Quick Navigation

- Report Overview

- Key Takeaways

- By Product Type Analysis

- By Ingredients Analysis

- By Packaging Type Analysis

- By End User Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

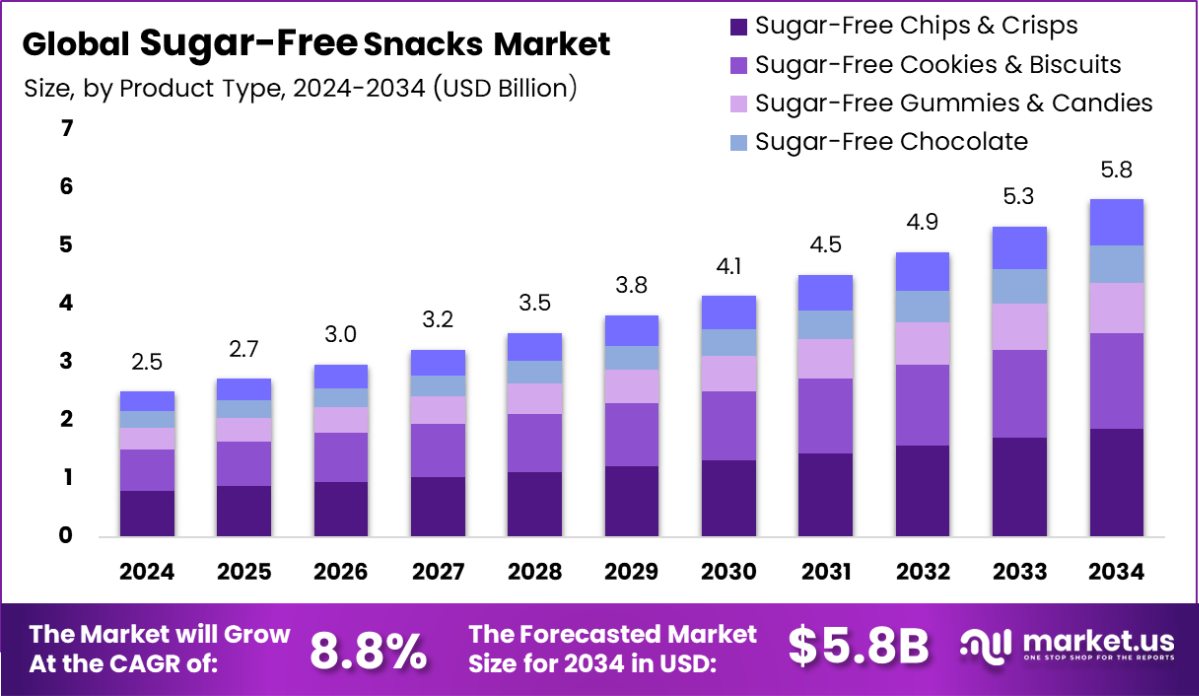

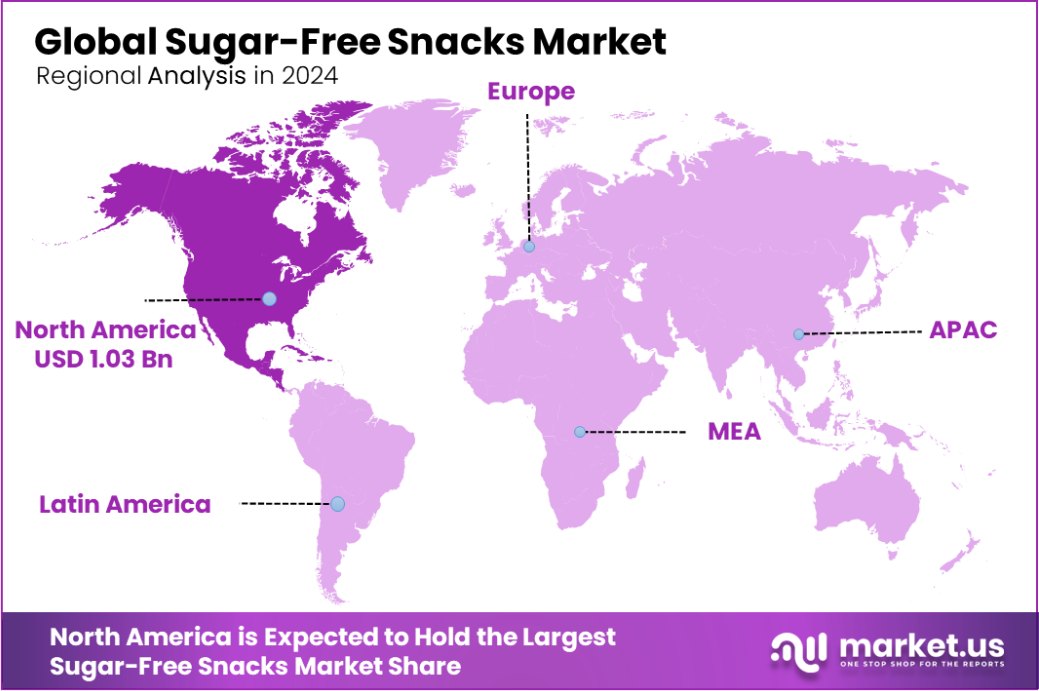

Global Sugar-Free Snacks Market is expected to be worth around USD 5.8 billion by 2034, up from USD 2.5 billion in 2024, and grow at a CAGR of 8.8% from 2025 to 2034. The Sugar-Free Snacks Market in North America reached a dominant share of 41.3%, generating USD 1.03 billion.

Sugar-free snacks are specifically designed to exclude added sugars, catering to those managing diabetes, following ketogenic diets, or reducing sugar intake. These snacks often include low-calorie sweeteners (LCSs) like stevia, erythritol, or artificial sweeteners, providing a sweet taste without the traditional caloric impact of sugar. Notably, 25.1% of children and 41.4% of adults have reported consuming LCSs, which are frequently used in these products.

In 2023, the total utilized production of 21 estimated noncitrus fruit crops in the United States was 16.2 million tons, marking a 5% increase from 2022. Grapes, strawberries, and apples were prominent, accounting for 74% of the total value of utilized noncitrus fruit production. Additionally, California’s organic product sales saw a significant rise, increasing by 18.2% from $9.4 billion in 2018 to $11.1 billion in 2022.

The market for sugar-free snacks is expanding as more health-conscious consumers seek healthier snacking options. This segment serves a diverse audience, including those with medical conditions that necessitate managing sugar intake, weight watchers, and individuals aiming for a healthier lifestyle.

A key growth driver is the increasing awareness of health risks associated with excessive sugar consumption, such as obesity and diabetes. This awareness motivates consumers to choose snacks that provide healthier alternatives without sacrificing taste.

Moreover, the demand for sugar-free snacks is supported by the growing number of consumers adopting specialized diets that limit sugar intake, such as keto and paleo diets. The availability of convenient, ready-to-eat, sugar-free snack options aligns well with the busy lifestyles of modern consumers who are still intent on maintaining a healthy diet.

Opportunities in the sugar-free snacks market include product innovation and geographic expansion. Manufacturers can leverage the trend toward clean-label products by developing snacks with minimal artificial ingredients and transparent labeling. Furthermore, venturing into emerging markets where health awareness is on the rise could open new revenue streams and expand market share.

Key Takeaways

- Global Sugar-Free Snacks Market is expected to be worth around USD 5.8 billion by 2034, up from USD 2.5 billion in 2024, and grow at a CAGR of 8.8% from 2025 to 2034.

- Sugar-Free Chips and Crisps hold a significant 32.5% share in the Sugar-Free Snacks Market product type segment.

- Natural Sweeteners are preferred in 42.4% of products in the Sugar-Free Snacks Market, indicating a trend towards healthier ingredients.

- Retail Packaging dominates the Sugar-Free Snacks Market packaging types, comprising 53.4% of the market.

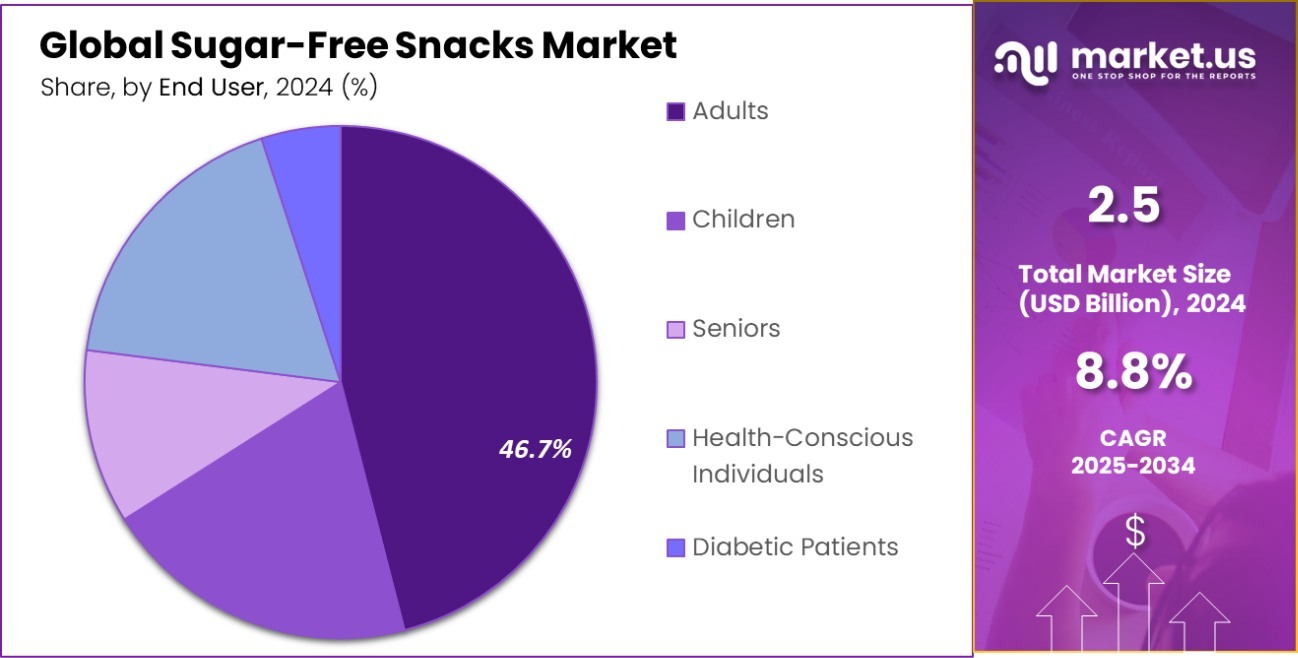

- Adults are the primary end users in the Sugar-Free Snacks Market, making up 46.7% of its consumer base.

- Supermarkets and hypermarkets are the leading distribution channel, capturing 44.5% of the Sugar-Free Snacks Market.

- North America led the Sugar-Free Snacks Market with a 41.3% share, amassing revenues worth USD 1.03 billion.

By Product Type Analysis

Sugar-Free Chips and Crisps hold a 32.5% share in the sugar-free snacks market.

In 2024, Sugar-Free Chips and Crisps held a dominant market position in the “By Product Type” segment of the Sugar-Free Snacks Market, capturing a 32.5% share. This prominence is attributed to consumers’ increasing preference for healthier versions of traditional snacks. The shift toward sugar-free options reflects a broader trend of health-conscious eating, driven by a growing awareness of the adverse effects associated with high sugar intake.

The popularity of sugar-free chips and crisps is further supported by innovations in flavor and texture, making them a desirable choice not only for health-conscious individuals but also for the general snacking population. Manufacturers have successfully leveraged advanced food processing technologies to maintain the satisfying crunch and flavor diversity that consumers expect from traditional snacks without the added sugars.

As market dynamics evolve, the segment continues to see robust growth, fueled by strategic marketing campaigns that highlight the health benefits of sugar-free snacking. The continued expansion of this segment is anticipated as consumer demand for diet-specific products increases, making sugar-free chips and crisps a staple in the snacking industry.

By Ingredients Analysis

Natural sweeteners dominate, comprising 42.4% of ingredients in sugar-free snacks.

In 2024, Natural Sweeteners held a dominant market position in the “By Ingredients” segment of the Sugar-Free Snacks Market, capturing a 42.4% share. This substantial market share underscores the growing consumer preference for snacks formulated with natural ingredients over artificial alternatives. Natural sweeteners, such as stevia, erythritol, and xylitol, are favored for their lower glycemic index and fewer health risks compared to synthetic sweeteners.

The appeal of natural sweeteners extends beyond just the health benefits; it also taps into the clean label trend that is sweeping the food industry. Consumers are increasingly scrutinizing labels, seeking products with recognizable and simple ingredients. This shift has prompted manufacturers to reformulate their products to include natural sweeteners, which align well with the demand for transparency and natural food sources.

The robust position of natural sweeteners in the market is also driven by regulatory support for natural ingredients and widespread public campaigns promoting natural and organic products. As awareness and education about the benefits of natural sweeteners continue to spread, their prevalence in sugar-free snacks is expected to grow, further cementing their leading position in the market.

By Packaging Type Analysis

Retail packaging is preferred for sugar-free snacks, capturing 53.4% of the market.

In 2024, Retail Packaging held a dominant market position in the “By Packaging Type” segment of the Sugar-Free Snacks Market, with a 53.4% share. This leadership is largely driven by the consumer shift towards convenient, on-the-go snacking options, which require robust and portable packaging solutions. Retail packaging, encompassing a range of formats such as flexible wrappers, rigid boxes, and resealable bags, caters effectively to this demand, offering both functionality and aesthetic appeal.

The dominance of retail packaging in the sugar-free snacks market is also bolstered by its critical role in brand differentiation and marketing. Eye-catching and informative packaging designs help brands communicate the health benefits of their sugar-free products directly to health-conscious consumers, influencing purchase decisions at the point of sale. Moreover, advances in packaging technology have allowed for improved preservation of freshness and taste, crucial for maintaining the quality of sugar-free products, which can be sensitive to environmental factors.

As consumers continue to favor snacks that align with their health-centric lifestyles, the importance of effective retail packaging is expected to grow. This trend is anticipated to drive further innovations in packaging solutions, aiming to enhance consumer convenience, product safety, and brand visibility.

By End User Analysis

Adults are major consumers of sugar-free snacks, representing 46.7% of the market.

In 2024, Adults held a dominant market position in the “By End User” segment of the Sugar-Free Snacks Market, with a 46.7% share. This segment’s strong performance is indicative of the growing health awareness among adults who are increasingly seeking snacks that align with their dietary preferences and health goals. Sugar-free snacks, offering reduced caloric intake and lower glycemic index, cater perfectly to adults managing weight or chronic conditions like diabetes.

The preference for sugar-free snacks among adults is further driven by broader lifestyle trends toward healthier eating and wellness. As adults become more informed about the impacts of sugar consumption, there is a noticeable shift toward products that promote sustained energy and wellness without sacrificing taste. Manufacturers have responded by developing a wide range of sugar-free snack options that do not compromise on flavor, thus broadening their appeal.

Moreover, the marketing strategies focusing on the benefits of sugar-free diets have successfully targeted adult consumers, emphasizing the snacks’ compatibility with a healthy lifestyle. This has not only bolstered sales but also reinforced the position of sugar-free snacks as a mainstream choice in adult diets. The trend is expected to continue, with more adults turning to sugar-free alternatives as part of a balanced diet.

By Distribution Channel Analysis

Supermarkets and hypermarkets lead distribution, with a 44.5% share in the market.

In 2024, Superarkets and Hypermarkets held a dominant market position in the “By Distribution Channel” segment of the Sugar-Free Snacks Market, capturing a 44.5% share. This substantial market share is a testament to the critical role these retail giants play in the consumer goods industry. Supermarkets and hypermarkets are pivotal in making sugar-free snacks readily available to a broad consumer base, offering a wide variety of choices under one roof.

The strength of supermarkets and hypermarkets in this sector is driven by their ability to provide a convenient shopping experience, combined with the advantage of physical browsing, which allows consumers to make informed choices by directly evaluating product information and packaging. These outlets also benefit from strategic shelf placements and promotional activities that increase the visibility of sugar-free snack options to health-conscious shoppers.

Additionally, the trust and reliability associated with well-known supermarket and hypermarket chains encourage consumers to try new products, including sugar-free snacks. As these retailers continue to expand their health and wellness product lines in response to consumer demand, their market share in the distribution of sugar-free snacks is expected to remain robust.

Key Market Segments

By Product Type

- Sugar-Free Chips And Crisps

- Sugar-Free Cookies And Biscuits

- Sugar-Free Gummies And Candies

- Sugar-Free Chocolate

- Sugar-Free Granola And Bars

By Ingredients

- Natural Sweeteners

- Artificial Sweeteners

- Whole Grains

- Nuts and Seeds

- Fruits and Vegetables

By Packaging Type

- Bulk Packaging

- Retail Packaging

- Reusable Containers

- Single Serve Packaging

- Eco-Friendly Packaging

By End User

- Adults

- Children

- Seniors

- Health-Conscious Individuals

- Diabetic Patients

By Distribution Channel

- Online Retail

- Supermarkets and Hypermarkets

- Specialty Stores

- Health Food Stores

- Convenience Stores

- Others

Driving Factors

Increased Health Awareness Among Consumers

One of the primary driving factors of the Sugar-Free Snacks Market is the heightened health awareness among consumers. In recent years, there has been a significant shift in consumer behavior as more individuals become aware of the health implications associated with sugar consumption. This awareness is largely due to widespread public health campaigns and the availability of nutritional information.

As a result, consumers are actively seeking healthier alternatives to traditional snacks that are high in sugar. Sugar-free snacks cater to this demand by offering options that not only satisfy cravings but also align with a health-conscious lifestyle. The market for these products continues to grow as consumers prioritize wellness and preventive health care in their dietary choices.

Restraining Factors

High Cost of Sugar-Free Snack Products

A significant restraining factor in the Sugar-Free Snacks Market is the high cost associated with these products compared to their sugary counterparts. Sugar-free snacks often require specialized ingredients, such as natural sweeteners and alternative flours, which are typically more expensive to source and process.

Additionally, the production of sugar-free snacks involves stringent quality controls and advanced technology to ensure a taste and texture that appeal to health-conscious consumers without the use of conventional sugar.

These factors contribute to higher manufacturing costs, which are then passed on to consumers in the form of higher retail prices. This price disparity can deter budget-conscious shoppers, limiting the market reach of sugar-free snacks among broader demographics.

Growth Opportunity

Expansion into Emerging Markets with Health Trends

A key growth opportunity in the Sugar-Free Snacks Market is the expansion into emerging markets where health trends are beginning to take hold. As global awareness of health and wellness increases, so does the demand for healthier food options, including sugar-free snacks. Emerging markets, with their rising middle-class populations and increasing disposable incomes, present a fertile ground for the introduction of health-oriented products.

These regions are witnessing a shift in consumer preferences towards foods that support a healthier lifestyle, but may have limited availability of such options. By entering these markets, companies can capitalize on first-mover advantages, establish brand loyalty, and build a strong consumer base eager for healthier snack alternatives.

Latest Trends

Rising Popularity of Organic Sugar-Free Snacks

A prominent trend in the Sugar-Free Snacks Market is the rising popularity of organic sugar-free snacks. Consumers are not only looking for snacks that are free from added sugars but also prefer organic options, ensuring that the ingredients used are free from pesticides and genetically modified organisms (GMOs). This trend is driven by a growing consumer desire for transparency and purity in food sourcing and production processes.

Organic, sugar-free snacks appeal to health-conscious consumers who are vigilant about both sugar content and the overall quality of the ingredients in their food. As a result, manufacturers are increasingly focusing on developing and marketing certified organic sugar-free snacks, which promise both health benefits and environmental sustainability.

Regional Analysis

In 2024, North America held 41.3% of the Sugar-Free Snacks Market, totaling USD 1.03 billion in revenue.

In the global landscape of the Sugar-Free Snacks Market, North America emerges as the dominating region, holding a substantial 41.3% market share and generating revenues amounting to USD 1.03 billion.

This robust market presence is attributed to a highly health-conscious population and widespread awareness regarding the benefits of reducing sugar intake. North America’s dominance is further bolstered by the presence of major market players who are continuously innovating sugar-free snack options.

Europe follows closely, leveraging its stringent food safety regulations, which favor the production and consumption of sugar-free snacks. The region’s focus on healthier living standards drives a significant demand for these products.

The Asia Pacific region is experiencing rapid growth in this market due to changing dietary habits and increasing disposable incomes, particularly in emerging economies like China and India, where there is a growing middle-class population seeking healthier food alternatives.

Meanwhile, the Middle East & Africa, and Latin America are gradually catching up, with an increasing number of health awareness initiatives and rising diabetes prevalence encouraging the consumption of sugar-free snacks. These regions present untapped opportunities for market expansion as consumer awareness and health infrastructure continue to improve.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global Sugar-Free Snacks Market is significantly shaped by the strategic actions and offerings of key players, including Hostess Brands Inc., Kellanova, Kraft Heinz, Mars Incorporated, Mondelez International Inc., Nestle SA, Strauss Group Ltd, The Hershey Company, The Kraft Heinz Company, and Unilever. These companies are pivotal in driving innovation and accessibility within the market.

Hostess Brands Inc. and Kellanova are making notable strides in diversifying their product portfolios to include a variety of sugar-free options that cater to the growing consumer demand for healthier snack choices. Both companies are leveraging their robust distribution networks to ensure the widespread availability of these healthier options.

Kraft Heinz and The Kraft Heinz Company, often leading in condiments and sauces, are expanding their reach by introducing sugar-free versions of popular snacks, thus tapping into the health-conscious consumer segment. Their established brand presence and marketing prowess enable them to effectively communicate the benefits of their sugar-free offerings.

Mars Incorporated and Mondelez International Inc. are at the forefront of reformulating their existing top-selling products to reduce sugar content without compromising taste. This strategy not only helps retain existing customers but also attracts new consumers looking for healthier alternatives.

Nestle SA and Unilever, with their global footprint, are innovating in sugar-free confections and ice creams, respectively. They focus on using natural sweeteners to maintain the sensory appeal of their products.

Lastly, Strauss Group Ltd and The Hershey Company are concentrating on targeted marketing strategies to highlight the health benefits of their sugar-free product lines, particularly in markets with high health awareness.

Top Key Players in the Market

- Hostess Brands Inc.

- Kellanova

- Kraft Heinz

- Mars Incorporated

- Mondelez International Inc.

- Nestle SA

- Strauss Group Ltd

- The Hershey Company

- The Kraft Heinz Company

- Unilever

Recent Developments

- In October 2024, launched Cerelac variants with no refined sugar in the Indian market. Out of 21 variants, 14 will be free of refined sugar, with seven available by November 2024 and the rest following shortly after.

- In May 2024, Mondelez International Inc. showed interest in investing in start-ups developing innovative snack technologies, such as Torr Foodtech, which creates snack bars without added sugar by using a unique “welding” technology.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.5 Billion |

| Forecast Revenue (2034) | USD 5.8 Billion |

| CAGR (2025-2034) | 8.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Sugar-Free Chips And Crisps, Sugar-Free Cookies And Biscuits, Sugar-Free Gummies And Candies, Sugar-Free Chocolate, Sugar-Free Granola And Bars) , By Ingredients (Natural Sweeteners, Artificial Sweeteners, Whole Grains, Nuts and Seeds, Fruits and Vegetables), By Packaging Type (Bulk Packaging, Retail Packaging, Reusable Containers, Single Serve Packaging, Eco-Friendly Packaging), By End User (Adults, Children, Seniors, Health-Conscious Individuals, Diabetic Patients), By Distribution Channel (Online Retail, Supermarkets and Hypermarkets, Specialty Stores, Health Food Stores, Convenience Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Hostess Brands Inc., Kellanova, Kraft Heinz, Mars Incorporated, Mondelez International Inc., Nestle SA, Strauss Group Ltd, The Hershey Company, The Kraft Heinz Company, Unilever |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |