Quick Navigation

Report Overview

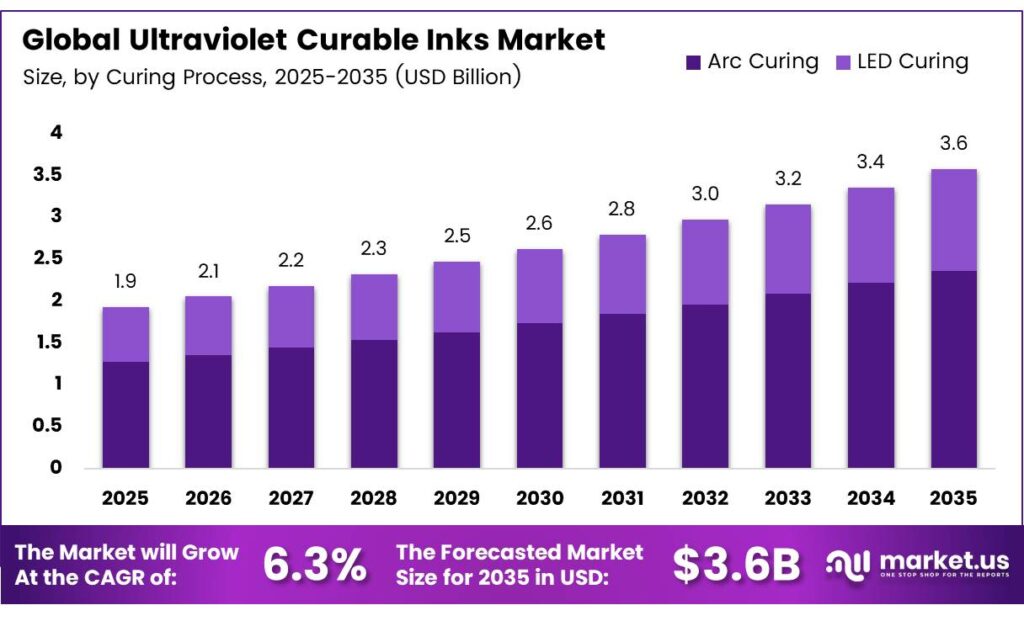

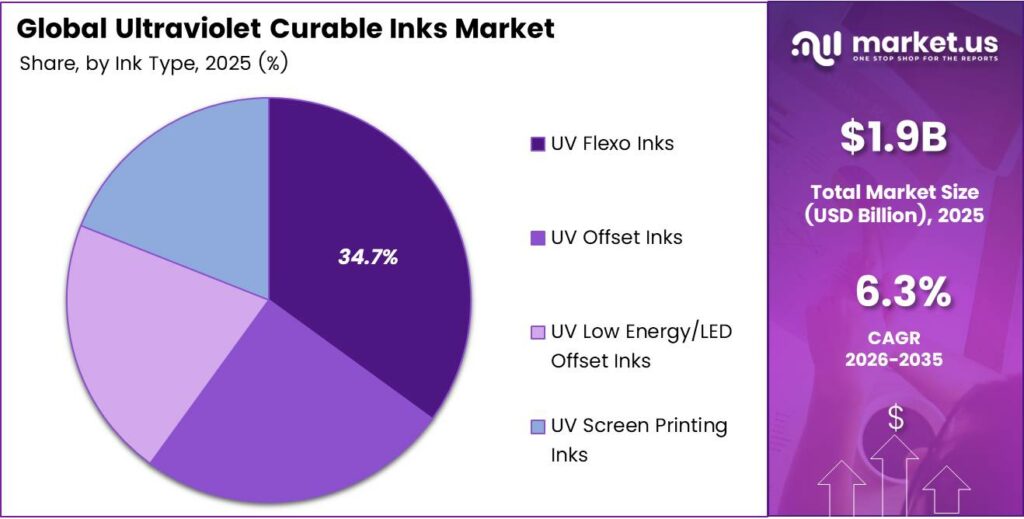

The Global Ultraviolet Curable Inks Market size is expected to be worth around USD 3.6 billion by 2035 from USD 1.9 billion in 2025, growing at a CAGR of 6.3% during the forecast period 2026 to 2035.

UV curable inks cure instantly when exposed to ultraviolet light, eliminating drying time and enabling high-speed production. Packaging, labeling, and commercial printing industries adopt these inks because they deliver sharper print quality and faster throughput than solvent-based alternatives. This technical advantage makes them a preferred choice across industrial printing applications.

The shift toward instant-curing ink systems is not merely a performance upgrade — it signals a fundamental change in how manufacturers approach printing line economics. Facilities that replace conventional ink systems with UV curable formulations reduce both energy costs and floor space requirements, since UV curing units occupy less physical footprint than thermal drying tunnels.

UV-curable inks for can printing are 100% solids and release zero VOC emissions. This characteristic removes the compliance burden entirely for can manufacturers operating in regulated markets, making UV curable inks the technically and commercially superior choice for metal substrate printing.

The Bobst M5 press equipped with UV LED curing consumed approximately 60% less electricity than its conventional predecessor, saving approximately 84,000 kWh per year and demonstrating that UV LED integration delivers measurable sustainability performance at the press level on commercially available equipment.

Key Takeaways

- The Global Ultraviolet Curable Inks Market was valued at USD 1.9 billion in 2025 and is forecast to reach USD 3.6 billion by 2035 at a CAGR of 6.3% over the forecast period 2026 to 2035.

- Arc Curing dominates with a 65.2% market share in 2025.

- UV Flexo Inks lead with a 34.7% share in 2025.

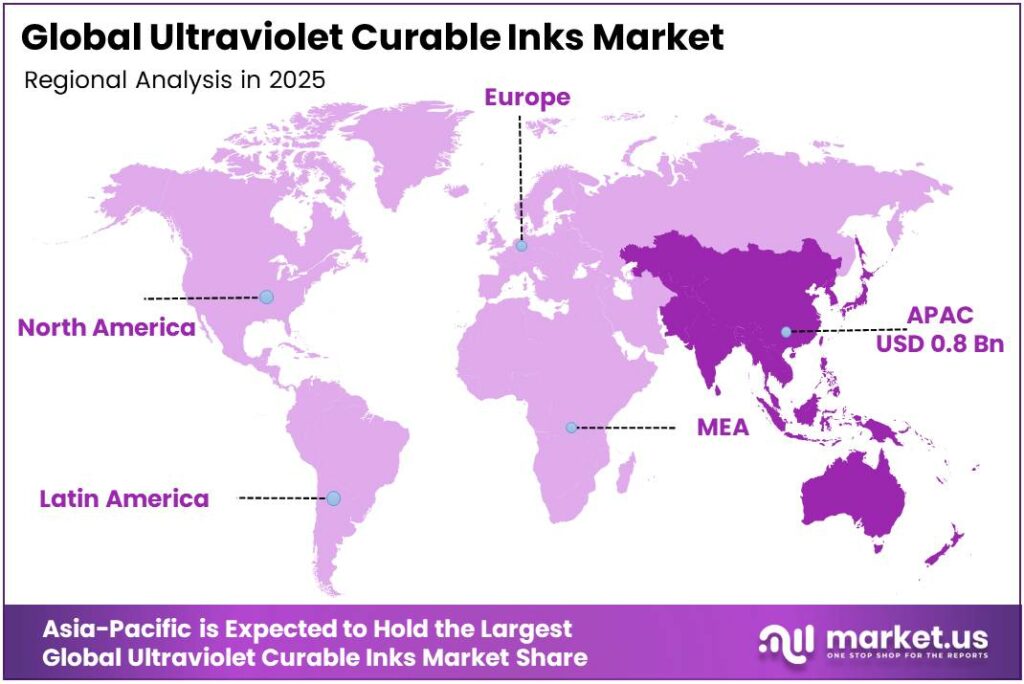

- Asia-Pacific holds the largest regional share at 39.5%, valued at USD 0.8 billion in 2025.

By Curing Process

Arc Curing dominates with 65.2% due to established infrastructure and broad substrate compatibility.

In 2025, Arc Curing held a dominant market position in the By Curing Process segment of the Ultraviolet Curable Inks Market, with a 65.2% share. Its dominance reflects decades of industrial deployment across commercial printing, packaging, and labeling lines where mercury arc lamp infrastructure is already installed and operational. Replacing proven equipment remains commercially unattractive for many large-scale operators.

LED curing is gaining growing strategic importance as energy economics shift against mercury arc systems. LED-based curing draws less power, generates no ozone, and lasts significantly longer per installation cycle — advantages that appeal to facilities under pressure to reduce operating costs and environmental footprints. However, LED curing still trails in installed base, which constrains its near-term volume share.

By Ink Type

UV Flexo Inks dominate with 34.7% due to dominance in flexible packaging production lines.

In 2025, UV Flexo Inks held a dominant market position in the By Ink Type segment of the Ultraviolet Curable Inks Market, with a 34.7% share. Flexographic printing remains the primary production method for high-volume label and flexible packaging runs, and UV-curable flexo formulations deliver the adhesion and color consistency that converters demand. This structural dependency on flexo in packaging keeps UV Flexo Inks at the top of the ink type hierarchy.

UV Offset Inks serve commercial sheet-fed and web offset printers seeking faster throughput than conventional ink-water systems allow. These formulations cure on-press without infrared drying, shortening makeready time and reducing substrate distortion — advantages that matter most in high-quality publication and carton printing environments where color accuracy is non-negotiable.

UV Low Energy/LED Offset Inks differentiate through compatibility with LED curing units, enabling printers to convert existing offset presses without full infrastructure overhauls. These formulations absorb and react at the specific wavelengths LED systems emit, making them essential to the growing segment of printers transitioning to lower-energy curing while preserving their capital investment in press hardware.

Key Market Segments

By Curing Process

- Arc Curing

- LED Curing

By Ink Type

- UV Flexo Inks

- UV Offset Inks

- UV Low Energy/LED Offset Inks (Except UV Offset Inks)

- UV Screen Printing Inks

Emerging Trends

LED UV Curing, Sustainable Formulations, and Nanotechnology Reshape UV Ink Performance Standards

LED UV curing technology is redefining the efficiency benchmark for ultraviolet ink systems. The LeoLED2 delivers up to 44 W/cm² UV irradiance with over 40,000-hour diode life — a combination that slashes replacement cycles and total ownership costs. Printers that adopt LED systems gain a durable infrastructure advantage that compounds over time.

Bio-based and sustainable UV curable ink formulations are advancing from niche to mainstream consideration. Formulators now develop plant-derived monomers and oligomers that reduce dependence on petrochemical inputs without compromising cure speed or adhesion. This shift responds directly to brand owner sustainability commitments, which increasingly influence ink purchasing decisions at the converter level.

Low migration inks for food packaging and nanotechnology-enhanced formulations represent two converging frontiers. Industrial UV LED systems typically last 20,000 to 30,000 hours, which is approximately 5 to 10 years of operational life. This durability, combined with nanoparticle-enhanced pigment dispersion, points toward UV inks that deliver both regulatory compliance and superior print resolution simultaneously.

Drivers

Energy Efficiency, Environmental Compliance, and Flexible Packaging Demand Accelerate UV Curable Ink Adoption

UV curable inks cure instantly without heat, eliminating the thermal drying infrastructure that conventional ink systems require. Their Nexus II UV LED systems provide up to 85% energy savings compared with mercury-vapor UV lamps. This level of operational reduction changes the investment calculus for printing facilities evaluating technology upgrades — payback periods compress significantly.

Flexible packaging and labeling markets are structural demand anchors for UV curable formulations. Brand owners require inks that maintain adhesion, color stability, and regulatory compliance across substrates ranging from polyethylene films to metalized laminates. UV curable systems deliver consistent performance across this substrate diversity, which solvent-based alternatives cannot match reliably at production speeds.

Digital printing expansion reinforces UV ink demand from a different angle. As converters invest in UV inkjet presses to handle short-run, variable-data, and personalized packaging orders, compatible UV formulations become a prerequisite rather than a preference. This parallel growth in UV-compatible press installations creates a durable, multi-year pipeline for UV ink suppliers.

Restraints

High Equipment Costs and Substrate Limitations Constrain UV Curable Ink Adoption Among Smaller Operators

UV curing equipment demands significant upfront capital investment. Specialized lamps, power supplies, press modifications, and safety enclosures add costs that smaller printing operations cannot easily absorb. A flexographic press retrofit reduced electricity use from 198,000 kWh per year to 58,000 kWh per year — but reaching those savings requires the initial conversion expenditure, which remains a barrier for budget-constrained converters.

Substrate compatibility creates a technical ceiling on UV ink deployment. Heat-sensitive films, certain coated papers, and low-surface-energy plastics resist UV ink adhesion or distort under curing lamp intensity. This limits the substrate range a UV-converted press can handle, forcing printers to maintain parallel conventional ink systems — increasing complexity and negating some of the efficiency gains that motivated conversion.

Together, these cost and compatibility constraints slow market penetration among small and mid-size printers who represent the largest segment by operator count. Until equipment costs decline and formulation breadth expands across difficult substrates, UV curable inks will face adoption resistance in this numerically significant buyer cohort — capping near-term volume growth below its technical potential.

Growth Factors

3D Printing, Electronics, Medical, Textile, and Automotive Applications Open New Revenue Channels for UV Curable Inks

UV curable inks are entering additive manufacturing workflows where photopolymer-based 3D printing requires precise, fast-curing inkjet formulations. This application category demands UV inks with specific viscosity, reactivity, and layer-bonding properties — creating a premium formulation segment with margins that exceed standard packaging ink categories. Early movers building UV ink portfolios for 3D applications gain specification advantages in a market with high switching costs.

Electronics printing represents another high-value expansion path. Printed circuits, display components, and flexible electronics require inks with electrical conductivity, thermal stability, and precision deposition — all achievable with engineered UV-curable systems. A UV LED retrofit generated over €38,000 per year in total operating savings per printer, and UV LED installation eliminated approximately 200 tons of CO₂ annually — making the environmental and financial case simultaneously for electronics manufacturers.

Medical device coatings, automotive surface treatments, and textile printing add further diversification to the UV ink addressable market. Each specialty application demands customized formulations with specific cure profiles, substrate adhesion, and regulatory compliance — creating sustained R&D demand and long-term supply relationships. These sectors collectively reduce UV ink suppliers’ dependence on the cyclical packaging and commercial print markets.

Regional Analysis

Asia-Pacific Dominates the Ultraviolet Curable Inks Market with a Market Share of 39.5%, Valued at USD 0.8 Billion

Asia-Pacific commands 39.5% of the global UV curable inks market, valued at USD 0.8 billion in 2025. China, Japan, South Korea, and India collectively house the world’s largest concentration of packaging converters, electronics manufacturers, and commercial printing operations — all of which are primary end-users of UV curable formulations. This industrial density creates structural, self-reinforcing demand.

North America maintains a mature UV curable inks base anchored by stringent VOC regulations and early technology adoption across the packaging and commercial print sectors. US and Canadian converters operate under EPA and provincial air quality mandates that make solvent-free UV inks the default compliance solution. This regulatory structure sustains consistent UV ink consumption independent of discretionary investment cycles.

Europe’s UV curable inks demand is shaped by the European Union’s REACH regulations and aggressive packaging sustainability targets. Food packaging producers across Germany, France, Italy, and the UK prioritize low migration UV formulations that comply with food contact material legislation. This compliance-driven specification process gives formulators with certified low-migration product lines a measurable commercial advantage in European tender processes.

Latin America represents a developing but capital-constrained market for UV curable inks. Brazil and Mexico lead regional adoption, driven by expanding consumer goods packaging sectors and multinational brand owner requirements for consistent print quality. However, high equipment import costs and limited local UV curing infrastructure slow broader market penetration beyond the largest converters.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ALTANA positions itself as a specialty chemistry-led UV ink innovator, concentrating on formulation science that delivers performance advantages in demanding print environments. Its investment in photo-initiator chemistry and sustainable raw material sourcing targets the segment of converters where regulatory compliance and ink performance carry equal weight in purchasing decisions.

APV Engineered Coatings focuses on industrial UV-curable coating applications that extend beyond standard printing into protective and functional surface treatments. This positioning allows APV to compete in specialty markets — including automotive and electronics coatings — where technical specification requirements reduce price sensitivity and create longer-term supply relationships than commodity packaging inks generate.

artience Co. Ltd. (TOYO INK CO., LTD.) leverages its parent group’s integrated pigment and resin manufacturing capability to develop UV ink formulations with controlled color performance across substrates. This vertical integration gives artience a cost and quality consistency advantage in high-volume Asian packaging markets, where maintaining ink-to-ink color matching across long production runs is a key converter requirement.

Avery Dennison Corporation approaches the UV ink space through its label materials and pressure-sensitive product ecosystem, where UV-curable inks serve as an integral component of finished label performance. This systems-level positioning, linking substrate, adhesive, and ink into a validated combination, reduces converter specification risk and creates multi-product commercial relationships that competitors selling ink alone cannot easily replicate.

Key Players

- ALTANA

- APV Engineered Coatings

- artience Co. Ltd. (TOYO INK CO., LTD.)

- Avery Dennison Corporation

- DIC Corporation

- Flint Group

- FUJIFILM Corporation

- Huber Group

- Marabu GmbH & Co. KG

- MIMAKI ENGINEERING CO., LTD.

Recent Developments

- In 2025, ALTANA’s ECKART division won the ALTANA Innovation Award for a new UV-curing printing ink formulation using PVD-based METALURE effect pigments, aimed at efficient, sustainable packaging printing and indirect food-contact applications.

- In 2025, APV offers UV-readable inks for tire and rubber manufacturing; the ink appears clear until exposed to UV light, is co-curable, UV laser readable, and designed for strong adhesion without mold fouling. APV was recognized among North America’s Top 25 coatings manufacturers; the company highlighted growth in contract manufacturing/private label coatings and advanced industrial coating solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.9 Billion |

| Forecast Revenue (2035) | USD 3.6 Billion |

| CAGR (2026-2035) | 6.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Curing Process (Arc Curing, LED Curing), By Ink Type (UV Flexo Inks, UV Offset Inks, UV Low Energy/LED Offset Inks, UV Screen Printing Inks) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | ALTANA, APV Engineered Coatings, artience Co. Ltd. (TOYO INK CO., LTD.), Avery Dennison Corporation, DIC Corporation, Flint Group, FUJIFILM Corporation, Huber Group, Marabu GmbH & Co. KG, MIMAKI ENGINEERING CO., LTD. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |