Quick Navigation

- Report Scope

- Key Takeaways

- Analysts’ Viewpoint

- Key Statistics

- Regional Analysis

- By Type

- By Application

- By Industry Vertical

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenging Factors

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Scope

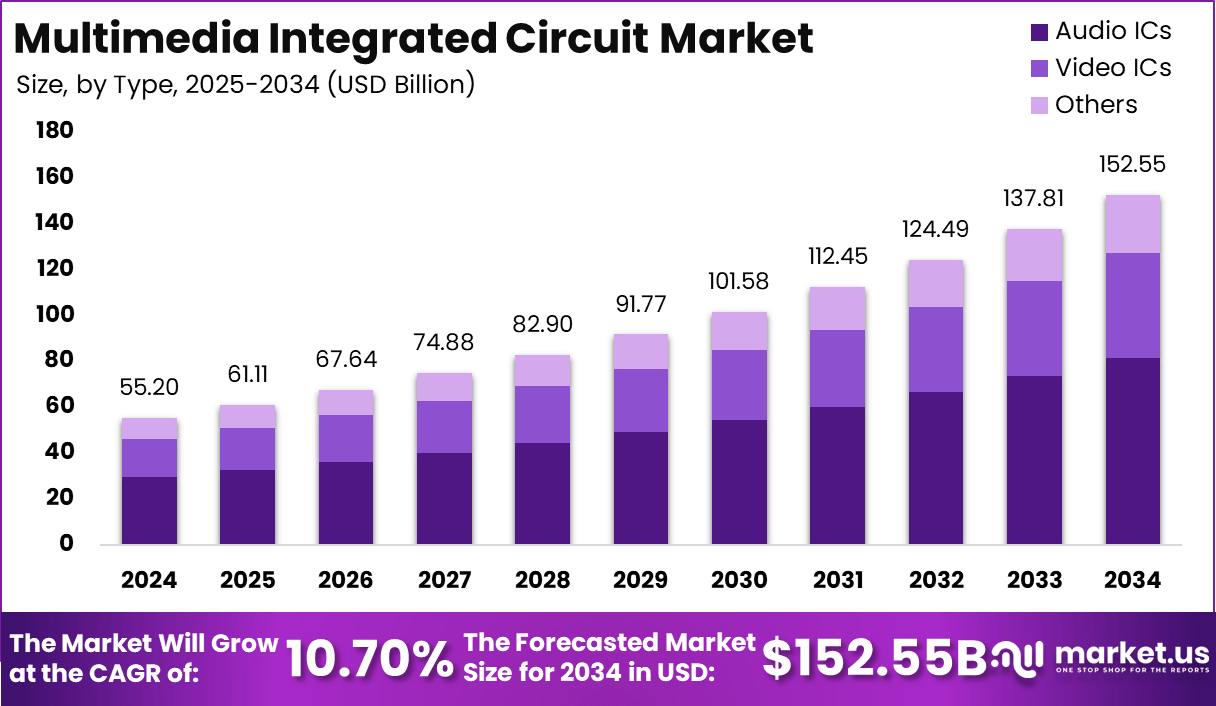

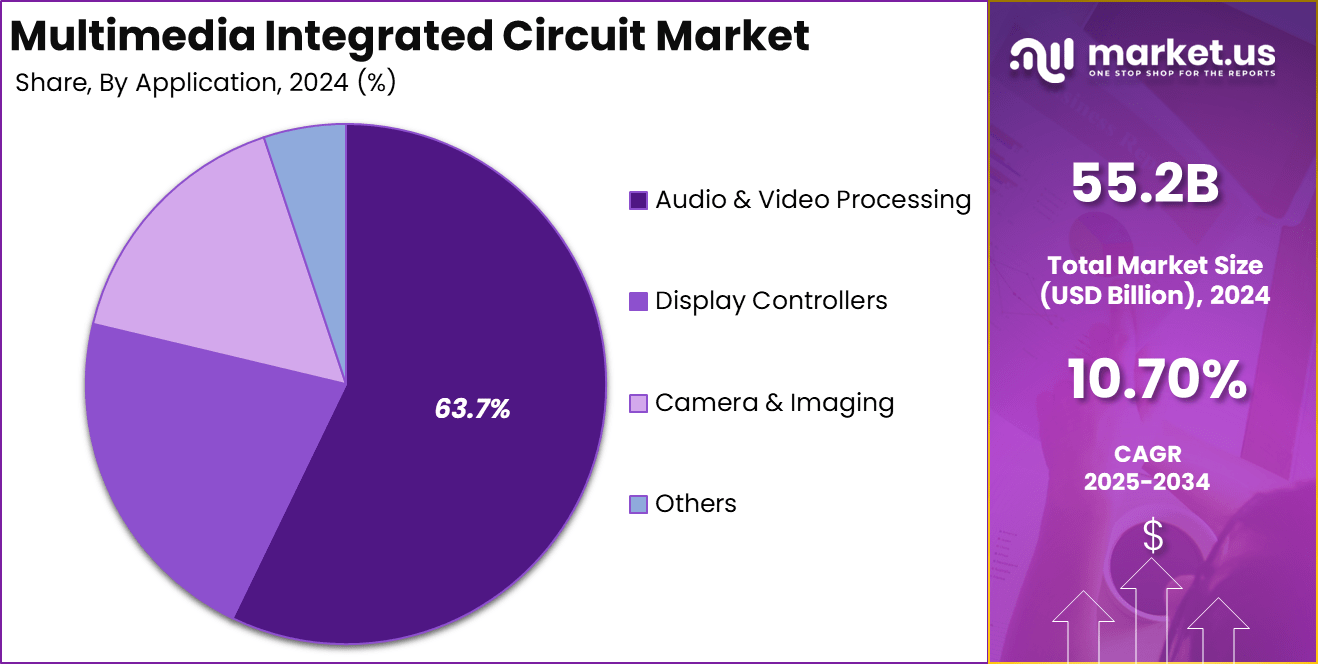

The Global Multimedia Integrated Circuit Market is expected to be worth around USD 152.55 Billion by 2034, up from USD 55.2 Billion in 2024. It is expected to grow at a CAGR of 10.70% from 2025 to 2034.

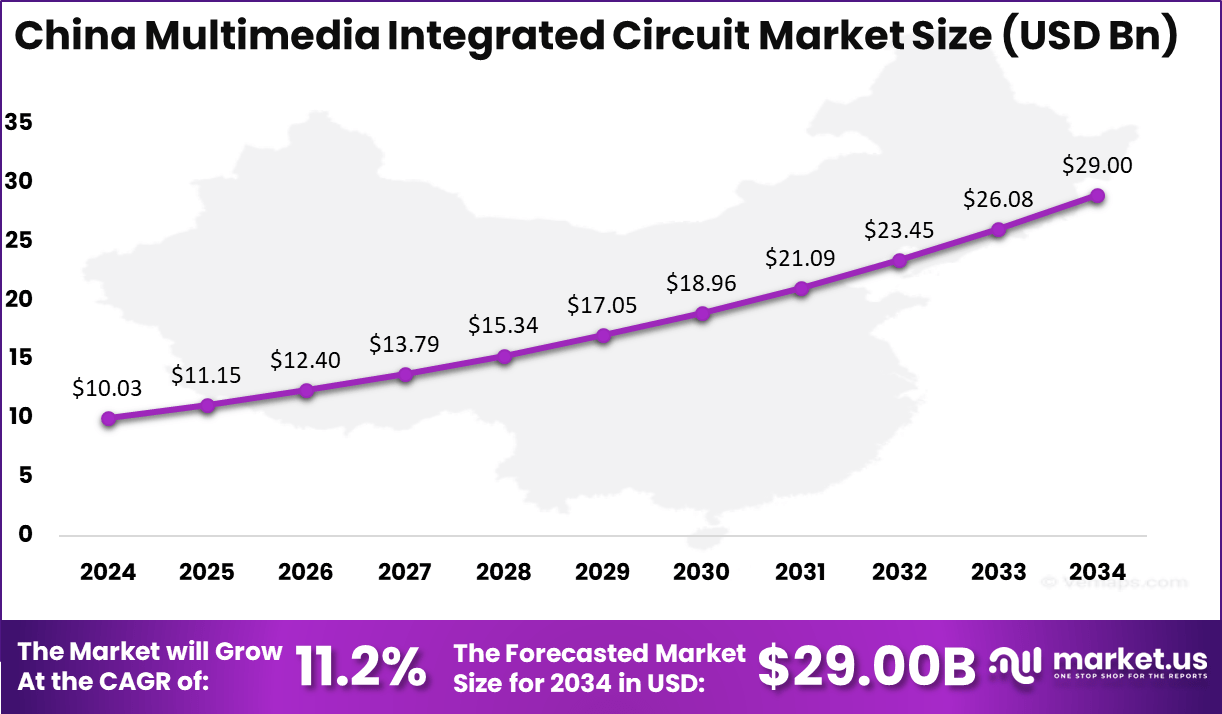

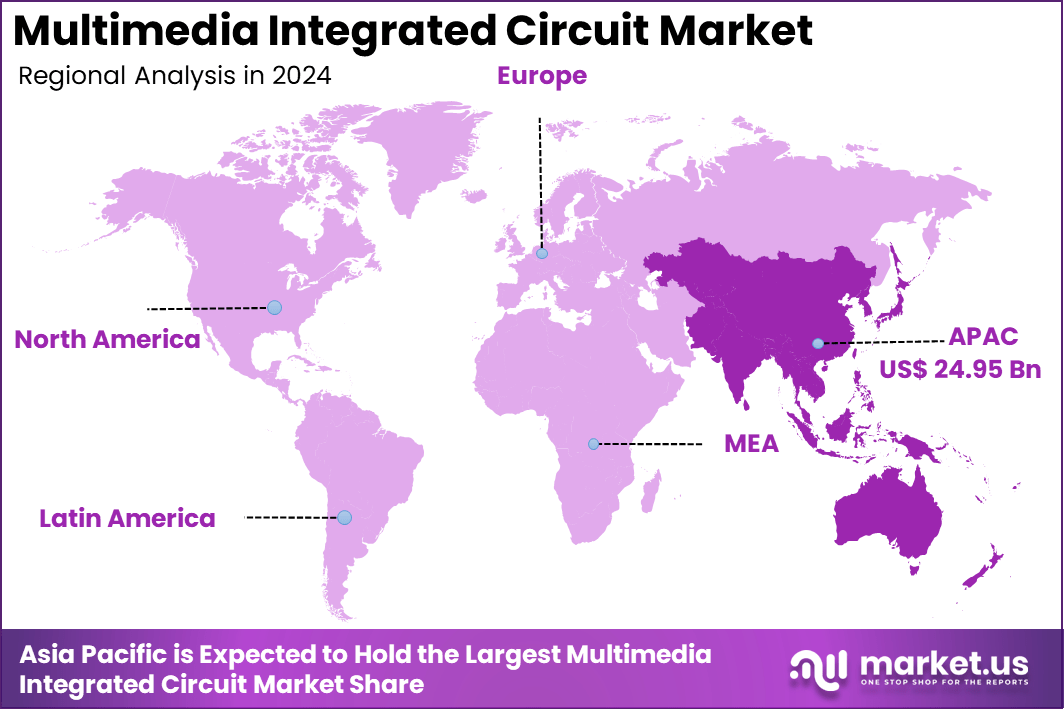

In 2024, Asia-Pacific held a dominant market position, capturing over a 45.2% share and earning USD 24.95 Billion in revenue. Further, China dominates the market by USD 10.03 Billion, steadily holding a strong position with a CAGR of 11.2%.

The Multimedia Integrated Circuit (IC) market is experiencing significant growth, driven by the increasing demand for high-quality audio and video processing in consumer electronics, automotive infotainment systems, and telecommunications devices. Multimedia ICs are essential components that enable efficient processing of audio, video, and graphics in devices such as smartphones, tablets, smart TVs, and automotive infotainment systems.

Several factors are propelling the expansion of the multimedia IC market. The rising consumer demand for immersive audio and visual experiences necessitates advanced multimedia processing capabilities. Additionally, the integration of multimedia functionalities in automotive infotainment systems, including navigation, entertainment, and connectivity features, contributes to market growth.

Key Takeaways

- Market Growth: The multimedia integrated circuit (IC) market is projected to grow from USD 55.2 billion in 2024 to USD 152.55 billion by 2034, reflecting a CAGR of 10.70% over the forecast period.

- Dominant Type: Audio ICs hold the largest market share (53.5%), driven by the increasing demand for high-quality sound processing in consumer electronics and automotive infotainment systems.

- Major Application: Audio & Video Processing accounts for 63.7% of the total market, highlighting the strong demand for high-definition multimedia processing in entertainment devices, gaming consoles, and smart devices.

- Leading Industry Vertical: Consumer Electronics dominates with a 72.6% market share, supported by the rising sales of smartphones, smart TVs, tablets, and home entertainment systems.

- Regional Insights: Asia Pacific leads with a 45.2% market share, fueled by the rapid growth of consumer electronics manufacturing and increasing demand for high-quality multimedia experiences. China alone contributes USD 10.03 billion in 2024, with a robust CAGR of 11.2%, making it a key growth driver in the region.

- Future Outlook: The market is set to experience rapid expansion, driven by advancements in AI-powered multimedia processing, 4K/8K video technology, and smart audio solutions, particularly in emerging markets like Asia Pacific and China.

Analysts’ Viewpoint

The demand for multimedia ICs is further amplified by the proliferation of high-definition multimedia devices and the expansion of the entertainment industry. Consumers’ desire for superior audio and video quality in their devices drives the need for advanced multimedia ICs. Moreover, the automotive sector’s adoption of multimedia functionalities enhances the in-car entertainment experience, leading to increased demand for these integrated circuits.

Opportunities within the multimedia IC market are abundant, particularly with the growing adoption of high-definition multimedia devices and the expansion of the entertainment industry. Manufacturers focusing on developing ICs with advanced features such as 4K/8K video processing, surround sound, and artificial intelligence capabilities are well-positioned to capitalize on these opportunities.

Technological advancements play a pivotal role in shaping the multimedia IC market. Innovations such as the development of system-on-chip (SoC) solutions, improved power efficiency, and enhanced processing speeds have significantly improved the performance and adoption of multimedia ICs. Manufacturers are continually enhancing ICs to meet the evolving needs of consumers and industries, incorporating features like 4K/8K video processing, surround sound, and AI capabilities.

Key Statistics

Numerical Trends

- Growth Rate: The demand for multimedia ICs is growing at a rate of around 10% annually due to advancements in technology and increasing demand for multimedia content.

- Performance Metrics: Performance metrics such as processing speed and memory capacity are continuously improving with each new generation of ICs, with improvements averaging 20% to 30% per year.

Usage and Users

- User Base: Estimated over 5 billion users worldwide, given the widespread use of multimedia-enabled devices like smartphones and smart TVs.

- Usage Rate: High usage rates in devices like smartphones (over 90% of users engage with multimedia daily) and tablets (around 70% daily usage).

Quantity and Production

- Production Volume: Over 10 billion units produced annually to meet global demand.

- Manufacturing Countries: Key manufacturing countries include China (producing over 4 billion units), Taiwan (over 2 billion units), and South Korea (over 1.5 billion units).

Other Numerical Data

- Power Consumption: Typically ranges from 5 milliwatts to 50 watts depending on the application.

- Clock Speed: Can range from 100 MHz to 5 GHz for high-performance applications.

- Memory Capacity: Integrated memory can range from 256 kilobytes to 16 gigabytes.

Regional Analysis

China Region Market Size

In Asia-Pacific, the market is expanding rapidly due to the region’s strong manufacturing base and increasing adoption of multimedia-enabled devices. China dominates the market, contributing USD 10.03 billion, maintaining its position as a key player in the industry. The country is growing at a CAGR of 11.2%, showcasing steady expansion and strong demand for multimedia ICs across various applications.

The Multimedia Integrated Circuit (IC) Market is experiencing substantial growth, driven by the increasing demand for high-quality audio and video processing across various industries. The market is expanding at a notable pace, fueled by advancements in consumer electronics, automotive infotainment systems, and entertainment devices. The integration of multimedia ICs in smart devices, gaming consoles, and high-resolution display systems is further accelerating this growth.

Among different IC types, Audio ICs hold a significant share, reflecting strong consumer demand for high-fidelity sound in personal and professional audio systems. Similarly, audio and video processing applications dominate the market, highlighting the critical role of multimedia ICs in enhancing user experiences across digital platforms. The consumer electronics sector remains the largest industry vertical, driven by the rapid adoption of smart technologies and entertainment gadgets.

Asia Pacific Market Size

In 2024, the Asia-Pacific region held a dominant position in the Multimedia Integrated Circuit (IC) market, capturing a substantial 45.2% share, which translated to approximately USD 24.95 billion in revenue. This leadership can be attributed to several key factors inherent to the region’s economic and industrial landscape.

A primary driver is the robust semiconductor manufacturing infrastructure present in countries like China, Taiwan, South Korea, and Japan. These nations host numerous semiconductor fabrication plants and integrated circuit manufacturers, creating a conducive environment for the production and development of multimedia ICs. The concentration of these facilities not only ensures a steady supply of components but also fosters innovation through close collaboration among industry players.

China, in particular, has been instrumental in the region’s dominance. The country’s strategic initiatives to bolster its semiconductor industry have led to significant investments and advancements in IC manufacturing capabilities. This focus has enabled China to meet the escalating demand for multimedia ICs, both domestically and internationally, reinforcing its position as a key contributor to the market’s expansion.

Furthermore, the Asia-Pacific region’s large consumer base, coupled with a high adoption rate of electronic devices such as smartphones, tablets, and smart televisions, has fueled the demand for advanced multimedia ICs. The integration of these circuits into consumer electronics enhances audio and visual experiences, aligning with the preferences of tech-savvy consumers in the region. This synergy between manufacturing prowess and consumer demand has solidified Asia-Pacific’s leading role in the global multimedia IC market.

By Type

In 2024, the Audio ICs segment held a dominant market position, capturing more than a 53.5% share of the Multimedia Integrated Circuit (IC) market. This leadership is primarily due to the increasing demand for high-quality audio processing in consumer electronics, automotive infotainment, and smart devices. With the rising popularity of wireless earbuds, smart speakers, and home entertainment systems, manufacturers are integrating advanced audio ICs to enhance sound clarity, noise cancellation, and power efficiency.

The automotive industry has also contributed significantly to the growth of the Audio ICs segment. Modern vehicles are equipped with premium audio systems, voice-controlled assistants, and hands-free communication features, all of which rely on sophisticated audio processing chips. Additionally, the growing penetration of AI-driven voice recognition technologies in smart devices has further propelled the demand for audio ICs.

Moreover, as high-resolution audio streaming services become more popular, there is an increasing need for audio ICs with superior sound processing capabilities. These factors, coupled with continuous advancements in low-power and high-performance audio chips, have solidified the Audio ICs segment’s dominance in the Multimedia IC Market.

By Application

In 2024, the Audio & Video Processing segment held a dominant market position, capturing more than a 63.7% share of the Multimedia Integrated Circuit (IC) market. This dominance is primarily driven by the increasing demand for high-definition audio and video experiences in consumer electronics, automotive infotainment systems, and broadcasting technologies. With the rapid growth of 4K and 8K ultra-high-definition (UHD) content, there is a strong need for advanced multimedia ICs that can efficiently process high-resolution video and high-fidelity audio.

The entertainment industry plays a crucial role in this segment’s growth, as streaming services, gaming consoles, and smart TVs require powerful audio and video processors for an immersive user experience. Additionally, AI-powered multimedia processing in smart devices, including real-time voice recognition and image enhancement, has further strengthened the demand for Audio & Video Processing ICs.

Furthermore, the automotive sector has embraced advanced infotainment systems, integrating multimedia ICs for real-time navigation, voice assistance, and rear-seat entertainment displays. As technology continues to evolve, the Audio & Video Processing segment will remain the driving force behind the Multimedia IC market, ensuring seamless, high-quality digital experiences across multiple industries.

By Industry Vertical

In 2024, the Consumer Electronics segment held a dominant market position, capturing more than a 72.6% share of the Multimedia Integrated Circuit (IC) market. This leadership is driven by the rising demand for high-performance multimedia processing in smartphones, tablets, smart TVs, laptops, and gaming consoles. As consumers seek superior audio-visual experiences, manufacturers are integrating advanced multimedia ICs to support 4K/8K video playback, immersive sound quality, and AI-driven enhancements.

The smartphone industry is a key contributor to this segment’s growth, with continuous innovations in camera technology, high-resolution displays, and AI-powered multimedia processing. Additionally, wearable devices, smart home systems, and wireless earbuds have further increased the demand for efficient and power-optimized multimedia ICs.

Moreover, the rapid expansion of online streaming services, cloud gaming, and virtual reality (VR) applications has intensified the need for high-performance multimedia chips that can handle real-time video and audio processing. As technology advances, the Consumer Electronics segment will continue to dominate the Multimedia IC market, fueled by growing consumer expectations and industry innovations in digital entertainment.

Key Market Segments

By Type

- Audio ICs

- Video ICs

- Others

By Application

- Audio & Video Processing

- Display Controllers

- Camera & Imaging

- Others

By Industry Vertical

- Consumer Electronics

- Automotive

- Healthcare

- Telecommunications

- Industrial

- Aerospace & Defense

- Others

Driving Factors

Proliferation of Consumer Electronics

The rapid growth of the consumer electronics sector is a significant driving force in the multimedia integrated circuit (IC) market. Devices such as smartphones, tablets, smart TVs, and wearable gadgets have become integral to daily life, leading to an increased demand for advanced multimedia ICs that can deliver superior audio and video performance.

Manufacturers are continually innovating to meet consumer expectations for high-quality multimedia experiences, integrating sophisticated ICs to enhance functionality and user satisfaction. For instance, the global sales of semiconductors experienced a substantial growth of about 24% in October 2021, reaching nearly USD 49 billion compared to the same month in the previous year. This surge underscores the escalating demand for integrated circuits in consumer electronics, highlighting their pivotal role in driving the multimedia IC market forward.

Restraining Factors

High Manufacturing Costs

Despite the growing demand, the multimedia IC market faces challenges due to the high costs associated with designing and producing these specialized circuits. Developing advanced ICs requires significant investment in research and development, sophisticated fabrication facilities, and skilled personnel.

These substantial expenses can lead to higher prices for end consumers, potentially limiting the widespread adoption of new technologies. Moreover, smaller companies may struggle to compete with established industry players due to the financial barriers to entry, which could stifle innovation and reduce market diversity. The complexity and cost of manufacturing advanced ICs pose significant challenges to the market’s growth trajectory.

Growth Opportunities

Integration of AI and Machine Learning

The convergence of artificial intelligence (AI) and machine learning with multimedia ICs presents a substantial growth opportunity. By embedding AI capabilities directly into ICs, devices can perform tasks such as real-time language translation, image recognition, and adaptive sound profiling more efficiently. This integration enhances user experiences and opens new applications in sectors like healthcare, automotive, and entertainment.

For example, the development of application-specific integrated circuits (ASICs) tailored for AI workloads has led to significant performance improvements in data processing and analytics. As AI continues to permeate various aspects of technology, the demand for AI-enabled multimedia ICs is expected to rise, offering lucrative opportunities for market expansion.

Challenging Factors

Rapid Technological Advancements

The multimedia IC market is characterized by rapid technological advancements, which, while driving innovation, also pose significant challenges. Manufacturers must continually invest in updating their technologies and processes to keep pace with evolving standards and consumer expectations.

This constant need for innovation can strain resources and lead to shorter product lifecycles, increasing the risk of obsolescence. Additionally, integrating new technologies into existing systems can be complex and costly, requiring extensive testing and validation to ensure compatibility and performance. Staying abreast of technological changes is a formidable challenge that companies must navigate to remain competitive in the multimedia IC market.

Growth Factors

Rising Demand for Consumer Electronics

The global integrated circuit (IC) market is experiencing significant growth, largely driven by the escalating demand for consumer electronics. Devices such as smartphones, tablets, and wearable gadgets have become integral to daily life, leading to a surge in the need for advanced ICs that enhance functionality and performance.

This upward trajectory is closely linked to consumer preferences for high-performance devices. Features such as high-resolution displays, faster processing speeds, and extended battery life are becoming standard expectations, necessitating the development of more sophisticated ICs. The proliferation of smart home devices and the Internet of Things (IoT) further amplifies this demand, as these technologies rely heavily on integrated circuits for seamless connectivity and functionality.

Emerging Trends

Integration of Artificial Intelligence in ICs

A notable emerging trend in the IC market is the integration of artificial intelligence (AI) capabilities into integrated circuits. This development is transforming various industries by enabling devices to perform complex tasks more efficiently.

Incorporating AI into ICs allows for real-time data processing and decision-making, which is particularly beneficial in applications such as autonomous vehicles, healthcare diagnostics, and smart home devices. For instance, AI-enabled ICs can process vast amounts of sensor data in autonomous cars, facilitating immediate responses to changing road conditions and enhancing safety.

Business Benefits

Enhanced Performance and Efficiency

The evolution of integrated circuits has led to significant business benefits, particularly in terms of enhanced performance and efficiency. Modern ICs offer improved reliability, reduced power consumption, and compactness, which are crucial for developing cost-effective and high-performing electronic devices.

For businesses, these advancements translate into products that meet consumer demands for longer battery life and faster processing speeds, thereby increasing market competitiveness. For example, the development of application-specific integrated circuits (ASICs) tailored for AI workloads has led to significant performance improvements in data processing and analytics.

Additionally, the miniaturization of ICs allows companies to design more compact and portable devices without compromising functionality. This capability is particularly advantageous in the wearable technology market, where space is limited, and efficiency is paramount. Overall, the advancements in IC technology provide businesses with the tools to innovate and meet evolving consumer expectations effectively.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

Qualcomm has actively pursued strategic acquisitions to diversify its technology portfolio. In January 2021, the company announced the acquisition of NUVIA, a startup specializing in high-performance processors, for approximately $1.4 billion.

This move aimed to enhance Qualcomm’s CPU capabilities, particularly in the realm of 5G computing. The acquisition was completed in March 2021, with plans to integrate NUVIA’s technology into Qualcomm’s Snapdragon processors, targeting next-generation laptops and digital infrastructure.

Broadcom has engaged in notable acquisition attempts to expand its market presence. In November 2017, Broadcom proposed a $130 billion acquisition of Qualcomm, offering $70 per share—a 28% premium over Qualcomm’s stock price at the time. However, this bid was rebuffed by Qualcomm’s board, and subsequent attempts were blocked by U.S. regulatory authorities in March 2018, citing national security concerns.

Texas Instruments (TI) has a history of strategic acquisitions to bolster its analog and embedded processing segments. In 2011, TI acquired National Semiconductor for $6.5 billion, significantly enhancing its analog capabilities and product offerings. This acquisition positioned TI as a leader in the analog semiconductor market.

Top Key Players in the Market

- Qualcomm Incorporated

- Broadcom Inc.

- Texas Instruments Incorporated

- NXP Semiconductors N.V.

- MediaTek Inc.

- Analog Devices, Inc.

- Samsung Electronics Co., Ltd.

- Renesas Electronics Corporation

- STMicroelectronics N.V.

- ON Semiconductor Corporation

- Micron Technology, Inc.

- Infineon Technologies AG

- Other Major Players

Recent Developments

- In 2024, the global multimedia integrated circuits (ICs) market experienced significant growth, driven by increasing demand for high-definition multimedia devices and advancements in IC technologies.

- In 2024, Siemens Digital Industries Software introduced the Solido™ Simulation Suite in January 2024, a cutting-edge platform for analog, mixed-signal, and RF IC design.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 55.2 Billion |

| Forecast Revenue (2034) | USD 152.55 Billion |

| CAGR (2025-2034) | 10.70% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Audio ICs, Video ICs, Others), By Application (Audio & Video Processing, Display Controllers, Camera & Imaging, Others), By Industry Vertical (Consumer Electronics, Automotive, Healthcare, Telecommunications, Industrial, Aerospace & Defense, Others), By Revenue Model (Subscription-Based, Ad-Supported, Pay-Per-View, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Qualcomm Incorporated, Broadcom Inc., Texas Instruments Incorporated, NXP Semiconductors N.V., MediaTek Inc., Analog Devices, Inc., Samsung Electronics Co., Ltd., Renesas Electronics Corporation, STMicroelectronics N.V., ON Semiconductor Corporation, Micron Technology, Inc., Infineon Technologies AG, Other Major Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |