Quick Navigation

Report Overview

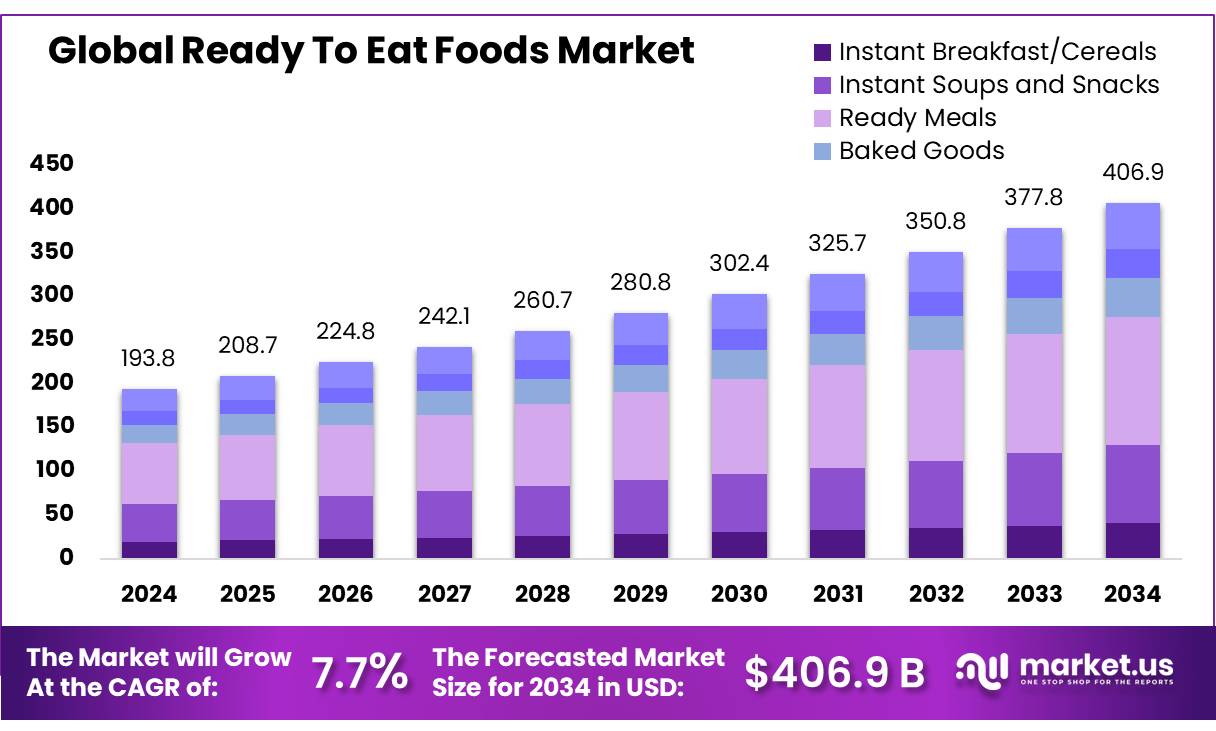

The Global Ready-to-Eat Foods Market size is expected to be worth around USD 406.9 Billion by 2034, from USD 193.8 Billion in 2024, growing at a CAGR of 7.7% during the forecast period from 2025 to 2034.

Foods that are liable to carry a higher risk of infection include ready-to-eat (RTE) foods, These are defined as “foods intended by the producer or manufacturer for direct human consumption without the need for cooking or other processing effective to eliminate or reduce to an acceptable level microorganisms of concern.

This sector encompasses a broad range of products, including frozen dinners, pre-packaged salads, snacks, and cooked grains that are prepped for immediate consumption, reflecting a major shift in eating habits globally.

The industrial scenario of the RTE foods market is marked by robust production innovations and packaging advancements that ensure food safety, extend shelf life, and maintain nutritional value. Leading players in the food industry have adopted technologies such as High-Pressure Processing (HPP) and Modified Atmosphere Packaging (MAP) to meet these needs.

Additionally, a rise in disposable incomes and consumer awareness regarding health-conscious diets are pushing demand for premium, organic, and health-centric RTE options. Statistically, urban consumers spend an average of 35% of their food budget on convenience foods.

Key Takeaways

-

The Global Ready-to-Eat Foods Market is anticipated to grow from USD 193.8 Bn in 2024 to USD 406.9 Bn by 2034, a CAGR of 7.7% during the forecast period from 2025 to 2034.

-

The Ready Meals segment dominated the market, holding a 36.1% share, favored for their convenience and variety.

-

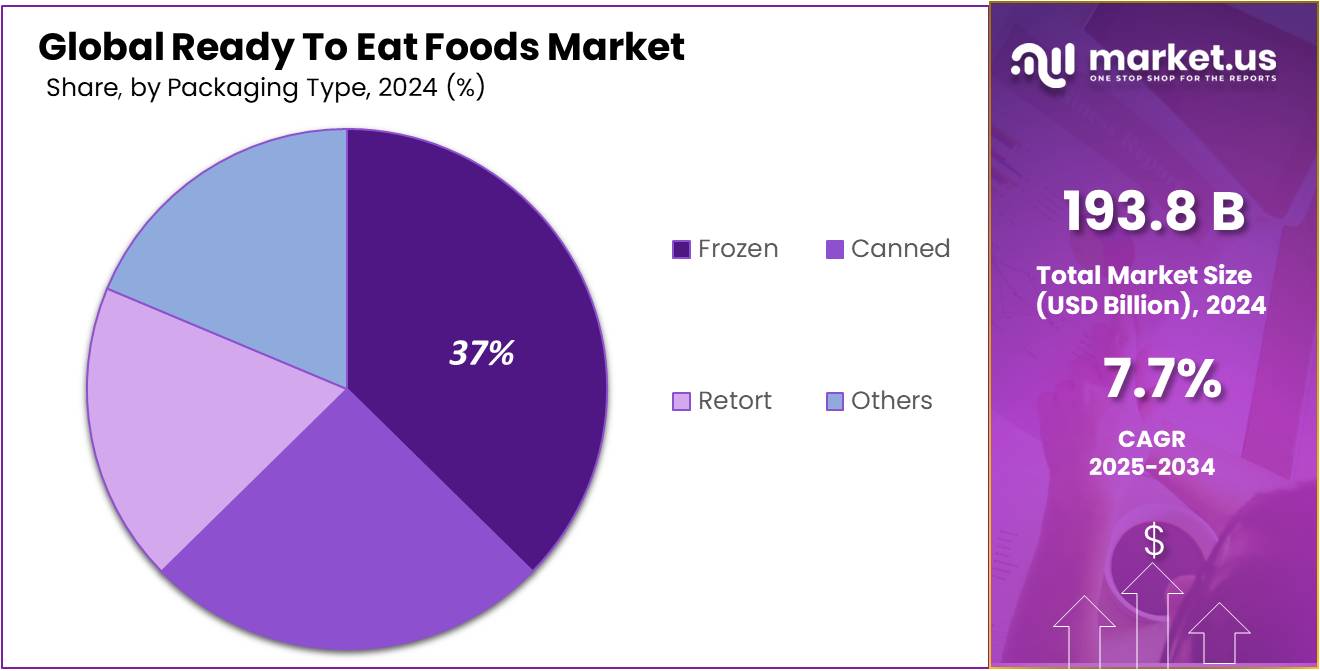

Frozen packaging was the leading segment, capturing a 37.8% share, crucial for preserving food quality, taste, and nutritional value.

-

Individual consumers were the largest consumer group, with a 63.2% market share, highlighting the significant role of convenience for people with busy lifestyles.

-

These outlets were the predominant distribution channels, holding a 51.2% share, offering diverse and accessible Ready-to-Eat food options under one roof.

-

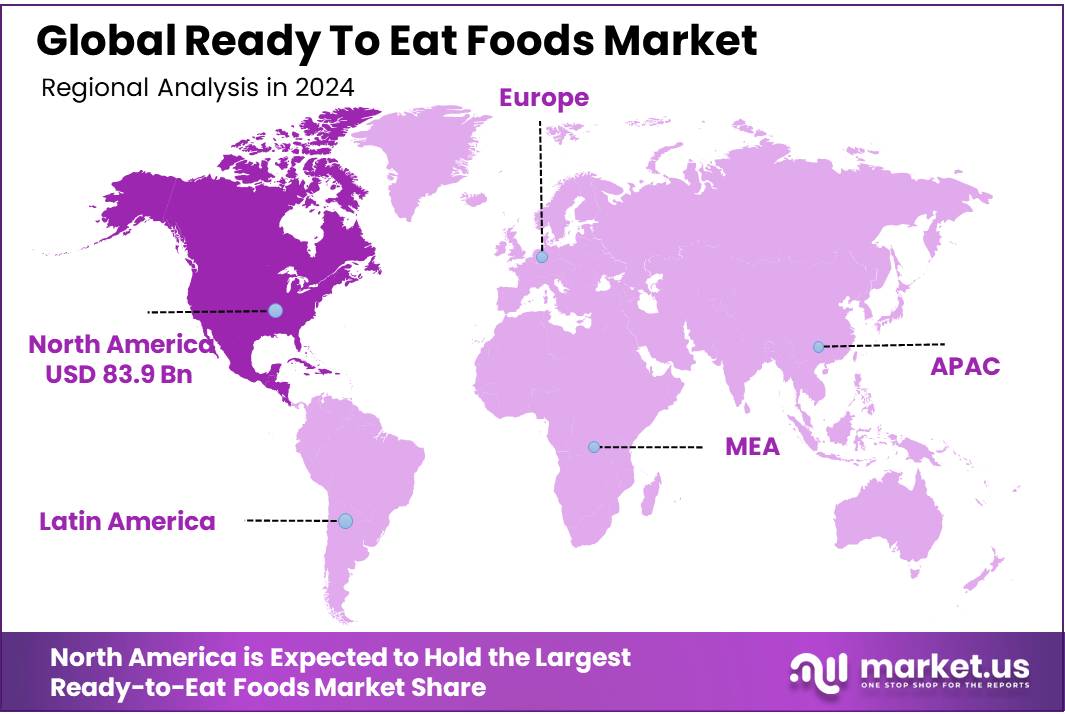

North America, particularly the U.S., will lead the Ready-to-Eat foods market in 2024 with a 43.3% share, driven by a fast-paced lifestyle and high consumer spending power.

By Product Type

In 2024, Ready Meals held a dominant market position, capturing more than a 36.1% share of the global Ready-to-Eat Foods market. This segment’s strong performance is attributed to its wide acceptance among consumers seeking quick dining solutions without the hassle of preparation.

Ready Meals include a variety of options such as frozen dinners, refrigerated meals, and shelf-stable dinners, catering to a diverse range of tastes and dietary preferences. The convenience offered by Ready Meals, combined with their longer shelf life and ease of preparation, has made them particularly popular in urban areas where time is often at a premium.

This segment has also benefited from continuous innovation by manufacturers who have focused on improving taste, nutritional value, and variety to meet consumer demands. As a result, Ready Meals have not only retained their appeal among traditional consumers but have also attracted health-conscious individuals looking for balanced diet options.

By Packaging Type

In 2024, Frozen packaging held a dominant market position in the Ready-to-Eat foods sector, capturing more than a 37.8% share. This segment’s leadership stems from its crucial role in preserving the quality, taste, and nutritional value of foods, making it a top choice for consumers prioritizing convenience and longevity in their meal selections.

Frozen Ready-to-Eat foods encompass a broad spectrum, from complete meals to individual components like vegetables and proteins, offering versatility and ease for meal preparation. The popularity of frozen Ready-to-Eat foods is particularly pronounced in regions with busy urban lifestyles, where time constraints make cooking daily meals challenging.

The frozen method locks in freshness and reduces food wastage, aligning with consumer trends toward sustainability and efficient living. Technological advancements in freezing techniques have also enhanced the texture and taste of these products, broadening their appeal.

By End-User

In 2024, Individual Consumers held a dominant market position in the Ready-to-Eat foods sector, capturing more than a 63.2% share. This substantial portion underscores the significant role that convenience plays in the daily lives of consumers.

Individual buyers, particularly those with fast-paced or busy lifestyles, gravitate toward Ready-to-Eat foods as a practical solution to save time and effort without compromising on the quality of their meals. The preference for Ready-to-Eat foods among individual consumers is further driven by the diversity of options available that cater to various dietary preferences, including organic, gluten-free, and vegan choices.

The segment benefits from the increasing number of single-person households and the rising trend of smaller family units, both of which contribute to the growing demand for single-serving and easy-to-prepare food products.

By Distribution Channel

In 2024, Hypermarkets and Supermarkets held a dominant market position in the distribution of Ready-to-Eat foods, capturing more than a 51.2% share. This channel’s predominance is largely attributed to its ability to offer a wide array of Ready-to-Eat products under one roof, providing convenience and accessibility to consumers.

The physical presence of these stores allows customers to browse and compare a diverse selection of products, making it easier for them to make informed purchasing decisions based on quality, price, and dietary preferences. Hypermarkets and supermarkets are particularly favored for their regular promotions and discounts, which attract budget-conscious consumers looking for value in their purchases.

Key Market Segments

By Product Type

- Ready Meals

- Instant Breakfast and Cereals

- Instant Soups and Snacks

- Baked Goods

- Meat Products

- Others

By Packaging Type

- Frozen

- Canned

- Retort

- Others

By End-User

- Individual Consumers

- Foodservice & Catering

- Institutional Use

- Others

By Distribution Channel

- Hypermarkets and Supermarkets

- Convenience Stores

- Online Retail Stores

- Others

Drivers

Increasing Urbanization and Busy Lifestyles

One of the major driving factors for the growth of the Ready-to-Eat foods market is the rapid urbanization and increasingly busy lifestyles of consumers globally. As more individuals move to urban areas for employment opportunities, there is a noticeable shift in lifestyle that prioritizes convenience and time-saving options.

This urban migration has been significant, with the United Nations estimating that 68% of the world’s population will live in urban areas by 2050. The demand for Ready-to-Eat foods is further amplified by the hectic schedules that leave urban dwellers with limited time for traditional cooking.

According to data from the United States Department of Agriculture (USDA), the average American spends approximately 37 minutes a day in food preparation and cleanup, a significant decrease from past decades.

Restraints

Health Concerns Associated with Preservatives and Additives

One of the major restraining factors in the growth of the Ready-to-Eat (RTE) foods market is the growing consumer concern over the health impacts of preservatives and additives used in these products. As awareness increases about the potential health risks associated with long-term consumption of artificial preservatives and high levels of sodium and sugar, consumers are becoming more cautious about their food choices.

According to the World Health Organization (WHO), reducing salt intake to less than 5 grams per day can help prevent hypertension and reduce the risk of heart disease and stroke in the adult population. However, many RTE products contain high levels of sodium to enhance flavor and extend shelf life, which can significantly exceed daily intake recommendations.

Opportunity

Increased Consumer Demand for Convenience

A significant growth factor for the Ready-to-Eat (RTE) foods market is the increasing demand for convenience among consumers globally. This trend is primarily driven by the fast-paced lifestyles of modern consumers who are looking for quick and easy meal solutions that fit their busy schedules.

As work hours extend and commuting times increase, the time available for traditional cooking diminishes, making RTE foods an appealing option. According to a survey by the Food Industry Association, over 55% of adults in urban areas prefer to purchase Ready-to-Eat (RTE) foods several times a week due to their convenience.

These foods eliminate the need for preparation and cooking, saving valuable time and effort. Moreover, the improvement in packaging technology has enabled RTE foods to maintain their taste and nutritional quality, enhancing their attractiveness to consumers who do not want to compromise on the quality of their diet.

Trends

Plant-Based Innovations Driving Market Expansion

An emerging factor significantly impacting the growth of the Ready-to-Eat (RTE) foods market is the surge in consumer interest and demand for plant-based products. This shift is largely influenced by a growing awareness of health, environmental concerns, and ethical considerations regarding animal welfare.

Recent surveys from global food organizations highlight that the plant-based food market is expected to grow exponentially. For instance, a report by the United Nations Food and Agriculture Organization underscores the environmental benefits of a plant-based diet, which has encouraged more consumers to make the switch from traditional animal-based products.

Regional Analysis

North America continues to lead the Ready-to-Eat (RTE) foods market, commanding a significant 43.3% market share, which translated into revenue of approximately USD 83.9 billion in 2024. This dominance is largely driven by the United States, where a fast-paced lifestyle and high consumer spending power combine to bolster the demand for convenient meal solutions.

The regional market benefits from advanced food processing technologies and high standards in food safety regulations, ensuring that RTE foods are not only convenient but also safe and of high quality. The substantial market share in North America is supported by a well-established retail infrastructure, which makes RTE foods widely available through various channels, including supermarkets, hypermarkets, and online platforms.

The presence of major food corporations in the region, which continuously innovate and expand their product portfolios, also plays a critical role in driving the market forward. These companies often introduce healthier, organic, and niche products to cater to the diverse dietary preferences and health-conscious trends prevalent among North American consumers.

The North American market is characterized by a high level of consumer awareness regarding the nutritional content of foods. This has encouraged manufacturers to develop and market RTE products that align with the evolving health trends, such as low-carb, high-protein, and plant-based diets.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

- Campbell Soup Company is a major player in the ready-to-eat foods market, known for its iconic soups, sauces, and snacks. With a focus on convenience and nutrition, it offers products like ready-to-serve soups and meal kits.

- Conagra Brands excels in the ready-to-eat foods market with a diverse portfolio, including frozen meals, snacks, and pantry staples. Brands like Healthy Choice and Marie Callender’s cater to convenience-driven and health-conscious consumers.

- Dr. Oetker is a prominent name in the ready-to-eat foods market, specializing in frozen pizzas, desserts, and baking mixes. Known for quality and convenience, it appeals to consumers seeking easy meal solutions.

- Kellogg’s dominates the ready-to-eat foods market with its breakfast cereals, snacks, and convenience meals. Known for brands like Corn Flakes, it targets busy lifestyles with nutritious, quick options.

- Amy’s Kitchen stands out in the ready-to-eat foods market with its organic, vegetarian, and vegan offerings, including frozen meals and soups. Catering to health-conscious consumers, it emphasizes natural ingredients and sustainability.

Top Key Players in the Market

- Campbell Soup Company

- Conagra Brands

- Dr. Oetker

- General Mills

- Kellogg’s Amy’s Kitchen

- Kraft Heinz

- Nestlé

- Nomad Foods

- Tyson Foods

- Unilever

Recent Developments

- In 2025, Campbell Soup Company’s market presence will be bolstered by a strong brand reputation and innovation in healthier options. The company competes through strategic acquisitions and a wide distribution network, targeting busy consumers seeking quick, flavorful meals.

- In 2025, Conagra emphasizes product innovation, such as plant-based options, and leverages e-commerce growth. Its strong supply chain and partnerships enhance market reach, positioning it as a key competitor in the evolving food industry.

- In 2025, Dr. Oetker company will strengthen its global footprint through innovation and premium offerings. Its focus on taste and variety, combined with strategic marketing, ensures a competitive edge in the fast-paced, convenience-focused food sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 193.8 Billion |

| Forecast Revenue (2034) | USD 406.9 Billion |

| CAGR (2025-2034) | 7.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Ready Meals, Instant Breakfast and Cereals, Instant Soups and Snacks, Baked Goods, Meat Products, Others), By Packaging Type (Frozen, Canned, Retort, Others), By End-User (Individual Consumers, Foodservice & Catering, Institutional Use, Others), By Distribution Channel (Hypermarkets and Supermarkets, Convenience Stores, Online Retail Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Campbell Soup Company, Conagra Brands, Dr. Oetker, General Mills, Kellogg’s Amy’s Kitchen, Kraft Heinz, Nestlé, Nomad Foods, Tyson Foods, Unilever |

| Customization Scope | Customization for segments at the regional/country level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited Users and Printable PDF) |