Quick Navigation

Report Overview

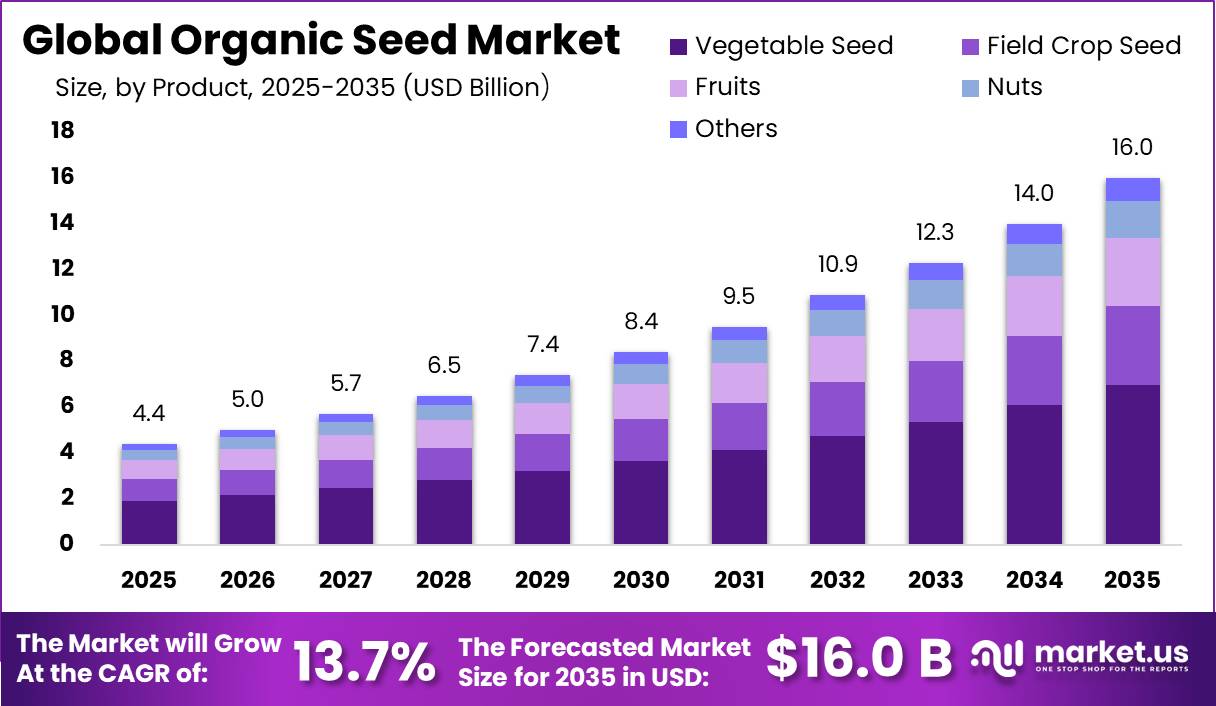

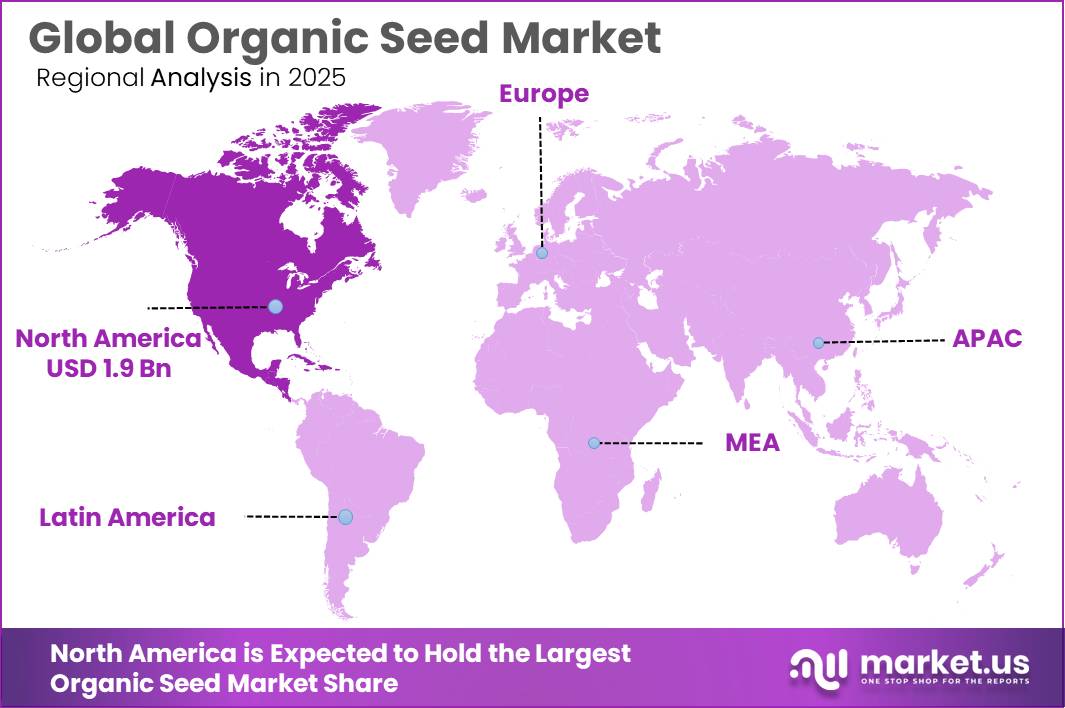

The Global Organic Seed Market size is expected to be worth around USD 16.0 Billion by 2035, from USD 4.4 Billion in 2025, growing at a CAGR of 13.7% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 43.3% share, holding USD 1.9 Billion revenue.

Organic seed is positioned as a critical input for certified organic farming, because growers must use organically grown seed where commercially available under USDA organic rules. The industry is supported by the wider organic sector: global organic farmland reached nearly 99 million hectares in 2023, covering 2.1% of agricultural land, with 4.3 million organic producers and €136.4 billion in organic food sales.

Key Takeaways

- Organic Seed Market size is expected to be worth around USD 16.0 Billion by 2035, from USD 4.4 Billion in 2025, growing at a CAGR of 13.7%.

- Vegetable Seed held a dominant market position, capturing more than a 43.7% share in the Organic Seed Market.

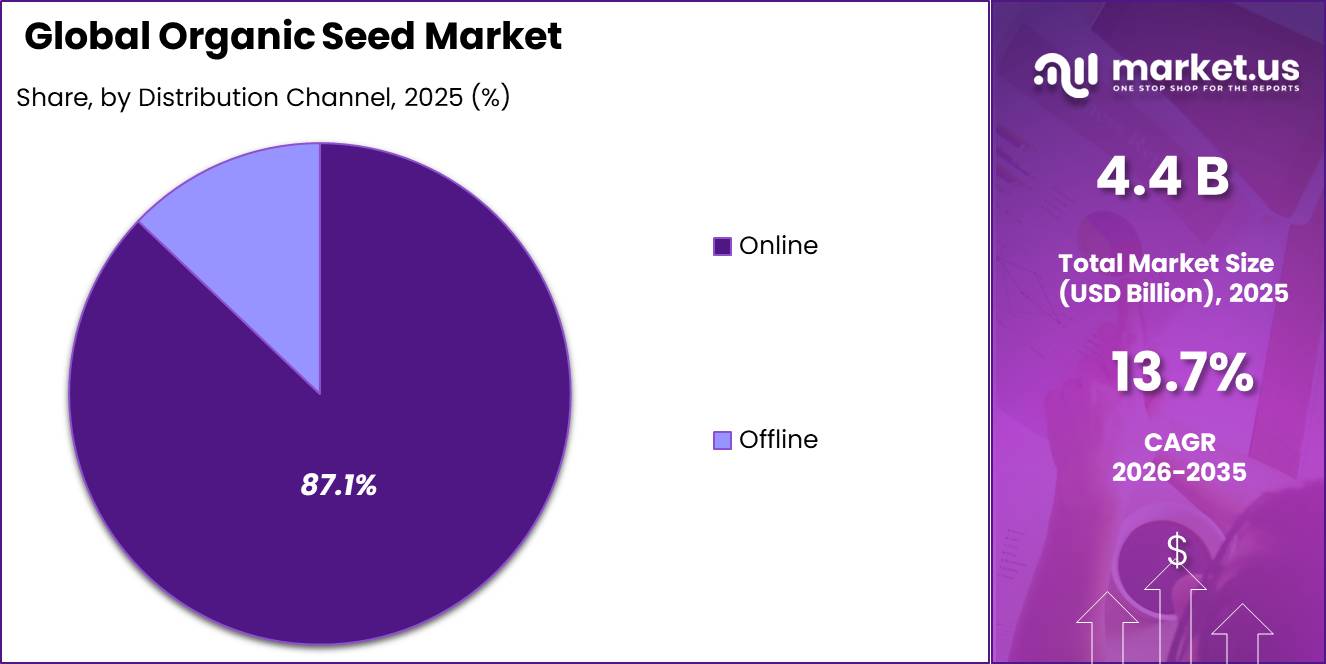

- Online held a dominant market position, capturing more than a 87.1% share in the Organic Seed Market.

- North America held a dominant position in the Organic Seed Market, accounting for 43.3% of the global market and reaching a value of USD 1.9 Billion.

The industrial scenario is shaped by rising demand for traceable, non-GMO, untreated, and climate-resilient seed varieties. In the U.S., organic food sales reached US$65.4 billion in 2024, and produce represented 33% of organic food sales, creating direct demand for organic vegetable, herb, grain, and cover-crop seeds. Companies such as Seeds of Change and Fedco Seeds, Inc. operate in this value chain through certified-organic, heirloom, biodiversity-focused, and non-GMO seed offerings. Seeds of Change states that it began in 1989 to protect biodiversity through organic food and seeds, while Fedco was founded in 1978 and serves more than 21,000 consumers, farmers, and retailers.

Key growth drivers include organic acreage expansion, stricter certification systems, seed biodiversity concerns, and public transition funding. USDA’s Organic Transition Initiative is a US$300 million multi-agency effort supporting farmers through the 36-month transition period required before land can be certified organic.

In Europe, policy pressure is stronger: the EU targets 25% of agricultural land under organic farming by 2030, while non-organic seed derogations are scheduled to be phased out by 31 December 2036, supporting long-term demand for fully organic seed supply. Seeds of Change states that it offers 100% certified organic seeds, has operated as a trusted brand for more than 30 years, and positions itself as the oldest pure organic seed company in the U.S.

Seeds of Change operates as a long-established organic seed brand offering certified-organic vegetable, herb, and flower seeds. The company states that its seeds are 100% organic and 100% non-GMO, and that the brand has operated for more than 30 years. Fedco Seeds, founded in 1978, is a worker- and consumer-owned cooperative supplying seeds, trees, tubers, and garden supplies, with reported service to more than 21,000 consumers, farmers, and retailers.

By Product Analysis

Vegetable Seed dominates with 43.7% share due to strong demand from commercial farming and year-round vegetable cultivation

In 2025, Vegetable Seed held a dominant market position, capturing more than a 43.7% share in the Organic Seed Market by product segment. This leadership was supported by the growing preference for organically cultivated vegetables across both developed and emerging agricultural regions. Vegetable seeds continued to attract strong demand because of their direct connection to food consumption patterns, increasing awareness around chemical-free produce, and rising cultivation of vegetables under organic farming systems.

By Distribution Channel Analysis

Online dominates with 87.1% share driven by easy access, wider product availability, and growing digital purchasing habits

In 2025, Online held a dominant market position, capturing more than a 87.1% share in the Organic Seed Market by distribution channel. The segment’s strong position was supported by the increasing shift of farmers, growers, and agricultural buyers toward digital purchasing platforms for seed procurement. Online channels offered greater convenience, broader product visibility, easier comparison of seed varieties, and direct access to organic seed suppliers, making purchasing decisions faster and more efficient.

Key Market Segments

By Product

- Vegetable Seed

- Field Crop Seed

- Fruits

- Nuts

- Others

By Distribution Channel

- Online

- Offline

Emerging Trends

Rising Demand for Climate-Resilient Organic Seeds

A major latest trend in the organic seed sector is the growing demand for climate-resilient seed varieties. Farmers are looking for organic seeds that can perform better under heat, drought, irregular rainfall, and new pest pressure. This trend is becoming stronger because organic farming is expanding worldwide. FiBL and IFOAM reported that global organic farmland reached 98.9 million hectares in 2023, growing by 2.6%, while organic food sales crossed €136 billion. This wider organic base is pushing seed suppliers to focus more on varieties that are not only certified organic but also practical for changing farm conditions.

Government Support Is Encouraging Organic Seed Use

Government support is also helping this trend move forward. In the U.S., the USDA’s Organic Transition Initiative is a $300 million program designed to support farmers shifting to organic production and strengthen organic markets. Since organic crops usually need 36 months of land management without prohibited synthetic inputs before certification, farmers need reliable seeds early in the transition period. This is increasing interest in organic seeds that can reduce crop risk and support stable yields. As a result, organic seed development is moving beyond basic certification and toward stronger, locally adapted varieties that help farmers manage real field challenges.

Drivers

Growing Demand for Sustainable and Chemical-Free Agriculture

One of the biggest driving factors behind the growth of organic seed is the increasing demand for sustainable and chemical-free farming. Farmers and consumers today are becoming more aware of how food is produced and how farming practices affect soil, water, and long-term food security. Organic seeds are produced without synthetic chemicals and are designed to perform better in organic farming systems, making them an important starting point for clean agriculture.

The numbers show this change clearly. According to FAO and the 2024 edition of The World of Organic Agriculture, organic farming is now practiced in 188 countries, with more than 96 million hectares of agricultural land managed organically by at least 4.5 million farmers worldwide. Global sales of organic food and drinks reached almost EUR 135 billion in 2022. These figures reflect how consumer demand is encouraging farmers to shift toward organic methods, which naturally increases the need for organic seeds.

Government Support and Seed Diversity Are Expanding Organic Seed Adoption

Another strong reason for the rise of organic seed use is growing policy support and efforts to protect agricultural biodiversity. Governments and international food organizations increasingly recognize that seeds are not only an input for farming but also a foundation for resilient food systems.

FAO explains that quality seed systems support food security, rural development, and long-term agricultural sustainability. Organic seed helps preserve crop diversity and encourages varieties that can adapt to local climate conditions. In India and several other countries, organic farming initiatives continue to support reduced chemical dependence and healthier soil management.

Studies reviewed through FAO highlight that organic farming can improve soil quality, lower external input use, and create opportunities for rural income growth when managed effectively. This shift is encouraging more farmers to choose organic seed because they see value not only in production, but also in protecting land for future generations.

Restraints

Limited Availability of Certified Organic Seed

One of the biggest restraining factors for the organic seed industry is the limited availability of certified organic seed across many crop types and growing regions. Organic farming rules in several countries require growers to use certified organic seed whenever it is available, but supply does not always match production needs.

This creates delays in planting decisions and limits wider adoption of organic farming systems. Since 2002, producers operating under the USDA National Organic Program have been required to use organic seed when it is commercially available. However, when an equivalent organic variety cannot be sourced, farmers may request permission to use untreated conventional seed instead.

According to guidance adopted by the USDA National Organic Standards Board, producers must document attempts to source organic seed and are generally expected to contact at least three organic seed suppliers before using non-organic alternatives. This requirement shows that availability remains a real operational issue. Industry discussions in 2025 also noted that large-scale farms continue to face difficulty securing organic seed for grains, cover crops, and some vegetable categories because supply remains inconsistent across regions.

Compliance Burden and Higher Operational Complexity

Another important restraint is the amount of documentation and compliance needed to maintain organic seed use. Organic production systems depend on traceability, certification records, supplier verification, and annual review processes. While these standards help protect product integrity, they also increase the time and administrative effort required for both growers and seed suppliers.

Government guidance requires producers to maintain updated commercial availability records as part of each organic system plan review and provide evidence that organic seed was unavailable before exceptions are granted. In addition, certified organic farms must continue documenting sourcing decisions every year to remain compliant.

Opportunity

Expansion of Organic Farming Areas Creates Strong Growth Opportunity for Organic Seed

One of the biggest growth opportunities for the organic seed industry is the continued expansion of organic farming land across the world. As more farmers move toward chemical-free and environmentally responsible agriculture, the need for certified organic seed naturally increases. Organic farming begins with the seed, which means growth in organic cultivated area directly creates demand for organic seed production and distribution.

This growth creates a long-term opportunity for organic seed suppliers because every additional hectare requires seed adapted to organic standards. Governments and agricultural agencies continue encouraging sustainable farming practices, creating space for stronger organic seed systems and more local seed production.

Government Support for Sustainable Agriculture Opens New Paths for Organic Seed Development

Another important opportunity comes from government initiatives and public programs that promote sustainable agriculture and strengthen food systems. Many countries are supporting farming methods that reduce chemical use, improve soil health, and increase agricultural resilience. Organic seed becomes an important part of these efforts because seed quality influences productivity and environmental outcomes from the beginning of the crop cycle.

According to FAO, sustainable food and agriculture policies are increasingly focusing on biodiversity protection, climate resilience, and improved agricultural inputs. In India, programs supporting natural and organic farming have encouraged awareness and adoption among farming communities. FAO also highlights that stronger seed systems help improve long-term food security and farmer livelihoods. As governments continue investing in sustainable agriculture, opportunities increase for local organic seed production, breeding programs, and improved access to certified seed. This creates not only market expansion but also supports more stable and environmentally responsible farming systems for future generations.

Regional Insights

North America dominated the Organic Seed Market with a 43.3% share, reaching USD 1.9 Billion through strong organic farming adoption and established seed infrastructure

In 2025, North America held a dominant position in the Organic Seed Market, accounting for 43.3% of the global market and reaching a value of USD 1.9 Billion. The region’s leadership was supported by its well-established organic agriculture ecosystem, increasing consumer preference for organic food products, and the presence of advanced seed production and distribution networks. Organic farming practices across the region continued to expand as growers focused on improving sustainability, soil quality, and long-term agricultural productivity.

The United States remained the primary contributor to regional growth due to strong organic food consumption and large-scale certified organic cultivation. Canada also supported regional market development through continued expansion of organic acreage and growing participation in sustainable farming systems. The region benefits from mature regulatory frameworks that encourage organic certification and maintain production standards across agricultural supply chains.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Fedco Seeds operates through a cooperative business structure and has developed a strong position among regional and organic growers. Established in 1978, the company is structured with approximately 60% customer ownership and 40% employee ownership, creating a community-led operating model. Fedco specializes in vegetable seeds, seed potatoes, trees, bulbs, and varieties adapted to shorter growing seasons. The company also supports non-GMO agriculture through participation in the Safe Seed Pledge, strengthening its identity within sustainable seed supply.

Seed Savers Exchange represents one of the strongest preservation-focused organizations in the organic and heirloom seed landscape. Founded in 1975, the organization now includes more than 13,000 members worldwide and has distributed over 1 million seed samples covering more than 20,000 endangered varieties. Its operations are supported through 890 acres at Heritage Farm in the United States, where rare varieties are regenerated and conserved. The organization’s preservation model strengthens genetic diversity and long-term seed resilience.

Top Key Players Outlook

- Seeds of Change

- Fedco Seeds, Inc.

- Johnny’s Selected Seeds

- Seed Savers Exchange

- High Mowing Organic Seeds

- Wild Garden Seed

- Vitalis Organic Seeds

- HILD Samen

- Fleuren

- Navdanya

- De Bolster

Recent Industry Developments

In 2026, Johnny’s continued product development with a “New for 2026” range that included 36+ additional items shown on its new-products page, including organic tomato seed, organic seed potatoes, flowers, lettuce, and melon varieties. For partnership and expansion, a 2026 University of New Hampshire update confirmed Johnny’s long-running partnership of more than 40 years with UNH, including co-located plant development work at the Macfarlane Research Greenhouses for zinnia breeding.

In 2025, High Mowing Organic Seeds continued to work as an independent, farm-based organic seed company focused on 100% certified organic and non-GMO seeds for growers and gardeners. Its 2025 catalog included more than 750 organic vegetable, herb and flower varieties, with a record 65 new varieties and growing supplies, showing clear new product development. The company also continued partnership-led sourcing, stating in 2025 that it had worked with Genesis Seeds for around 30 years, while its reseller guide shows expansion through hundreds of retail partners.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.4 Bn |

| Forecast Revenue (2035) | USD 16.0 Bn |

| CAGR (2026-2035) | 13.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Vegetable Seed, Field Crop Seed, Fruits, Nuts, Others), By Distribution Channel (Online, Offline) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Seeds of Change, Fedco Seeds, Inc., Johnny’s Selected Seeds, Seed Savers Exchange, High Mowing Organic Seeds, Wild Garden Seed, Vitalis Organic Seeds, HILD Samen, Fleuren, Navdanya, De Bolster |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |