Quick Navigation

Report Overview

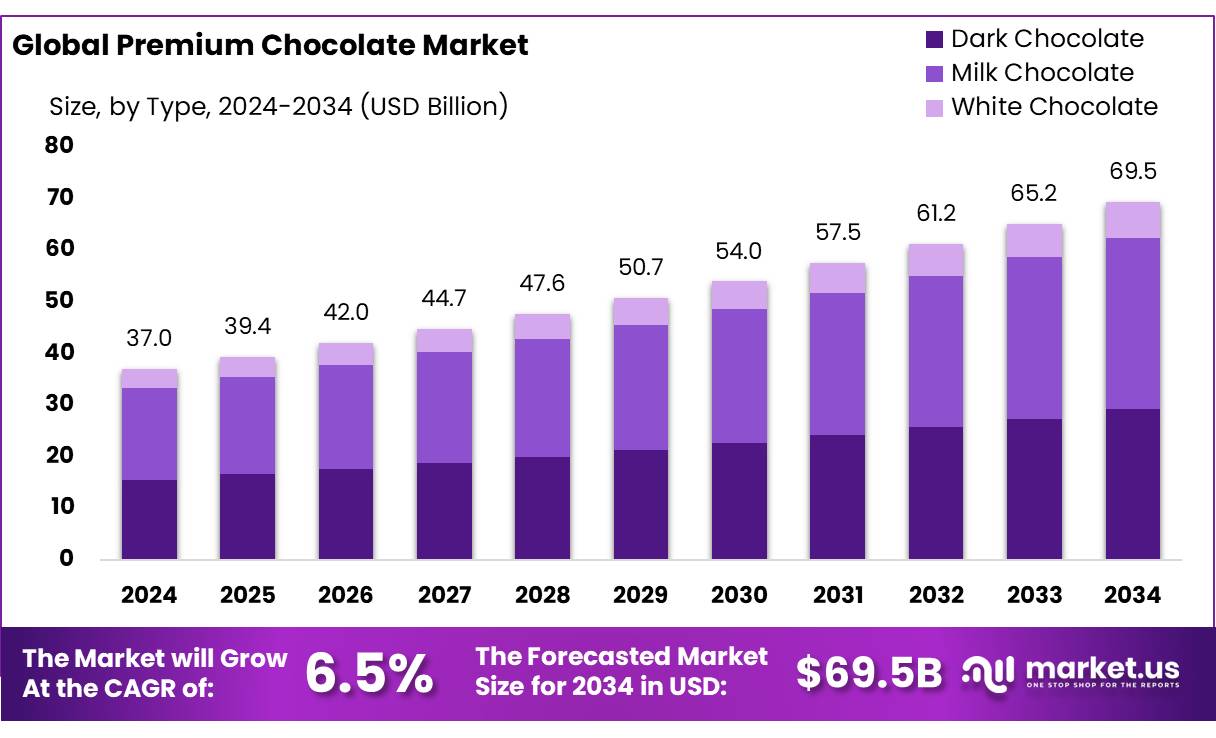

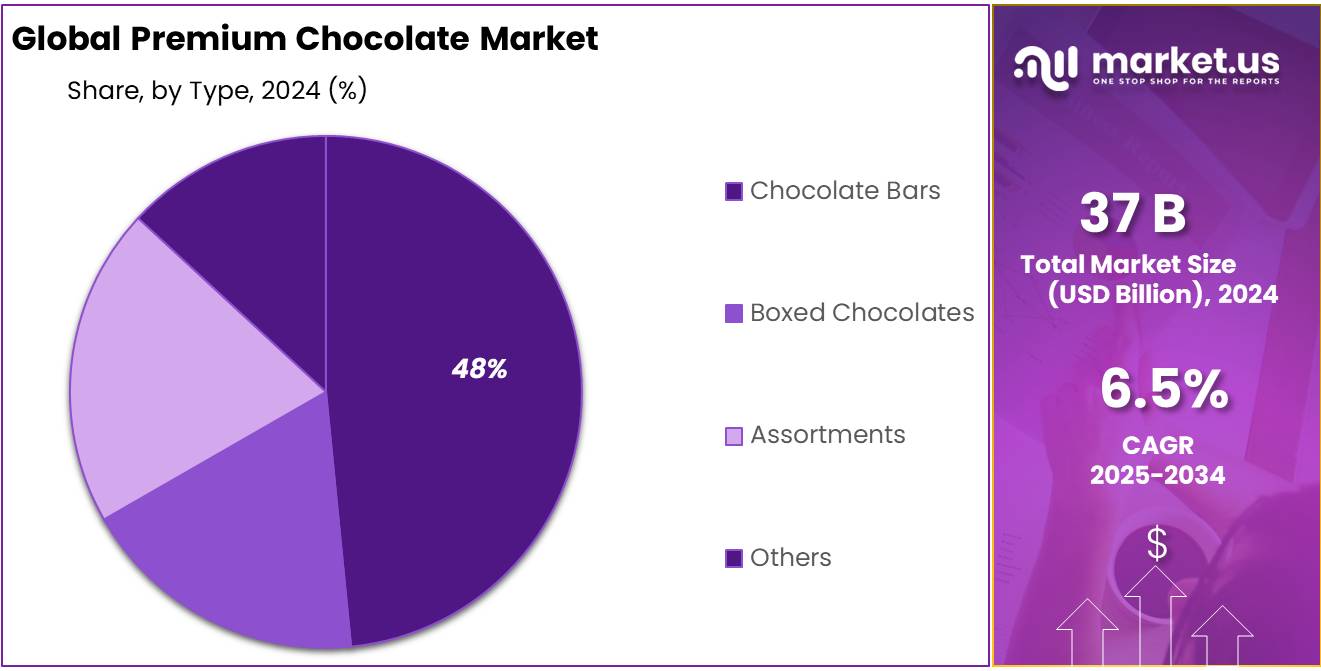

The Global Premium Chocolate Market size is expected to be worth around USD 69.5 Bn by 2034, from USD 37.0 Bn in 2024, growing at a CAGR of 6.5% during the forecast period from 2025 to 2034.

The growth of premium product ranges in the global market is largely driven by continuous innovation from manufacturers, particularly the introduction of new and unique flavors aimed at attracting consumers. This includes the incorporation of indulgent “comfort foods” like bacon, cereal, and cookie dough into premium offerings. Additionally, the use of distinct flavors, such as gourmet salts and alcohol, further boosts the appeal of these products, contributing to their expanding market share.

Premium chocolates, which are crafted with high-quality ingredients and precision, exemplify this trend. These chocolates are typically characterized by higher cocoa content, which enhances their richness and complexity compared to standard chocolates. Many premium varieties also feature single-origin cocoa, sourced from specific regions or countries, offering a unique flavor profile that reflects the terroir. Furthermore, these chocolates are often handcrafted, with meticulous attention to detail in their creation and decoration, making them a luxury product.

As noted in a 2023 report from the International Cocoa Organization, there is a growing consumer preference for exclusive confectionery products that feature unique flavor profiles and high-quality ingredients. The desire for rare and distinctive items that offer a sense of exclusivity and prestige is increasingly influencing purchasing behavior.

Africa, particularly countries such as Ivory Coast and Ghana, plays a dominant role in the global cocoa supply, producing approximately 70% of the world’s cocoa. However, this reliance on African cocoa creates vulnerabilities within the market, as its supply is affected by factors like labor shortages, adverse weather conditions, crop diseases, pests, and political instability.

Key Takeaways

- The global premium chocolate market size is expected to reach USD 69.5 billion by 2034, growing from USD 37.0 billion in 2024 at a CAGR of 6.5%.

- Milk Chocolate had a market share of over 48.4% in 2024, expected to maintain or slightly increase its share due to its popularity.

- Standard Packaging captured over 67.8% of the market share in 2024, due to its practicality and cost-effectiveness.

- Chocolate Bars had a 48.9% market share in 2024, anticipated to remain dominant due to consumer preference for their convenience and variety.

- Hypermarkets and Supermarkets were the leading distribution channels with a 38.4% market share in 2024, expected to stay prominent due to their wide product range.

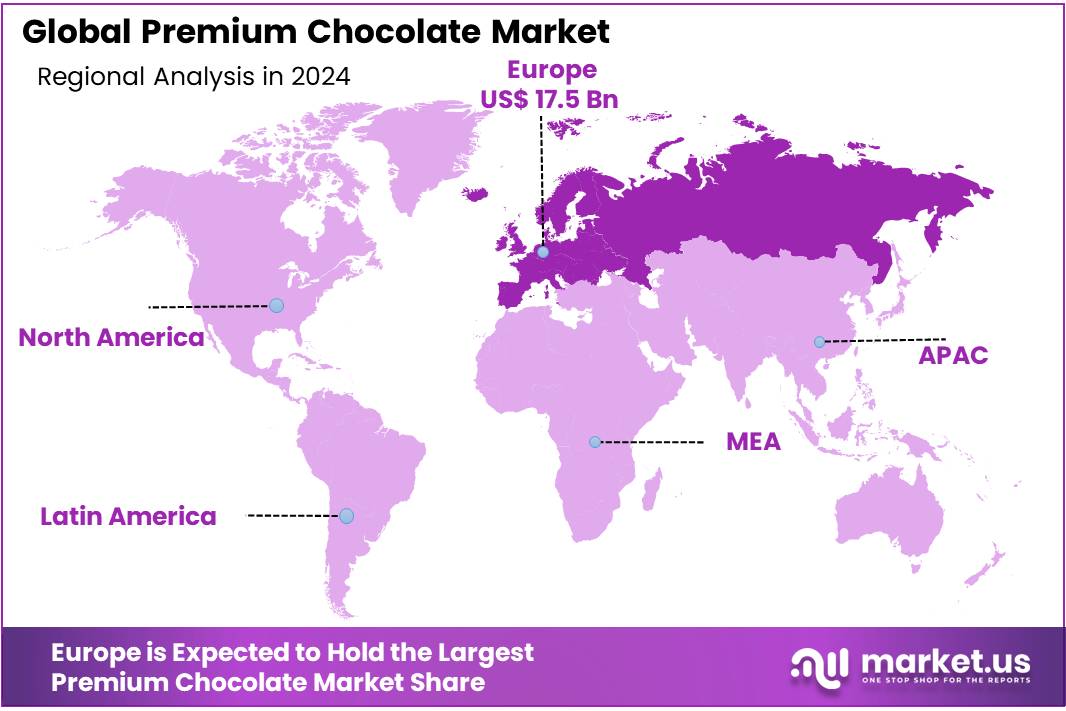

- Europe dominates the regional market with a 47.3% share, valued at approximately USD 17.5 billion.

By Product

In 2024, Milk Chocolate held a dominant market position, capturing more than a 48.4% share of the premium chocolate market. This segment continued to experience strong consumer preference due to its rich, creamy texture and sweetness, making it a staple in both gifting and everyday consumption. As global demand for indulgent and high-quality chocolate grows, milk chocolate has remained the top choice, particularly in regions such as North America and Europe, where it is a key product in the premium chocolate category.

The appeal of milk chocolate can be attributed to its widespread availability and consistent flavor profile, which resonates with a broad demographic. In 2025, the market for milk chocolate is projected to maintain a strong growth trajectory, with expectations to hold a similar market share, if not slightly increase, as consumer tastes continue to favor familiar, comforting options within the premium chocolate space.

By Packaging Type

In 2024, Standard Packaging held a dominant market position, capturing more than a 67.8% share of the premium chocolate market. This packaging type remains the most popular choice among consumers, primarily due to its convenience and cost-effectiveness. Standard packaging is widely used for a range of premium chocolate products, including bars, pralines, and truffles, making it the go-to option for both retailers and consumers alike. It offers a balance between practicality and appeal, with its simple, yet attractive design providing easy storage and transportation, which has contributed to its continued dominance.

As we look toward 2025, the preference for standard packaging is expected to persist, although growth may slow slightly due to the rise of more innovative and sustainable packaging options. However, the cost advantages and wide-ranging use of standard packaging will likely keep it in the lead, with no significant changes expected in its market share. Consumers continue to prioritize practicality, and in many cases, the familiarity and reliability of standard packaging outweigh other factors.

By Type

In 2024, Chocolate Bars held a dominant market position, capturing more than a 48.9% share of the premium chocolate market. The popularity of chocolate bars continues to grow due to their convenience, wide variety of flavors, and portability. As a classic choice for premium chocolate lovers, chocolate bars are available in many forms, from plain milk chocolate to more complex varieties with added ingredients like nuts, fruits, and spices. This versatility has made chocolate bars a top choice for both gifting and personal indulgence.

Looking ahead to 2025, the market share of chocolate bars is expected to remain strong, driven by ongoing consumer demand for easily accessible premium chocolate. While other product types, such as truffles and pralines, are gaining traction, the chocolate bar segment is predicted to maintain its dominant position due to its consistent appeal across different demographics and regions.

By Distribution Channel

In 2024, Hypermarkets & Supermarkets held a dominant market position, capturing more than a 38.4% share of the premium chocolate market. These large retail outlets continue to be the primary point of sale for premium chocolates, offering a wide range of products from popular brands to niche, artisanal options. The convenience of shopping in hypermarkets and supermarkets, along with the ability to easily compare prices and products, has contributed to their sustained dominance in the market.

In 2025, the share of hypermarkets and supermarkets is expected to remain strong, although the rise of online shopping and smaller, specialized retailers may start to capture a larger portion of the market. Despite this, the sheer size and accessibility of hypermarkets and supermarkets will ensure that they remain a key distribution channel for premium chocolates in the coming year. These stores’ ability to cater to mass-market demand while still offering premium options makes them a central hub for chocolate sales.

Key Market Segments

By Product

- Dark Chocolate

- Milk Chocolate

- White Chocolate

By Packaging Type

- Standard Packaging

- Gift Packaging

By Type

- Chocolate Bars

- Boxed Chocolates

- Assortments

- Others

By Distribution Channel

- Hypermarkets & Supermarkets

- Specialty Stores

- Grocery Stores

- Convenience Stores

- Online

- Others

Drivers

Growing Consumer Demand for Premium and Dark Chocolate

One of the major driving factors for the growth of the premium chocolate market is the increasing consumer preference for high-quality, healthier, and indulgent chocolate options. Consumers are becoming more discerning about the quality of ingredients and are willing to spend more on chocolates that are sustainably sourced and made with premium ingredients. Dark chocolate, in particular, has seen a surge in demand due to its perceived health benefits, such as high antioxidant content and lower sugar levels compared to milk chocolate.

According to a report by the National Confectioners Association (NCA), the premium chocolate segment in the United States alone has experienced steady growth, with premium chocolate sales seeing a 6.5% increase in 2023, compared to previous years. This growth is fueled by an increasing awareness of the benefits of dark chocolate, which is often marketed as a healthier indulgence. The NCA highlights that more consumers are seeking chocolate with higher cocoa content, ranging from 60% to 85%, driven by both taste preferences and the growing demand for antioxidant-rich foods.

In addition to health benefits, sustainability has become a major focus for premium chocolate brands. A report by Fairtrade International states that 60% of global chocolate consumers are now willing to pay more for products that have ethical certifications, such as Fairtrade or Rainforest Alliance certification, which guarantee sustainable sourcing practices. These certifications ensure that farmers receive fair wages and that the cocoa is grown in a way that is environmentally friendly, contributing to the long-term growth of the premium chocolate market.

Restraints

Rising Cocoa Prices and Supply Chain Challenges

One of the major restraining factors for the growth of the premium chocolate market is the rising cost of cocoa and the ongoing supply chain challenges. Cocoa, being the primary raw material in chocolate production, has seen significant price increases in recent years.

According to the International Cocoa Organization (ICCO), cocoa prices have risen by nearly 20% in 2023 due to various factors, including poor harvests in key producing countries like Ivory Coast and Ghana, as well as increasing demand for sustainable and traceable sourcing practices. These price hikes directly impact the cost of premium chocolate production, making it more expensive for manufacturers to produce high-quality products.

The ICCO has also highlighted that global cocoa production is facing long-term challenges due to climate change, which affects the yield and quality of cocoa beans. Unpredictable weather patterns, such as excessive rainfall or droughts, have disrupted the cocoa supply, leading to further price volatility. As a result, manufacturers of premium chocolate are under pressure to maintain product quality while dealing with higher raw material costs. This, in turn, leads to higher prices for consumers, which can limit the market’s growth, particularly in price-sensitive regions.

Additionally, the push for ethical sourcing and certifications like Fairtrade or Rainforest Alliance, while beneficial for sustainability, adds to the cost of production. According to Fairtrade International, while these certifications are critical for ensuring fair wages for farmers and promoting environmentally friendly farming practices, they come with an additional premium that can push prices higher.

Opportunity

Expansion of Sustainable and Ethical Chocolate Products

One of the key growth opportunities for the premium chocolate market lies in the growing consumer demand for sustainably sourced and ethically produced chocolate. As more consumers become environmentally and socially conscious, there is a rising preference for premium chocolate products that align with these values. Consumers are increasingly looking for brands that support fair trade practices, ensure the well-being of cocoa farmers, and use environmentally friendly production methods.

A 2023 study by Fairtrade International found that 60% of consumers globally are willing to pay more for chocolate that comes with ethical certifications, such as Fairtrade or Rainforest Alliance. This shift toward ethical consumption is driving growth in the premium chocolate market, especially among younger generations who are more attuned to sustainability issues. These consumers are not only concerned with the quality of the chocolate but also the impact their purchase has on the environment and society.

Furthermore, government initiatives aimed at supporting sustainable agriculture and fair trade practices are helping to boost this trend. For example, in countries like the United States and the UK, there are increasing efforts to promote ethical sourcing within the food and beverage industry. Governments are encouraging chocolate manufacturers to trace their supply chains and adopt more transparent practices. These initiatives are creating a supportive environment for the growth of sustainable premium chocolate products.

According to The World Cocoa Foundation, the demand for sustainably sourced cocoa is expected to grow by 10% annually over the next five years, highlighting a significant opportunity for premium chocolate brands to capitalize on this trend. By embracing ethical sourcing and investing in sustainability initiatives, companies can not only meet consumer demand but also position themselves as leaders in the future of the chocolate industry.

Trends

Rise of Plant-Based and Vegan Premium Chocolate

A major trend currently shaping the premium chocolate market is the increasing demand for plant-based and vegan chocolate products. With growing awareness around health, environmental sustainability, and animal welfare, consumers are opting for chocolates that are free from animal-derived ingredients. This shift is especially prominent among millennials and Gen Z consumers, who are more likely to choose plant-based or vegan products as part of a broader lifestyle choice.

In 2023, the global market for plant-based chocolates grew by 10%, according to The Good Food Institute, a leading nonprofit organization focused on promoting plant-based foods. Vegan and dairy-free chocolates are now seen as more than just niche offerings—they’re becoming a mainstream choice for consumers seeking healthier and more ethical alternatives to traditional chocolate.

Governments and organizations are also playing a role in this trend by encouraging more sustainable food production practices. For example, the UK’s Department for Environment, Food & Rural Affairs (DEFRA) has supported initiatives that promote plant-based food production and consumption, citing benefits for both personal health and the environment. These initiatives are creating an environment where plant-based premium chocolate brands can thrive.

Regional Analysis

The premium chocolate market in Europe remains the dominant region, accounting for 47.3% of the global market share, with a valuation of approximately USD 17.5 billion. This substantial market share can be attributed to the high demand for premium and artisanal chocolate products among European consumers, who are increasingly seeking high-quality ingredients, unique flavors, and luxury experiences.

Europe is home to some of the world’s leading chocolatiers, with countries like Belgium, Switzerland, and France renowned for their long-standing chocolate-making traditions. Additionally, the growing trend of health-conscious consumption has fueled the demand for premium chocolates with higher cocoa content, organic certifications, and minimal added sugars, further driving market growth.

The rising popularity of premium chocolates in Europe is also supported by consumer preferences for single-origin cocoa products, which offer distinctive flavors linked to specific regions. Countries such as Belgium and Switzerland have capitalized on this trend, emphasizing their expertise in crafting chocolates from high-quality cocoa beans sourced from regions like Latin America and Africa. Moreover, the increasing interest in artisanal and handcrafted products has led to a rise in boutique chocolate brands, further boosting market dynamics in the region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Barry Callebaut is a leading global supplier of premium chocolate and cocoa products, serving manufacturers, artisans, and foodservice businesses. With operations in over 30 countries, the company offers a wide range of high-quality chocolate, cocoa powder, and ingredients. Barry Callebaut emphasizes sustainable sourcing through its Cocoa Horizons program, which aims to improve the lives of cocoa farmers while promoting environmental stewardship. It holds a dominant position in the premium chocolate industry, driven by innovation and sustainability initiatives.

Cargill is a major player in the premium chocolate market, offering high-quality chocolate, cocoa, and related ingredients to food manufacturers. The company focuses on sustainable sourcing and is involved in the Cargill Cocoa Promise initiative, aimed at improving cocoa farming communities. With a strong presence in both the North American and European markets, Cargill has continued to expand its product portfolio, including organic and fair-trade-certified chocolate, meeting the growing demand for premium and ethical chocolate options globally.

Cemoi Chocolatier SA, based in France, is one of the largest independent chocolate manufacturers in Europe. Specializing in premium chocolate products, Cemoi serves both the retail and industrial sectors. The company offers a broad array of products, including chocolate bars, pralines, and gourmet chocolates, and focuses on high-quality raw materials sourced from sustainable cocoa farms. Cemoi’s commitment to quality and innovation has helped it build a loyal customer base across Europe and beyond.

Top Key Players

- Barry Callebaut

- Cargill Incorporated

- Cemoi Chocolatier SA

- CEMOI Group

- Chocoladefabriken Lindt & Sprüngli AG

- Chocolat Frey AG

- Choetta AB

- Endangered Species Chocolate

- Ferrero International S.A.

- Govida

- Lake Champlain Chocolate Co.

- Mars, Inc.

- Mondelez International Inc.

- Nestle SA

- Pierre Marcolini Group.

- Rococo Chocolates

- The Hershey Company

- Yildiz Holding Inc.

Recent Developments

In 2024 Barry Callebaut, the company reported significant growth, maintaining a dominant market share of over 25% in the global chocolate and cocoa industry. Barry Callebaut’s focus on innovation and sustainability has positioned it as a top choice for premium chocolate products.

In 2024 Cargill Incorporated, the company reported annual revenues of around $165 billion across all sectors, with its food ingredient division, including premium chocolate, contributing a sizable portion to this total.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 37.0 Bn |

| Forecast Revenue (2034) | USD 69.5 Bn |

| CAGR (2025-2034) | 6.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Dark Chocolate, Milk Chocolate, White Chocolate), By Packaging Type (Standard Packaging, Gift Packaging), By Type (Chocolate Bars, Boxed Chocolates, Assortments, Others), By Distribution Channel (Hypermarkets And Supermarkets, Specialty Stores, Grocery Stores, Convenience Stores, Online, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Barry Callebaut, Cargill Incorporated, Cemoi Chocolatier SA, CEMOI Group, Chocoladefabriken Lindt & Sprüngli AG, Chocolat Frey AG, Choetta AB, Endangered Species Chocolate, Ferrero International S.A., Govida, Lake Champlain Chocolate Co., Mars, Inc., Mondelez International Inc., Nestle SA, Pierre Marcolini Group., Rococo Chocolates, The Hershey Company, Yildiz Holding Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |