Quick Navigation

Report Overview

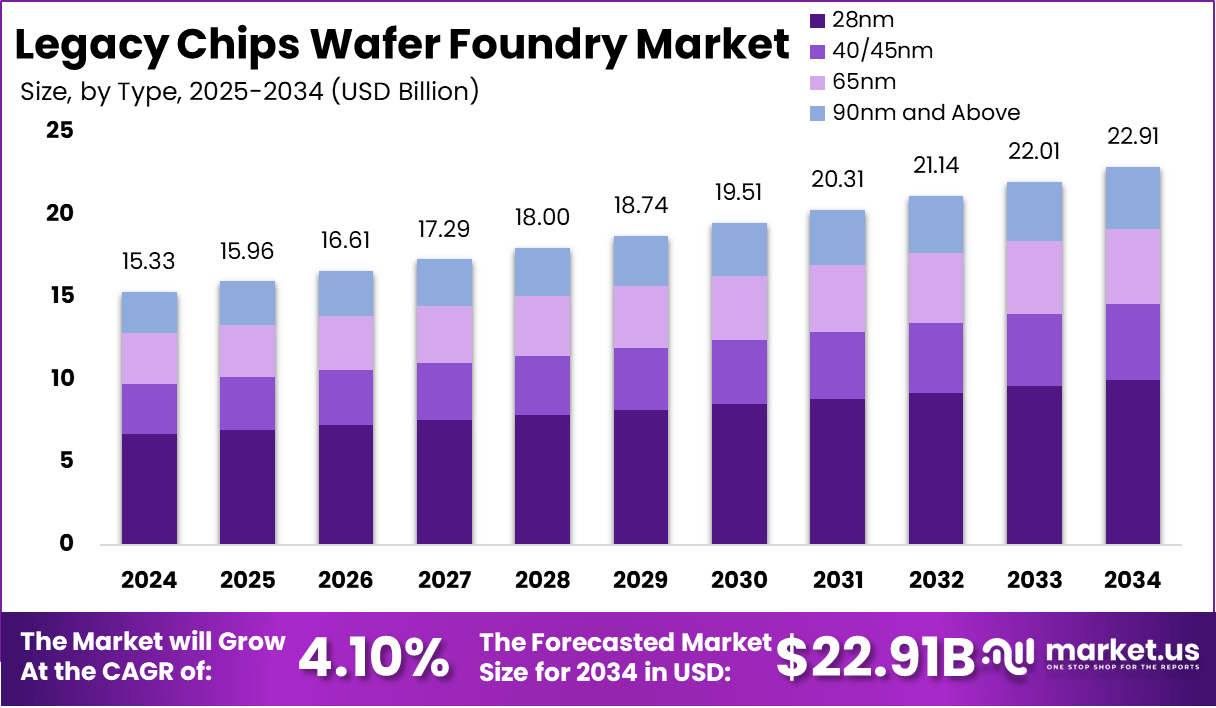

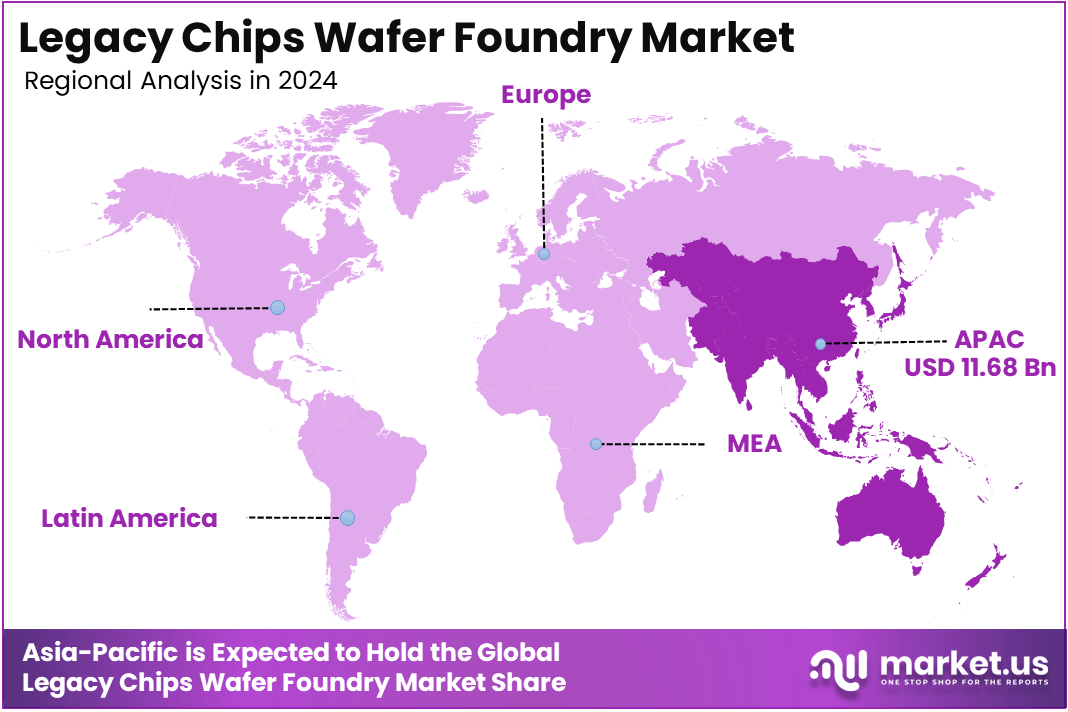

The Global Legacy Chips Wafer Foundry Market size is expected to be worth around USD 22.91 Billion By 2034, from USD 15.33 Billion in 2024, growing at a CAGR of 4.10% during the forecast period from 2025 to 2034. In 2024, Asia-Pacific held a dominant market position, capturing more than a 76.2% share, holding USD 11.68 Billion in revenue.

A legacy chips wafer foundry is a semiconductor manufacturing facility specializing in producing mature-node integrated circuits (ICs) on older process technologies, typically ranging from 90nm to 350nm. These foundries focus on producing chips that, while not utilizing the latest fabrication processes, remain essential for various applications due to their cost-effectiveness and sufficient performance.

Legacy chips are integral to numerous industries, including automotive, industrial machinery, consumer electronics, and medical devices, where advanced processing capabilities are not always necessary. The production of these chips involves established manufacturing techniques, making them more accessible and affordable compared to cutting-edge semiconductors.

Key Statistics

Production and Demand

- Total production of legacy chips is projected to grow significantly, with a focus on nodes larger than 28nm.

- China accounted for approximately 31% of global legacy chip production by the end of 2023, expected to increase to 39% by 2027.

Usage Statistics

- The production of integrated circuits (ICs) in China reached 395.3 billion units in the first eleven months of 2024, with a year-on-year growth of 23.1%.

- Exports of ICs from China were valued at nearly $145 billion, marking an increase of 18.8% from the previous year.

Import and Export Data

- China imported around 501.47 billion ICs in 2024, valued at approximately $349 billion, reflecting a year-on-year increase of 14.8%.

- Major export destinations for Chinese ICs include Hong Kong, South Korea, Taiwan, Vietnam, and Malaysia.

Lifecycle and Quantity

- The lifecycle of legacy chips typically spans several years due to their application in automotive electronics, industrial machinery, and household appliances.

- Europe faces a supply gap projected at 12.7 million wafers per year by 2030, necessitating imports of at least 8.2 million wafers annually to meet demand.

Regional Production Insights

- North America and Asia are significant players in the legacy chip manufacturing landscape.

- Planned fabrication plants in the EU are expected to produce only 4.5 million wafers per year, highlighting the need for additional capacity to meet local demand.

The legacy chips wafer foundry market encompasses the global industry dedicated to the production of mature-node semiconductors. Despite the rapid advancement of technology and the shift towards smaller process nodes, the demand for legacy chips remains robust.

These semiconductors are crucial for applications where high performance is not the primary requirement, such as in automotive control systems, industrial automation, home appliances, and certain consumer electronics.

The market is characterized by a diverse range of players, including established foundries and specialized manufacturers focusing on mature-node processes. The ongoing need for these chips ensures a steady demand, even as the industry progresses towards more advanced technologies.

The legacy chips wafer foundry market is primarily driven by cost-effectiveness, as mature-node semiconductors are less expensive to produce compared to the latest cutting-edge chips. This makes them ideal for applications where high performance is not the primary requirement, such as in automotive control systems, industrial machinery, and consumer electronics.

Another key factor is the well-established manufacturing processes that ensure stable and reliable production, further strengthening the market demand. Additionally, the long lifecycle of certain industries, such as the automotive and industrial sectors, creates a continued need for these chips, as these industries rely on legacy technology that does not require the latest innovations but must be dependable and available for extended periods.

Key Takeaways

- Market Value Growth: The legacy chips wafer foundry market is projected to grow from USD 15.33 billion in 2024 to USD 22.91 billion by 2034, reflecting steady market expansion.

- CAGR: The market is expected to grow at a Compound Annual Growth Rate (CAGR) of 4.10% over the next decade.

- By Process Node – 28nm: The 28nm process node dominates the market, accounting for 43.6% of the total market share due to its balanced performance and cost-effectiveness for many applications.

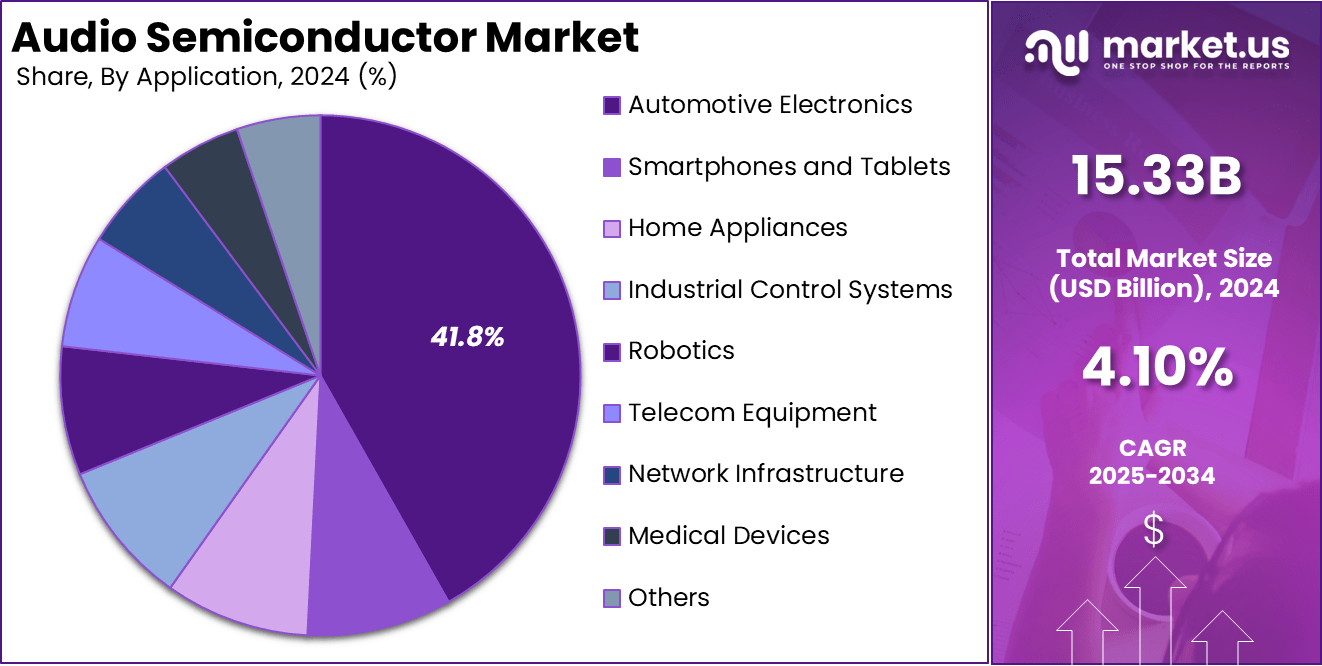

- By Application – Automotive Electronics: Automotive electronics are the leading application segment, representing 41.8% of the legacy chips wafer foundry market, driven by the increasing demand for semiconductors in automotive control systems, infotainment, and safety features.

- Regional Dominance – Asia Pacific: The Asia Pacific region holds the largest market share, contributing 76.2% of the global legacy chips wafer foundry market, supported by a strong semiconductor manufacturing base and high demand from key industries in the region.

- Steady Growth Potential: The market shows consistent growth potential, driven by ongoing demand for affordable, reliable legacy chips in sectors like automotive, industrial, and consumer electronics.

Regional Analysis

In 2024, Asia-Pacific held a dominant market position, capturing more than a 76.2% share, holding USD 11.68 billion in revenue. This dominant position is largely driven by the region’s strong semiconductor manufacturing infrastructure, which includes some of the world’s largest foundries located in countries like China, Taiwan, Japan, and South Korea.

These countries play a crucial role in the global semiconductor supply chain, with a heavy focus on legacy chips that are used across multiple industries, including automotive, industrial, and consumer electronics.

Asia-Pacific’s significant share of the legacy chips wafer foundry market is also fueled by the booming automotive sector in the region. With the rise of automotive electronics, such as advanced driver-assistance systems (ADAS) and infotainment, the demand for reliable and cost-effective legacy chips continues to increase.

Additionally, many industrial applications, including factory automation and robotics, rely on these semiconductors, further strengthening the demand in the region. The region’s leadership is also attributed to the lower production costs associated with semiconductor manufacturing in countries like China and Taiwan, which allows legacy chips to be produced efficiently.

Furthermore, Asia-Pacific benefits from large-scale production and high-volume manufacturing capabilities, which allow for the continued supply of legacy chips at competitive prices, driving their adoption across multiple sectors. Given these factors, Asia-Pacific is poised to maintain its dominant position in the legacy chips wafer foundry market well into the future.

By Process Node

In 2024, the 28nm segment held a dominant market position, capturing more than a 43.6% share due to its balanced performance, cost-effectiveness, and wide applicability in various industries. The 28nm process node has become the preferred choice for manufacturing legacy chips as it offers a good compromise between power efficiency, performance, and cost.

These chips are used in a variety of applications, including automotive electronics, industrial control systems, and consumer electronics, where advanced performance is not as critical as in cutting-edge technologies. The 28nm node is particularly favored in automotive applications, which require high reliability and long product lifecycles, making it well-suited for legacy semiconductor manufacturing.

Furthermore, the 28nm process node benefits from established production capabilities, making it a go-to solution for legacy chip manufacturers looking to meet the growing demand for these semiconductors in cost-sensitive sectors.

It also remains compatible with many older systems, providing continuity for industries that continue to rely on mature-node technologies. As the demand for reliable, cost-effective semiconductors remains steady, the 28nm process node is expected to continue its dominant role in the legacy chips wafer foundry market.

By Application

In 2024, the Automotive Electronics segment held a dominant market position, capturing more than a 41.8% share of the legacy chips wafer foundry market. This dominance is primarily due to the increasing reliance on semiconductors in automotive applications, particularly for advanced driver-assistance systems (ADAS), in-car entertainment, and safety features.

Automotive electronics require highly reliable and long-lasting chips, making legacy nodes like 28nm and 40nm ideal for these applications. As vehicles become more connected and feature-rich, the demand for automotive semiconductors continues to grow.

The automotive industry also benefits from the steady supply and lower production costs associated with legacy chips, making them an attractive option for manufacturers. Additionally, the extended lifespan of automotive products aligns well with the longevity of legacy chips, making them a perfect fit for this sector.

As the push for electric vehicles (EVs) and autonomous driving systems continues to grow, the demand for reliable and cost-efficient semiconductor solutions in the automotive sector is expected to increase, allowing the automotive electronics segment to retain its dominant position in the legacy chips wafer foundry market.

Key Market Segments

By Process Node

- 28nm

- 40/45nm

- 65nm

- 90nm and Above

By Application

- Smartphones and Tablets

- Home Appliances

- Automotive Electronics

- Industrial Control Systems

- Robotics

- Telecom Equipment

- Network Infrastructure

- Medical Devices

- Others

Driving Factors

Geopolitical Tensions and Supply Chain Diversification

Geopolitical tensions, particularly between the United States and China, have significantly influenced the legacy chips wafer foundry market. The U.S. has implemented export controls on advanced semiconductor technologies to China, aiming to curb China’s technological advancements.

In response, China has accelerated its efforts to develop domestic semiconductor manufacturing capabilities, including the production of legacy chips. This shift has led to increased competition in the global market, as Chinese foundries expand their production capacity and market share.

For instance, Chinese foundries have increased their global market share in mature nodes from 14% in 2017 to 18% in 2023. This growth poses a challenge to Western semiconductor manufacturers, who may face increased competition in both domestic and international markets. Additionally, the U.S. strategy of focusing on restricting advanced technology may need to adapt as the chip conflict pervades other sectors, including legacy chips.

Restraining Factors

Supply Chain Disruptions

The legacy chips wafer foundry market faces significant challenges due to supply chain disruptions. The COVID-19 pandemic exposed vulnerabilities in global supply chains, leading to shortages of essential components and raw materials. These disruptions have affected the production schedules of foundries, causing delays and increased costs.

For example, the semiconductor industry has experienced shortages of critical materials like silicon wafers and rare earth metals, which are essential for chip manufacturing. These shortages have led to increased production costs and longer lead times for customers.

Furthermore, geopolitical tensions have exacerbated these supply chain issues. Trade restrictions and tariffs have disrupted the flow of materials and components across borders, leading to increased costs and uncertainty in the supply chain. For instance, the U.S.-China trade war has resulted in tariffs on semiconductor manufacturing equipment and materials, affecting the cost structures of foundries.

Growth Opportunities

Expansion into Emerging Markets

The growing demand for consumer electronics in emerging markets presents a significant growth opportunity for the legacy chips wafer foundry market. As disposable incomes rise in regions such as Southeast Asia, Africa, and Latin America, there is an increasing demand for affordable electronic devices like smartphones, home appliances, and automotive electronics.

These devices often rely on legacy chips due to their cost-effectiveness and sufficient performance for basic functionalities. For example, the adoption of smartphones in Africa has been accelerating, with millions of new users joining the mobile ecosystem annually.

These smartphones typically utilize legacy chips, creating a substantial market for foundries specializing in mature-node semiconductors. Similarly, the automotive industry in Southeast Asia is expanding, with a growing number of vehicles incorporating electronic systems that depend on legacy chips.

Challenging Factors

Technological Advancements in Advanced Nodes

The rapid advancement of semiconductor manufacturing technologies presents a challenge for the legacy chips wafer foundry market. As the industry moves towards smaller process nodes, such as 5nm and 3nm, the demand for legacy chips may decline, leading to reduced production volumes and profitability for foundries specializing in mature-node semiconductors.

For instance, major semiconductor companies are investing heavily in advanced manufacturing technologies to produce cutting-edge chips for applications like artificial intelligence and high-performance computing. This shift in focus toward advanced nodes can lead to a decrease in the availability of legacy chips, as foundries allocate resources to more profitable advanced node production.

Growth Factors

The legacy chips wafer foundry market is experiencing significant growth, driven by several key factors:

Rising Demand for Consumer Electronics: The global surge in consumer electronics, including smartphones, home appliances, and automotive electronics, has significantly increased the demand for legacy chips.

Automotive Industry Expansion: The automotive sector’s rapid adoption of electronic systems, such as advanced driver-assistance systems (ADAS) and infotainment, has bolstered the demand for legacy chips.

Cost-Effectiveness of Legacy Chips: Manufacturing legacy chips is more cost-effective compared to advanced-node semiconductors, making them attractive for applications where high performance is not critical. This cost advantage has led to increased adoption across various industries.

Emerging Trends

Several emerging trends are shaping the legacy chips wafer foundry market:

Geopolitical Shifts: The U.S.-China trade tensions have led to increased investments in domestic semiconductor manufacturing. For example, the U.S. Department of Commerce announced $1.5 billion in funding for GlobalFoundries to expand manufacturing capacity for essential chips.

Supply Chain Diversification: Companies are diversifying their supply chains to mitigate risks associated with geopolitical tensions and natural disasters. This strategy, known as “friend-shoring,” involves relocating manufacturing to politically stable regions.

Technological Advancements: While focusing on mature-node processes, foundries are implementing process optimizations to enhance efficiency and yield, ensuring the continued relevance of legacy chips.

Business Benefits

Engaging in the legacy chips wafer foundry market offers several business benefits:

Stable Revenue Streams: The consistent demand for legacy chips across various industries provides foundries with stable and predictable revenue streams. For instance, the automotive electronics segment alone accounted for 41.8% of the market share in 2024.

Lower Capital Investment: Manufacturing legacy chips requires less capital investment compared to advanced-node semiconductors, allowing companies to achieve quicker returns on investment.

Market Penetration: By focusing on legacy chips, foundries can penetrate less competitive markets, such as the automotive and industrial sectors, where the demand for advanced technology is lower.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

TSMC, established in 1987, has solidified its position as a global leader in semiconductor manufacturing. In 2024, TSMC announced plans to build a semiconductor fabrication plant in Arizona, USA, with production expected to commence in 2025. This strategic move aims to bolster TSMC’s presence in the U.S. market and align with the U.S. government’s efforts to enhance domestic semiconductor production.

Samsung Foundry, a division of Samsung Electronics, has been a significant player in the semiconductor manufacturing industry. In 2024, Samsung secured an order from Japanese AI firm Preferred Networks to produce AI application chips using its advanced 2-nanometer foundry process. This collaboration highlights Samsung’s commitment to advancing semiconductor technologies and meeting the evolving needs of the AI industry.

GlobalFoundries, established in 2009, has been a key player in the semiconductor manufacturing industry. In 2023, the company opened a $4 billion semiconductor fabrication plant in Singapore, aiming to expand its production capacity and serve the growing demand for semiconductors in the Asia-Pacific region.

Top Key Players in the Market

- TSMC

- Samsung Foundry

- GlobalFoundries

- United Microelectronics Corporation (UMC)

- SMIC

- Tower Semiconductor

- PSMC

- VIS (Vanguard International Semiconductor)

- Huahong Group

- Nexchip

- Other Major Players

Recent Developments

- In December 2024, President Joe Biden announced the launch of a Section 301 investigation into Chinese-manufactured legacy semiconductors. This move aims to assess potential risks to national security and critical infrastructure posed by China’s dominance in the legacy chip market.

- In December 2024, the U.S. Commerce Department finalized a $406 million grant to Taiwan’s GlobalWafers. This funding supports the expansion of silicon wafer production in the United States, focusing on projects in Texas and Missouri.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 15.33 Bn |

| Forecast Revenue (2034) | USD 22.91 Bn |

| CAGR (2025-2034) | 4.10% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Process Node (28nm, 40/45nm, 65nm, 90nm, and Above), By Application (Smartphones and Tablets, Home Appliances, Automotive Electronics, Industrial Control Systems, Robotics, Telecom Equipment, Network Infrastructure, Medical Devices, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | TSMC, Samsung Foundry, GlobalFoundries, United Microelectronics Corporation (UMC), SMIC, Tower Semiconductor, PSMC, VIS (Vanguard International Semiconductor), Huahong Group, Nexchip, Other Major Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |