Quick Navigation

Report Overview

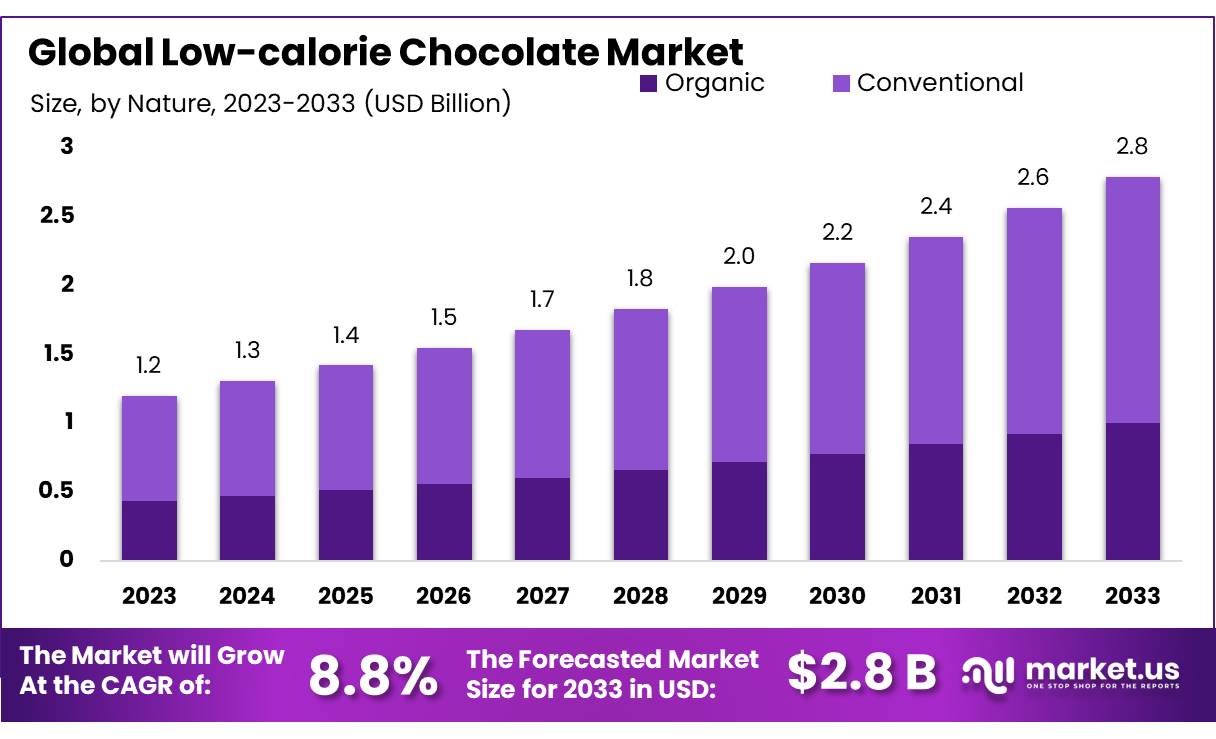

The Global Low-calorie Chocolate Market size is expected to be worth around USD 2.8 Bn by 2033, from USD 1.2 Bn in 2023, growing at a CAGR of 8.8% during the forecast period from 2024 to 2033.

Low-calorie chocolate refers to chocolate products formulated with fewer calories compared to traditional chocolates. These products are typically made using alternative sweeteners like stevia, erythritol, or other sugar substitutes, which maintain the sweetness of chocolate without adding significant calories.

Additionally, many low-calorie chocolates also have reduced fat content and may include high-fiber additives, which contribute to a more satisfying texture and a slower release of energy, helping to curb cravings.

The food and beverage industry plays a significant role in the growth of the low-calorie chocolate market. Major companies like Nestlé and Mars have introduced reduced-calorie versions of their popular chocolate products, catering to the increasing demand from health-conscious consumers.

In 2022, Nestlé’s “Better for You” category, which includes low-calorie and reduced-sugar products, grew by 6.4% globally, highlighting the positive consumer reception to healthier chocolate options.

From a global trade perspective, the import and export of low-calorie chocolate is expanding, particularly in developed markets such as North America, Europe, and parts of Asia-Pacific. Germany, for instance, exported around USD 700 million worth of chocolate products in 2022, with a growing share attributed to low-calorie variants. This indicates strong international demand for these healthier alternatives.

On the innovation front, major brands continue to invest heavily in developing low-calorie chocolate options. Brands like ChocZero, which raised over USD 15 million to expand its portfolio of sugar-free chocolates, and Lily’s Sweets, which saw a 23% increase in market share in 2022, are leading the way in offering low-calorie products. These innovations are driving the continued growth of the market.

The dark chocolate segment led the market in 2020, accounting for approximately 52.3% of the total market share due to its health benefits and popularity among health-conscious consumers. Meanwhile, the milk chocolate segment is expected to grow at the fastest rate, with a projected compound annual growth rate (CAGR) of 10.5% during the forecast period. This trend reflects a growing preference for healthier chocolate options across various consumer segments.

Key Takeaways

- Low-calorie Chocolate Market size is expected to be worth around USD 2.8 Bn by 2033, from USD 1.2 Bn in 2023, growing at a CAGR of 8.8%.

- Dark Chocolate held a dominant market position, capturing more than 53.3% of the overall low-calorie chocolate market.

- Bars held a dominant market position, capturing more than 45.7% share of the low-calorie chocolate market.

- Stevia held a dominant market position, capturing more than 46.1% share of the low-calorie chocolate market.

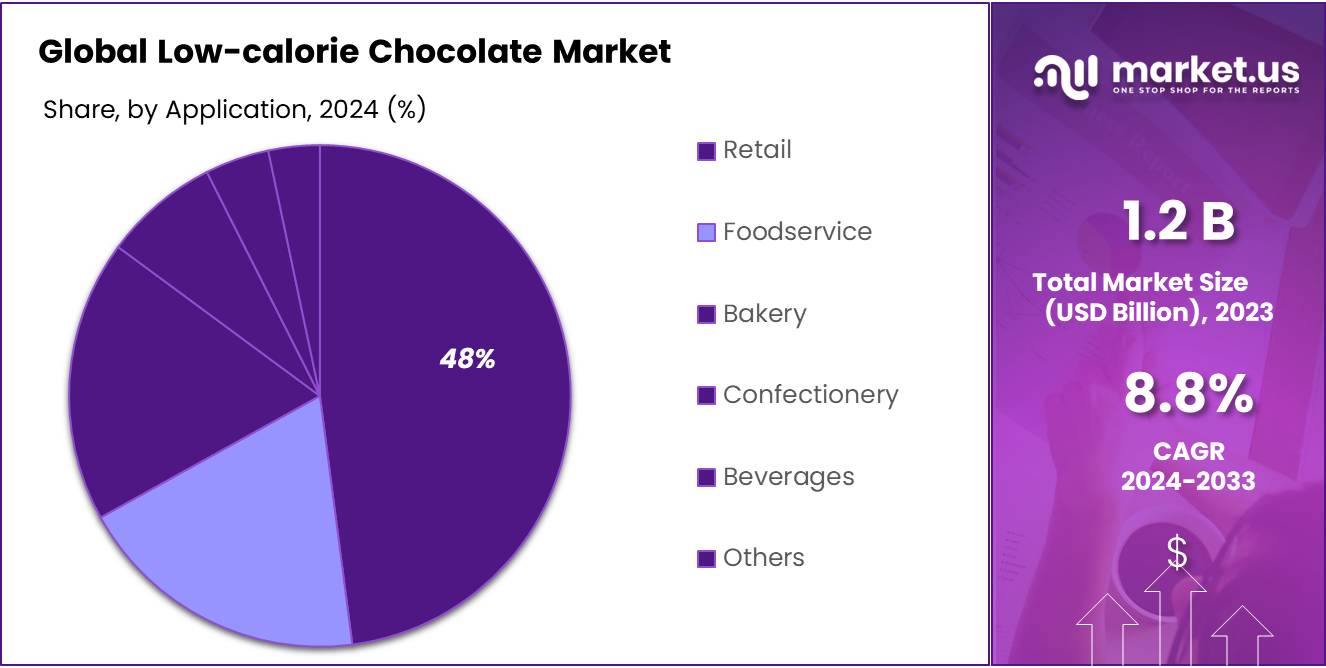

- Retail held a dominant market position, capturing more than 48.2% share of the low-calorie chocolate market.

- Supermarket/Hypermarket held a dominant market position, capturing more than a 39.1% share.

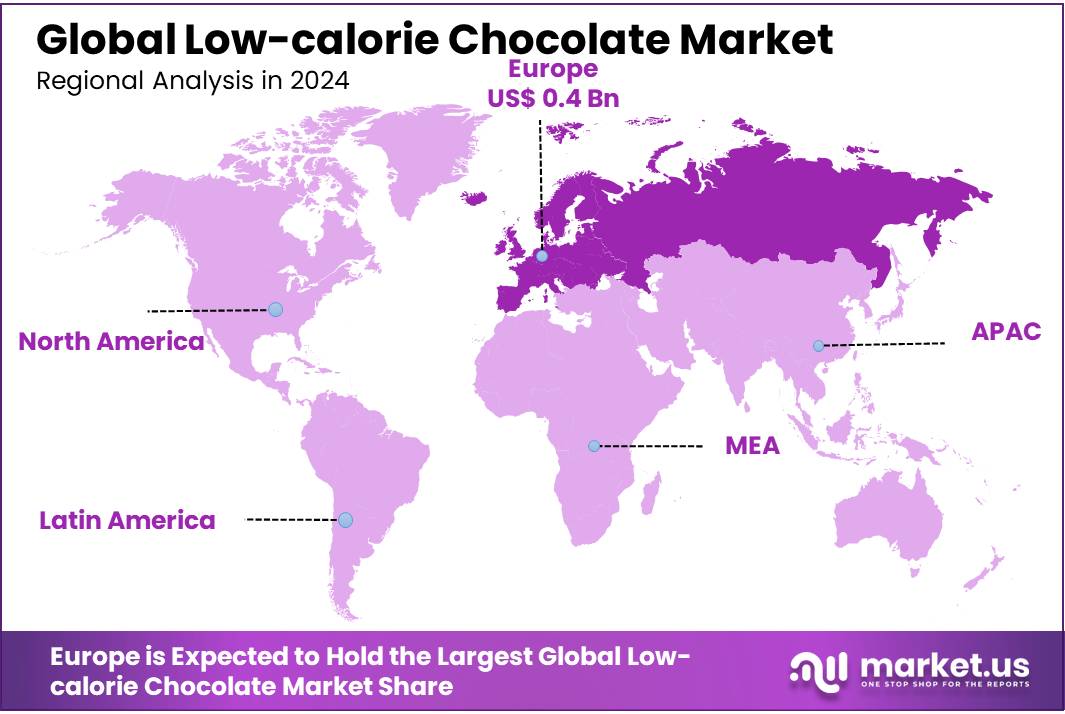

- Europe, the market is dominated by countries such as Germany, the UK, and France, with the region accounting for 34.6% of the global share, valued at approximately USD 0.4 billion in 2022.

By Product Type

Low-Calorie Chocolate Market by Product Type: Dark Chocolate, White Chocolate, Milk Chocolate

In 2023, Dark Chocolate held a dominant market position, capturing more than 53.3% of the overall low-calorie chocolate market. This segment benefits from growing consumer interest in the health benefits of dark chocolate, such as higher antioxidant content and lower sugar levels. Additionally, dark chocolate is often preferred by consumers seeking rich, intense flavors, making it the top choice in the low-calorie category.

White Chocolate, while holding a smaller market share, has shown notable growth. Its appeal lies in its creamy texture and sweeter taste, which attract consumers with a preference for milder, dessert-like options. Despite its popularity, white chocolate generally contains higher sugar levels compared to dark or milk varieties, which can limit its appeal to those focused on low-calorie options.

Milk Chocolate, traditionally one of the most popular types of chocolate globally, accounts for a significant portion of the low-calorie chocolate market. While it faces strong competition from dark chocolate, its milder flavor and broader consumer acceptance continue to make it a key segment. Milk chocolate’s ability to balance sweetness with the creamy texture has ensured its steady demand in the low-calorie segment.

By Product

Low-Calorie Chocolate Market by Product: Bars, Truffles, Bites, Spreads, Powders

In 2023, Bars held a dominant market position, capturing more than 45.7% share of the low-calorie chocolate market. The bar segment continues to lead due to its convenience, wide availability, and strong consumer preference for easy-to-consume, portion-controlled products. Bars are also the most commonly available format across major retailers, making them the go-to choice for many consumers seeking low-calorie indulgence.

Truffles, though a smaller segment, have gained popularity, particularly among consumers looking for a premium experience. These products offer a luxurious texture and rich flavor, appealing to those willing to spend more on indulgent but lower-calorie treats. Truffles are often marketed as a high-end product, enhancing their appeal to health-conscious consumers seeking a special treat without excess calories.

Bites, typically smaller and more portion-controlled than bars, have also seen increasing demand. These products are favored for their snackable format and convenience, especially for consumers with busy lifestyles. Bites offer a balanced solution for those looking to satisfy chocolate cravings in a more controlled, bite-sized portion.

Spreads, while a niche segment, are growing as consumers increasingly use low-calorie chocolate spreads in baking or as a topping. These products cater to consumers who want to incorporate low-calorie chocolate into various recipes or enjoy it as part of their daily meals without overindulgence.

Powders, another niche segment, are primarily used for making hot chocolate or adding to smoothies. While not as widely adopted as bars or bites, the powder segment is appealing to health-conscious consumers who prefer a customizable, low-calorie chocolate experience in beverages or other food products.

By Sweetener Type

Low-Calorie Chocolate Market by Sweetener Type: Stevia, Erythritol, Monk Fruit, Others

In 2023, Stevia held a dominant market position, capturing more than 46.1% share of the low-calorie chocolate market. Stevia’s widespread use can be attributed to its natural origin and its ability to provide a sweet taste without adding calories. This has made it the preferred sweetener for many low-calorie chocolate products. Additionally, Stevia is often marketed as a healthier alternative to artificial sweeteners, appealing to health-conscious consumers.

Erythritol, a sugar alcohol, is another key sweetener in the low-calorie chocolate market, accounting for a significant share. It is favored for its nearly zero-calorie content and its ability to mimic the taste and texture of sugar without the bitter aftertaste often associated with other low-calorie sweeteners. Erythritol also has a minimal impact on blood sugar levels, which has made it particularly popular in products targeted at diabetics and those following low-carb diets.

Monk Fruit, a natural sweetener derived from the monk fruit plant, is gaining traction in the market. While its market share is smaller compared to Stevia and Erythritol, its appeal lies in its intense sweetness, which is much stronger than sugar, allowing for smaller quantities to be used. Monk Fruit is also prized for being a natural, zero-calorie sweetener, making it attractive to health-conscious consumers looking for alternatives to both sugar and artificial sweeteners.

By Application

Low-Calorie Chocolate Market by Application: Retail, Foodservice, Bakery, Confectionery, Beverages, Others

In 2023, Retail held a dominant market position, capturing more than 48.2% share of the low-calorie chocolate market. Retail remains the largest application segment due to the widespread availability of low-calorie chocolate products in supermarkets, health food stores, and online platforms. Consumers prefer the convenience of purchasing ready-to-eat products in retail outlets, driving strong demand for low-calorie chocolate bars, bites, and other snack formats.

The Foodservice segment, though smaller than retail, is experiencing steady growth. Low-calorie chocolate is increasingly being incorporated into restaurant menus, cafes, and specialty food outlets. Many foodservice operators are adopting low-calorie chocolate as an ingredient in desserts, beverages, and other offerings to cater to the rising consumer demand for healthier options in dining establishments.

The Bakery segment also plays a significant role in the low-calorie chocolate market. Low-calorie chocolate is used in various bakery products, including cakes, cookies, and pastries. As health-conscious consumers seek to reduce calorie intake while enjoying baked goods, demand for low-calorie chocolate in this sector continues to rise, especially in premium and artisanal products.

The Confectionery segment is another key application for low-calorie chocolate. This includes chocolate-based candies and snack items that are marketed as healthier alternatives to traditional sweets. As consumers become more health-aware, the confectionery industry is increasingly adopting low-calorie ingredients to appeal to a broader audience, including those looking to reduce sugar intake.

The Beverages segment has seen a rise in low-calorie chocolate products, particularly in hot chocolate mixes, smoothies, and protein shakes. Low-calorie chocolate syrups and powders are popular in the health and wellness sector, where consumers are looking for indulgent yet healthier beverage options.

By Sales Channel

Low-Calorie Chocolate Market by Sales Channel: Supermarket/Hypermarket, Convenience Stores, Specialty Stores, Online Sales Channel, Others

In 2023, Supermarket/Hypermarket held a dominant market position, capturing more than a 39.1% share of the low-calorie chocolate market. Supermarkets and hypermarkets continue to be the leading sales channels due to their wide reach, large customer base, and extensive product offerings. Consumers prefer shopping at these locations for convenience, variety, and the ability to compare different low-calorie chocolate brands. The availability of low-calorie chocolates in mainstream grocery stores makes them easily accessible to a broad audience.

Convenience stores, while smaller in market share, play an important role in reaching consumers who prioritize quick, on-the-go purchases. These stores typically offer a limited selection of low-calorie chocolate products, often focusing on snack-sized options. The demand for such products is driven by busy lifestyles, with consumers seeking healthier, portion-controlled alternatives for immediate consumption. Convenience stores are a key channel for impulse buys and cater to consumers who need quick access to low-calorie treats.

Specialty Stores represent a growing but niche segment in the low-calorie chocolate market. These stores, which focus on health foods, organic products, or dietary-specific items, attract consumers looking for premium or specialty low-calorie chocolates. Specialty stores often stock unique, high-quality products that may not be available in larger retail outlets. This channel appeals to health-conscious individuals, those following specific diets (such as vegan or gluten-free), or consumers looking for unique or artisanal chocolate options.

The Online Sales Channel has seen significant growth in recent years, driven by the increasing shift towards e-commerce. Consumers increasingly purchase low-calorie chocolates through online platforms such as brand websites, marketplaces, and health food e-stores.

Key Market Segments

By Product Type

- Dark Chocolate

- White Chocolate

- Milk Chocolate

By Product

- Bars

- Truffles

- Bites

- Spreads

- Powders

By Sweetener Type

- Stevia

- Erythritol

- Monk Fruit

- Others

By Application

- Retail

- Foodservice

- Bakery

- Confectionery

- Beverages

- Others

By Sales Channel

- Supermarket/Hypermarket

- Convenience stores

- Specialty Stores

- Online sales channel

- Others

Drivers

Rising Obesity and Health Concerns

The rising rates of obesity and related health issues, such as diabetes and heart disease, are significant contributors to the increasing demand for low-calorie chocolate. According to the World Health Organization (WHO), global obesity rates have nearly tripled since 1975, with 39% of adults worldwide being overweight and 13% classified as obese as of 2020. This has driven consumers to actively seek healthier alternatives to sugary snacks, including chocolate products.

Growing Focus on Nutritional Labels and Clean Label Trends

As consumers become more health-conscious, they are paying closer attention to product labels, particularly the nutritional content. The clean label trend, which refers to the desire for food products with simple, recognizable ingredients, has gained momentum in the food industry.

According to the Clean Label Project, 67% of consumers actively seek out products with natural or simple ingredients, and 55% of consumers report avoiding products that contain artificial ingredients or excessive added sugars.

Supportive Government Initiatives and Public Health Campaigns

Governments around the world are playing a crucial role in shaping consumer behavior and promoting healthier food choices.

Public health campaigns, such as the “Healthy Eating” initiatives in the U.S., the “National Health Service’s Change4Life” campaign in the UK, and the “Eatwell Guide” in Australia, are all focused on educating consumers about the importance of balanced diets and the risks of excessive sugar consumption. These initiatives have contributed to growing awareness about the negative health impacts of sugary foods, including chocolate, and have led to an increase in demand for low-calorie alternatives.

Restraints

Cost of Alternative Sweeteners

The use of alternative sweeteners is one of the main factors driving up the production costs of low-calorie chocolate. While traditional chocolate is made with sugar, low-calorie chocolate requires sweeteners such as stevia, erythritol, or monk fruit, which are significantly more expensive than sugar.

According to data from the Food and Agriculture Organization (FAO), the price of stevia, for example, is around 20-30% higher per kilogram than conventional sugar. Monk fruit, another common alternative sweetener, is even more expensive, with prices being up to 10 times higher than sugar per kilogram.

These higher ingredient costs directly impact the overall production costs of low-calorie chocolate products. Additionally, many sweeteners used in these chocolates are sourced from specialty suppliers or require additional processing, further contributing to the overall cost.

Premium Ingredient Costs and Clean Label Demands

Another significant contributor to the high production costs of low-calorie chocolate is the growing consumer demand for premium, clean-label ingredients. Consumers are increasingly seeking products that contain natural, organic, or sustainably sourced ingredients, leading manufacturers to use higher-quality raw materials.

According to the Clean Label Project, 67% of consumers prefer foods with simple, recognizable ingredients, and 55% actively avoid products with artificial ingredients or excessive added sugars. While this trend is beneficial for health-conscious consumers, it raises the cost of sourcing and producing low-calorie chocolates.

Impact on Market Accessibility

Due to the high production costs, many low-calorie chocolate products are positioned in the premium market segment, often out of reach for the average consumer. According to data from the U.S. Bureau of Labor Statistics, the average price of premium chocolate in the U.S. was approximately $4.50 per 100 grams in 2022, while conventional chocolate products could be found for as low as $1.50 per 100 grams.

This price difference can make low-calorie chocolate an unattractive option for price-sensitive consumers, especially in emerging markets or lower-income demographics. The high price point can limit the growth potential of low-calorie chocolates in these regions, restraining the overall market growth.

Opportunity

Growing Global Health and Wellness Trend

The global health and wellness market has experienced significant growth in recent years, reflecting consumers’ increasing focus on healthier lifestyles and improved eating habits.

According to the World Health Organization (WHO), the global prevalence of obesity has more than tripled since 1975, with 39% of adults classified as overweight and 13% as obese in 2020. This alarming trend has prompted consumers to shift towards healthier snack options, including low-calorie chocolate, to manage their calorie intake while still satisfying their sweet cravings.

A report by the Global Wellness Institute reveals that the global wellness economy was valued at $4.5 trillion in 2020, with the health and nutrition sector accounting for a significant portion of this value.

Expansion of Clean-Label and Natural Products

The demand for clean-label products, which are perceived as healthier and more transparent, is another key growth opportunity for the low-calorie chocolate market. Consumers are increasingly seeking snacks with simple, natural ingredients, and are actively avoiding products that contain artificial additives or excessive added sugars. According to the Clean Label Project, 67% of consumers look for products with recognizable, clean ingredients, and 55% actively avoid foods with artificial ingredients.

According to the U.S. Department of Agriculture (USDA), organic food sales in the U.S. reached $56.4 billion in 2020, with organic chocolate being one of the fastest-growing categories in the broader organic food market.

Increasing Demand for Special Diet Products

The increasing popularity of specialized diets such as vegan, gluten-free, and keto is creating a significant growth opportunity for the low-calorie chocolate market. According to the Vegan Society, the number of vegans in the U.S. grew by 300% between 2004 and 2019, and it is estimated that around 3% of the global population follows a vegan diet. This shift towards plant-based eating has led to increased demand for vegan-friendly low-calorie chocolates, which do not contain dairy or animal-derived ingredients.

Trends

Surge in Vegan and Plant-Based Diets

The global shift towards veganism and plant-based diets is one of the primary drivers of the growing popularity of vegan low-calorie chocolates. The Vegan Society reports that the number of people following a vegan diet in the U.S. has increased by 300% from 2004 to 2019.

In fact, the U.S. market for plant-based foods reached $7 billion in 2020 and is projected to grow at a compound annual growth rate (CAGR) of 11.9% from 2021 to 2027. As more consumers adopt plant-based lifestyles, the demand for vegan chocolate products has surged, and this demand is extending into the low-calorie chocolate segment.

Rising Environmental Awareness and Ethical Sourcing

In addition to health motivations, growing environmental awareness is another key factor driving the trend toward vegan and plant-based low-calorie chocolates. According to a 2021 report by the United Nations, the food industry accounts for approximately 25% of global greenhouse gas emissions, with animal-based products being a major contributor.

This has led many consumers to make more sustainable food choices, including opting for plant-based and vegan options. In the chocolate industry, this trend is evident as consumers increasingly prefer products that align with their environmental values.

Innovation in Plant-Based Ingredients for Better Taste and Texture

As demand for vegan and plant-based chocolates grows, manufacturers are also focusing on improving the taste and texture of these products. Traditional chocolate relies on milk to provide creaminess and texture, but plant-based alternatives need to replicate these qualities using non-dairy ingredients.

To meet consumer expectations, manufacturers are increasingly turning to innovations in plant-based ingredients that provide a similar taste and mouthfeel to dairy-based chocolate while maintaining low-calorie profiles.

Regional Analysis

In Europe, the market is dominated by countries such as Germany, the UK, and France, with the region accounting for 34.6% of the global share, valued at approximately USD 0.4 billion in 2022. This growth can be attributed to increasing health consciousness and the rising demand for healthier food alternatives. Regulatory support for lower-sugar products and innovations from key players like Nestlé and Lindt have also contributed to this expansion.

North America, particularly the United States, holds a significant portion of the market, driven by the growing trend of health and wellness products. The U.S. accounts for nearly 30% of the global low-calorie chocolate consumption, with demand for sugar-free and reduced-calorie options rising among health-conscious consumers. Companies such as Hershey’s and ChocZero are investing heavily in low-calorie chocolate innovation, propelling the market forward.

In Asia Pacific, the market is witnessing rapid growth, particularly in countries like Japan, China, and India, as health awareness increases and urban populations seek healthier food options. Although the market share is still smaller compared to North America and Europe, the region is expected to grow at the highest compound annual growth rate (CAGR) of 9.8% over the forecast period.

The Middle East & Africa and Latin America markets are relatively nascent but show potential for growth as consumer awareness of health and wellness products increases. The low-calorie chocolate segment is expected to expand steadily in these regions, driven by changing dietary habits and increasing disposable income.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Low-Calorie Chocolate Market is highly competitive, with several leading global players driving innovation and expansion. Barry Callebaut AG, a major supplier of chocolate and cocoa products, is at the forefront, offering a range of low-calorie and sugar-reduced chocolate products aimed at health-conscious consumers.

Similarly, Nestlé S.A. has capitalized on the growing demand for healthier alternatives, with their “Better for You” category, which includes low-calorie chocolate options like their sugar-free chocolate bars. Another major player, Lindt & Sprüngli, continues to innovate in the premium chocolate sector with low-calorie options, maintaining a strong foothold in the European market.

The Hershey Company and Kraft Heinz are key players in North America, with Hershey focusing on expanding its low-calorie chocolate portfolio through brands like Reese’s and Kisses, while Kraft Heinz has developed health-focused chocolate products to cater to a broader market.

In the premium segment, brands such as Raaka and Lang’s Chocolates are gaining traction by offering artisanal low-calorie chocolates made with high-quality ingredients. Ben & Jerry’s and Haagen Dazs, known for their indulgent frozen desserts, have also ventured into the low-calorie chocolate market by launching healthier alternatives to their classic chocolate ice cream offerings.

Emerging brands such as Swee10, Sweegen Delights, and Chocolette Confectionary LLC are tapping into the growing demand for low-calorie and sugar-free products, particularly in North America and Europe. These companies are leveraging new ingredients like stevia, erythritol, and other natural sweeteners to create innovative low-calorie chocolate products. Toblerone and Twix, two iconic brands owned by Mars, have also introduced reduced-calorie versions to cater to the increasing consumer demand for healthier snack options, further intensifying competition in the market.

Top Key Players in the Market

- Barry Callebaut AG

- BARRY CALLEBAUT AG

- Ben & Jerry’s

- Blommer Chocolate Company

- Chocolette Confectionary LLC

- GATSBY Chocolate

- Haagen Daaz

- Kraft Heniz Company

- Langs Chocolates

- Lindt & Sprungli

- Nestlé S.A

- Raaka

- Swee10

- Sweegen Delights

- The Hershey Company

- Toblerone

- Twix

Recent Developments

In 2023 Barry Callebaut AG, a leading player in the global chocolate and cocoa sector, has made significant strides in the low-calorie chocolate market through its innovation and focus on healthier alternatives.

In 2023, Barry Callebaut reported a 5.4% growth in its chocolate segment, largely attributed to innovations in healthier products.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.2 Bn |

| Forecast Revenue (2033) | USD 2.8 Bn |

| CAGR (2024-2033) | 8.8% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Dark Chocolate, White Chocolate, Milk Chocolate), By Product (Bars, Truffles, Bites, Spreads, Powders), By Sweetener Type (Stevia, Erythritol, Monk Fruit, Others), By Application (Retail, Foodservice, Bakery, Confectionery, Beverages, Others), By Sales Channel ( Supermarket/Hypermarket, Convenience stores, Specialty Stores, Online sales channel, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Barry Callebaut AG, BARRY CALLEBAUT AG, Ben & Jerry’s, Blommer Chocolate Company, Chocolette Confectionary LLC, GATSBY Chocolate, Haagen Daaz, Kraft Heniz Company, Langs Chocolates, Lindt & Sprungli, Nestlé S.A, Raaka, Swee10, Sweegen Delights, The Hershey Company, Toblerone, Twix |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |