Quick Navigation

Report Overview

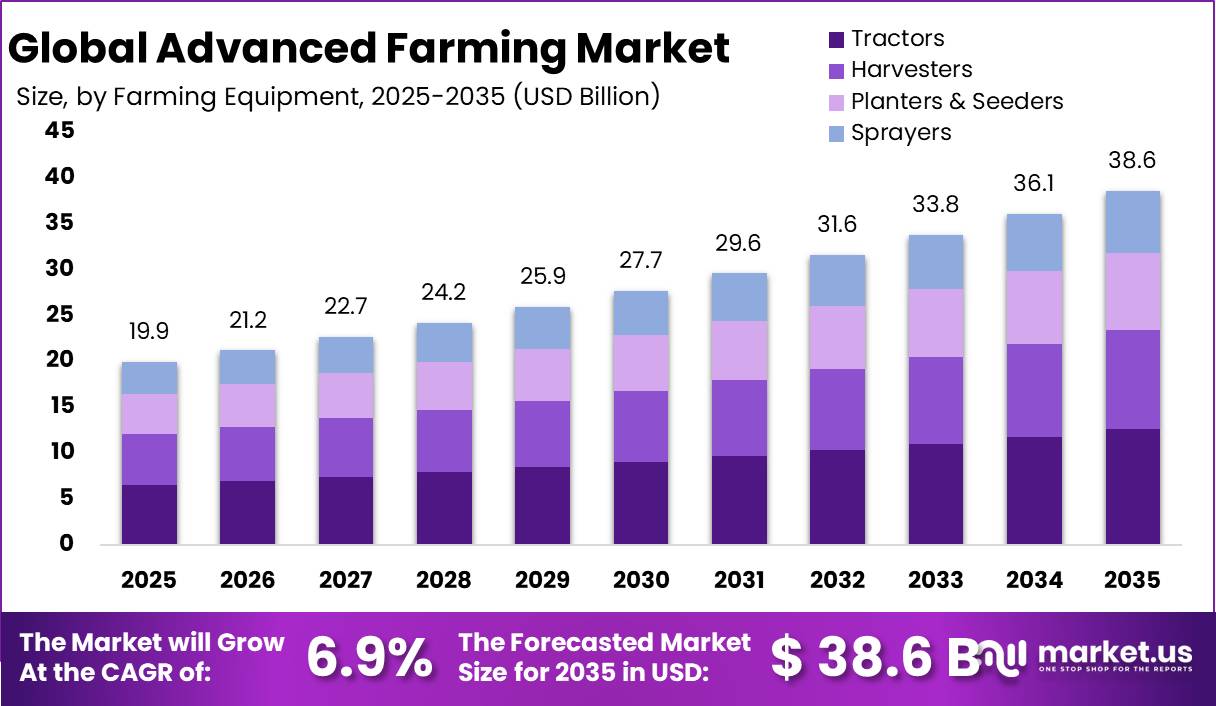

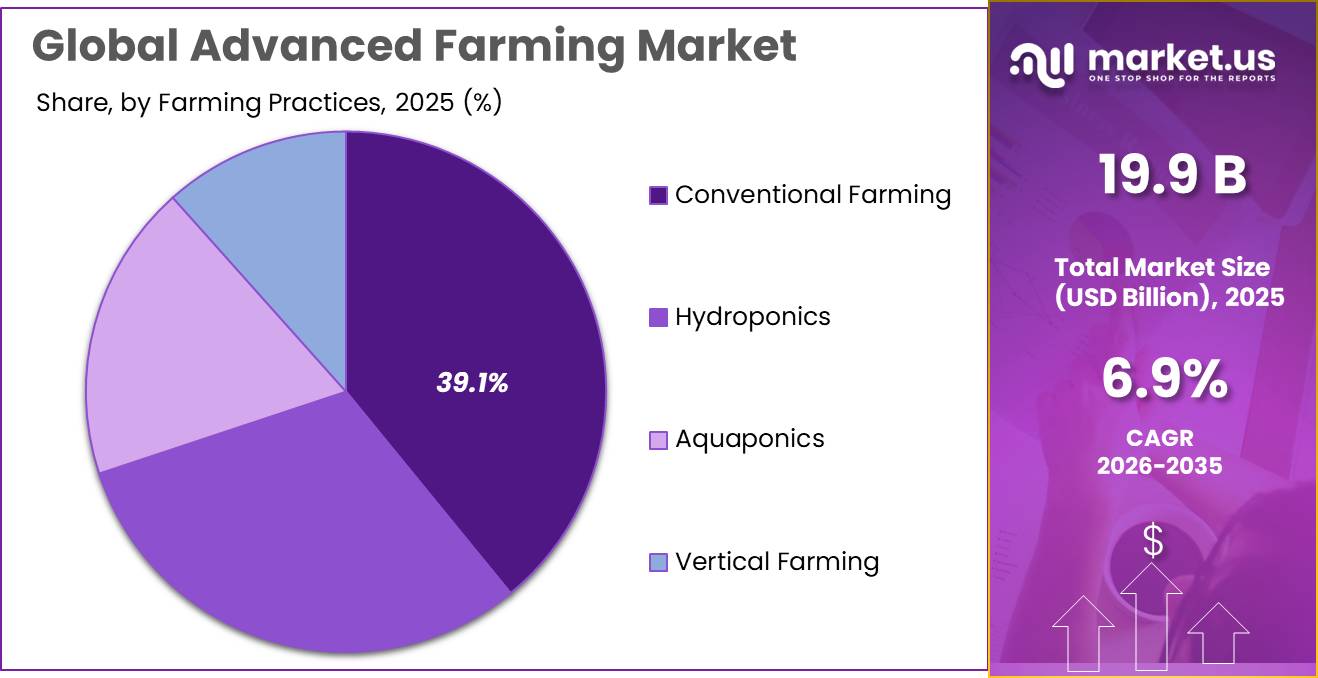

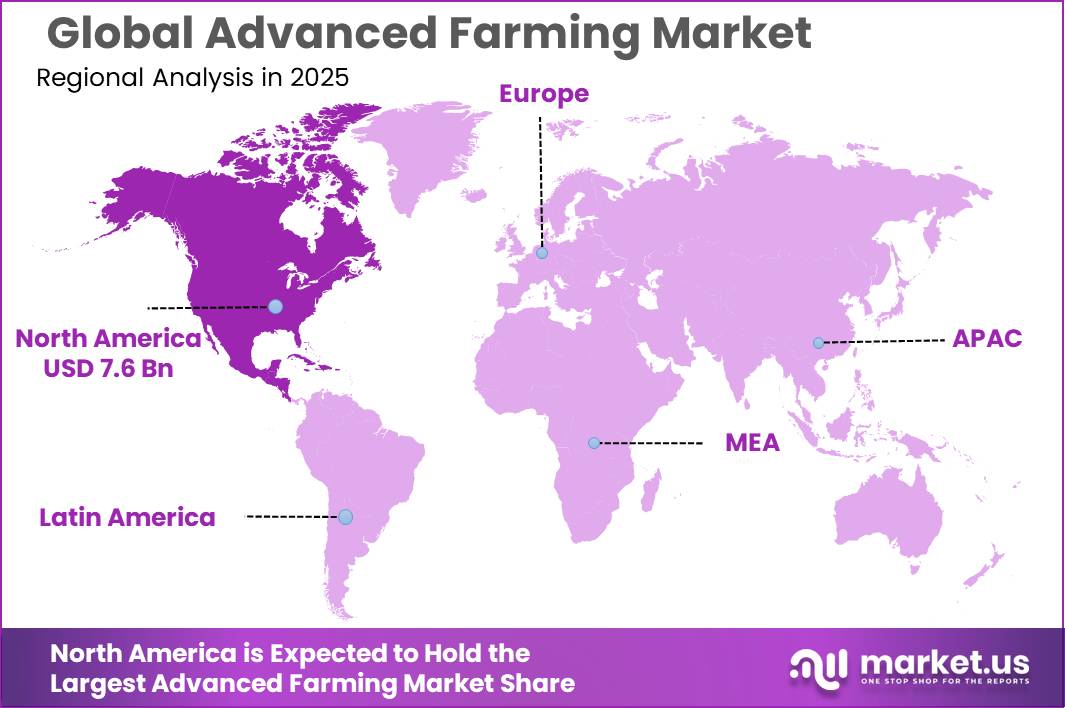

The Global Advanced Farming Market size is expected to be worth around USD 38.6 Billion by 2035, from USD 19.9 Billion in 2025, growing at a CAGR of 6.9% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 38.3% share, holding USD 7.6 Billion revenue.

Advanced farming is shifting from mechanization to connected, data-led production through GPS, AI, sensors, autonomy, satellite connectivity and variable-rate input systems. The industry is being pulled by food-security pressure, as FAO estimates agriculture must produce almost 50% more food, fibre and biofuel by 2050 versus 2012, while earlier FAO projections said global food production may need to rise 70% by 2050.

Key Takeaways

- Advanced Farming Market size is expected to be worth around USD 38.6 Billion by 2035, from USD 19.9 Billion in 2025, growing at a CAGR of 6.9%.

- Precision Agriculture held a dominant market position, capturing more than a 34.7% share in the advanced farming market.

- Tractors held a dominant market position, capturing more than a 32.6% share in the advanced farming market.

- Conventional Farming held a dominant market position, capturing more than a 39.1% share in the advanced farming market.

- Agriculture held a dominant market position, capturing more than a 59.2% share in the advanced farming market.

- North America held a dominant position in the global Advanced Farming Market, accounting for nearly 38.3% of the total market share and reaching a market value of approximately USD 7.6 Billion.

USDA ERS reported that 68% of large-scale U.S. crop-producing farms used yield monitors, yield maps and soil maps, showing that precision tools are moving from optional upgrades to core production infrastructure. OECD-FAO projects global agricultural and fish production to expand by 14% during 2025–2034, supported mainly by productivity improvements, while cereal production is projected to grow by 1.1% annually, with yield gains contributing 0.9% annually.

Driving factors include climate pressure, labor shortages, input-cost volatility and yield optimization. FAO states agrifood systems generate about one-third of human-caused greenhouse-gas emissions, making efficient fertilizer, fuel, water and chemical use a priority. OECD-FAO projects global agricultural and fish production to expand by about 14% by 2034, mainly through productivity gains. This supports investment in AI-enabled agronomy, satellite connectivity, GNSS positioning and autonomous equipment.

Government support is strengthening the ecosystem. USDA stated it was investing more than US$3.1 billion across 141 climate-smart commodity projects, while the European Commission reported at least €198 million from the CAP budget for digital transition during 2021–2023. The European Commission has allocated more than €200 million under Horizon 2020 for digital agriculture research and innovation, while USDA climate-smart resources support farm loans for climate-smart practices and related equipment. The EU’s CAP 2023–2027 rural development interventions include EUR 64 billion from the EU budget and EUR 43 billion from national funds.

Raven Industries strengthens the sector through guidance, input optimization, field computers, boom controls, Slingshot connectivity and autonomy solutions. CNH acquired Raven in 2021 for US$58 per share, representing a 33.6% premium and US$2.1 billion enterprise value, making Raven a core precision-agriculture technology platform inside CNH.

By Technology Analysis

Precision Agriculture dominates with 34.7% share due to rising adoption of data-driven farming technologies.

In 2025, Precision Agriculture held a dominant market position, capturing more than a 34.7% share in the advanced farming market by technology segment. The strong growth of this segment was mainly driven by the increasing use of smart farming tools that help farmers improve productivity while reducing operational costs. Technologies such as GPS-guided tractors, automated irrigation systems, yield monitoring, soil mapping, and drone-based crop analysis became more common across both large-scale and medium-sized farms. Farmers increasingly preferred precision agriculture solutions because they allowed better control over fertilizers, pesticides, and water usage, helping improve crop quality and reduce waste.

By Farming Equipment Analysis

Tractors dominate with 32.6% share due to their essential role in improving farm productivity and reducing manual labor.

In 2025, Tractors held a dominant market position, capturing more than a 32.6% share in the advanced farming market by farming equipment segment. The strong demand for tractors was mainly supported by the growing need for efficient and time-saving farming operations across small and large agricultural lands. Farmers increasingly relied on modern tractors for plowing, planting, harvesting, spraying, and transportation activities, making them one of the most important pieces of farm equipment. The availability of advanced tractor models with GPS guidance, fuel-efficient engines, and smart automation features also encouraged adoption among commercial farming operators.

By Farming Practices Analysis

Conventional Farming dominates with 39.1% share due to its large-scale adoption and established agricultural infrastructure.

In 2025, Conventional Farming held a dominant market position, capturing more than a 39.1% share in the advanced farming market by farming practices segment. The dominance of this segment was mainly supported by the widespread use of traditional agricultural methods combined with modern machinery and farming inputs. Many farmers continued to prefer conventional farming practices because they offered higher short-term productivity, easier crop management, and strong compatibility with existing farming equipment and irrigation systems. The use of chemical fertilizers, pesticides, and high-yield crop varieties remained common across large agricultural regions, helping farmers maintain stable production levels and meet growing food demand.

By End-Use Analysis

Agriculture dominates with 59.2% share due to increasing demand for higher crop productivity and modern farming solutions.

In 2025, Agriculture held a dominant market position, capturing more than a 59.2% share in the advanced farming market by end-use segment. The strong position of this segment was mainly driven by the rising need to improve food production efficiency and meet growing global food demand. Farmers increasingly adopted advanced farming technologies such as precision irrigation, automated machinery, smart monitoring systems, and data-based crop management to improve agricultural productivity. The agriculture sector remained the largest user of advanced farming solutions because these technologies helped reduce resource wastage, improve crop quality, and increase overall farm output.

Key Market Segments

By Technology

- Precision Agriculture

- Automation

- Artificial Intelligence (AI)

- Internet of Things (IoT)

- Robotic

By Farming Equipment

- Tractors

- Harvesters

- Planters & Seeders

- Sprayers

By Farming Practices

- Vertical Farming

- Hydroponics

- Aquaponics

- Conventional Farming

By End-Use

- Agriculture

- Horticulture

- Livestock Farming

Emerging Trends

AI and Digital Farming Technologies are Becoming the Biggest Trend in Advanced Farming

One of the latest trends in the advanced farming market is the rapid adoption of artificial intelligence (AI), drones, IoT sensors, and digital farming platforms. Farmers are increasingly using these technologies to monitor soil health, weather conditions, crop growth, and pest activity in real time. According to the Food and Agriculture Organization (FAO), digital agriculture and AI are creating new opportunities to improve farming efficiency, strengthen food security, and support sustainable agriculture worldwide.

Drones and satellite-based monitoring systems are also becoming more common because they help farmers identify crop stress early and reduce unnecessary chemical usage. Governments and agricultural agencies are actively supporting digital agriculture programs to modernize farming operations and improve long-term productivity. The growing use of connected farming equipment and smart analytics platforms is changing how farms are managed, especially in regions facing labor shortages and climate-related agricultural risks.

Precision Farming and Smart Monitoring Systems are Expanding Across Global Agriculture

Another major trend shaping the advanced farming market is the growing use of precision farming and smart monitoring technologies. Farmers are now focusing more on data-driven agriculture to improve crop yields while reducing water, fertilizer, and fuel consumption. Research studies published in agricultural journals showed that precision farming technologies can improve yields by nearly 20% to 30% through better resource management and targeted farming practices.

Smart tractors, automated irrigation systems, and IoT-enabled field sensors are helping agricultural producers reduce operational costs and improve sustainability. The International Telecommunication Union (ITU) also highlighted that AI, connected services, and autonomous systems are allowing farmers to manage crops and livestock with greater precision than traditional farming methods. Governments across several countries are investing in rural digital infrastructure and agricultural automation to support the growth of smart farming technologies.

Drivers

Rising Global Food Demand is Increasing the Need for Advanced Farming Technologies

One of the biggest driving factors for advanced farming is the rapid increase in global food demand. According to the Food and Agriculture Organization (FAO), the world population is expected to reach around 9.7 billion by 2050, creating strong pressure on the agriculture sector to produce significantly more food with limited farmland and water resources. FAO also stated that global food production may need to increase by nearly 70% by 2050 to meet future demand.

This situation is encouraging farmers and agricultural industries to adopt advanced farming technologies such as precision agriculture, smart irrigation, drones, automated tractors, and AI-based crop monitoring systems. These technologies help improve crop yields, reduce wastage, and increase farming efficiency. Governments across several countries are also supporting digital agriculture programs to strengthen food security and improve farm productivity.

Government Support and Rising Precision Agriculture Adoption are Supporting Market Growth

Government initiatives and growing awareness about smart farming benefits are also strongly driving the advanced farming market. The United States Department of Agriculture (USDA) reported that the adoption of precision agriculture technologies continues to increase, especially among large farming operations. According to USDA data, around 68% of large-scale crop farms were using technologies such as yield monitoring, soil mapping, and precision guidance systems.

In addition, the U.S. Government Accountability Office mentioned that USDA and the National Science Foundation together provided nearly US$200 million in funding for precision agriculture research and development activities. Such investments are helping improve access to smart farming technologies and encouraging innovation in agricultural automation and digital farming solutions. Similar support programs are also being introduced in developing countries to modernize agriculture and improve long-term food production capabilities.

Restraints

High Initial Investment and Technology Costs are Limiting Advanced Farming Adoption

One of the major restraining factors for the advanced farming market is the high cost associated with modern agricultural technologies and equipment. Many small and medium-sized farmers struggle to afford advanced tools such as GPS-enabled tractors, drones, smart irrigation systems, robotic harvesters, and AI-based monitoring platforms. According to the World Bank, nearly 80% of farms worldwide are smallholder farms, and many of them operate with limited financial resources and low access to credit facilities.

In developing countries, the problem becomes even bigger because rural infrastructure, internet connectivity, and technical training are often limited. Farmers may also hesitate to adopt new technologies due to uncertainty about returns on investment and maintenance costs. Although governments are introducing subsidy programs and agricultural modernization initiatives, adoption remains slower in price-sensitive regions where farming incomes are unstable and seasonal.

Lack of Digital Skills and Rural Connectivity Continues to Slow Market Growth

Another major challenge affecting advanced farming growth is the lack of digital knowledge and internet access in rural farming communities. Advanced farming systems depend heavily on real-time data, cloud platforms, sensors, and connected devices, which require stable internet services and technical understanding. According to the International Telecommunication Union (ITU), around 2.6 billion people globally were still offline in recent years, with a large share living in rural areas.

In many agricultural regions, farmers still depend on traditional farming methods because they are easier to manage and require less technical expertise. Governments and agricultural organizations are working to improve rural broadband infrastructure and provide digital farming training programs, but progress remains uneven across countries.

Opportunity

Expansion of Smart Irrigation and Precision Farming Creates Strong Growth Opportunities

One of the biggest growth opportunities in the advanced farming market is the rising adoption of smart irrigation and precision farming technologies. Water scarcity is becoming a serious concern for agriculture worldwide, and farmers are increasingly looking for efficient ways to reduce water usage while maintaining crop productivity.

- According to the Food and Agriculture Organization (FAO), agriculture accounts for nearly 70% of global freshwater withdrawals, making efficient irrigation systems extremely important for future food production.

Smart irrigation technologies, soil moisture sensors, and AI-based crop monitoring systems are helping farmers optimize water use and improve farm efficiency. Governments in several countries are also promoting precision farming through subsidy programs and digital agriculture initiatives to improve sustainable farming practices. These technologies not only help save water and fertilizers but also improve crop quality and reduce operational expenses.

Government Investments in Digital Agriculture are Opening New Market Potential

Government support for digital agriculture and smart farming infrastructure is creating another major growth opportunity for the advanced farming market. Many countries are investing heavily in agricultural modernization to improve food security and strengthen rural economies. According to the United States Department of Agriculture (USDA), precision agriculture technologies can reduce input costs while improving field productivity through better resource management.

Regional Insights

North America dominates the Advanced Farming Market with a 38.3% share, valued at USD 7.6 Billion, driven by strong technology adoption and large-scale commercial farming.

In 2025, North America held a dominant position in the global Advanced Farming Market, accounting for nearly 38.3% of the total market share and reaching a market value of approximately USD 7.6 Billion. The region’s leadership was mainly supported by the rapid adoption of precision agriculture technologies, automated farming equipment, AI-based crop monitoring systems, and advanced irrigation solutions across the United States and Canada.

The United States remained the largest contributor to regional growth due to its highly developed agricultural infrastructure and strong government support for digital farming initiatives. According to data from the United States Department of Agriculture (USDA), precision agriculture technologies such as GPS guidance systems, yield monitoring, and automated tractors have seen widespread adoption among large farming operations across the country.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, John Deere & Company continued strengthening its position in the advanced farming market through autonomous tractors, precision agriculture software, and smart spraying technologies. The company reported annual revenue exceeding USD 51 billion, with agriculture remaining its largest business segment. Deere expanded the use of AI-enabled farming equipment capable of reducing herbicide usage by nearly 60% through targeted spraying systems.

AGCO Corp. remained a major player in advanced farming during 2025 through smart tractors, automated harvesting systems, and precision agriculture platforms. The company generated approximately USD 11.7 billion in annual revenue and expanded its digital farming business through PTx Trimble solutions. AGCO invested in AI-driven farm management technologies and autonomous machinery to improve operational efficiency and sustainability.

CNH Industrial continued expanding its advanced farming portfolio in 2025 through autonomous machinery, precision farming systems, and smart fleet management technologies. The company reported annual revenue above USD 24 billion, supported by strong agricultural equipment demand. CNH increased investment in AI-powered farming solutions and telematics systems that allow real-time monitoring of field operations and machine performance.

Top Key Players Outlook

- John Deere & Company

- Raven Industries, Inc.

- AGCO Corp.

- CNH Industrial

- Trimble Inc

- Yanmar Co., Ltd.

- Escorts Ltd.

- Kverneland AS

Recent Industry Developments

In 2025, Trimble Inc. worked in advanced farming mainly through PTx Trimble, its precision agriculture joint venture with AGCO. Under this agreement, AGCO owns 85% of PTx Trimble, while Trimble keeps a 15% stake. The platform supports mixed-fleet farming with guidance, autonomy, precision spraying, connected farming, data management, and sustainability tools. In 2025, Trimble and PTx Trimble expanded IonoGuard on the NAV-900 guidance controller to help farmers reduce downtime during GNSS signal disruption.

In 2025, Yanmar Co., Ltd. strengthened its advanced farming work through smart machinery, robotics, and sustainable farm models. The company reported FY2024 revenue of JPY 1,079.6 billion, while its first half FY2025 net sales reached JPY 577.8 billion, up 9.2% year-on-year. In product development, Yanmar continued expanding SMARTPILOT robot tractors, auto rice transplanters, and smart combine harvesters, where one operator can manage two tractors and RTK-GNSS supports centimeter-level accuracy.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 19.9 Bn |

| Forecast Revenue (2035) | USD 38.6 Bn |

| CAGR (2026-2035) | 6.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Precision Agriculture, Automation, Artificial Intelligence (AI), Internet of Things (IoT), Robotic), By Farming Equipment (Tractors, Harvesters, Planters And Seeders, Sprayers), By Farming Practices (Vertical Farming, Hydroponics, Aquaponics, Conventional Farming), By End-Use (Agriculture, Horticulture, Livestock Farming) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | John Deere & Company, Raven Industries, Inc., AGCO Corp., CNH Industrial, Trimble Inc, Yanmar Co., Ltd., Escorts Ltd., Kverneland AS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |