Quick Navigation

Report Overview

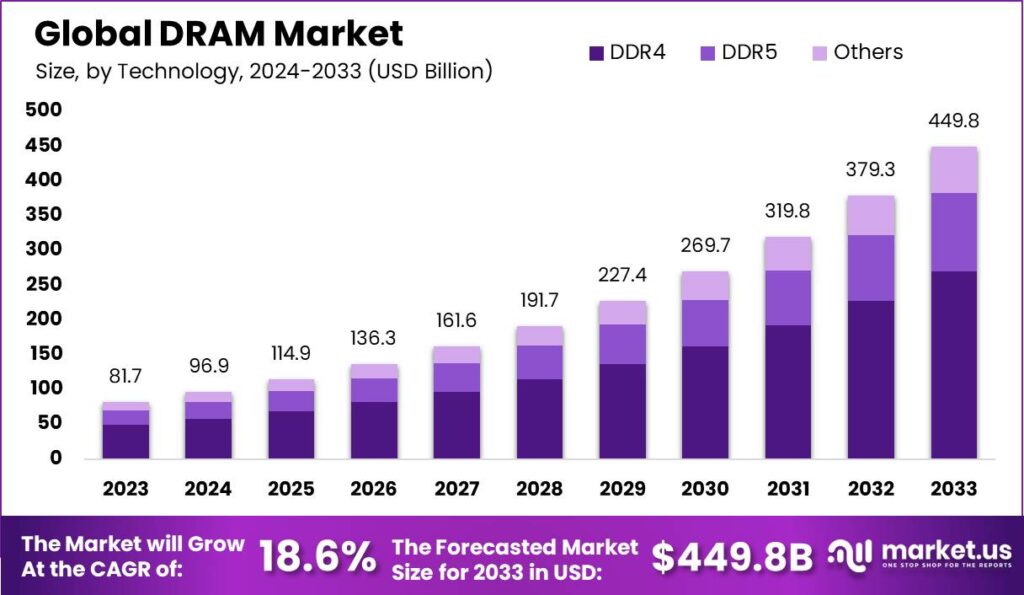

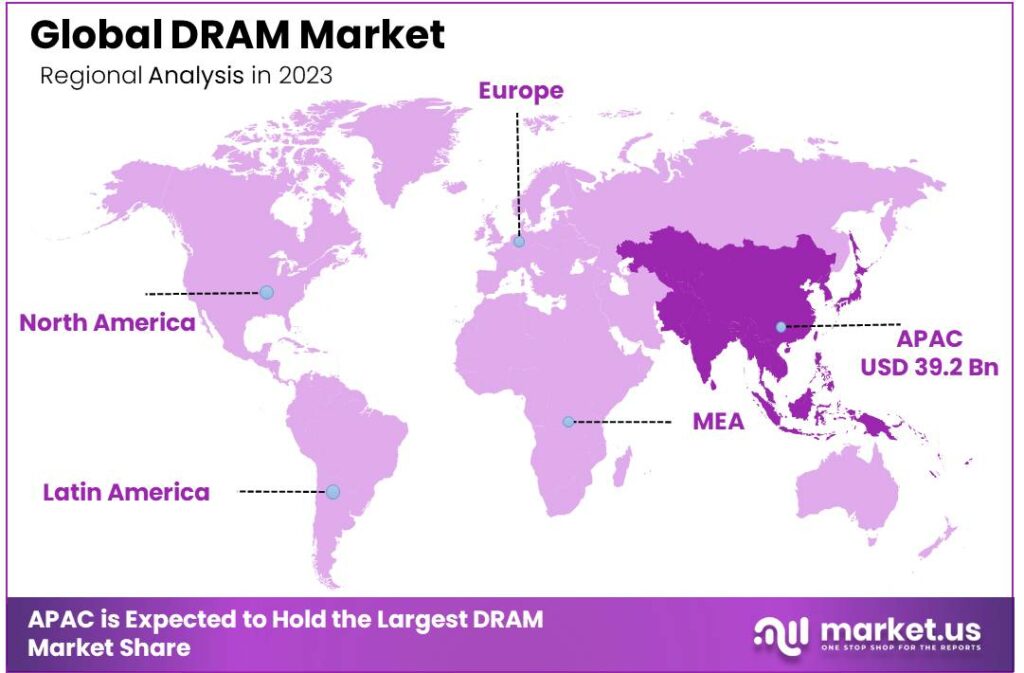

The Global DRAM Market size is expected to be worth around USD 449.8 Billion By 2033, from USD 81.69 Billion in 2023, growing at a CAGR of 18.60% during the forecast period from 2024 to 2033. In 2023, the Asia-Pacific (APAC) region dominated the global DRAM market, accounting for over 48% of the total market share. This dominance resulted in a revenue of approximately USD 39.2 billion.

Dynamic Random Access Memory, commonly known as DRAM, is a type of memory used in various computing devices for storing data temporarily. This technology is essential for facilitating quick access and processing of data by CPUs, GPUs, and other processors. Unlike other types of memory, DRAM needs to be refreshed periodically to maintain the data stored in it. This characteristic enables it to offer rapid read and write speeds, crucial for high-performance computing environments.

The DRAM market is a dynamic sector within the electronics industry, characterized by its cyclical demand patterns influenced by new technology rollouts and economic shifts. It’s a competitive field dominated by a few key players who manage large-scale manufacturing facilities capable of substantial output. The market’s performance is closely tied to the production strategies and technological enhancements introduced by these leading manufacturers.

The primary driving force behind the DRAM market’s growth is the increasing demand for faster computing by both individual consumers and large enterprises. As more devices become interconnected and data-intensive applications like cloud computing and artificial intelligence gain traction, the need for DRAM with higher speed and greater capacity expands.

Currently, the demand for DRAM is surging due to the rapid growth in technology sectors such as smartphones, PCs, and data centers. Each new generation of smartphones and computers offers more power and functionality, which in turn requires more memory. This trend is likely to continue as technology evolves, keeping the demand for DRAM robust in the foreseeable future.

There are significant opportunities in the DRAM market, especially in areas involving emerging technologies. The expansion of IoT (Internet of Things) devices, which rely on real-time processing, presents a growing market for DRAM modules. Furthermore, as countries and companies invest more in developing smart infrastructure and autonomous vehicles, the need for high-performance memory will escalate, offering ample opportunities for DRAM manufacturers.

Technological innovation is a cornerstone of the DRAM industry. Recent advancements include the development of 3D stacking technology, which allows for multiple layers of memory cells to be stacked vertically, greatly increasing the density and speed of memory chips. Manufacturers are also exploring new types of memory that can offer the speed of DRAM with the non-volatility of flash storage, potentially revolutionizing the market with hybrid memory solutions that could offer the best of both worlds.

Key Takeaways

Type Analysis

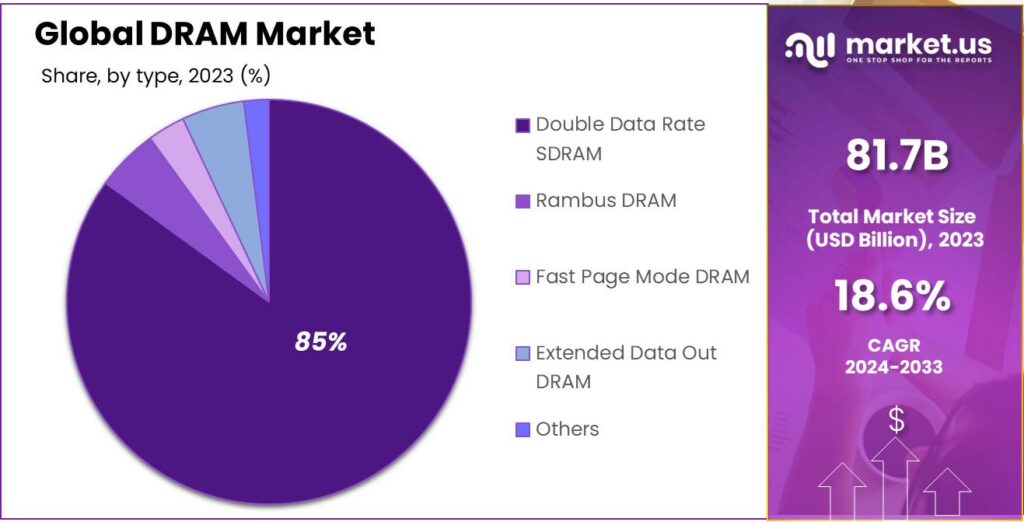

In 2023, the Double Data Rate SDRAM (DDR SDRAM) segment held a dominant market position, capturing more than 85% of the total DRAM market share. DDR SDRAM has become the preferred memory type due to its high performance and efficiency, making it suitable for a wide range of applications, from personal computing to enterprise-level servers.

DDR SDRAM dominates due to advancements in computing technology requiring high-speed memory for tasks like gaming, multimedia, and data-heavy applications. Its reliability and speed make it the preferred choice for both consumer electronics and industrial sectors.

One of the primary reasons DDR SDRAM leads the market is its ability to transfer data on both the rising and falling edges of the clock signal, effectively doubling the data rate compared to traditional SDRAM. This results in faster data processing and greater overall system performance, which is essential in meeting the needs of modern computing environments.

Furthermore, the evolution of DDR SDRAM through successive generations (DDR2, DDR3, DDR4, and DDR5) has enabled manufacturers to deliver memory modules with higher speeds, greater bandwidth, and increased capacity, allowing it to keep pace with the ever-growing demands of industries like gaming, cloud computing, and artificial intelligence (AI).

Technology Analysis

In 2023, the DDR4 segment held a dominant market position, capturing more than a 60% share of the DRAM market. This can be attributed to its widespread adoption across consumer electronics, including personal computers, laptops, and servers.

DDR4 offers a balanced combination of high speed and reliability, making it a preferred choice for both end consumers and businesses. Its cost-effectiveness compared to newer memory technologies like DDR5 has further contributed to its market dominance.

The leading position of DDR4 is also due to the relatively lower power consumption and lower operating cost associated with this technology. As many consumers and enterprises are still upgrading or replacing older systems, DDR4 remains the go-to solution due to its compatibility with a wide array of legacy systems.

Additionally, manufacturers continue to push out DDR4-enabled products, ensuring its availability across a broad spectrum of devices. The segment’s established manufacturing processes further contribute to its continued market leadership, with economies of scale ensuring competitive pricing.

Application Analysis

In 2023, the Mobile Phones segment held a dominant market position, capturing more than a 44% share of the global DRAM market. This can be attributed to the continuous demand for smartphones with advanced features and higher processing power.

As mobile phones increasingly incorporate more RAM to support resource-intensive applications, gaming, multi-tasking, and high-definition content, the demand for DRAM has escalated. Moreover, the shift toward 5G technology has further driven the need for faster and more efficient memory solutions to ensure optimal device performance.

The Mobile Phones segment’s growth is also fueled by the constant innovations in smartphone designs, such as foldable phones and ultra-high-resolution displays. These advancements require larger memory capacities, propelling DRAM consumption in this sector.

The Mobile Phones segment thrives due to competitive pricing by DRAM manufacturers, making high-performance memory more affordable. This has enabled smartphone makers, especially in emerging markets, to offer advanced models at lower prices, driving increased DRAM demand.

Key Market Segments

By Type

- Double Data Rate SDRAM

- Rambus DRAM

- Fast Page Mode DRAM

- Extended Data Out DRAM

- Others

By Technology

- DDR4

- DDR5

- Others

By Application

- Gaming Console

- PCs/Laptops

- Automotive

- Mobile Phones

- Others

Driver

Rising Demand for Consumer Electronics

The growing demand for consumer electronics is a key driver for the DRAM (Dynamic Random Access Memory) market. As smartphones, tablets, laptops, and gaming consoles continue to evolve, the need for high-performance, energy-efficient memory solutions intensifies. DRAM plays a vital role in these devices, enabling faster processing speeds, enhanced multitasking, and better energy management.

Additionally, the rise of 5G connectivity is expected to drive the demand for high-capacity, high-speed memory chips to support faster data transfer. This trend is observed in the increasing adoption of DRAM in gaming, where high-definition graphics and real-time data processing require more advanced memory systems.

Restraint

Supply Chain Vulnerabilities

Despite the positive growth in demand for DRAM, the market faces significant supply chain vulnerabilities. The production of DRAM chips is concentrated in a few regions, mainly South Korea, Taiwan, and Japan, which makes the market susceptible to geopolitical tensions and disruptions.

Events like natural disasters, trade conflicts, or supply chain interruptions have led to volatility in DRAM availability and pricing. Additionally, the COVID-19 pandemic exposed vulnerabilities in semiconductor manufacturing, leading to prolonged shortages. As DRAM manufacturers aim to meet growing demand, they must focus on strengthening their supply chain resilience by diversifying production capabilities and mitigating geopolitical risks.

Opportunity

Expansion of Data Centers and Cloud Computing

The rapid growth of cloud computing and the expansion of data centers present a significant opportunity for the DRAM market. As businesses increasingly rely on cloud infrastructure to store and process vast amounts of data, the demand for high-capacity memory chips is surging.

DRAM is essential for powering data centers, facilitating faster data retrieval and processing. The increasing reliance on data storage, coupled with the shift to more advanced applications like artificial intelligence (AI), machine learning (ML), and big data analytics, will drive a greater need for high-performance DRAM solutions.

Data centers require efficient, scalable memory solutions to maintain performance while managing large data workloads. This creates a lucrative market for DRAM manufacturers to innovate and cater to the growing needs of data-heavy applications.

Challenge

Technological Advancements and Competitive Pressure

One of the most significant challenges facing the DRAM market is the relentless pace of technological advancements and the accompanying competitive pressure. As consumer demand for faster, more energy-efficient devices increases, DRAM manufacturers must continually innovate and scale their production capacities.

However, the rapid pace of technological progress requires substantial investment in research and development (R&D), which can strain resources. In addition, the DRAM market is highly competitive, with major players like Samsung, SK Hynix, and Micron vying for market share.

Furthermore, emerging technologies like 3D NAND and new memory architectures are challenging traditional DRAM solutions. Manufacturers need to address these technological shifts while maintaining cost-effective production.

Emerging Trends

The DRAM industry is witnessing several emerging trends driven by technological advancements and evolving market demands. A notable trend is the growing adoption of high bandwidth memory (HBM), which is particularly crucial for applications in artificial intelligence (AI), gaming, and data centers.

HBM is designed to support faster data transfer rates, addressing the increasing need for quicker and more efficient processing. Additionally, DDR5 (Double Data Rate 5) memory is gaining momentum due to its superior speed and performance compared to its predecessor, DDR4.

Another emerging trend is the miniaturization of memory chips, which allows for the production of more compact, yet high-capacity DRAM modules. As devices continue to become smaller and more powerful, DRAM manufacturers are focusing on developing smaller, more energy-efficient solutions.

Business Benefits

The adoption of DRAM technology offers several key business benefits across various sectors. For businesses in the consumer electronics industry, DRAM plays a crucial role in improving device performance and user experience. Smartphones, laptops, and gaming consoles benefit from DRAM’s ability to enhance processing speeds and multitasking capabilities.

In the data center sector, DRAM is a critical component for improving server performance. The ability of DRAM to handle high-speed data transfer enables faster processing and storage, making it indispensable for cloud service providers and enterprises reliant on big data analytics.

The automotive industry also reaps significant benefits from DRAM in areas like in-vehicle entertainment systems and advanced driver assistance systems (ADAS). DRAM enables faster data processing for real-time navigation, safety features, and enhanced infotainment experiences.

Regional Analysis

In 2023, Asia-Pacific (APAC) held a dominant market position in the global DRAM market, capturing more than 48% of the total market share, which translates to a revenue of approximately USD 39.2 billion. This regional dominance is primarily driven by the presence of major DRAM manufacturers in countries such as South Korea, Japan, and China.

These countries are home to industry leaders like Samsung Electronics, SK Hynix, and Micron Technology, who contribute significantly to both production and innovation in DRAM technology. The high concentration of DRAM manufacturing in the APAC region has made it a critical hub for global supply chains, facilitating cost-effective production and meeting the growing demand for DRAM across various industries.

The rapid adoption of smartphones, tablets, and other electronic devices in APAC is a key driver behind the region’s dominant market share. Countries like China and India, with their large populations and fast-growing middle class, have seen a substantial rise in demand for consumer electronics, which in turn boosts the need for DRAM.

In addition, the rise of 5G networks in the region is expected to further accelerate DRAM consumption, as mobile devices and infrastructure rely heavily on high-speed memory to manage increasing data traffic. The significant investments in data centers and cloud computing services across Asia-Pacific, particularly in countries such as China and India, are also fueling the demand for high-capacity DRAM solutions.

APAC leads the global DRAM market due to strong manufacturing infrastructure and high demand from sectors like consumer electronics, IT, and automotive. While North America and Europe contribute to market growth, their share is smaller compared to APAC’s dominance in both production and consumption.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

The DRAM market is highly competitive, with several prominent players leading the industry.

Samsung Electronics is the largest player in the global DRAM market, holding the top spot with a market share of around 40%. The company’s leadership in DRAM manufacturing can be attributed to its robust R&D capabilities and advanced semiconductor fabrication processes. Samsung has consistently led the way in introducing new generations of DRAM technology, including DDR5, which offers higher speeds and bandwidth compared to previous generations.

Micron Technology holds the second-largest market share in the DRAM segment, with a strong presence in both consumer and enterprise markets. The company is known for its high-performance DRAM solutions and has made significant strides in developing advanced memory technologies, including DDR4 and DDR5 memory.

SK Hynix ranks third among the top DRAM manufacturers globally, capturing a substantial share of the market. The company has made significant advancements in DRAM technology, particularly in the development of DDR4 and DDR5 memory modules, as well as in emerging memory types such as high-bandwidth memory (HBM).

Top Key Players in the Market

- Samsung Electronics

- Micron Technology

- SK Hynix

- Elpida

- Transcend Information

- Nanya Technology

- Powerchip

- Winbond

- Infineon Technologies

- Kingston Technology

- Other Key Players

Top Opportunities Awaiting for Players

- Advancements in High-Bandwidth Memory (HBM): The evolution of HBM technology is reshaping the DRAM landscape. Manufacturers prioritizing HBM production are well-positioned to meet the escalating demand for high-speed data processing, particularly in artificial intelligence (AI) applications.

- Integration with AI and Machine Learning Applications: The surge in AI-driven technologies necessitates efficient memory solutions. DRAM manufacturers can capitalize on this by developing products tailored to AI workloads, thereby enhancing performance and energy efficiency.

- Expansion in Data Center and Cloud Computing Services: The proliferation of data centers and cloud services requires substantial memory capacities. DRAM suppliers focusing on high-capacity, reliable memory solutions can tap into this growing market segment.

- Emergence of 5G Technology: The rollout of 5G networks is expected to boost demand for advanced consumer electronics, including smartphones and tablets, which rely heavily on DRAM for optimal performance. Manufacturers investing in low-power DRAM variants, such as LPDDR5X, can gain a competitive edge.

- Automotive Industry Innovations: The automotive sector’s shift towards autonomous and connected vehicles increases the need for robust memory solutions. DRAM products designed to meet automotive-grade standards present a lucrative opportunity for market players.

Recent Developments

- In November 2023, Micron unveiled a 128GB DDR5 Registered DIMM (RDIMM) memory module, based on a 32GB monolithic device, offering performance up to 8000 MT/s, suitable for data center applications.

- In August 2024, Samsung’s 8-layer HBM3E chips passed Nvidia’s qualification tests for use in AI processors, marking a significant milestone in high-performance memory solutions.

- In September 2024, SK Hynix commenced mass production of its 12-layer HBM3E chips, enhancing its position in the high-bandwidth memory market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 81.7 Bn |

| Forecast Revenue (2033) | USD 449.8 Bn |

| CAGR (2024-2033) | 18.6% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Double Data Rate SDRAM, Rambus DRAM, Fast Page Mode DRAM, Extended Data Out DRAM, Others), By Technology (DDR4, DDR5, Others), By Application (Gaming Console, PCs/Laptops, Automotive, Mobile Phones, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Samsung Electronics, Micron Technology, SK Hynix, Elpida, Transcend Information, Nanya Technology, Powerchip, Winbond, Infineon Technologies, Kingston Technology, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |