Quick Navigation

Report Overview

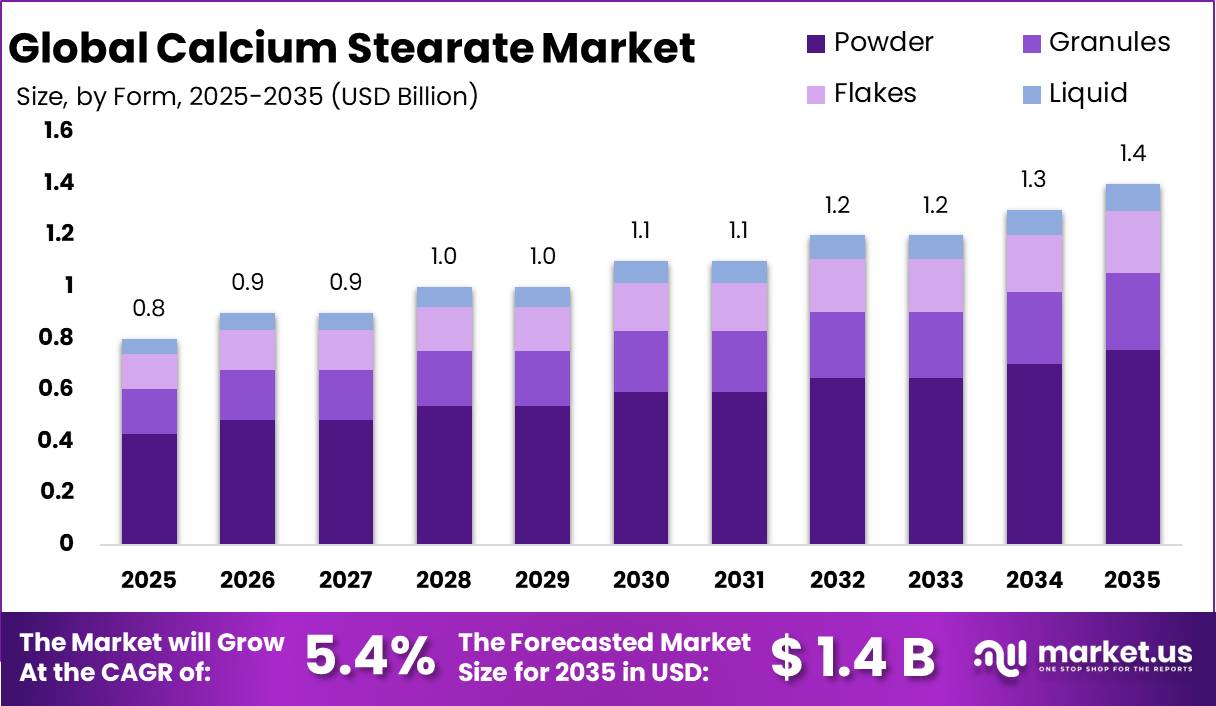

The Global Calcium Stearate Market size is expected to be worth around USD 1.4 Billion by 2035, from USD 0.8 Billion in 2025, growing at a CAGR of 5.4% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 45.80% share, holding USD 22.3 Billion revenue.

Calcium stearate is a white, hydrophobic metallic soap produced from stearic acid and calcium salts. It is used as a lubricant, mold-release agent, acid scavenger, anti-caking additive, and water-repellent additive in plastics, rubber, construction materials, coatings, paper, food-contact materials, and pharmaceuticals. In regulated food applications, the U.S. FDA lists calcium stearate under 21 CFR §184.1229 as the calcium salt of stearic acid derived from edible sources, with use under good manufacturing practice.

Key Takeaways

- Calcium Stearate Market size is expected to be worth around USD 1.4 Billion by 2035, from USD 0.8 Billion in 2025, growing at a CAGR of 5.4%.

- Powder held a dominant market position, capturing more than a 53.90% share in the global Calcium Stearate market.

- Plastics held a dominant market position, capturing more than a 39.30% share in the global Calcium Stearate market.

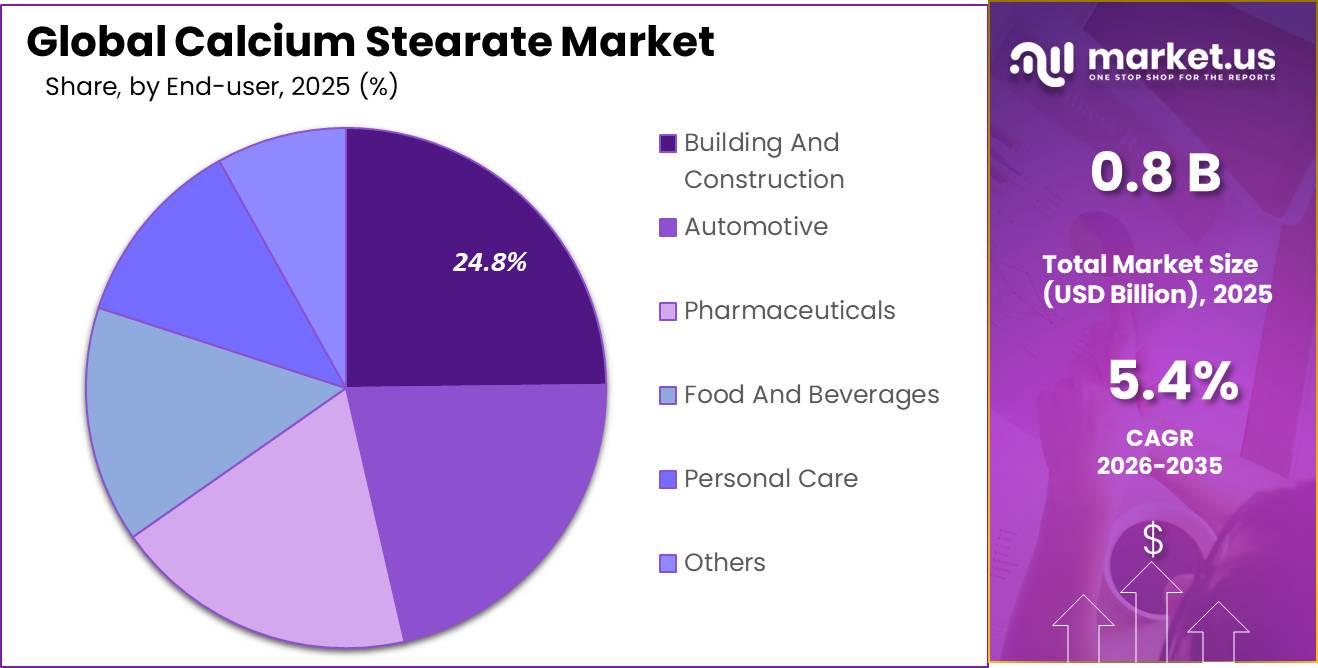

- Building And Construction held a dominant market position, capturing more than a 24.80% share in the global Calcium Stearate market.

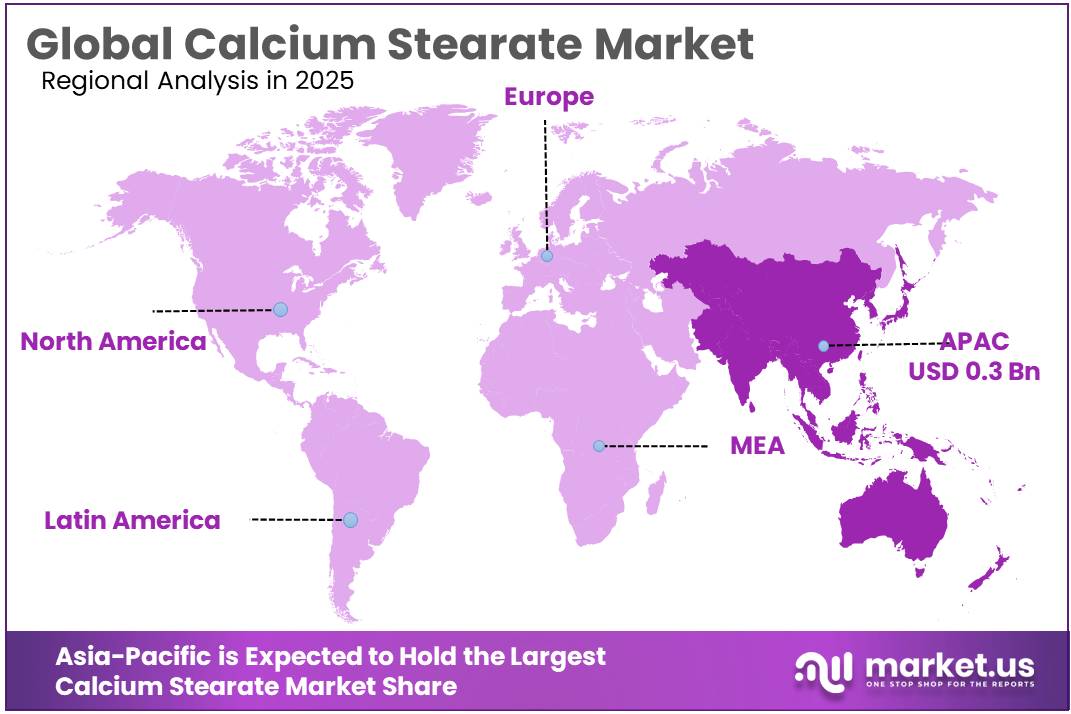

- Asia-Pacific held the dominant position in the global Calcium Stearate market, accounting for 43.50% of total market share and reaching a market value of USD 0.3 Billion.

The industrial scenario remains positive because calcium stearate is linked with large downstream sectors such as polymers, PVC processing and construction chemicals. Plastics Europe reported that Europe’s share in global plastics production declined from 22% in 2006 to 12% in 2024, while circular plastics represented 15.4% of European plastics production in 2024.

This shows pressure on producers to improve processing efficiency, recycling compatibility and additive performance. Cefic also reported that the European chemical industry generated EUR 635 billion turnover and employed 1.2 million people, while Europe held 13% of global chemical sales and China held 46%.

In the United States, the chemical industry remains a large downstream base, with the American Chemistry Council reporting USD 673 billion generated annually by the business of chemistry and 547,000 direct jobs. Construction also supports demand, as U.S. construction spending reached an annual rate of USD 2,172.4 billion in April 2026, with USD 657.2 billion spent in the first four months of 2026.

The main driving factor for calcium stearate is the shift toward safer, multifunctional additives in PVC, polymer compounding and construction materials. It helps reduce friction during extrusion and molding, improves release performance, supports heat-stable processing and reduces moisture penetration in cement-based products.

Demand is also linked to sustainability regulation, as the buildings and construction sector accounts for around 37% of global CO₂ emissions and nearly 50% of global material extraction, increasing the need for durable, long-life and performance-enhancing construction chemicals. Calcium stearate is used in construction for waterproofing and hydrophobic performance, and European renovation policy targets 35 million building renovations by 2030, which can support demand for additives used in building materials, coatings, pipes, profiles, sealants, and cement-related applications.

Recent Development 2025: In May 2025, Baerlocher was reported to plan a MYR 220 million metallic stearate manufacturing plant in Malaysia, with projected capacity of 30 kta for calcium-zinc stearates and expected operations in 2027.

By Form Analysis

Powder dominates with 53.90% due to its ease of handling, uniform dispersion, and broad industrial compatibility.

In 2025, Powder held a dominant market position, capturing more than a 53.90% share in the global Calcium Stearate market. This strong position was supported by the material’s wide acceptance across plastics, rubber, construction materials, pharmaceuticals, and chemical processing industries where consistent blending and smooth processing are important. Powder-form Calcium Stearate remains preferred because of its fine particle structure, which allows faster mixing, better dispersion, and improved production efficiency across large-scale industrial operations.

By Application Analysis

Plastics dominate with 39.30% due to their extensive use of Calcium Stearate for smoother processing and improved product performance.

In 2025, Plastics held a dominant market position, capturing more than a 39.30% share in the global Calcium Stearate market. This leadership was mainly supported by the material’s strong role as a lubricant, acid neutralizer, and processing aid in plastic manufacturing. Calcium Stearate is widely used during polymer production because it improves flow characteristics, reduces friction during processing, and helps manufacturers achieve consistent product quality across large production volumes.

By End-User Industry Analysis

Building and Construction dominates with 24.80% due to increasing use of Calcium Stearate in construction materials and process improvement applications.

In 2025, Building And Construction held a dominant market position, capturing more than a 24.80% share in the global Calcium Stearate market. The segment maintained its leading position due to the growing use of Calcium Stearate in construction-related materials where moisture resistance, processing support, and surface performance are important. Its application across cement-based products, coatings, sealants, and construction compounds continued to support steady demand throughout the year.

Key Market Segments

By Form

- Powder

- Granules

- Flakes

- Liquid

By Application

- Plastics

- Rubber

- Construction

- Personal Care

- Pharmaceuticals

- Food

- Others

By End-User Industry

- Building And Construction

- Automotive

- Pharmaceuticals

- Food And Beverages

- Personal Care

- Others

Market Dynamics

Driver Analysis - Rising Demand from Processed Food and Packaging Industries

One of the major driving factors for Calcium Stearate is the steady expansion of the processed food and food packaging industries, where the material is widely used as an anti-caking agent, lubricant, and processing aid. Calcium stearate is approved for controlled food-related applications and supports smoother production by improving powder flow, reducing sticking, and maintaining product consistency in manufacturing operations. It is commonly used in bakery premixes, seasoning blends, powdered ingredients, and food-contact plastic applications.

- According to the food sector data referenced across industry and regulatory sources, food-grade calcium stearate usage exceeded 6,500 metric tons globally in 2023, mainly supported by powdered food production and storage applications. In addition, food manufacturers are increasingly adopting additives that improve operational efficiency while maintaining product quality standards. Calcium stearate contributes by lowering moisture-related clumping and enabling more stable processing conditions in large-scale production facilities.

Government-backed food safety frameworks and manufacturing modernization programs are also supporting this demand trend. Regulatory acceptance of fatty acid salts for food processing applications has strengthened their industrial use. The U.S. Department of Agriculture (USDA) recognizes salts of fatty acids for defined food-processing applications, supporting wider acceptance in industrial food production systems.

Packaging expansion further supports calcium stearate demand because food-grade plastics require processing additives that improve molding performance and thermal stability. Industry estimates indicate the global packaging additives sector is expected to increase from US$630 million in 2025 to US$857 million by 2032, reflecting continued investment in advanced food packaging materials and processing technologies. Calcium stearate remains important in these value chains because it improves surface quality, supports faster production cycles, and helps maintain consistency in food-contact materials.

Restraint Analysis - Increasing Food Additive Regulations Limiting Market Expansion

One of the major restraining factors affecting the growth of the Calcium Stearate market is the increasing regulatory attention on food additives and ingredient transparency across global food processing industries. Although Calcium Stearate is permitted for use in specific applications and controlled concentrations, manufacturers continue to face stricter compliance requirements related to formulation approval, labeling standards, and safety assessments. These evolving regulations increase production complexity and can slow product approvals across end-use industries.

Food producers are increasingly adapting to changing consumer expectations for cleaner ingredient labels and reduced additive use. As a result, manufacturers are reassessing formulation strategies and limiting dependency on processing aids where possible. This trend has created pressure on ingredient suppliers to demonstrate performance, traceability, and regulatory compliance while maintaining production efficiency.

- According to the European Food Safety Authority (EFSA), a structured re-evaluation program was established to reassess 315 food additives that were authorized in the European Union before January 2009, with more than 70% of evaluations already completed. These ongoing reviews have encouraged food manufacturers to strengthen documentation, testing, and reformulation activities before maintaining or expanding additive usage. Such regulatory scrutiny increases operational costs and extends commercialization timelines for additive-based formulations.

Additional pressure is also coming from food labeling policies and government-backed transparency initiatives. The U.S. Food and Drug Administration (FDA) continues to support updated food labeling practices to improve consumer understanding of ingredients used in processed food products. As ingredient disclosure becomes more detailed, manufacturers are becoming more selective in additive adoption decisions.

Opportunity Analysis - Expanding Sustainable Polymer Processing Creates Future Demand

One major growth opportunity for Calcium Stearate is its increasing use in sustainable polymer processing and next-generation plastic manufacturing. As industries move away from heavy-metal stabilizers and adopt cleaner production methods, calcium stearate is gaining attention because it works as a lubricant, acid scavenger, release agent, and processing stabilizer across plastics, packaging, construction materials, and specialty compounds.

The opportunity is becoming stronger because global plastics production and processing continue to expand while environmental regulations become stricter. According to the Organisation for Economic Co-operation and Development, plastics remain essential across industrial manufacturing and continue to be widely used because of their versatility and cost efficiency. At the same time, the United Nations Environment Programme reported that more than 13,000 substances have been associated with plastics and over 3,200 substances show hazardous characteristics, increasing pressure on manufacturers to shift toward safer and lower-impact chemical systems.

Government and regulatory action is also opening opportunities. Regulatory restrictions on lead-based stabilizers in several industrial regions are encouraging producers to adopt alternative additive systems. Industry reports show that plastics applications continue to represent one of the largest end-use areas for calcium stearate because of its role in stabilization and lubrication during polymer conversion.

Emerging Trend - Eco-Friendly PVC Stabilizer Systems Shape Market Direction

According to the International Food Information Council (IFIC) 2024 Food & Health Survey, around 62% of consumers reported paying attention to ingredients listed on food labels when making food purchasing decisions. This consumer behavior is encouraging manufacturers to redesign formulations and strengthen ingredient communication while continuing to maintain production efficiency. The trend is influencing suppliers to provide more traceable and application-specific additive solutions.

Calcium Stearate is gaining attention because it helps improve flow performance, processing stability, and equipment efficiency without requiring major production redesign. Chemical producers are increasingly investing in additives that support longer equipment life and more controlled manufacturing environments. At the same time, industrial users are looking for materials that align with circular production practices and stricter environmental standards.

Government and regulatory initiatives are also supporting this transition. The European Food Safety Authority (EFSA) continues to review and monitor approved food additives to ensure safe use across food categories and strengthen consumer confidence in ingredient systems. These frameworks are encouraging food manufacturers to adopt better documentation and more transparent production practices.

According to the Organisation for Economic Co-operation and Development (OECD), the chemical industry is expected to quadruple globally between 2020 and 2060, highlighting the need for more efficient and sustainable chemical management systems as production scales further. The OECD also reports that its Mutual Acceptance of Data (MAD) framework helps save approximately EUR 309 million annually by reducing duplicate chemical testing and supporting more efficient market access. These developments are encouraging producers to prioritize smarter chemical formulations and performance-driven additives.

Regional Insights

Asia-Pacific dominated the Calcium Stearate market with a 43.50% share, reaching USD 0.3 Billion

In 2025, Asia-Pacific held the dominant position in the global Calcium Stearate market, accounting for 43.50% of total market share and reaching a market value of USD 0.3 Billion. The region maintained leadership due to its strong manufacturing ecosystem, expanding plastics production, rising construction activities, and growing industrial processing capabilities across major economies. Calcium Stearate continues to see extensive usage in plastics, rubber, building materials, pharmaceuticals, and selected food-related processing applications, supporting consistent regional demand.

The region benefits from large-scale industrial output and continuous infrastructure expansion. According to the United Nations Industrial Development Organization (UNIDO), Asia remains the largest global manufacturing region, contributing a significant portion of worldwide industrial production. Strong industrial activity supports continuous demand for processing additives and specialty chemicals such as Calcium Stearate.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Baerlocher GmbH remains one of the strongest participants in the calcium stearate industry through its long-standing specialization in metallic stearates, PVC stabilizers, and polymer additives. Its calcium stearate portfolio supports applications including acid scavenging, lubrication, release agents, waterproofing, and thermal stabilization across plastics and construction materials. Recent expansion initiatives included increased metallic stearate capacity and reported plans for a MYR 220 million (approximately USD 52 million) investment in Malaysia targeting 30 kta calcium-zinc stearate production capacity with operations planned from 2027 onward.

Dover Chemical Corporation is recognized in calcium stearate and metallic stearates through its Doverlube product line serving plastics, rubber, and engineered materials. Through its parent organization’s industrial network, Dover operates within a business generating more than USD 8 billion annual revenue globally. The company continues to strengthen additive performance solutions for polymer processors focusing on operational efficiency and sustainable formulation development.

Top Key Players Outlook

- Baerlocher GmbH

- Dover Chemical Corporation

- FACI Corporate S.p.A.

- Shandong Repolyfine Additives Co., Ltd.

- Valtris Specialty Chemicals (US)

- Peter Greven GmbH & Co. KG (DE)

- Fujian Sannong Calcium Carbonate Co., Ltd.

- Allan Chemical Corporation

- Norac Additives

- PMC Biogenix

Recent Industry Developments

For 2025 partnership activity, Valtris expanded its collaboration with Transfar Group on September 16, 2025, focused on sustainable polymer solutions and TCPP supply, after a 2024 technology-license agreement linked to barium stabilizers.

In 2025/2026, Shandong Repolyfine Additives’ work in the calcium stearate sector appears focused more on PVC additives, lubricant systems, and capacity-backed product supply rather than public mergers or acquisitions. The company is based in Zibo, Shandong, was founded in 2016, and operates with about 51–200 employees, serving PVC additives such as lubricants, stabilizers, processing aids, impact modifiers, OPE wax, and related polymer additives.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 0.8 Bn |

| Forecast Revenue (2035) | USD 1.4 Bn |

| CAGR (2026-2035) | 5.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Powder, Granules, Flakes, Liquid), By Application (Plastics, Rubber, Construction, Personal Care, Pharmaceuticals, Food, Others), By End-User Industry (Building And Construction, Automotive, Pharmaceuticals, Food And Beverages, Personal Care, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Baerlocher GmbH, Dover Chemical Corporation, FACI Corporate S.p.A., Shandong Repolyfine Additives Co., Ltd., Valtris Specialty Chemicals (US), Peter Greven GmbH & Co. KG (DE), Fujian Sannong Calcium Carbonate Co., Ltd., Allan Chemical Corporation, Norac Additives, PMC Biogenix |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |