Quick Navigation

Report Overview

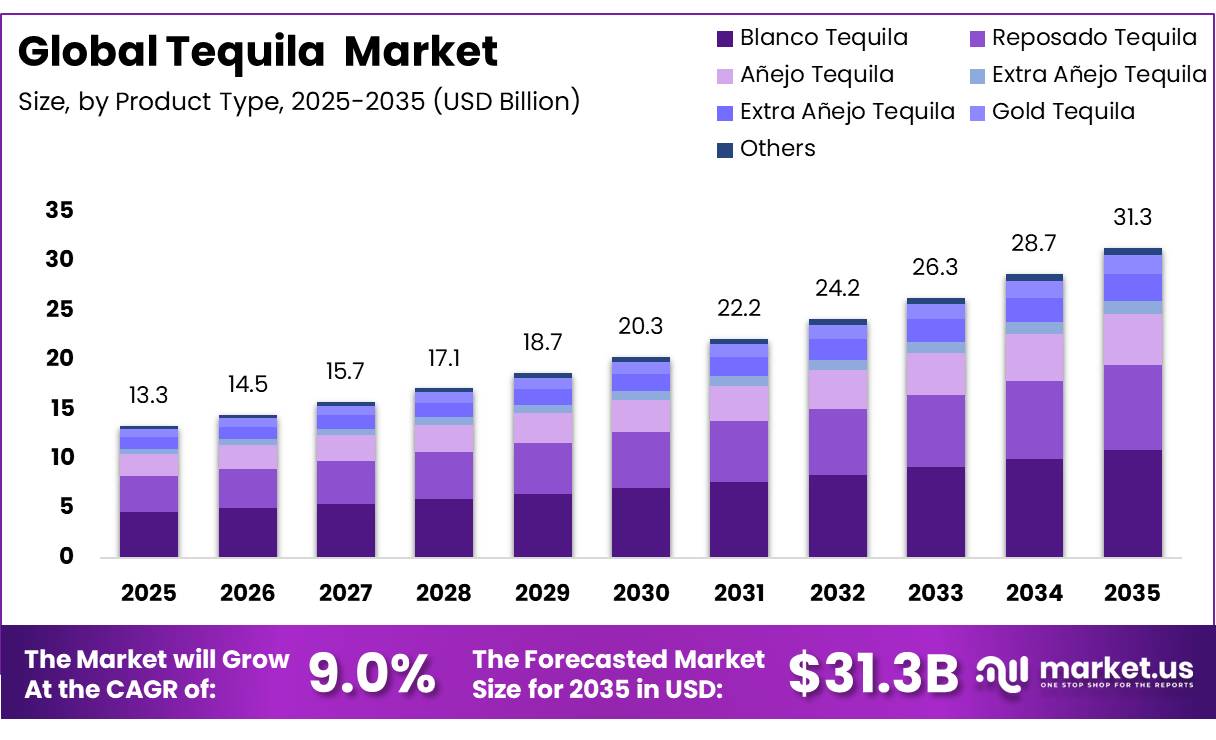

In 2025, the Global Tequila Market was valued at USD 13.3 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 9.0%, reaching about USD 31.3 billion by 2035. In 2025, North America led the market, achieving over 48.6% share with a revenue of USD 6.46 Billion.

Tequila is a protected Mexican distilled spirit produced mainly from blue agave grown within officially authorized regions. The industry combines agriculture, distillation, maturation, bottling, certification, logistics, hospitality, and international trade. Its strong identity is supported by origin protection, strict production standards, and a close connection with Mexican culture. These factors have helped tequila develop from a traditional regional drink into a globally recognized premium spirits category.

- Jalisco’s strong export economy continues to support the growth of the tequila market, as the state remains the primary production hub for tequila. According to official trade data, Jalisco recorded approximately USD 13.84 billion in total exports during the third quarter of 2025, representing a year-over-year increase of 89.1%.

Key Takeaways

- The global tequila market was valued at USD 13.3 billion in 2025.

- The global market is projected to grow at a CAGR of 9.0% and is estimated to reach USD 31.3 billion by 2035.

- Blanco tequila is the dominant product type, accounting for 34.8%, driven by cocktail usage and younger consumer preference.

- 100% agave tequila leads purity demand at 68.5%, indicating a clear consumer shift toward authentic products.

- Premium Price Range tequila dominates value positioning with a 42.7% share, reflecting strong premiumization trends.

- Unflavored flavor type dominates the market with a 72.4% market share, reflecting strong consumer preference for traditional tequila profiles and minimal adoption of flavored variants.

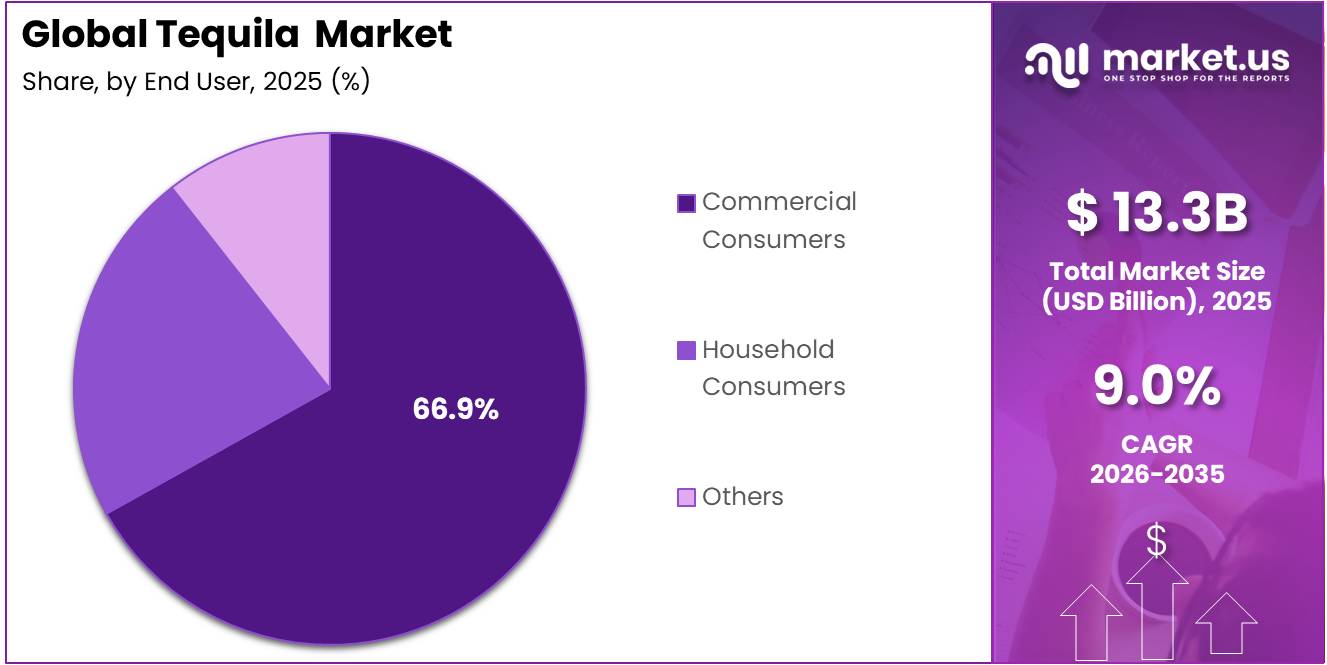

- Based on End User the Commercial consumers dominate the market with 66.9%, led by hospitality outlets such as bars and restaurants.

- Off-trade channels dominate distribution channels at 57.3%, supported by supermarkets, liquor stores, and rising online retail.

- North America is the leading region with 48.6% share, confirming its role as the primary demand center.

The industrial structure is built around agave growers, distillers, brand owners, bottlers, distributors, and certification bodies. Production remains concentrated in Mexico, where authorized manufacturers follow established rules covering raw materials, fermentation, distillation, aging, labelling, and traceability. This regulated framework protects product authenticity and supports consumer confidence across domestic and export markets. At the same time, the long cultivation cycle of agave creates planning challenges because planting decisions must be made years before the spirit reaches the market.

Producers are increasingly exploring water reuse, cleaner energy, waste recovery, and better use of agave fibre. Stronger trademark protection and origin enforcement in overseas markets will also support long-term brand value. The tequila industry is therefore likely to remain an attractive global spirits segment, supported by authenticity, premium positioning, product innovation, and expanding consumer interest.

Tequila Market Segmentation

Product Type Analysis

Blanco Tequila represents dominant Segment in the Market.

In 2025, Blanco Tequila held a dominant market position, capturing more than a 34.8% share of the global tequila market. Its leadership is supported by growing consumer preference for fresh, unaged tequila that delivers the natural flavor of 100% blue agave. Blanco tequila is widely used in premium cocktails such as Margaritas and Palomas, making it the preferred choice across bars, restaurants, and retail channels. The segment also benefits from the expansion of premium tequila brands focused on clean-label and additive-free products. These trends continue to support strong demand for Blanco tequila in both domestic and international markets.

Reposado Tequila is the fastest-growing segment in the global tequila market because it offers a balance between the fresh character of Blanco tequila and the richer flavors developed during barrel aging. This makes it attractive to consumers looking for premium sipping tequila as well as high-end cocktails. The rising popularity of premium and super-premium spirits is further supporting demand for this category.

- According to the Consejo Regulador del Tequila (CRT), tequila exports reached more than 400 million liters in 2025, highlighting strong international demand for premium tequila styles, including Reposado. Growing premiumization across North America, Europe, and Asia is expected to keep Reposado as one of the fastest-expanding product categories.

Purity Type Analysis

100% Agave Tequila leads the market.

100% Agave Tequila account for 68.5% of the tequila market, driven by a strong shift in consumer preference toward higher-quality, authentic spirits. Consumers are increasingly moving away from mixto variants in favor of pure agave tequila, which is seen as cleaner, smoother, and more premium. This preference is also supported by strict production standards under NOM regulations, which help ensure consistency and product trust. Rising income levels in key markets have further encouraged buyers to upgrade to 100% agave options rather than lower-cost alternatives.

Mixto Tequila production is becoming a major trend, with the goal of reaching big sales targets between 2030 and 2035. For example, brands that use biodynamic farming and waste-free extraction techniques are gaining popularity in areas where customers care about the environment. This growth is being driven by tighter environmental regulations and an increasing number of consumers who want to support sustainable supply chains. However, the main challenges come from the high cost of getting organic agave fields certified and handling waste materials like agave bagasse.

Price Range Analysis

Premium price tequila dominates the tequila market.

In 2025, Premium held a dominant market position, capturing more than a 42.7% share of the global tequila market. The segment maintained its leadership as consumers continued to shift toward high-quality tequila made from 100% Blue Weber agave, driven by growing interest in authentic production methods and aged expressions such as Reposado, Añejo, and Extra Añejo. Premium tequila also benefited from rising demand in bars, restaurants, specialty liquor stores, and online retail channels.

- From January to April 2025, Mexico produced 9 million liters of tequila and exported 138.5 million liters, reflecting strong global demand for authentic tequila. The steady export volume highlights the growing preference for premium tequila, particularly products made from 100% Blue Weber agave, across major international markets.

Mid-Range is the fastest-growing segment in the tequila market as consumers increasingly seek products that offer good quality at an affordable price. In 2025, demand for mid-range tequila grew across both retail stores and hospitality venues, supported by rising interest in premium cocktails and casual social drinking. This price category appeals to a broad consumer base by offering 100% agave and quality blended tequilas at accessible prices, making it suitable for both everyday consumption and special occasions.

Flavor Type Analysis

Unflavored Tequila Are the Most Widely Used Tequila.

Unflavored tequila type dominated the market and accounting for 72.4%. This dominance is due to strong consumer preference for authentic agave-forward taste profiles. It is widely seen as the most traditional form of tequila, where the natural flavor of blue agave is preserved without additives. Consumers prefer it for its consistency, purity, and versatility in both sipping and cocktail applications. Classic cocktails and bartender preferences further reinforce its leadership, as most drinks are built on a clean, unflavored base.

Flavored tequila type is expected to grow the fastest between 2026 and 2035, with a big increase in its value by 2035. This category is growing quickly from a small starting point, thanks to new and creative flavors that are drawing in different groups of people. The growth is because more people like spicy, fruity, and herbal tastes, such as jalapeño and coconut flavors, which are popular with younger consumers. However, one challenge is that some traditional consumers are not happy with these flavored options, as they think they take away from the original character of tequila.

End Use Analysis

Tequila Are Mostly Utilized in the Commercial Consumers Sector.

The commercial consumers segment, accounting for 66.9% of the tequila market, is the dominant end-use category, supported by strong demand from hospitality, nightlife, and travel-driven consumption. Bars, restaurants, hotels, and resorts are the main buyers, placing regular bulk orders to serve high daily turnover. This makes tequila a core part of cocktail menus across lounges, resorts, and airport venues where consumption is frequent and experience-led. Growth in dining out and global travel continues to support this segment, although it remains sensitive to tourism slowdowns and rising operational costs.

- According to the National Restaurant Association, the U.S. restaurant industry was projected to reach USD 1.5 trillion in sales in 2025, reflecting continued growth in foodservice spending that supports demand for alcoholic beverages, including tequila

Household consumers are a growing trend that’s expected to take a bigger share of the market between 2030 and 2035. During 2025, more consumers purchased tequila for home celebrations, casual gatherings, and cocktail preparation, supported by the expansion of online alcohol retailing and wider availability in supermarkets and liquor stores. Growing interest in mixology, premium sipping tequila, and ready-to-serve cocktail experiences has encouraged household purchases across many countries.

Distribution Channel Analysis

Off-Trade Held a Major Share of the Tequila Market.

Off-Trade distribution channel, accounting for 57.3% of the market, is driven by supermarkets, hypermarkets, and liquor stores that make tequila easily accessible to everyday shoppers at competitive prices. This channel benefits from wide shelf presence, promotions, and the convenience of purchasing alongside regular groceries, creating steady and repeat sales. However, rising retail costs and changing shopping habits are putting pressure on traditional store-based sales.

- According to the Distilled Spirits Council of the United States, U.S. spirits supplier sales reached USD 4 billion in 2025, representing a 2.2% decline from 2024. However, supplier volume increased by 1.9% to 318.1 million nine-litre cases. Spirits retained the largest share of U.S. beverage-alcohol supplier revenue for the fourth consecutive year, accounting for 42.4% in 2025.

On-Trade is the fastest-growing segment in the tequila market, driven by the increasing number of consumers choosing premium spirits in bars, restaurants, hotels, and entertainment venues. During 2025, the recovery of the hospitality and tourism sectors continued to increase tequila consumption through cocktails, tequila tastings, and premium dining experiences. Consumers showed greater interest in sipping tequila and craft cocktails, encouraging restaurants and bars to expand their premium tequila offerings.

Key Market Segments

By Product Type

- Blanco Tequila

- Reposado Tequila

- Añejo Tequila

- Extra Añejo Tequila

- Cristalino Tequila

- Gold Tequila

- Others

By Purity Type

- 100% Agave Tequila

- Mixto Tequila

By Price Range

- Economy

- Mid-Range

- Premium

By Flavor Type

- Unflavored

- Flavored

By End User

- Household Consumers

- Commercial Consumers

- Others

By Distribution Channel

- On-Trade

- Off-Trade

Driver Analysis

USMCA Trade Architecture & Tariff Immunity

The 2025–2026 US trade tariff environment represents an acute structural advantage for Mexican tequila producers relative to competing imported spirits, and its CAGR impact derives precisely from competitive displacement rather than organic category growth alone. President Trump’s Executive Orders 14193 and 14194 imposed a blanket 25% tariff on non-USMCA-compliant Mexican goods, but a critical carve-outaffirmed in the White House Fact Sheet of March 7, 2025 exempted USMCA-qualifying goods, including most tequila, from the additional duties. As of 2026, Mexico accounts for approximately 47.3% of all US spirits imports by value, with USMCA-compliant tequila entering duty-free while competing EU-origin spirits now carry a 15% tariff under the August 2025 EU–US framework, and non-USMCA origins face a ~10% Section 122 baseline.

US tequila imports in 2024 were valued at approximately $5.2 billion and represented 70.7 million proof gallons a 5% year-on-year increase and January 2025 exports from Mexico jumped 29.3% year-on-year, confirming that the USMCA shelter was operationalized by producers pre-emptively front-loading inventory. The compliance infrastructure requirement under NOM-006 including CRT Certificates of Authenticity, TTB Federal Basic Importer Permits, and FDA Prior Notice filings effectively raises the barrier to entry for non-Mexican agave spirit imitation products, further reinforcing the category’s structural moat within the US market and contributing an estimated incremental +1.5 percentage points to the medium-term CAGR trajectory.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization & 100% Agave Consumer Shift | +2.2% | North America core (US dominant), EU leading corridor (Germany, Spain, UK), Australia spillover | Short–Medium term (1–4 years) |

| USMCA Trade Architecture & Tariff Immunity | +1.5% | US–Mexico bilateral corridor; indirect benefit across Canada, emerging EU diversion | Short term (≤ 2 years) |

| Global Geographic Diversification Beyond US | +1.8% | EU (Germany, Spain, France, UK); APAC (Japan, China, Australia); South America (Colombia) spill-over | Medium–Long term (2–6 years) |

| Agave Supply Normalization & Input Cost Deflation | +1.2% | Mexico supply base (Jalisco, Tamaulipas, Michoacán, Nayarit, Guanajuato); benefits pass through to export-oriented North America, EU | Short–Medium term (1–3 years) |

| Cocktail Culture Expansion & RTD Tequila-Based Formats | +1.6% | North America (core US, Mexico), EU on-trade corridors, APAC emerging | Medium term (2–4 years) |

| Denomination of Origin (DOT) Regulatory Expansion & IP Enforcement | +0.8% | Emerging APAC, Middle East (UAE), Africa (OAPI bloc), South America expansion corridors | Long term (≥ 4 years) |

Restraint Analysis

TTB Alcohol Facts & Allergen Labeling Compliance Burden

The U.S. Alcohol and Tobacco Tax and Trade Bureau (TTB) published two landmark Notices of Proposed Rulemaking on January 17, 2025 Notice No. 237, requiring mandatory “Alcohol Facts” label panels on all distilled spirits, and Notice No. 238, requiring major food allergen declarations across wines, distilled spirits, and malt beverages regulated under the Federal Alcohol Administration Act.

The compliance burden translates directly to operational costs: each COLA re-submission carries TTB administrative timelines of 30–90+ days; reformulating or auditing production lines for allergen traceability requires plant-level certification changes; and smaller artisanal producers many of which rely on shared-use CRT-certified distillery infrastructure under linking agreements will face disproportionate cost-per-SKU impacts compared to large multinational portfolio holders.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Agave Oversupply & Structural Price Collapse | -2.0% | Jalisco (MX); global supply chain | Medium term (2–4 years) |

| U.S. Tariff Volatility & USMCA Review Uncertainty | -1.8% | North America core (US–MX corridor) | Short–Medium term (1–4 years) |

| Freshwater Scarcity in Denomination of Origin Zones | -1.5% | Jalisco, Guanajuato, Michoacán (MX) | Long term (≥ 4 years) |

| Demand Normalization & Consumer Spending Contraction | -1.7% | United States, EU, Canada | Short–Medium term (1–3 years) |

| Mexico’s New Mandatory Export Notice Regime (DOF 2025) | -1.0% | All MX export corridors, US–MX border | Short term (≤ 2 years) |

| TTB Alcohol Facts & Allergen Labeling Compliance Burden | -0.8% | United States, Canada | Medium term (2–5 years) |

Opportunity Analysis

Agave Surplus Monetization via Ultra-Premium Aging & Controlled-Scarcity Reserve Releases

The current agave oversupply crisis a surplus of approximately 500 million liters estimated by the CRT, with agave farmgate prices having crashed from $0.77/lb in 2021–2022 to $0.07–$0.20/lb by early 2025, and the number of registered agave producers having grown from 3,180 in 2014 to over 41,000 by 2023 is universally treated as a market headwind in baseline forecasts; strategically sophisticated operators, however, have the structural conditions to convert this supply glut into a long-dated, controlled-scarcity premium play that the market is not currently pricing.

US Census Bureau trade data shows that the unit value of Mexican tequila and mezcal imports has more than doubled, from roughly $9/liter in 2017 to almost $20/liter in 2024, confirming that consumers have already demonstrated consistent willingness to pay a premium for provenance and age credentials; the super-premium segment (>$250 per case) already represents 48% of U.S. tequila and mezcal revenue, with another 20% in the high-end premium tier.

A producer acquiring bulk tequila at current distressed input costs approximately $0.07–$0.20/lb for agave versus $0.77/lb at the cycle peaks and aging it for controlled release between 2029–2033 could achieve per-unit COGS reductions of 60–75% relative to a normal-cycle vintage, while marketing those expressions as “recession-era reserve lots” or “crisis vintage” editions at $150–$350 retail price points.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| India & Emerging APAC Market Entry via FTA Tariff Arbitrage | +1.8% – +2.2% | India, South Korea, China, Australia | Medium term (2–4 years) |

| Tequila-Based RTD / Canned Cocktail Category Capture | +1.5% – +2.0% | North America core, EU (Germany, UK, Spain) | Short term (≤ 2 years) |

| Agave Surplus Monetization: Ultra-Premium Aging & Controlled-Scarcity Reserve Releases | +1.2% – +1.6% | North America, EU, Japan | Short-to-Medium term (1–3 years) |

| Adjacent Agave Spirit Portfolio Roll-Up (Mezcal, Sotol, Raicilla) | +1.0% – +1.4% | North America, EU emerging | Medium term (2–4 years) |

| Digital DTC / E-Commerce Channel Monetization & Subscription Commerce | +0.8% – +1.2% | North America (U.S. lead), UK, Germany | Short term (≤ 2 years) |

| Zero-Proof & Functional Agave Spirit Innovation | +0.6% – +1.0% | North America, UK, EU, Australia | Medium-to-Long term (2–5 years) |

Challenges Analysis

DO Geographic Lock & Regulatory Compliance Costs

The tequila Denomination of Origin, declared by the Mexican government in 1974 and now internationally recognized across 58 countries, is simultaneously the category’s most powerful competitive moat and its most operationally burdensome structural constraint, as it legally restricts production to Agave tequilana Weber blue variety grown and processed exclusively within Jalisco and four additional states administered through the CRT’s verification, certification, and NOM compliance architecture which covers producers, agave growers, bottlers, marketers, and government agencies in an integrated audit chain.

For producers seeking market access in the EU, UK, Australia, and emerging APAC markets where local labeling requirements, allergen disclosure rules, and geographical indication registration protocols layer on top of Mexico’s NOM mandates compliance costs per market-entry event for a new SKU can range from USD 15,000 to USD 60,000 in legal, regulatory advisory, and laboratory testing fees, disproportionately penalizing the 135+ CRT-registered tequila producers that are small-to-mid-sized and lack the regulatory infrastructure of conglomerate-owned brands, imposing a -0.8 percentage point CAGR friction through its systematic suppression of competitive market-entry velocity in geographies beyond the US corridor.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Agave Boom–Bust Supply Cycle | -1.8% | Jalisco, Los Altos, Nayarit, Guanajuato | Long term (≥ 4 years) |

| Jalisco Aquifer Stress & Water Scarcity | -1.2% | Jalisco core; Michoacán, Tamaulipas corridors | Long term (≥ 4 years) |

| US Trade Policy & Tariff Volatility | -1.5% | US import corridor (80%+ of exports); EU secondary markets | Medium term (2–4 years) |

| DO Geographic Lock & Regulatory Compliance Costs | -0.8% | All five DO states; EU/UK/APAC export markets | Medium term (2–4 years) |

| Category Demand Normalization & Premiumization Erosion | -1.0% | North America (US core); EU emerging; APAC frontier | Medium term (2–4 years) |

| Vinasse & Bagasse Waste Management Burden | -0.7% | Jalisco industrial distillery belt; Tamaulipas | Long term (≥ 4 years) |

Geopolitical Impact Analysis

War, Tariffs, and Shifting trade alliances are quietly redrawing the map for global tequila.

Trade tensions, tariffs, and changing global alliances are reshaping the tequila industry by influencing production costs, exports, and consumer demand. Since tequila can only be produced in designated regions of Mexico under the Denomination of Origin (DOT), the global market depends heavily on a concentrated supply chain. Any disruption caused by trade disputes, tariffs, or transportation bottlenecks directly affects exports, pricing, and product availability in key importing markets.

The Russia–Ukraine conflict increased energy prices, freight costs, and inflation during 2022–2023, raising operating expenses across the global spirits industry. Higher transportation and packaging costs reduced profit margins for tequila producers and importers, while elevated inflation and interest rates in major European markets such as Germany, France, and Italy weakened consumer spending on premium and ultra-premium tequila.

The United States, which accounts for the majority of global tequila imports, continues to be the industry’s largest export destination. Any future tariff changes, customs regulations, or trade negotiations involving Mexico and the U.S. could significantly influence tequila prices, cross-border trade volumes, and investment decisions across the supply chain. Overall, geopolitical developments are creating a mixed outlook raising production and logistics costs in some regions while opening new export opportunities in others, encouraging producers to diversify markets and strengthen supply chain resilience.

Regional Analysis

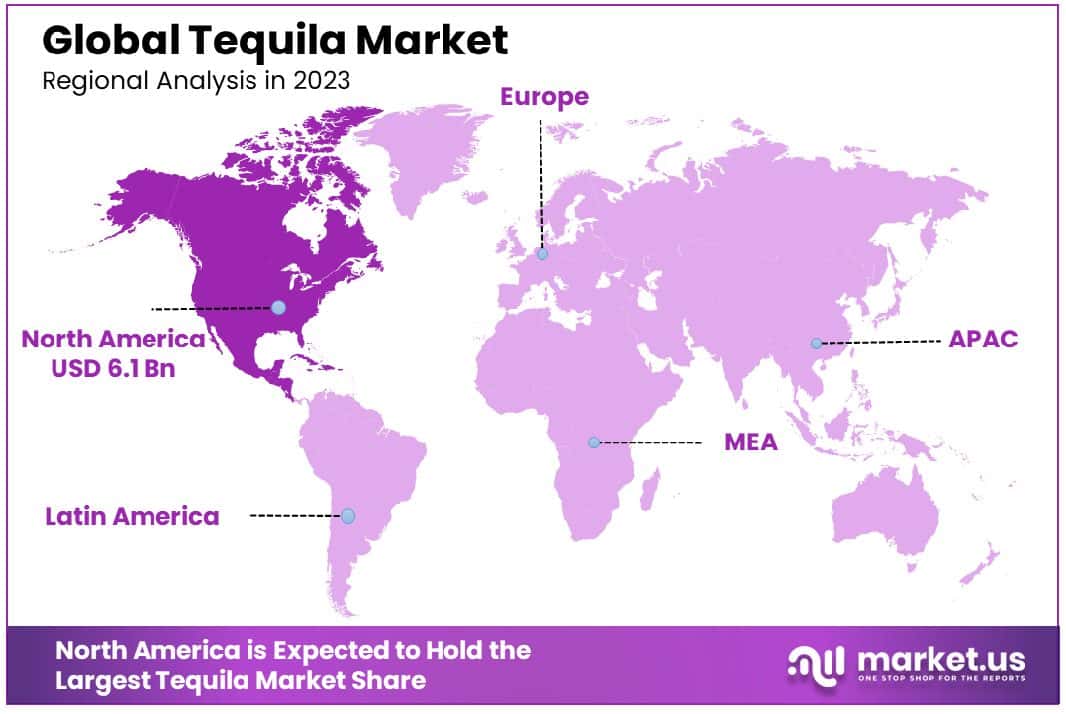

North America Held the Largest Share of the Global Tequila Market.

In 2025, North America dominated the global tequila market, holding about 48.6% of the total global consumption, this strong position is largely driven by the United States, which acts as the main hub for both volume and value demand for agave spirits. The region’s leadership is supported by a deeply rooted cocktail culture, where tequila is a key base spirit in widely consumed drinks. High disposable incomes and a steady shift toward premium products have also pushed consumers away from lower-tier spirits toward 100% agave options.

The remaining global market is distributed across rapidly expanding corridors in Europe, Asia Pacific, Latin America, and the Middle East & Africa (MEA). Europe stands as the second key value market, with growing demand in countries like the UK, Spain, and Germany, where consumers are increasingly drawn to premium and craft-style spirits with strong authenticity. The Asia Pacific region is the fastest-emerging growth area, supported by urbanization, rising incomes, and a growing premium nightlife culture in cities across China, Japan, and India.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Milagro continues to strengthen its position in the premium tequila market through product innovation and international distribution. The brand offers over 10 tequila variants across Silver, Reposado, Añejo, Select Barrel Reserve, and Cristalino categories. The brand focuses on 100% Blue Weber agave sourced from the Jalisco Highlands, reinforcing its premium positioning. Clase Azul remains one of the fastest-growing luxury tequila brands, recognized for handcrafted ceramic decanters and ultra-premium positioning. In 2024, Clase Azul expanded its visitor experience at its Jalisco facilities while increasing exports to luxury retail and hospitality channels, supporting growth in the high-end spirits segment.

Espolón is a key premium tequila brand within Campari Group’s spirits portfolio. The brand markets over 7 tequila expressions, including Blanco, Reposado, Añejo, Cristalino, and limited editions. Campari Group operates in 190+ markets worldwide, providing Espolón with extensive international distribution. Tres Generaciones is Beam Suntory’s premium tequila brand, known for triple-distilled tequila produced in Jalisco, Mexico. The portfolio includes more than 6 expressions, such as Plata, Reposado, Añejo, Cristalino, and special editions. Beam Suntory distributes its spirits in over 70 markets globally through its international sales network.

The Major Players In The Industry

- Jose Cuervo

- Patrón

- Don Julio

- Sauza

- 1800 Tequila

- El Jimador

- Milagro

- Clase Azul

- Espolón

- Olmeca (including Altos)

- Casamigos

- Tres Generaciones

- Código 1530

- Corralejo

- Maestro Dobel

- Other Key Players

Key Development

- In April 2026, Patrón strengthened its position in the premium tequila sector by launching Patrón 100, its first distilled-to-proof tequila bottled at 100 proof, or 50% alcohol by volume, without dilution. The small-batch product is made through 100% tahona-stone production using only 3 ingredients Weber Blue Agave, water and yeast.

- In February 2026, Jose Cuervo entered a multi-year partnership with NASCAR, becoming its Official Tequila, Official Margarita and an official partner from the 2026 racing season. Under the agreement, Cuervo received exclusive promotional rights for tequila, mezcal and other agave-based spirits across NASCAR events and media platforms

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 13.3 Bn |

| Forecast Revenue (2035) | USD 31.3 Bn |

| CAGR (2026-2035) | 9.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Blanco Tequila, Reposado Tequila, Añejo Tequila, Extra Añejo Tequila, Cristalino Tequila, Gold Tequila, Others), By Purity Type (100% Agave Tequila, Mixto Tequila), By Price Range (Economy, Mid-Range, Premium), By Flavor Type (Unflavored, Flavored), By End User (Household Consumers, Commercial Consumers, Others) By Distribution Channel (On-Trade, Off-Trade) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Jose Cuervo, Patrón, Don Julio, Sauza, 1800 Tequila, El Jimador, Milagro, Clase Azul, Espolón, Olmeca (including Altos), Casamigos, Tres Generaciones, Código 1530, Corralejo, Maestro Dobel, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |