Quick Navigation

Report Overview

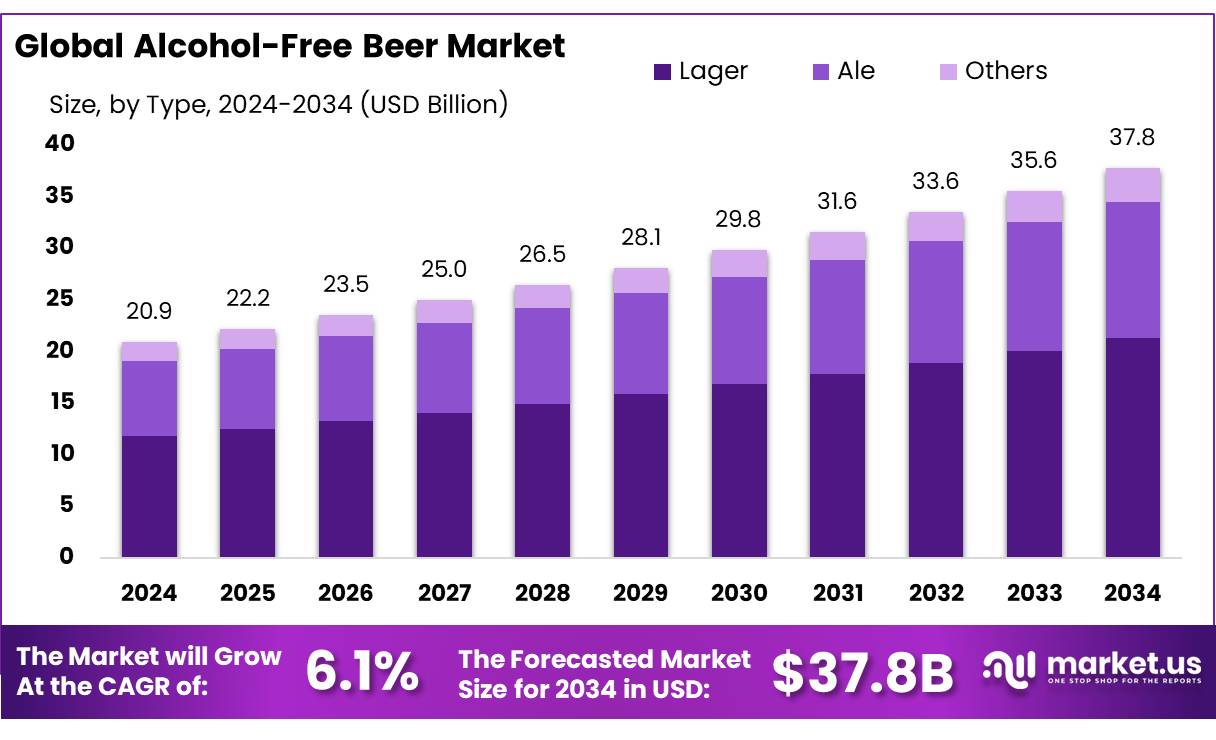

The Global Alcohol-Free Beer Market size is expected to be worth around USD 37.8 Billion by 2034, from USD 20.9 Billion in 2024, growing at a CAGR of 6.1% during the forecast period from 2025 to 2034. The global alcohol-free beer market has experienced significant growth and transformation in recent years, driven by shifting consumer preferences, rising health consciousness, and increasing demand for low-alcohol and alcohol-free alternatives.

Alcohol-free beer, typically containing less than 0.5% alcohol by volume (ABV), caters to individuals seeking to reduce or eliminate alcohol consumption due to health and lifestyle intention. The appeal of these beverages lies in their ability to deliver the taste and experience of traditional beer without the intoxicating effects of alcohol.

The market has seen notable product innovation, with breweries introducing a wide variety of alcohol-free options, ranging from hoppy India Pale Ales (IPAs) to rich stouts and fruit-infused radlers. Companies are also exploring the use of specialty ingredients, such as natural extracts, hop oils, and ester replacement products, to refine flavors and mask any undesirable characteristics resulting from the absence of alcohol. This focus on innovation has significantly improved both the quality and variety of alcohol-free beers available in the market, attracting a broader consumer base.

Additionally, countries like Iran have witnessed a rise in innovative non-alcoholic products tailored to local tastes. This growing demand aligns with global wellness trends, as consumers increasingly prioritize healthier lifestyles. Campaigns like “Dry January” and “Sober October” have further accelerated this shift by promoting alcohol moderation and encouraging consumers to explore alcohol-free options.

Major beverage companies are capitalizing on these trends by expanding their portfolios to include alcohol-free alternatives. For instance, Heineken has successfully positioned its Heineken 0.0 product as a popular choice in key markets such as the United Kingdom, Spain, and Russia, where non-alcoholic beer sales now represent a notable portion of the company’s revenue.

Similarly, AB InBev leveraged the global stage at the 2024 Paris Olympic Games by promoting Corona Cero as the official non-alcoholic beer sponsor. The brand’s “Golden Moments” campaign emphasized responsible drinking and encouraged consumers to incorporate non-alcoholic options into their celebrations, reinforcing the growing acceptance of alcohol-free beverages in mainstream culture.

Key Takeaways

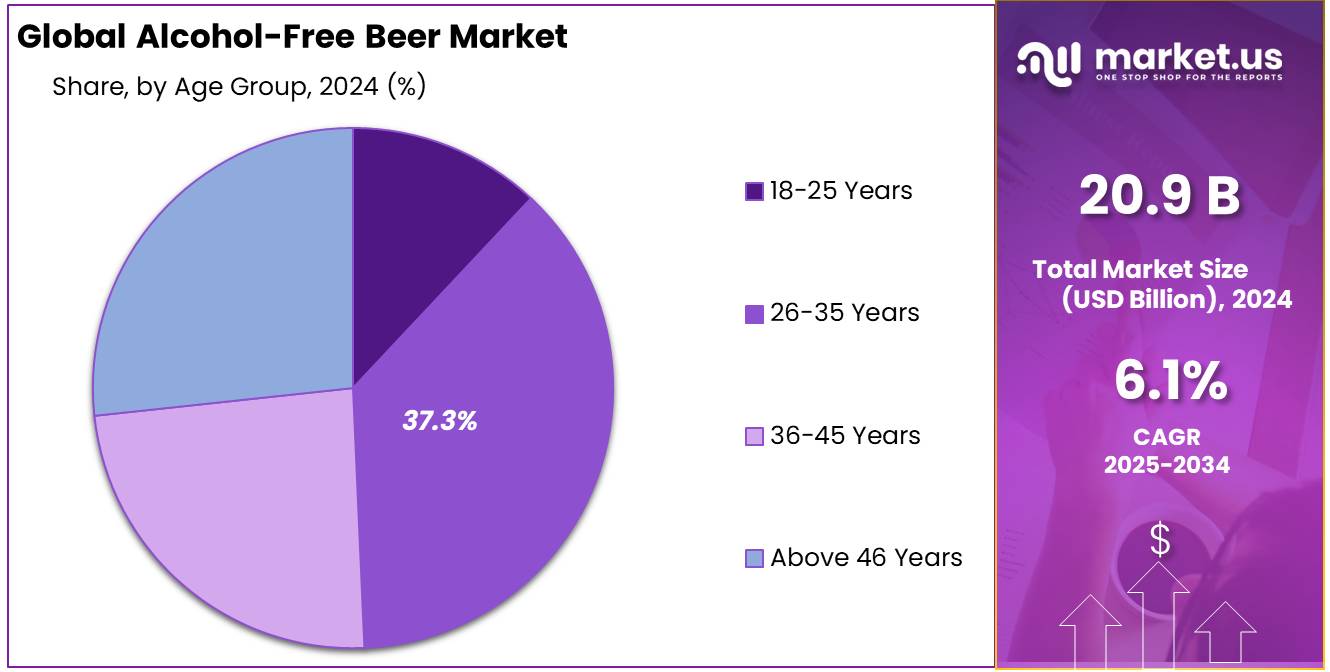

- In 2024, the global alcohol-free beer market was valued at US$ 20.9 Billion

- Among product types, the lager held the majority of the revenue share at 56.4%

- Based on category, plain alcohol-free beer accounted for the largest market share with 73.4%

- By production method, the physical process segment dominated the global market with 65.4% market share in 2024

- Among packaging type, can packaging dominated the market with significant market share of 57.1%

- By distribution channel, supermarkets & hypermarkets held majority of market share at 42.3%

- Based on age group, 26-35 years segment accounted for 37.3% of the market revenue share

- Among end-user, male segment accounted for the majority of the alcohol-free beer market share with 58.6%

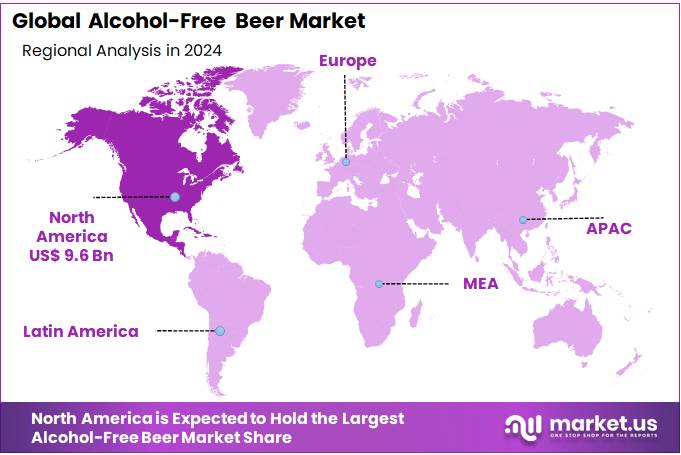

- In 2024, North America dominated the global market with significant market share of 46.3%

Product Type Analysis

The lager segment holds a significant share in the alcohol-free beer market, driven by its widespread popularity and smooth, crisp flavor profile that appeals to a broad consumer base.

The global alcohol-free beer market is segmented by product type into lager, ale, and others. Among these, the lager segment dominated the market, holding a 56.4% share, driven by its nutritional properties, mood-enhancing qualities, and taste profile that closely resembles traditional alcoholic beer.

Lager, a classic mainland European beer—often referred to as Pilsner lager or Pils, originating from Pilsen in Bohemia—is characterized by its fermentation process and distinct flavor attributes. Known for its clean, crisp, and smooth taste compared to ales, non-alcoholic lager offers a light and refreshing experience. It is typically brewed with the same ingredients as regular lager, with the alcohol removed during the brewing process, making it an appealing option for classic beer enthusiasts seeking alcohol-free alternatives.

Major commercial breweries have increasingly introduced alcohol-free versions of their popular lagers, reflecting the growing consumer demand for healthier beverage choices. Notably, non-alcoholic lager contains fewer calories than its alcoholic counterpart, with approximately 20 kcal per 100 ml compared to around 40 kcal for regular lager. Companies like IMPOSSIBREW have strengthened their position in the non-alcoholic beer market by leveraging innovative brewing methods, such as their proprietary Social Blend technology, which mimics the relaxation effects of alcoholic drinks. As per survey conducted by IMPOSSIBREW over the 775 customers, 70.6% responded the relaxation benefits associated with alcohol free lager.

Category Analysis

The plain alcohol-free beer segment holds a significant share in the global market, driven by growing consumer demand for traditional beer experiences

Based on category, the global alcohol-free beer market is segmented into plain and flavored variants. Among these, the plain alcohol-free beer segment accounted for the majority of the market share, representing 73.4%. Plain alcohol-free beers are characterized by their traditional, malty taste with minimal added flavoring, closely replicating the taste, aroma, and mouthfeel of conventional alcoholic beers. This segment appeals to classic beer enthusiasts who value authenticity and prefer a familiar drinking experience without the presence of alcohol.

Popular brands such as Heineken 0.0, Clausthaler Original, and Guinness 0.0 have established strong positions within this category. Plain alcohol-free beers are typically produced using traditional brewing methods, with alcohol removed through processes such as vacuum distillation, reverse osmosis, or limited fermentation. These methods ensure that the core flavor profiles remain intact while significantly reducing the alcohol content. Their lower calorie content, combined with classic beer flavors, has made them a preferred choice for health-conscious individuals.

By Production Method

Physical processes dominated the market, driven by their efficiency in reducing alcohol content while preserving the beer’s sensory characteristics

Based on production methods, the global alcohol-free beer market is segmented into physical and biological processes. Among these, the physical process segment accounted for a dominant market revenue share of 65.4%, driven by the availability of various advanced techniques such as thermal treatments and membrane separation. The growing preference for physical methods is attributed to their efficiency in preserving the sensory characteristics of beer while effectively reducing or eliminating alcohol content.

In recent decades, production methods for non-alcoholic and low-alcohol beer have evolved significantly, aligning with rising market demand. This growth has been fueled by stricter alcohol consumption policies, particularly within the European Union, and increasing consumer awareness of the benefits associated with moderate beer consumption.

By Packaging Type

The can segment holds a significant share of the alcohol-free beer market, driven by its convenience, portability, and sustainability

Based on packaging type, the global alcohol-free beer market is segmented into cans and bottles. In 2024, the can-based segment dominated the market, accounting for a substantial 57.1% revenue share. Cans have emerged as a preferred packaging option due to their convenience, portability, and visual appeal, attracting active consumers with on-the-go lifestyles. To enhance their aesthetic appeal, cans often feature a matte lacquer finish, providing a smooth texture and a striking look, while internal lacquer coatings prevent corrosion and protect the beverage from contamination.

The growing emphasis on sustainability has further propelled the adoption of aluminum and steel cans. These materials are not only lightweight and durable but also highly recyclable. According to Metal Packaging Europe, aluminum cans have a higher recycling rate and greater recycled content compared to other packaging types. Recycling aluminum requires up to 95% less energy than producing it from raw ore, significantly reducing greenhouse gas emissions.

As per The International Aluminium Institute, globally, nearly 70% of all aluminum beverage cans are recycled, with Europe leading at an 81% Recycling Efficiency Rate (RER). With their strong blend of practicality, aesthetic appeal, and environmental benefits, cans are expected to maintain their dominance in the alcohol-free beer market.

By Distribution Channel

The supermarkets/hypermarkets distribution channel dominated the global market owing to recurrent promotional initiatives and discounted offerings

Based on distribution channel, the global alcohol-free beer market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail, and others. Among these, the supermarkets/hypermarkets segment dominated the market, accounting for a notable 42.3% of revenue share in 2024. Supermarkets and hypermarkets have maintained their leading position due to a combination of key factors.

These large-scale retail outlets offer a wide and diverse selection of alcohol-free beers, including both well-established brands and niche, craft alternatives. Their ability to provide consumers with a convenient, one-stop shopping experience has strengthened their appeal, seamlessly integrating alcohol-free options into routine grocery purchases. The extensive shelf space and storage capacity of supermarkets and hypermarkets allow for the effective display of a broad range of flavors, product innovations, and packaging formats — catering to various consumer preferences.

By Age Group Analysis

The 26-35 years segment represents a significant share of the alcohol-free beer market, driven by a strong focus on health, fitness, and overall wellness.

The 26-35 years segment dominates the alcohol-free beer market, capturing a significant share of 37.3% in 2024, due to this group’s strong focus on wellness and balanced lifestyles. Consumers in this age group are actively seeking alternatives that allow them to enjoy social experiences without compromising their health. Their preference leans towards alcohol-free beers that offer authentic flavors, innovative ingredients like adaptogens, and added functional benefits such as vitamins or probiotics. This demographic is highly brand-conscious, often drawn to products with eco-friendly packaging and transparent sourcing.

Additionally, their digital-savviness drives online purchases, with many influenced by targeted social media campaigns and influencer endorsements. Supermarkets and specialty stores also remain crucial points of sale, allowing them to explore new varieties in person. As they prioritize both indulgence and well-being, brands that offer sophisticated, health-conscious options tailored to their tastes are gaining traction, reinforcing the segment’s dominant position in the alcohol-free beer market.

By End-users Analysis

The male segment dominates the alcohol-free beer market, supported by a rising trend of “sober curiosity” and performance-driven lifestyles.

In 2024, the male segment holds a prominent share of 58.6% in the alcohol-free beer market, driven by the growing interest in healthier lifestyle choices without sacrificing the social experience of drinking. Many male consumers are turning to alcohol-free alternatives to reduce their alcohol intake while still enjoying the taste and ritual of beer.

This shift is particularly noticeable among fitness enthusiasts and athletes who seek beverages with fewer calories and added functional benefits like electrolytes or vitamins. Moreover, marketing strategies targeting men often highlight the authenticity of alcohol-free beers, emphasizing bold flavors, craft brewing techniques, and sports sponsorships — such as partnerships with major events like the Olympics.

Key Market Segments

By Product Type

- Lager

- Ale

- Other

By Category

- Plain

- Flavor

By Production Type

- Physical

- Thermal

- Membrane

- Others

- Biological

- Traditional

- Continuous Fermentation

By Packaging Type

- Can

- Bottles

Based on Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

- Others

By Age Group

- 18-25 Years

- 26-35 Years

- 36-45 Years

- Above 46 Years

Based on End-users

- Male

- Female

Drivers

Rise of health and wellness focus and mindful drinking movement in the market is propelling the market revenue growth

Alcohol-free beer, with a history spanning more than four decades, has steadily gained prominence in global markets, both in terms of volume and market share, while also securing a place in modern culture. This growth can be attributed to advancements in essential brewing technologies and a notable shift in lifestyle and socializing patterns. Initially, the market was dominated by “low-alcohol” beers — products that met legal criteria but contained approximately 0.5% ABV. However, the category has since evolved, with zero-alcohol beers now taking the lead, offering beverages that are entirely free from alcohol.

The rising demand for alcohol-free beer is largely driven by growing consumer awareness surrounding health and wellness. As individuals become increasingly conscious of the negative impacts of alcohol consumption on a healthy lifestyle, many are seeking low- or no-alcohol alternatives. The growing “mindful drinking” movement has further amplified this trend, encouraging consumers to opt for alcohol-free beverages.

Several key factors are contributing to the expansion of the alcohol-free beer market. These beverages are associated with a range of health benefits, including improved cardiovascular health, bone health, stress reduction, and sleep promotion. Studies suggest that alcohol-free beer may help lower blood pressure, reduce inflammation, and decrease the risk of developing atherosclerosis.

Restraints

Presence of strengthen rules and regulations is having negative influence on the market revenue growth

Regulations play a crucial role in shaping the growth potential and market entry strategies for non-alcoholic beer. Regulatory bodies have the authority to impose specific restrictions, often creating challenges for companies as they navigate multiple and sometimes conflicting regulations. Federal oversight of the beverage industry can impede the growth of the non-alcoholic beer market, with key areas of regulation including tax treatment, production processes, FDA requirements, labeling compliance, and ingredient approvals.

Non-alcoholic beer must adhere to FDA standards concerning microbiological safety and chemical contamination, such as heavy metals. Furthermore, the maximum allowable alcohol content in non-alcoholic beers varies significantly across countries. In Brazil and the Mercosur region, for instance, non-alcoholic beers are legally defined as those containing an alcohol content of less than or equal to 0.5% by volume, while beverages exceeding this threshold are classified as alcoholic beers.

Before production, companies developing non-alcoholic beer must submit their product formulas for approval by the Food and Drug Administration (FDA). Additionally, if the beverage is entirely alcohol-free, the Alcohol and Tobacco Tax and Trade Bureau (TTB) requires the submission of laboratory testing results. These regulatory processes directly impact market growth by increasing manufacturing and labeling costs and restricting product formulation through ingredient limitations.

Opportunity

Innovation in Flavor Enhancement and Brewing Techniques

The growing consumer demand for non-alcoholic beer that replicates the rich flavors and aromas of full-strength brews presents a significant opportunity for market expansion. Brewers and beverage innovators are leveraging advanced brewing techniques and premium ingredients to craft non-alcoholic beer that delivers an authentic and satisfying drinking experience while remaining alcohol-free. The non-alcoholic beer landscape has evolved to offer a diverse range of styles — from hoppy India Pale Ales (IPAs) to robust stouts — ensuring consumers can explore a wide spectrum of taste profiles.

For instance, innovations such as DSM’s Brewers TasteZyme G have emerged as game-changers, addressing the challenge of achieving well-balanced flavor profiles by mitigating the excessive sweetness often associated with non-alcoholic beer and enhancing their refreshing quality.

Additionally, the rapid development of the zero-alcohol flavored beer segment provides further growth potential. Consumers are increasingly drawn to bold, fruity flavors and unique combinations, incorporating ingredients such as fruit juices, pulps, and tea leaves. Brewers are also utilizing a variety of malts, hops, and hop oils to create complex flavor notes — from caramel and sponge cake to citrus and floral scents.

Trends

Advancements in Brewing Technologies

Advancements in brewing technologies have played a pivotal role in the growth of the alcohol-free beer market. Innovations such as membrane technology and natural fermentation have enabled the production of alcohol-free beer without compromising taste or quality. These technological strides allow consumers to enjoy a refreshing beverage while preserving the authentic beer experience.

Among the various techniques used to craft alcohol-free beer, one method stands out for its ability to retain flavor — the use of specialized yeast cultures that convert only a minimal amount of sugar into alcohol. This approach allows brewers to produce alcohol-free or low-alcohol specialty beers with an alcohol content as low as 0.2% to 0.3%, offering a well-balanced alternative for health-conscious consumers.

Growing Influence of Marketing and Branding

Marketing and branding have become pivotal in shaping consumer perceptions and driving the growth of the non-alcoholic beer market. As the market matures, breweries are placing greater emphasis on developing strong brand identities that resonate with target audiences by highlighting the unique attributes of their products.

A key trend involves positioning non-alcoholic beers as premium and aspirational beverages, focusing on quality, craftsmanship, and refined flavor profiles. This strategy often incorporates sleek packaging designs, distinctive brand names, and sophisticated marketing campaigns aimed at appealing to a discerning consumer base.

Regional Analysis

The demand for non-alcoholic beer in North America is projected to witness substantial growth during the forecast period. In 2024, the region accounted for a significant market revenue share of 46.3% in the global non-alcoholic beer market. The increasing preference for health-conscious consumption and the rising demand for sophisticated alternatives to traditional alcoholic beverages have been key drivers of this growth in both the United States and Canada. This evolving consumer landscape presents significant opportunities for alcohol brands to diversify their product portfolios and cater to changing market preferences.

A recent survey conducted by the Beer Institute highlights the growing popularity of non-alcoholic beer in the United States, particularly in alignment with trends such as Dry January and mindful drinking. The survey, conducted between January 2 and January 6, 2025, among over 2,000 adults of legal drinking age, indicated that 60% of Americans perceive low- and no-alcohol beer as a viable option for long-term moderation, reflecting a two-percentage-point increase from 2024.

Additionally, 22% of respondents expressed a preference for non-alcoholic beer over other alcohol-free alternatives, compared to 10% for non-alcoholic spirits and 13% for non-alcoholic wine. Wellness considerations (49%) and cost savings (48%) emerged as the primary motivations for engaging in Dry January or Damp January.

Independent breweries in the United States have been proactive in addressing the increasing demand for non-alcoholic beer. Craft breweries such as Athletic Brewing and Best Day Brewing have positioned themselves exclusively within the non-alcoholic beer segment, while established brands, including Deschutes Brewery and Samuel Adams, have also introduced their own non-alcoholic product lines. These breweries have witnessed strong consumer engagement, not only during seasonal events such as Dry January but also among year-round mindful drinkers. Athletic Brewing, in particular, has gained prominence as the 14th largest craft brewery in the United States, driven by its entirely non-alcoholic product portfolio.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Market players in the alcohol-free beer industry are adopting diverse strategies to address evolving consumer preferences and sustain their competitive edge. Companies are increasingly investing in research and development to produce advanced alcohol-free beers with improved flavor profiles, enhanced quality, and balanced nutritional content. These innovations aim to meet the rising demand for non-alcoholic beverages across various consumer segments.

Additionally, industry participants are actively pursuing collaborations, mergers, and acquisitions to strengthen their market presence and diversify product portfolios. Strategic partnerships and acquisitions enable companies to leverage cutting-edge technologies, expand their geographical reach, and access new consumer bases. By integrating innovative brewing techniques and forming alliances, market players not only enhance their product offerings but also solidify their position in the competitive landscape of the alcohol-free beer market.

Market Key Players

- Bavarian State Brewery Weihenstephan

- Anheuser-Busch InBev

- Heineken N.V.

- Coors Brewing Company

- BERNARD Family Brewery, a.s.

- Athletic Brewing Company

- Moscow Brewing Company

- Big Drop Brewing Pty Ltd

- Carlsberg Breweries A/S

- Bravus Brewing Company

- Brooklyn Brewery

- ERDINGER Weißbier

- Krombacher Startseite

- Swinkels Family Brewers

- Other Key Players

Recent Development

- In November 2024, HEINEKEN announced a €45 million investment in the Dr. H.P. Heineken Centre, a state-of-the-art R&D facility in Zoeterwoude, set to open in mid-2025. Spanning 8,800 m², the Global R&D Centre will focus on enhancing existing products, developing new offerings, and supporting innovation for global brands like Heineken, Desperados, and Amstel. The facility will feature offices, laboratories, a model service centre, and sensory research and packaging development departments, strengthening HEINEKEN’s global R&D network across Mexico, South Africa, and Southeast Asia.

- In September 2024, Anheuser-Busch, America’s leading brewer, announced the launch of Michelob ULTRA Zero, a premium alcohol-free brew designed to offer consumers aged 21 and above more choice as part of an active lifestyle. This new offering aims to cater to a wider range of social occasions, reinforcing Anheuser-Busch’s commitment to innovation and meeting the growing demand for alcohol-free beverage options.

- In July 2024, Athletic Brewing Company, the largest non-alcoholic brewery in the United States, announced the successful closure of a $50 million equity financing round. The round was led by General Atlantic, a prominent global growth investor, with participation from several existing investors. The company intends to utilize the newly secured capital to support its long-term growth strategy, which includes the acquisition of a third U.S. brewing facility and the continued expansion of its non-alcoholic beer offerings across global retail markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 20.9 Bn |

| Forecast Revenue (2034) | USD 37.8 Bn |

| CAGR (2025-2034) | 6.1 % |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Geopolitical Impacts, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Lager, Ale, Others), By Category (Plain, Flavored), By Production Method (Physical, Biological), By Packaging Type (Can, Bottles), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online) Age Group (18-25 Years, 26-35 Years, 36-45 Years, Above 46 Years), By End-User (Male, Female) |

| Regional Analysis | North America: The US and Canada; Europe: Germany, France, The UK, Italy, Spain, Russia & CIS, and the Rest of Europe; APAC: China, India, Japan, South Korea, ASEAN, and the Rest of APAC; Latin America: Brazil, Mexico, and Rest of Latin America; Middle East & Africa: GCC, South Africa, and Rest of Middle East & Africa. |

| Competitive Landscape | Bavarian State Brewery Weihenstephan, Anheuser-Busch InBev, Heineken N.V., Coors Brewing Company, BERNARD Family Brewery, a.s., Athletic Brewing Company, Moscow Brewing Company, Big Drop Brewing Pty Ltd, Carlsberg Breweries A/S, Bravus Brewing Company, Brooklyn Brewery, ERDINGER Weißbier, Krombacher Startseite, Swinkels Family Brewers and Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |