of food processing facilities and the increasing focus on hygienic production environments. Silicone sealants are widely used in food plants because they offer strong resistance to moisture, temperature changes, cleaning chemicals, and long operating life. These properties help maintain sealed joints in processing units, cold storage facilities, packaging areas, and food-grade production lines.

The global food industry continues to expand at a strong pace. According to the Food and Agriculture Organization (FAO), global food production will need to increase by nearly 50% by 2050 compared with 2012 levels to meet rising consumption demand. This growth requires large investments in food manufacturing infrastructure, storage facilities, and processing equipment where silicone sealants play an important role in maintaining sanitation and operational efficiency.

Expansion of Cold Chain and Food Packaging Facilities Increasing Use of Silicone Sealants

Another important growth driver for Silicone Sealants is the expansion of cold-chain logistics and food packaging infrastructure worldwide. Food industries are investing heavily in refrigerated warehouses, processing plants, and packaging units to reduce waste and improve food quality. These facilities require sealing solutions that can tolerate low temperatures, water exposure, and repeated cleaning cycles.

According to the Food and Agriculture Organization (FAO), around 14% of food produced globally is lost before reaching retail stages, which has encouraged governments and industries to improve storage and preservation systems. Improved cold storage and processing infrastructure increases the use of silicone sealants in insulated panels, refrigeration systems, food-grade equipment, and facility construction. In parallel, regulatory focus on hygiene and contamination control has encouraged manufacturers to adopt materials that remain stable across varying environmental conditions.

Restraints

Strict Food Safety and Environmental Compliance Increasing Operational Costs for Silicone Sealants

One major restraining factor for the Silicone Sealants market is the growing pressure from food safety standards and environmental compliance requirements. Silicone sealants are widely used in food processing units, cold storage systems, packaging infrastructure, and hygienic construction areas because they provide moisture resistance and long service life. However, manufacturers are facing higher costs to meet food-contact regulations, product certification requirements, low-emission standards, and sustainability targets.

Food industries are placing stronger focus on reducing contamination and improving production efficiency. According to the Food and Agriculture Organization (FAO), around 13.2% of food is lost globally in supply chains after harvest and before retail, while an additional 19% is wasted at retail, food service, and household levels. To reduce these losses, governments and food industries continue investing in upgraded food infrastructure and stricter material performance standards.

High Raw Material and Processing Costs Limiting Adoption Across Food Infrastructure Projects

Another important restraint affecting the Silicone Sealants market is the rising cost of raw materials and advanced processing technologies. Silicone sealants deliver excellent durability and performance, but their production requires specialized formulations and manufacturing processes that increase final product pricing compared with alternative sealing materials.

The food sector is increasingly investing in storage and preservation systems to reduce product losses. According to FAO estimates, nearly 14% of food produced globally is lost between harvest and retail stages, creating pressure to improve cold chains, storage facilities, and processing plants valued at approximately USD 400 billion in annual food losses. Governments and international organizations continue supporting infrastructure modernization to improve efficiency and reduce waste.

Opportunity

Expansion of Food Processing and Cold Storage Infrastructure Creating Long-Term Demand for Silicone Sealants

One major growth opportunity for the Silicone Sealants market comes from the rapid expansion of food processing plants and cold storage infrastructure across global markets. Silicone sealants are increasingly used in food-grade facilities because they provide strong resistance to moisture, temperature variation, cleaning chemicals, and long operating life. These characteristics make them suitable for sealing joints, refrigeration units, insulated panels, processing lines, and hygienic construction areas.

According to the Food and Agriculture Organization (FAO), the global food system must produce nearly 50% more food by 2050 compared with 2012 levels to meet future demand. This target is encouraging governments and food industries to invest in modern processing facilities and storage networks. At the same time, the United Nations Environment Programme (UNEP) estimates that around 1.05 billion tonnes of food were wasted globally in 2022, highlighting the need for improved preservation and storage systems.

Rising Investment in Sustainable Food Packaging and Hygienic Facility Development

Another major opportunity for Silicone Sealants is linked to increasing investment in sustainable packaging systems and hygienic food manufacturing environments. Food producers are focusing on reducing waste, improving shelf life, and strengthening facility performance through advanced materials and modern infrastructure.

Silicone sealants are gaining attention because they offer flexibility, weather resistance, and durability in high-moisture conditions without frequent replacement. They are increasingly used in insulated food facilities, processing equipment, packaging support structures, and refrigerated logistics centers. As investment in food preservation and sustainable infrastructure continues to rise, silicone sealant manufacturers have an opportunity to expand product adoption and strengthen their position across long-term industrial applications.

Regional Insights

Asia-Pacific dominates the Silicone Sealants market with 46.80% share, valued at USD 2.1 Billion, supported by large-scale construction and industrial expansion.

In 2025, Asia-Pacific held the dominant position in the Silicone Sealants market, accounting for more than 46.80% of the global market and reaching a value of USD 2.1 Billion. The region maintained leadership due to continued growth across construction, infrastructure development, manufacturing activities, and urban expansion. Rising investment in residential and commercial projects created strong demand for high-performance sealing materials that deliver durability, flexibility, and long-term weather protection.

The region’s market strength was supported by increasing use of silicone sealants in façade systems, glazing applications, expansion joints, roofing structures, and industrial assembly operations. Rapid urban development and the growing adoption of energy-efficient building practices encouraged wider use of advanced sealant technologies across both public and private sector projects.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Dow remains one of the prominent participants in the Silicone Sealants market through its broad portfolio of construction, industrial, and specialty silicone solutions. In 2025, the company continued focusing on high-performance sealants designed for durability, weather resistance, and long service life across glazing, façade, infrastructure, and industrial applications. Dow reported 2025 net sales of approximately USD 42.9 billion and continued investment in performance materials and customer-focused product development.

Huntsman International LLC maintains a presence in sealants and specialty materials through advanced formulation capabilities and industrial material solutions. In 2025, the company continued supporting construction and industrial markets with performance-driven chemical technologies. Huntsman reported approximately USD 5.9 billion in annual revenue and maintained operations across more than 25 countries. The company’s focus on product efficiency, application performance, and sustainable material development supports its position in the broader silicone and specialty sealants landscape.

Mapei continues to expand its position in the Silicone Sealants market through construction chemicals and sealing technologies. In 2025, the company emphasized sealants for building envelopes, waterproofing systems, and infrastructure applications. Mapei operates through 100+ subsidiaries and manufacturing facilities across 35+ countries. The company generated annual revenue exceeding EUR 4 billion, supported by investments in sustainable construction products and technical innovation for modern building requirements.

Top Key Players Outlook

- Dow

- Huntsman International LLC

- Shin-Etsu Chemical Company

- Mapei

- Wacker Chemie AG

- H.B. Fuller

- 3M

- Tremco Incorporated

- Bostik

- Sika AG

- Henkel Corporation

Recent Industry Developments

In financial terms, H.B. Fuller reported 2025 net revenue of USD 3.47 billion, adjusted EBITDA of USD 621 million, and an adjusted EBITDA margin of 17.9%, showing stable earnings support for product development and expansion. For investment and expansion, the company highlighted its global reach across 150 countries, more than 30 market segments, and over 7,100 employees in 2026.

In 2025, 3M increased innovation activity in 2025, launching 70 new products in Q3 and targeting more than 250 launches for the full year, supporting wider material-science applications across industrial bonding and sealing. Financially, 3M reported full-year 2025 GAAP sales of USD 24.9 billion, while its Q4 2025 sales reached USD 6.1 billion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.7 Bn |

| Forecast Revenue (2035) | USD 8.1 Bn |

| CAGR (2026-2035) | 5.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Neutral Cure Silicone Sealants, Acetoxy, Silicone Sealants, Oxime Silicone Sealants, Others), By Technology (Room Temperature Vulcanizing (RTV), Thermoset or Heat Cured, Pressure Sensitive, Radiation Cured), By Application (Construction, Insulating Glass, Industrial, Automotive, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Dow, Huntsman International LLC, Shin-Etsu Chemical Company, Mapei, Wacker Chemie AG, H.B. Fuller, 3M, Tremco Incorporated, Bostik, Sika AG, Henkel Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |