Quick Navigation

Report Overview

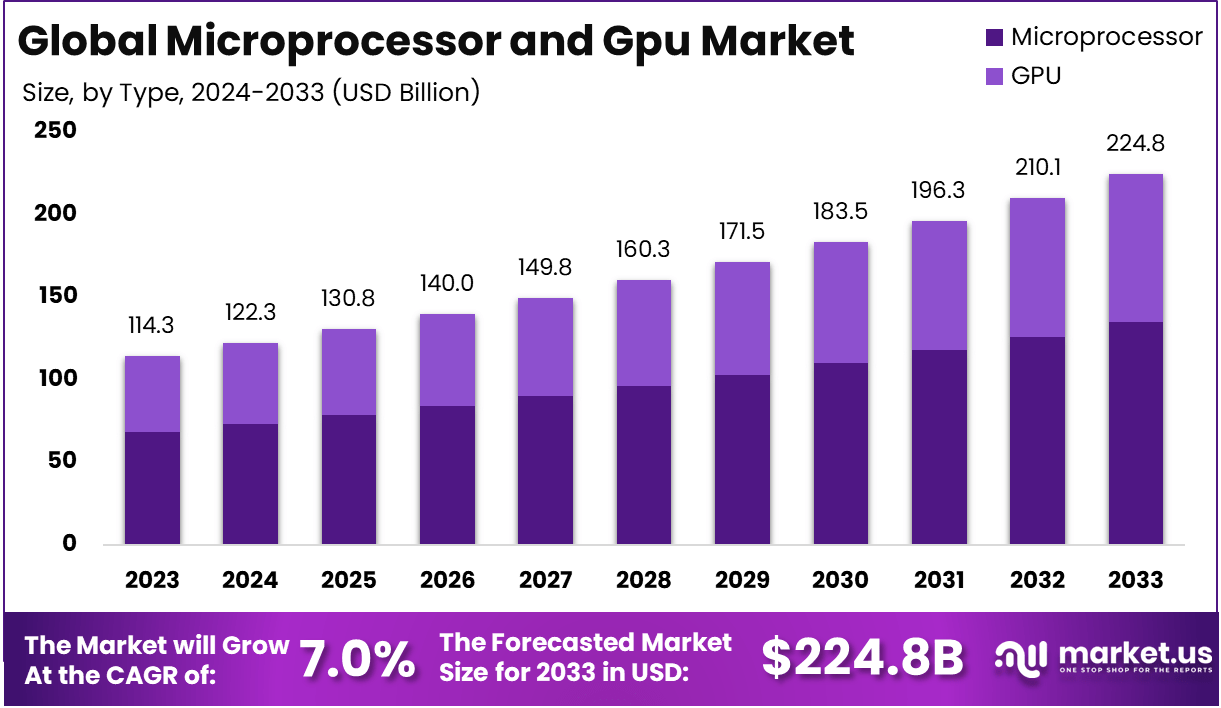

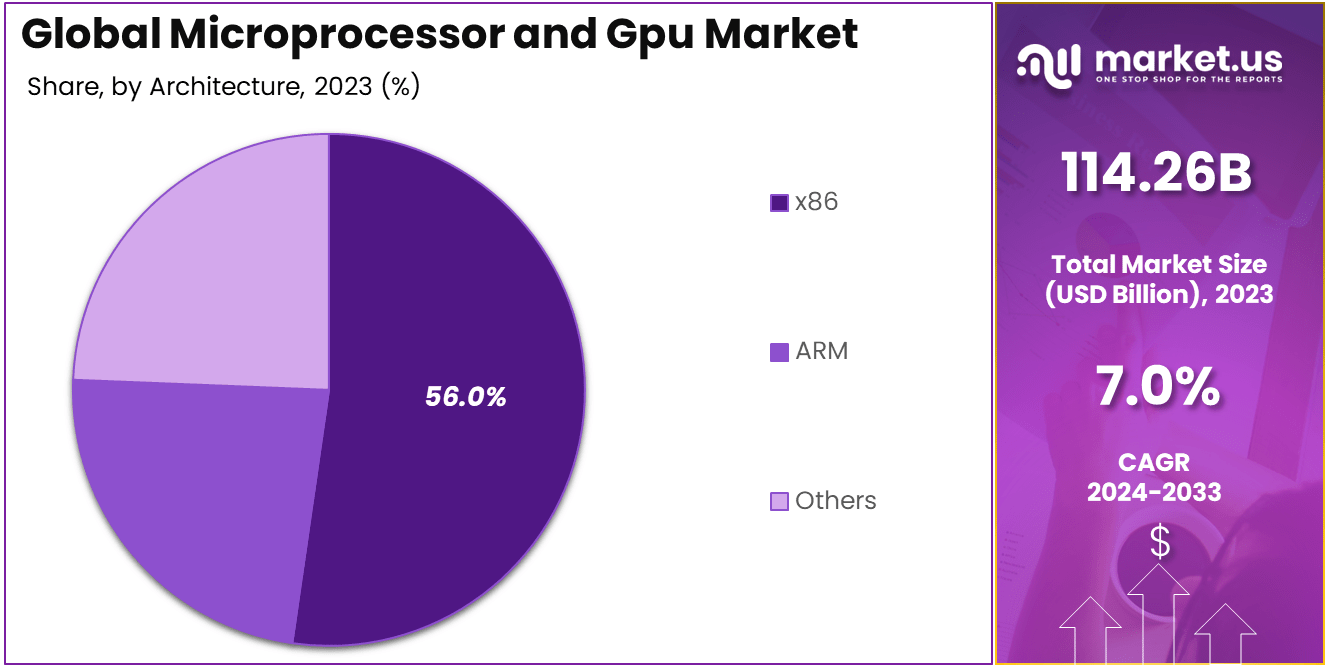

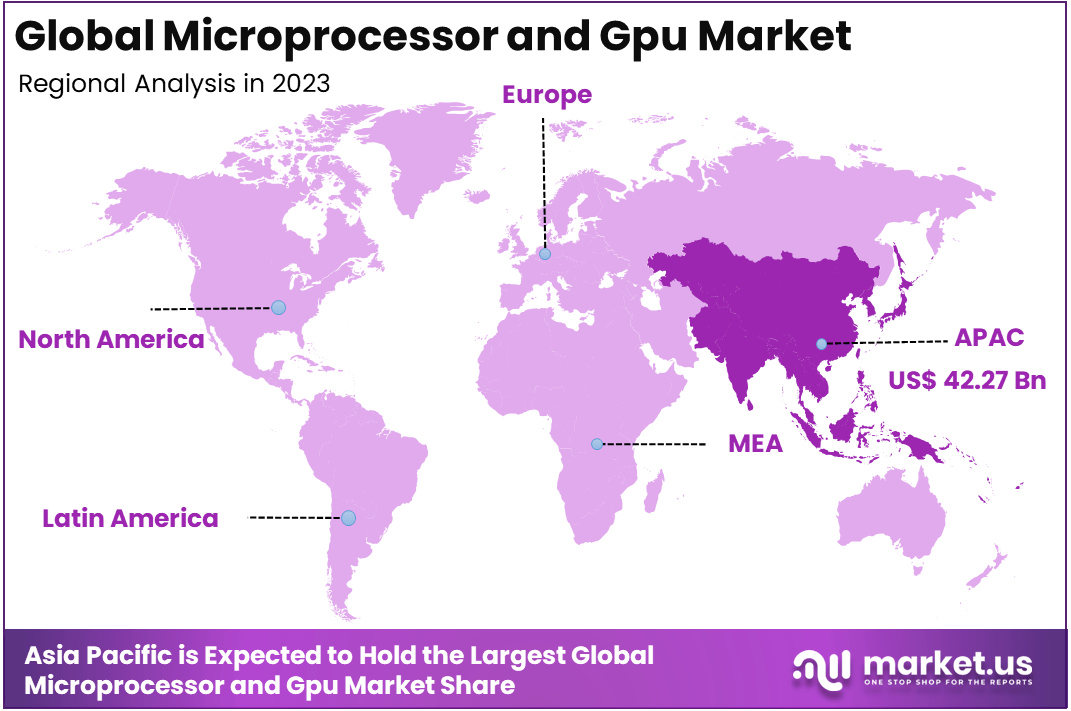

The Global Microprocessor and GPU Market size is expected to be worth around USD 224.8 Billion By 2033, from USD 114.26 Billion in 2023, growing at a CAGR of 7% during the forecast period from 2024 to 2033. In 2023, Asia Pacific held a dominant market position, capturing more than a 37% share, holding USD 42.27 Billion in revenue.

A microprocessor is a central processing unit (CPU) on a single integrated circuit (IC) chip, responsible for executing instructions in computing systems. It performs all arithmetic, logic, control, and input/output operations required for computing tasks.

Microprocessors are the heart of most electronic devices, including computers, smartphones, and other embedded systems. They have evolved from simple, single-core processors to more complex multi-core processors, enabling significant improvements in computational power and energy efficiency.

The Microprocessor Market is primarily driven by the continuous advancements in technology and the rising demand for smarter and faster devices. As the demand for smartphones, tablets, laptops, and wearables grows, microprocessors are becoming increasingly advanced to handle more complex applications, artificial intelligence (AI), machine learning (ML), and 5G connectivity.

The market is expected to witness significant growth with new technological advancements, such as quantum computing and 3D chip architectures, paving the way for the next generation of microprocessors. Additionally, the increasing penetration of the Internet of Things (IoT) is creating a high demand for low-power, efficient microprocessors in devices like smart home gadgets and automotive systems.

A graphics processing unit (GPU) is a specialized processor designed to accelerate the rendering of images, video, and animations in electronic devices. Initially designed for rendering graphics in video games, GPUs have become essential for a range of applications beyond gaming, including AI, deep learning, and cryptocurrency mining. GPUs are highly parallelized, which means they can process a large number of tasks simultaneously, making them ideal for handling workloads that require high-performance computing power.

The GPU Market is experiencing rapid growth, driven by factors such as the increasing adoption of AI and machine learning algorithms, the rise in cryptocurrency mining, and the expansion of gaming. Technological advancements, such as the development of cloud gaming and AI-powered video editing software, have boosted the demand for high-performance GPUs.

The market is also benefiting from the rise of data centers and the expansion of 5G technology, which demands greater computational power. Opportunities lie in the further integration of GPUs in sectors such as automotive (for autonomous vehicles) and healthcare (for medical imaging and research). The growing popularity of edge computing and the need for real-time processing also present substantial growth opportunities for GPU manufacturers.

The Microprocessor and GPU Market is primarily driven by the constant need for more processing power and better performance in modern electronics. The proliferation of AI, big data analytics, and cloud computing has drastically increased the demand for processors that can handle high volumes of complex tasks simultaneously.

Additionally, the rising consumer demand for high-performance gaming, VR/AR applications, and autonomous systems is propelling the development of more powerful GPUs. The shift towards multi-core microprocessors and the development of specialized processors for AI applications are also contributing significantly to market growth.

Furthermore, the adoption of 5G technology is expected to drive innovation in both microprocessor and GPU sectors, enabling faster data processing and enhancing the overall computing experience. The demand for microprocessors and GPUs is expected to remain strong due to the increased usage of high-performance computing applications.

The continued growth in sectors such as gaming, automotive (for self-driving cars), AI, cloud computing, and edge computing will fuel demand for these processors. GPUs are particularly in demand for tasks such as cryptocurrency mining, high-resolution video processing, and AI-driven tasks that require parallel computing.

As businesses and consumers seek more power-efficient and faster processing systems, companies are expected to invest more in developing next-gen processors that integrate AI and IoT capabilities. The Microprocessor and GPU Market has seen significant technological advancements over the years, with ongoing improvements in processing power, energy efficiency, and design complexity.

Recent innovations include multi-core processors, which significantly enhance parallel processing and enable devices to handle more tasks simultaneously. Additionally, advancements in AI-accelerated GPUs have enabled faster processing of AI workloads, providing enhanced performance in machine learning and data analytics.

The transition to smaller process nodes (such as 3nm and 5nm technology) has improved performance while reducing power consumption, benefiting not only consumer electronics but also data centers and AI-based applications.

Microprocessors and GPUs are critical components in modern computing, each with distinct performance metrics and specifications. Microprocessors typically operate at clock speeds ranging from 1 GHz to over 5 GHz, with some high-performance models achieving speeds up to 6 GHz.

They often feature multiple cores, with common configurations including Dual-core (2 cores), Quad-core (4 cores), Hexa-core (6 cores), and octa-core (8 cores), allowing for parallel processing capabilities. The number of instructions per cycle (IPC) can vary significantly based on architecture, with values typically ranging from 1 to 4, impacting overall performance.

Additionally, microprocessors utilize cache memory effectively, with L1 cache sizes generally around 32 KB per core, L2 cache sizes from 256 KB to 1 MB per core, and L3 cache sizes reaching up to 32 MB shared among all cores.

On the other hand, Graphics Processing Units (GPUs) are designed for parallel processing and are essential for rendering graphics and performing complex computations. Modern GPUs can have thousands of cores; for instance, NVIDIA’s Ampere architecture features up to 10,752 CUDA cores.

GPU clock speeds usually range from 1 GHz to 2.5 GHz, depending on the model and workload. Memory bandwidth is another critical metric, with high-end GPUs achieving bandwidths exceeding 800 GB/s. The memory size in contemporary GPUs varies widely.

With common configurations including 4 GB, 8 GB, and even up to 48 GB of GDDR6 memory in top-tier models. Furthermore, GPUs support various architectures optimized for different tasks, such as Tensor Cores for AI computations and Ray Tracing Cores for enhanced graphics rendering.

Key Takeaways

- Market Growth: The global Microprocessor and GPU Market was valued at USD 114.26 Billion in 2023 and is expected to reach USD 224.8 Billion by 2033, with a CAGR of 7% over the forecast period.

- Market Dominance by Microprocessors: The Microprocessor segment dominates the market, capturing more than 60% of the market share in 2023. This is due to the widespread use of microprocessors in various devices, including computers, smartphones, and consumer electronics.

- Leading Architecture: The x86 architecture holds a significant share of 56% in 2023. This is driven by its use in a wide range of computing applications, especially in personal computers, laptops, and workstations.

- Consumer Electronics Application: The Consumer Electronics segment accounts for 42% of the market, indicating the growing demand for microprocessors and GPUs in consumer products such as smartphones, gaming consoles, and smart devices.

- Regional Market Leadership: Asia-Pacific (APAC) holds the largest regional share of 37% in 2023, largely due to the high demand for electronic devices and the growing technological advancements in countries like China, Japan, and South Korea.

- Future Growth: With a CAGR of 7%, the market is expected to continue expanding, driven by the growing demand for high-performance computing, AI applications, and advanced consumer electronics.

By Type

In 2023, the Microprocessor segment held a dominant market position, capturing more than 60% of the total market share. The microprocessor’s leading role in the market can be attributed to its essential function in powering a wide array of devices, including personal computers, smartphones, tablets, and embedded systems.

As the central processing unit (CPU) of a system, the microprocessor handles a variety of computational tasks, making it indispensable across many industries, such as consumer electronics, automotive, and industrial automation.

The dominance of the microprocessor segment is also supported by its significant presence in the personal computing market, where high-performance microprocessors are integral to running advanced applications. The rise of AI, machine learning, and gaming further accelerates the demand for more powerful microprocessors capable of supporting complex operations.

In addition, the integration of microprocessors in Internet of Things (IoT) devices is boosting the overall demand, expanding their presence into smart home devices, wearable technologies, and connected vehicles.

While GPUs (Graphics Processing Units) also play an essential role in high-performance applications like gaming and AI computing, they serve more specialized needs compared to microprocessors. Microprocessors, being the core unit in nearly all computing systems, continue to dominate the market due to their broad applicability across different sectors.

The ability of microprocessors to handle both general-purpose and specific computing tasks, combined with advancements in their processing power and energy efficiency, further cements their leading position in the market.

By Architecture

In 2023, the x86 architecture segment held a dominant market position, capturing more than 56% of the market share. The x86 architecture, which has been the backbone of personal computing for decades, remains the leading architecture in both microprocessors and GPUs.

This dominance is primarily driven by its widespread use in desktops, laptops, and servers, especially in the consumer electronics and enterprise markets. The x86 architecture has been a consistent performer due to its strong legacy in personal computers, where it powers nearly all Windows-based devices and a significant portion of workstations.

The key reason behind the continued dominance of the x86 architecture is its long-standing presence and compatibility with a wide range of software applications. Many operating systems, such as Windows, Linux, and macOS, are optimized for x86 processors, making them the default choice for both consumers and enterprises.

Furthermore, the architecture’s compatibility with legacy applications and support for high-performance computing tasks like gaming, data processing, and AI further strengthens its position in the market. The ongoing development of high-performance chips based on x86 architecture, such as Intel’s Core and AMD’s Ryzen series, continues to fuel its market share.

Another factor contributing to the leadership of x86 in the market is the significant investment made by major semiconductor companies in optimizing the architecture for modern computing needs. Companies like Intel and AMD have continuously improved x86 chips to deliver better energy efficiency, multi-core processing capabilities, and higher speeds, making them indispensable for a wide range of applications.

Additionally, the scalability of x86 processors, especially in data centers and cloud computing, ensures their continued dominance as the demand for cloud services and high-performance computing grows.

By Application

In 2023, the Consumer Electronics segment held a dominant market position, capturing more than 42% of the microprocessor and GPU market share. This leadership can be attributed to the pervasive use of microprocessors and GPUs in a wide range of consumer electronic devices, such as smartphones, laptops, gaming consoles, tablets, and smart TVs.

The consumer electronics sector has become one of the primary drivers of demand for high-performance microprocessors and GPUs, as consumers increasingly demand more advanced, faster, and more power-efficient devices.

A key factor propelling the dominance of the consumer electronics segment is the rising demand for high-end smartphones and gaming consoles. Devices like smartphones, which have become essential for communication, entertainment, and productivity, rely heavily on powerful microprocessors and GPUs for tasks such as gaming, photo and video editing, and seamless multitasking.

Similarly, the gaming industry’s growth has spurred the need for advanced GPUs, as high-definition graphics, faster rendering, and smoother performance are critical for modern gaming experiences. This ongoing innovation and upgrading of consumer devices continuously boost demand for high-performance processors.

The expansion of smart home devices, wearables, and virtual assistants is also contributing significantly to the growth of the consumer electronics segment. With the rise of the Internet of Things (IoT) and increased consumer reliance on smart devices, the need for powerful and efficient microprocessors and GPUs to process real-time data and perform complex functions is at an all-time high.

Moreover, consumer interest in immersive technologies such as virtual reality (VR) and augmented reality (AR) is further fueling the demand for powerful GPUs capable of handling sophisticated graphics and real-time processing.

Key Market Segments

By Type

- Microprocessor

- GPU

By Architecture

- x86

- ARM

- Others

By Application

- Consumer Electronics

- Automotive

- Healthcare

- Industrial

- Aerospace & Defense

- Others

Driving Factors

Increasing Demand for High-Performance Computing

The escalating need for high-performance computing (HPC) is a significant driver of the microprocessor and GPU market. Industries such as artificial intelligence (AI), machine learning (ML), data analytics, and scientific research require advanced computational capabilities to process vast amounts of data efficiently.

For instance, AI applications demand powerful processors to handle complex algorithms and large datasets, leading to a surge in demand for high-performance microprocessors and GPUs. The proliferation of data centers and cloud computing services further amplifies this demand.

As businesses and consumers generate and consume more data, the need for robust processing power to manage and analyze this information becomes critical. This trend is evident in the expansion of cloud service providers investing heavily in advanced microprocessors and GPUs to enhance their service offerings.

For example, major cloud providers are integrating GPUs into their infrastructure to support AI and ML workloads, thereby driving the market for these processors. Additionally, the gaming industry contributes significantly to the demand for high-performance GPUs.

With the advent of 4K gaming, virtual reality (VR), and augmented reality (AR), gamers seek superior graphics and processing capabilities, propelling the need for advanced GPUs. This consumer-driven demand has led to continuous innovation and competition among GPU manufacturers, further stimulating market growth.

Restraining Factors

High Development and Manufacturing Costs

A significant restraint in the microprocessor and GPU market is the high development and manufacturing costs associated with producing advanced processors. Developing cutting-edge microprocessors and GPUs requires substantial investment in research and development (R&D), as well as in state-of-the-art manufacturing facilities.

For instance, the development of 7nm and 5nm process nodes involves complex fabrication techniques and significant capital expenditure, which can be a financial burden for manufacturers. The microprocessor market faces challenges such as high design and production costs, which can hinder market growth.

Moreover, the rapid pace of technological advancement means that products can become obsolete quickly, leading to increased pressure on manufacturers to innovate continuously. This constant need for innovation requires ongoing investment, which can strain financial resources, especially for smaller companies.

Additionally, the global semiconductor supply chain is complex and susceptible to disruptions, such as shortages of raw materials and geopolitical tensions. These factors can lead to increased production costs and delays, further impacting the profitability of manufacturers. For example, the COVID-19 pandemic highlighted vulnerabilities in the supply chain, leading to shortages of essential components and increased costs.

Growth Opportunities

Growth in Artificial Intelligence and Machine Learning Applications

The rapid advancement of artificial intelligence (AI) and machine learning (ML) technologies presents a substantial opportunity for the microprocessor and GPU market. AI and ML applications require powerful processors capable of handling complex computations and large datasets efficiently. GPUs, in particular, are well-suited for parallel processing tasks inherent in AI and ML workloads, making them essential components in AI infrastructure.

Industries such as healthcare, automotive, and finance are increasingly adopting AI and ML technologies, creating a growing demand for high-performance processors. In healthcare, AI is used for tasks like medical imaging analysis and drug discovery, requiring advanced processing capabilities.

In the automotive sector, AI powers autonomous driving systems, necessitating powerful processors for real-time data processing. Similarly, the finance industry utilizes AI for algorithmic trading and fraud detection, further driving the demand for advanced processors.

Furthermore, the rise of edge computing, where data processing occurs closer to the data source, is increasing the need for powerful processors in devices such as smartphones, IoT devices, and autonomous vehicles. This trend presents opportunities for manufacturers to develop specialized processors tailored for edge computing applications.

Challenging Factors

Supply Chain Disruptions and Geopolitical Tensions

A significant challenge facing the microprocessor and GPU market is the vulnerability of the semiconductor supply chain to disruptions and geopolitical tensions. The global semiconductor industry relies on a complex network of suppliers for raw materials, manufacturing equipment, and specialized components.

Disruptions in this supply chain can lead to shortages of essential components, production delays, and increased costs. For example, the COVID-19 pandemic exposed vulnerabilities in the supply chain, leading to shortages of semiconductors and delays in production across various industries.

In addition to geopolitical concerns, natural disasters, such as earthquakes and floods, can impact semiconductor manufacturing facilities. These events have the potential to halt production for extended periods, which disrupts the supply of microprocessors and GPUs to various industries.

For instance, Japan and Taiwan are key hubs for semiconductor manufacturing, and natural disasters in these regions can cause significant setbacks for global semiconductor production. Furthermore, the semiconductor supply chain is highly dependent on complex manufacturing processes that require specialized equipment and expertise.

A shortage of skilled labor, as well as insufficient manufacturing capacity, can create bottlenecks in production, making it difficult to meet the growing demand for microprocessors and GPUs.

Growth Factors

The Microprocessor and GPU Market is experiencing substantial growth, driven by several key factors. The increasing demand for high-performance computing in sectors such as gaming, artificial intelligence (AI), and data centers is a primary driver.

Advancements in manufacturing technologies have enabled the production of more powerful and efficient chips, meeting the evolving needs of these industries. Additionally, the rise of cloud gaming and machine learning applications has further propelled market expansion.

Emerging Trends

Several emerging trends are shaping the microprocessor and GPU market. There is a significant focus on developing high-performance processors with advanced features, including integration of AI capabilities and energy-efficient designs.

Manufacturers are emphasizing the launch of processors that can handle heavy computing workloads in AI applications, aiming to challenge existing market leaders.

Business Benefits

For businesses operating in the microprocessor and GPU market, these growth factors and emerging trends present several benefits. Companies that invest in developing high-performance processors with advanced features can gain a competitive advantage, catering to the increasing demand in sectors like AI and data centers.

Additionally, focusing on energy-efficient solutions can attract environmentally conscious consumers and businesses, aligning with global sustainability goals. Expanding into emerging markets and forming strategic partnerships can also open new revenue streams and enhance market presence.

Regional Analysis

In 2023, Asia-Pacific held a dominant position in the Microprocessor and GPU Market, capturing more than a 37% share and generating approximately USD 42.27 billion in revenue. This stronghold can be attributed to the rapid technological advancements and booming consumer electronics industry across major economies such as China, Japan, South Korea, and India.

The region’s high demand for GPUs and microprocessors is fueled by the increasing adoption of smartphones, laptops, gaming devices, and other consumer electronics, which are integral to daily life in these nations.

One of the primary reasons for Asia-Pacific’s leadership is its role as a global manufacturing hub. The region houses key semiconductor giants like TSMC (Taiwan Semiconductor Manufacturing Company) and Samsung Electronics, which are at the forefront of producing advanced microprocessors and GPUs.

These companies cater not only to domestic demand but also serve global markets, ensuring that Asia-Pacific remains the focal point of the semiconductor supply chain. Moreover, the growing investments in AI-driven technologies, 5G networks, and IoT applications are further strengthening the demand for high-performance processors in the region.

The booming gaming industry in Asia-Pacific is another critical growth driver. Countries like China and South Korea are known for their massive gaming communities, which demand cutting-edge GPUs for immersive gaming experiences.

In 2023, China alone accounted for a significant portion of gaming-related GPU sales, further solidifying the region’s market dominance. Additionally, the increasing popularity of esports in the region has created a substantial market for high-performance GPUs and microprocessors, making Asia-Pacific a key player in the global market landscape.

Asia-Pacific’s leadership is further reinforced by government initiatives to boost the semiconductor industry. For instance, China’s “Made in China 2025” policy and India’s Semiconductor Mission have been designed to enhance local manufacturing capabilities and reduce dependence on imports.

These initiatives are attracting global tech companies to invest in the region, paving the way for sustained growth. With an ever-expanding consumer base, robust manufacturing infrastructure, and significant investments in advanced technologies, Asia-Pacific is expected to maintain its leading position in the Microprocessor and GPU Market well into the future.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

In 2024, Intel Corporation made significant strides in the semiconductor market by acquiring Tower Semiconductor for USD 5.4 billion. This strategic move aimed to bolster Intel’s manufacturing capabilities, particularly for advanced microprocessors catering to automotive, industrial, and consumer electronics sectors.

Additionally, Intel introduced its latest Meteor Lake architecture for mobile processors, which combines power efficiency with AI-optimized performance, setting a new benchmark for laptops and portable devices.

Intel’s ongoing investments in manufacturing facilities, such as its Arizona and Ohio fabs, reinforce its commitment to meet global demand while competing with other chipmakers in both the microprocessor and GPU domains.

NVIDIA continues to dominate the GPU market with cutting-edge innovation. In 2024, the company launched its Ada Lovelace GPU architecture, tailored for AI-driven workloads and high-performance gaming. This new architecture provides unmatched efficiency for applications ranging from autonomous vehicles to large-scale data centers.

Additionally, NVIDIA expanded its presence in the cloud computing market by partnering with Oracle Cloud Infrastructure to integrate its AI GPUs for advanced data processing and machine learning tasks.

AMD maintained its competitive edge in 2024 with the release of the Ryzen 8000 series processors, built on the advanced 4nm architecture. These processors offer industry-leading performance for gaming and enterprise applications, leveraging enhanced energy efficiency and multi-core processing power.

AMD also announced a collaboration with Microsoft Azure to optimize cloud services with its EPYC processors and Radeon GPUs, ensuring seamless performance for enterprise-level workloads.

Top Key Players in the Market

- Intel Corporation

- NVIDIA Corporation

- AMD (Advanced Micro Devices)

- Qualcomm Incorporated

- Samsung Electronics

- Broadcom Inc.

- IBM Corporation

- MediaTek Inc.

- ARM Limited (SoftBank Group)

- Texas Instruments

- Apple Inc.

- Other Key Players

Recent Developments

- In 2024: NVIDIA Corporation announced the launch of its next-generation Ada Lovelace GPU architecture, designed specifically for AI workloads and high-performance computing. The new GPUs integrate advanced tensor cores and increased memory bandwidth, enabling faster training and inference capabilities for AI models.

- In 2024: Intel Corporation finalized the acquisition of Tower Semiconductor, an Israeli chipmaker, for USD 5.4 billion to expand its manufacturing capacity for advanced microprocessors. This move strengthens Intel’s position in the semiconductor industry by increasing its capabilities in producing chips for consumer electronics, automotive, and industrial applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 114.26 Bn |

| Forecast Revenue (2033) | USD 224.8 Bn |

| CAGR (2024-2033) | 7% |

| Largest Market | North America |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Microprocessor, GPU), By Architecture (x86, ARM, Others), By Application (Consumer Electronics, Automotive, Healthcare, Industrial, Aerospace & Defense, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Intel Corporation, NVIDIA Corporation, AMD (Advanced Micro Devices), Qualcomm Incorporated, Samsung Electronics, Broadcom Inc., IBM Corporation, MediaTek Inc., ARM Limited (SoftBank Group), Texas Instruments, Apple Inc., Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |