Quick Navigation

Report Overview

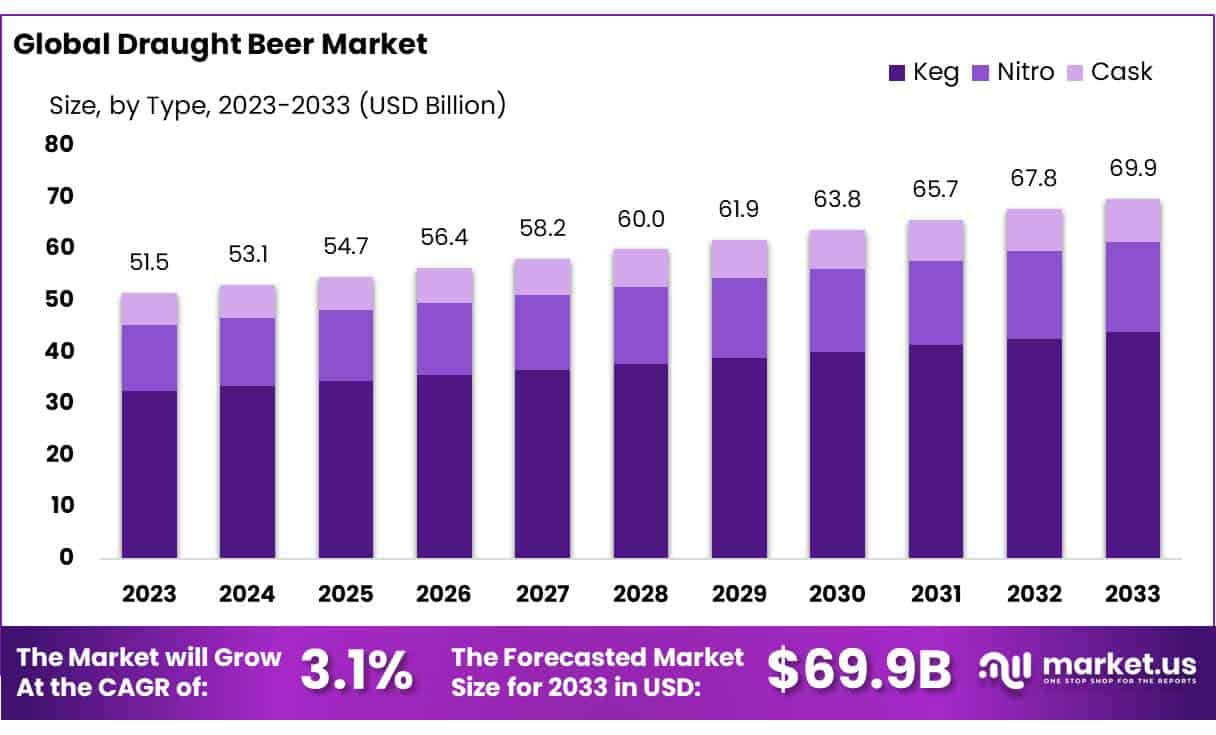

The Global Draught Beer Market size is expected to be worth around USD 69.9 Bn by 2033, from USD 51.5 Bn in 2023, growing at a CAGR of 3.1% during the forecast period from 2024 to 2033.

Draught beer, known for its fresh flavor and aroma, is typically served from a keg or cask rather than a bottle or can. Unlike bottled beer, draught beer avoids pasteurization and filtration, preserving the original taste and aromatic profile of the brew. This type of beer is served under pressure, usually with carbon dioxide or occasionally nitrogen, to maintain its carbonation and freshness.

Regulatory oversight, especially from the Alcohol and Tobacco Tax and Trade Bureau (TTB), is stringent for the draught beer industry. Any draught beer with an alcohol volume exceeding 0.5% must adhere to federal standards designed to ensure consumer safety and fair trade practices. These regulations are critical in maintaining the quality and safety of beer that reaches consumers.

The U.S. beer industry faces one of the highest levels of regulation among beverage sectors. There are approximately 125,212 regulations influencing beer production and distribution, with about 94,212 of these being federal regulations. These regulations significantly affect the supply chain and operational flexibility within the industry.

The intensity of these regulations varies significantly from state to state. For example, South Dakota has around 1,177 specific beer regulations, whereas California implements approximately 25,399 regulations. On average, each state has about 10,212 regulations affecting the beer industry. This extensive regulatory environment underscores the complexity and compliance burden placed on breweries across the nation.

Understanding these regulations is crucial for breweries as they navigate the complexities of production and distribution in the U.S. market. The impact of these regulations can influence everything from the production process to the marketing and sales of draught beer. As such, breweries must stay informed and compliant to operate successfully within this heavily regulated landscape.

Key Takeaways

- Draught Beer Market size is expected to be worth around USD 69.9 Bn by 2033, from USD 51.5 Bn in 2023, growing at a CAGR of 3.1%.

- Keg draught beer held a dominant market position, capturing more than a 63.4% share.

- Premium draught beer held a dominant market position, capturing more than a 54.5% share.

- Macro Breweries held a dominant market position, capturing more than a 73% share of the draught beer market.

- Lager held a dominant market position, capturing more than a 45.5% share of the draught beer market.

- Millennials held a dominant market position in the draught beer market, capturing more than a 50.4% share.

- Regular Alcohol draught beers held a dominant market position, capturing more than a 71.2% share.

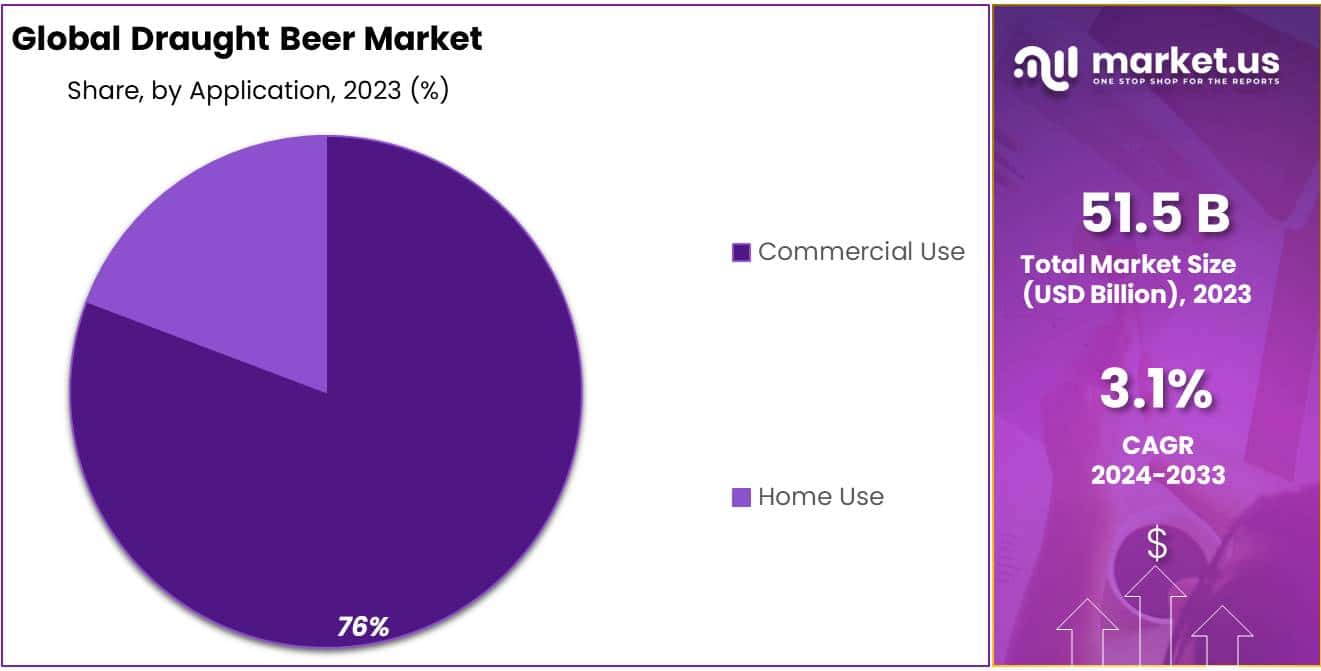

- Commercial Use held a dominant market position in the draught beer market, capturing more than a 76.3% share.

- On-Premise distribution channels for draught beer held a dominant market position, capturing more than a 63.4% share.

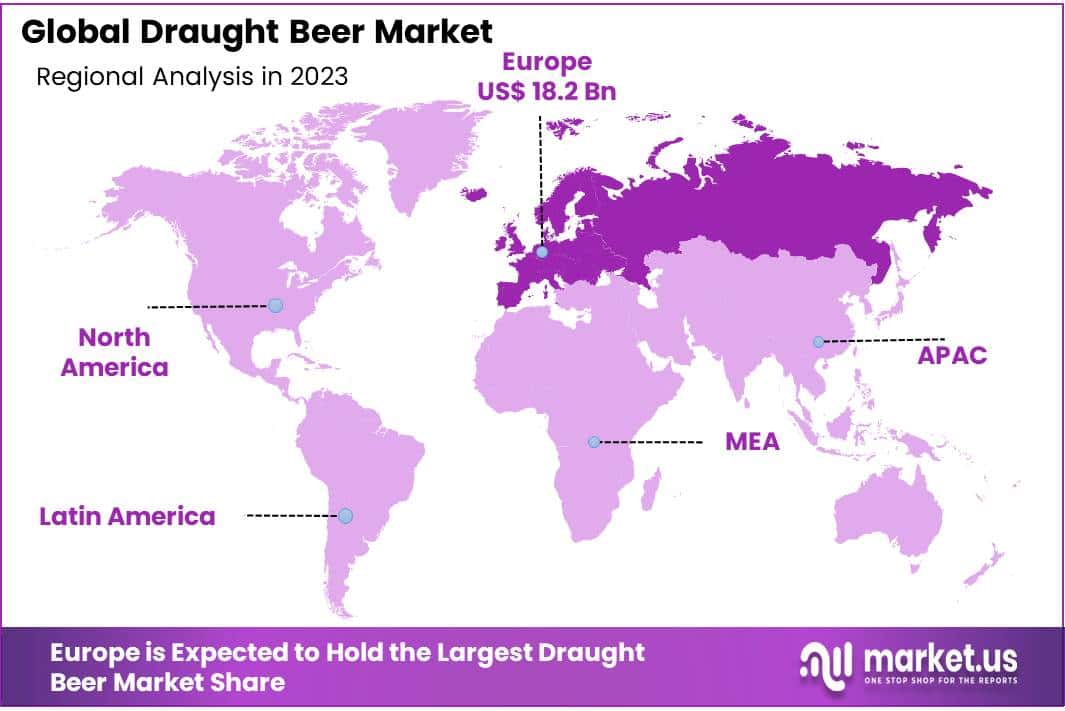

- Europe dominated the market, holding a substantial 45.3% share with a valuation of USD 18.2 billion.

By Type

In 2023, Keg draught beer held a dominant market position, capturing more than a 63.4% share. This popularity is largely due to the convenience and stability keg systems offer, allowing for consistent quality and flavor preservation over extended periods. Kegs, typically used with carbon dioxide or nitrogen, maintain the carbonation and aseptic conditions of the beer, making them a preferred choice for commercial venues such as pubs and restaurants.

Nitro draught beer, recognized for its smooth texture and rich creaminess, is served using nitrogen gas, which produces finer bubbles and a distinct mouthfeel compared to carbon dioxide. While it represents a smaller segment of the market, Nitro beer is gaining traction among consumers who appreciate its unique characteristics, especially in stouts and rich ales.

Cask, offers a traditional serving method where beer undergoes secondary fermentation in the cask and is served without additional nitrogen or carbon dioxide pressure. This type offers a more nuanced flavor profile and natural carbonation, appealing to purists and enthusiasts of traditional brewing. Despite its rich cultural heritage, cask beer holds a niche position in the market, cherished for its artisanal brewing and serving technique.

By Category

In 2023, Premium draught beer held a dominant market position, capturing more than a 54.5% share. This category benefits from a balanced blend of quality and affordability, making it a popular choice among a broad spectrum of consumers. Premium beers typically offer a step up in quality from regular beers without the high price tag of super premium options, appealing to consumers looking for better-tasting beers at reasonable prices.

Super Premium draught beers, although a smaller segment, are growing in popularity due to rising consumer interest in unique, high-quality brews. These beers are often characterized by their artisanal brewing methods and distinctive flavor profiles, catering to beer connoisseurs and those willing to pay a premium for exclusive products.

Regular draught beer remains a staple in many markets, appreciated for its accessibility and lower cost. This category caters to a large demographic that prioritizes affordability and traditional flavors, making it a key offering in many pubs and bars worldwide. While it doesn’t share the rapid growth of the premium categories, its established presence ensures continued relevance in the draught beer market.

By Production

In 2023, Macro Breweries held a dominant market position, capturing more than a 73% share of the draught beer market. This significant market share is attributed to their large-scale production capabilities and widespread distribution networks, which enable them to meet high demand efficiently and maintain consistent quality across extensive product lines.

Macro breweries typically produce a variety of beer styles at high volumes, catering to a broad consumer base with recognizable brands and competitive pricing.

Microbreweries, while holding a smaller portion of the market, are steadily increasing their presence, driven by consumer interest in diverse, locally crafted beers with unique flavors and brewing methods.

Microbreweries focus on quality, artisanal products, and often engage more directly with their customers through community-focused activities and limited-edition releases. This segment appeals particularly to enthusiasts looking for innovative and regionally distinct brews, contributing to a rich and varied beer culture.

By Product Type

In 2023, Lager held a dominant market position, capturing more than a 45.5% share of the draught beer market. Lagers are favored for their crisp and refreshing taste, achieved through bottom-fermentation at cooler temperatures, which makes them a popular choice across various demographics and drinking occasions. This category’s widespread appeal is bolstered by both major and craft breweries that offer a range of lagers from light and pale to dark and robust, catering to a broad taste spectrum.

Ale, another significant category, is known for its robust flavors and aromatic profiles, driven by top-fermentation at warmer temperatures. Ales include a variety of subtypes such as pale ale, brown ale, and Belgian ale, each offering distinct tastes and experiences. This diversity makes ales a favorite among beer enthusiasts looking for complexity and richness in their beer choices.

Stout, renowned for its dark, thick, and creamy texture, is another notable segment within the draught beer market. Stouts often feature roasted malt or barley, giving them a characteristic coffee-like taste that appeals to those who appreciate a fuller-bodied beer.

Pilsner, a type of pale lager, offers a golden hue and a clear, crisp taste with a slight bitterness from the hops. This beer type is highly regarded for its balanced flavor and is especially popular in European countries as well as in the U.S.

Wheat Beer, made with a significant proportion of wheat, provides a lighter, refreshing taste with hints of fruit and spice. This beer type is often served with a slice of lemon or orange to enhance its naturally bright and tangy flavors, making it particularly popular in warmer climates.

By Consumer Demographics

In 2023, Millennials held a dominant market position in the draught beer market, capturing more than a 50.4% share. This demographic’s preference for diverse and premium beverage options has significantly shaped the industry, with Millennials often seeking out craft beers for their authenticity and variety. Their demand for innovative flavors and sustainable brewing practices has prompted breweries to adapt and innovate continuously.

Generation X, while holding a smaller market share compared to Millennials, still represents a substantial segment of the draught beer market. Members of Generation X tend to value quality over quantity and are likely to spend on higher-end products. This group’s brand loyalty and preference for established beer brands have helped maintain a steady demand within this demographic.

Baby Boomers, known for their traditional preferences, tend to stick with classic beer styles and brands. Although their market share is less than that of Millennials, Baby Boomers contribute to the market’s stability with their consistent purchasing habits. They are less influenced by trends but are an important demographic due to their purchasing power and preference for dining out, where draught beer is a common choice.

By Alcohol Content

By Distribution Channel

In 2023, On-Premise distribution channels for draught beer held a dominant market position, capturing more than a 63.4% share. This segment primarily includes bars, pubs, restaurants, and breweries where draught beer is served directly to consumers. The preference for on-premise consumption is driven by the fresh quality and social experience that these settings offer, making them popular spots for enjoying draught beer. Additionally, the atmosphere and live service enhance the overall consumer experience, further solidifying the popularity of on-premise venues.

Off-Premise distribution includes retail stores like liquor shops and supermarkets where consumers purchase draught beer to consume at home or other locations. Although smaller than the on-premise segment, it benefits from the convenience and variety it offers, allowing consumers to enjoy a wide range of draught beers outside of traditional social settings.

eCommerce, while the smallest segment, is rapidly growing as technology and consumer behavior shift towards online shopping. This channel has been significantly boosted by improvements in logistics that allow for the efficient delivery of draught beer kegs and mini-kegs to consumers, catering to the rising demand for home consumption. As more consumers become accustomed to online shopping, the eCommerce channel is expected to expand, offering a broader selection and more accessibility to premium and craft draught beers.

Key Market Segments

By Type

- Keg

- Nitro

- Cask

By Category

- Super Premium

- Premium

- Regular

By Production

- Macro Breweries

- Microbreweries

By Product Type

- Lager

- Ale

- Stout

- Pilsner

- Wheat Beer

By Consumer Demographics

- Millennials

- Generation X

- Baby Boomers

By Alcohol Content

- Low Alcohol

- Regular Alcohol

- High Alcohol

By End Use

- Commercial Use

- Home Use

By Distribution Channel

- On-Premise

- Off-Premise

- eCommerce

Drivers

Growing Consumer Demand for Craft and Specialty Beers

There is a noticeable shift towards craft and specialty beers, which offer unique flavors and artisanal quality compared to mass-produced varieties. This shift is particularly strong in regions like Asia Pacific, where consumers are increasingly drawn to diverse and flavorful beer options due to the influence of Western culture and lifestyle trends.

Strategic Expansions and Innovations

Major beer companies are continuously expanding their product lines and entering new markets to cater to the growing demand for draught beer. For instance, Budweiser APAC recently inaugurated a new craft brewery in China, focusing on producing high-quality craft beers to meet regional consumer demands. Such expansions not only enhance production capabilities but also broaden the reach in both established and emerging markets.

Government Regulations and Market Adaptations

The draught beer market is heavily influenced by regulatory frameworks that vary significantly across different regions. In the Middle East, recent regulatory changes have allowed for more liberalized alcohol production and consumption, which is expected to boost the local draught beer market.

For example, new licenses permitting the fermentation of alcoholic beverages for on-site consumption in Abu Dhabi have opened up opportunities for microbreweries and craft beer ventures.

Economic Impact and Employment

The beer industry, including draught beer, plays a significant role in the U.S. economy, contributing billions in wages and supporting hundreds of thousands of jobs across its supply chain. The industry’s economic activity is vast, encompassing everything from production.

Restraints

Regulatory and Taxation Challenges

Regulations and taxes are major hurdles for the draught beer industry. High excise duties on alcohol can increase the cost to the consumer, potentially reducing demand. Furthermore, in regions like Europe, the variation in regulations across countries adds an additional layer of complexity for breweries operating internationally.

Market Saturation and High Competition

The draught beer market is becoming increasingly saturated, especially in mature markets such as the U.S. and Europe, where there are a vast number of brands competing for market share. This saturation makes it challenging for new entrants and can limit the growth potential of existing players.

Economic Uncertainties

Economic downturns and fluctuations can also significantly impact consumer spending on non-essential goods, including draught beer. During economic recessions, consumers tend to limit their spending on dining out and luxury items, directly affecting sales in bars and pubs where draught beer is a significant revenue generator.

Consumer Preferences Shifting

There’s also a growing trend towards healthier lifestyles, which can impact alcoholic beverage sales. Increasing health consciousness has led some consumers to reduce their alcohol consumption, seeking out non-alcoholic or low-alcohol alternatives instead.

Technological and Logistical Constraints

Finally, the need for specific infrastructure to store and serve draught beer (such as kegging systems and tap setups) can be a barrier, particularly for establishments with limited space or resources. Maintaining the quality of draught beer from brewery to bar requires precise technology and logistics, which can be a significant investment for new entrants or smaller players in the market.

Opportunity

Emphasis on Craft and Premium Beers

The craft beer movement has significantly influenced the draught beer market, with a growing number of consumers preferring craft beers for their authenticity and diverse flavors. This trend is particularly strong in regions like North America and Europe, where there is a deep cultural appreciation for craft beers.

Technological Advancements in Brewing and Dispensing

Advances in brewing technology and the development of sophisticated home draught systems are making it easier for consumers to enjoy high-quality draught beer at home. This is complemented by a rise in home entertainment, where draught beer plays a central role, offering growth potential for equipment manufacturers and beer brands alike.

Expansion in Emerging Markets

Emerging markets present new opportunities for growth, particularly in Asia Pacific and Latin America, where the increasing middle-class population and urbanization are driving the demand for premium alcoholic beverages. The expanding economic capabilities of these regions make them attractive markets for new and existing players in the draught beer industry.

Leveraging Local Ingredients and Sustainability

There is also a significant opportunity in leveraging local ingredients and sustainable practices in beer production, which appeals to the environmentally conscious consumer. This approach not only enhances brand image and consumer loyalty but also aligns with global trends towards sustainability in consumer goods.

Trends

Rise of Craft and Specialty Beers

Consumers’ growing interest in artisanal and specialty beers is evident, with a significant shift towards products that offer unique taste profiles and a sense of exclusivity. This trend is supported by an increase in disposable incomes, allowing more consumers to choose premium products.

Technological Innovations in Brewing

The draught beer market is also experiencing technological advancements in brewing and dispensing, enhancing the overall quality and consumer experience. Innovations such as Nitro draught systems, which infuse nitrogen to create a smoother and creamier texture, and advanced kegging systems that ensure optimal freshness, are becoming more prevalent. These technologies not only improve the sensory experience of draught beer but also increase operational efficiency for breweries and pubs.

Increasing Social and Dining Out Trends

The trend of socializing and dining out is another driving factor for the draught beer market. As more people enjoy social gatherings, sports events, and dining at pubs and restaurants, the demand for draught beer continues to grow. This social aspect is crucial for draught beer, as it is often consumed in environments that enhance its appeal, such as bars and beer gardens.

Sustainability and Eco-Friendly Practices

Sustainability is becoming increasingly important in the draught beer market. Many breweries are adopting eco-friendly practices, including using sustainable ingredients and implementing energy-efficient brewing processes. These practices not only appeal to environmentally conscious consumers but also help breweries reduce operational costs and comply with regulatory standards

Regional Analysis

In the draught beer market, regional dynamics significantly influence consumer preferences and market growth. In 2023, Europe dominated the market, holding a substantial 45.3% share with a valuation of USD 18.2 billion. This strong market presence is largely attributed to Europe’s rich brewing traditions and the high popularity of pub cultures in countries such as Germany, the UK, and Belgium. Additionally, European consumers tend to favor premium and artisanal beers, which supports a thriving market for both local and imported draught beers.

North America also represents a significant portion of the draught beer market, driven by a robust craft beer scene and a culture that appreciates diverse beer varieties. The U.S. and Canada are notable for their innovative brewing techniques and the widespread establishment of microbreweries, which cater to an ever-growing audience of craft beer enthusiasts.

In Asia Pacific, the draught beer market is rapidly expanding, driven by rising disposable incomes and the increasing westernization of dining experiences, especially in countries like China, Japan, and India. This region shows great potential for growth as local breweries begin to embrace craft beer trends, merging them with local flavors and preferences.

The Middle East & Africa, and Latin America regions, though smaller in market size compared to Europe, North America, and Asia Pacific, are experiencing gradual growth in draught beer consumption. This growth is spurred by urbanization, the expansion of the middle class, and the younger demographics’ increasing exposure to global beverage trends. Both regions are expected to increase their market share as they continue to develop economically and as global brewers invest in these markets to tap into new consumer bases.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The draught beer market is characterized by a mix of global giants and prominent regional players that shape industry trends through innovation, strategic mergers, acquisitions, and expansions. Key players like Anheuser-Busch InBev, Heineken International B.V., and Carlsberg Group dominate on a global scale due to their extensive portfolio of brands, massive production capabilities, and vast distribution networks. These companies have been instrumental in popularizing draught beer across various continents, capitalizing on their established market presence and brand loyalty among consumers.

Other significant contributors include Asahi Group Holdings, Ltd. and Molson Coors Beverage Company, which have strengthened their market positions through strategic acquisitions and by expanding their product lines to include craft and specialty beers, catering to the growing consumer demand for premium and unique beer experiences.

Companies like The Boston Beer Company and New Belgium Brewing Company represent the craft segment within the market, emphasizing quality ingredients and artisanal brewing techniques, which resonate with today’s consumer preference for authenticity and flavor diversity.

Moreover, regional players such as Anadolu Efes and China Resources Snow Breweries leverage local consumer insights to cater to specific tastes and preferences in their respective markets, helping to drive the growth of the draught beer sector regionally. The presence of these key players not only intensifies the competition but also encourages continuous innovation within the industry, ensuring that consumer needs for variety and quality are met.

Top Key Players in the Market

- Anadolu Efes

- AnheuserBusch InBev

- Asahi Group Holdings, Ltd.

- Boston Beer Company

- Carlsberg Group

- Castel Frères

- China Resources Snow Breweries

- Constellation Brands, Inc.

- Crown Imports

- Diageo

- Dogfish Head Craft Brewery

- G. Yuengling Son

- Gold Star

- Groupé Castel

- Grupo Petrópolis

- Heineken International B.V.

- Lagunitas Brewing Company

- Molson Coors Beverage Company

- New Belgium Brewing Company

- Pabst Brewing Company

- Red Bull GmbH

- SABMiller

- The Boston Beer Company

Recent Developments

In 2023 Anadolu Efes continued to innovate and adapt. The company’s financial health appeared stable with an increase in net income, signifying a 43.8% rise year-over-year, and substantial growth in free cash flow, which saw a 203.4% increase.

In 2023 Anheuser-Busch InBev (AB InBev), a leading force in the global draught beer market, demonstrated resilience and strategic growth.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 51.5 Bn |

| Forecast Revenue (2033) | USD 69.9 Bn |

| CAGR (2024-2033) | 3.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Keg, Nitro, Cask), By Category (Super Premium, Premium, Regular), By Production (Macro Breweries, Microbreweries), By Product Type (Lager, Ale, Stout, Pilsner, Wheat Beer), By Consumer Demographics (Millennials, Generation X, Baby Boomers), By Alcohol Content (Low Alcohol, Regular Alcohol, High Alcohol), By End Use (Commercial Use, Home Use), By Distribution Channel ( On-Premise, Off-Premise, eCommerce) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Anadolu Efes, AnheuserBusch InBev, Asahi Group Holdings, Ltd., Boston Beer Company, Carlsberg Group, Castel Frères, China Resources Snow Breweries, Constellation Brands, Inc., Crown Imports, Diageo, Dogfish Head Craft Brewery, G. Yuengling Son, Gold Star, Groupé Castel, Grupo Petrópolis, Heineken International B.V., Lagunitas Brewing Company, Molson Coors Beverage Company, New Belgium Brewing Company, Pabst Brewing Company, Red Bull GmbH, SABMiller, The Boston Beer Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |