Quick Navigation

Report Overview

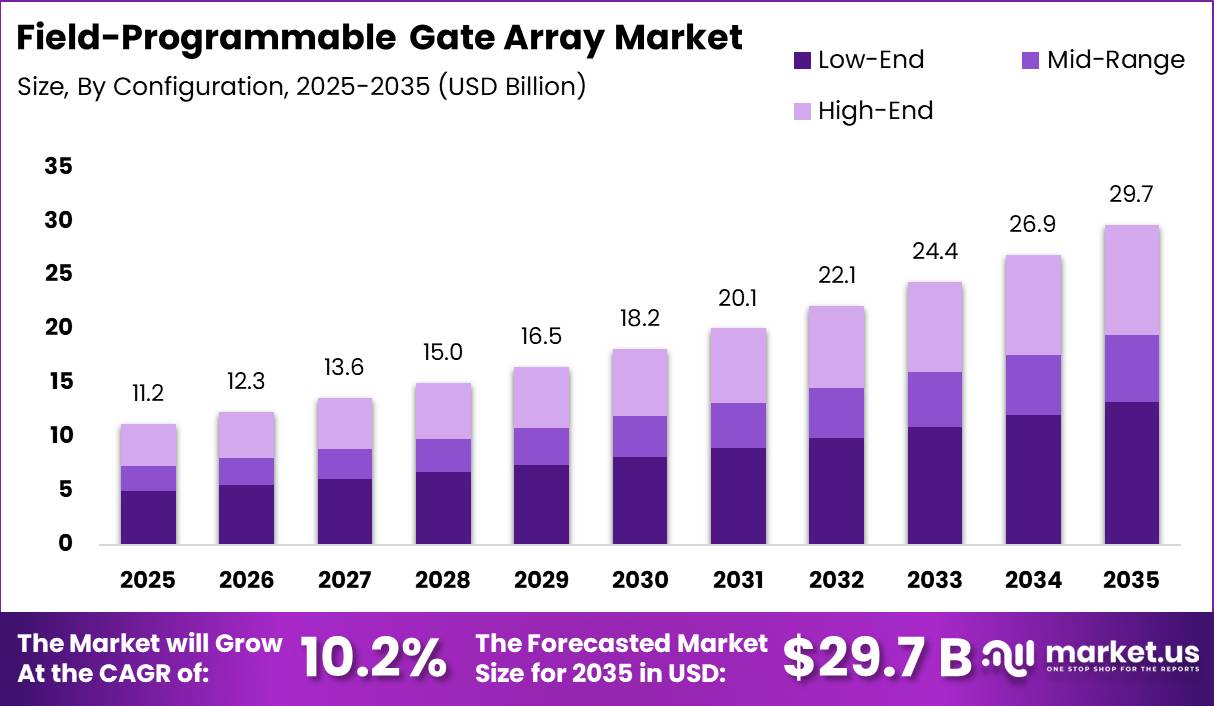

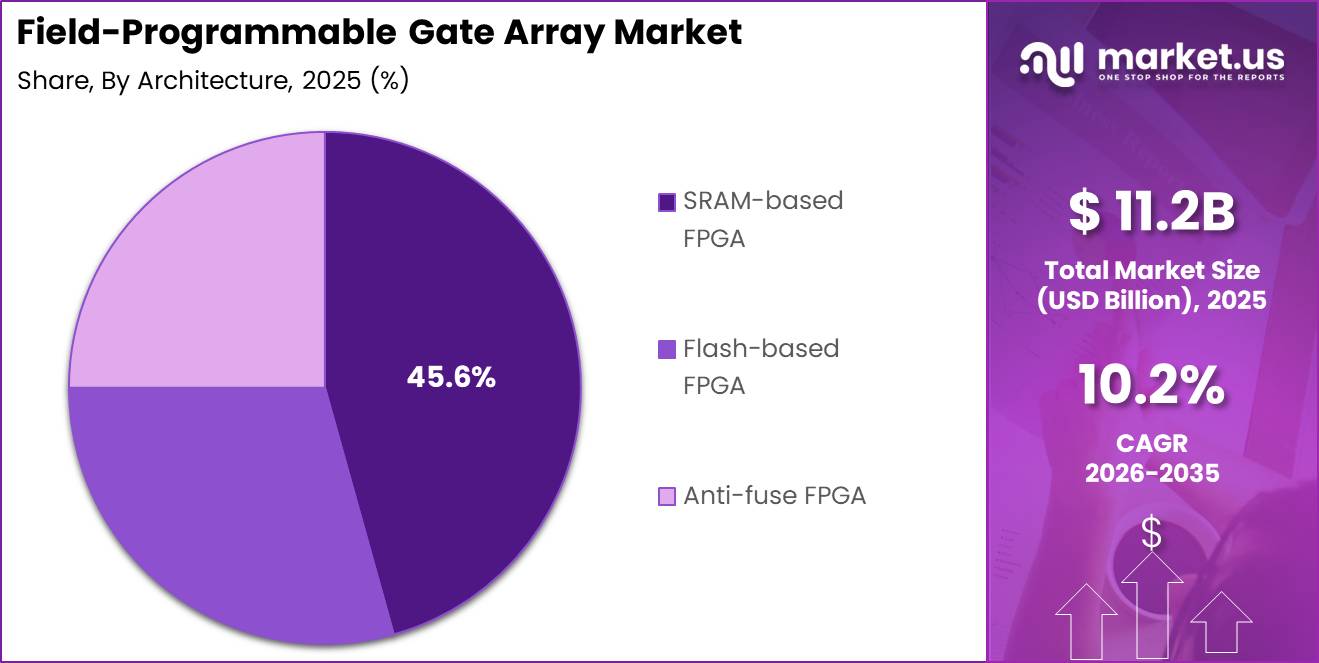

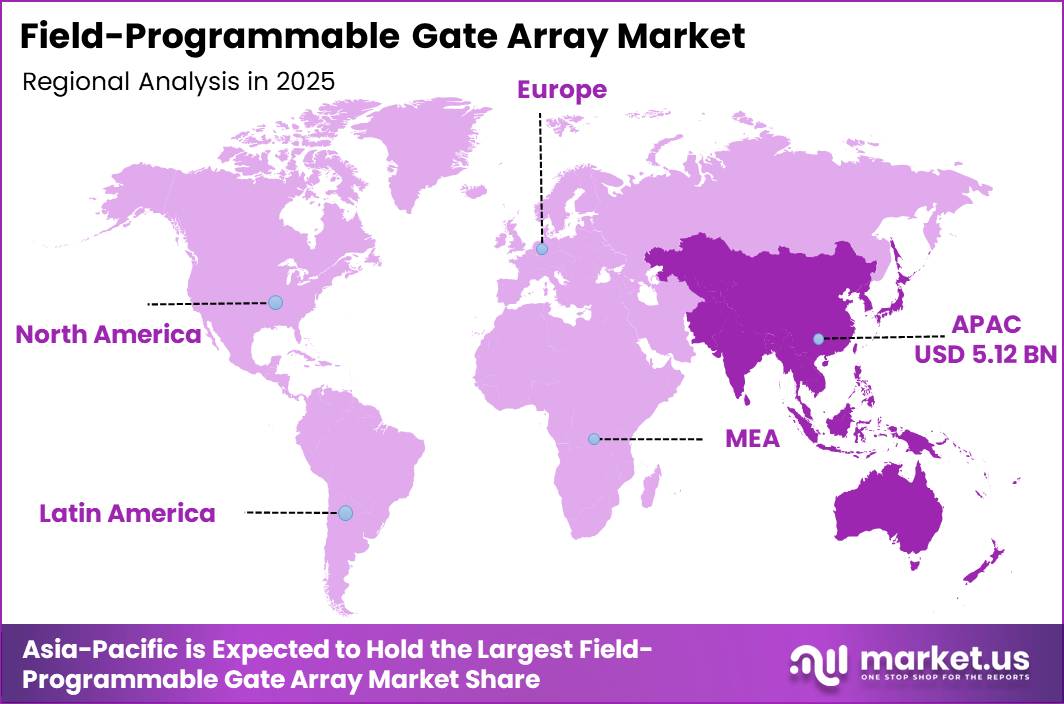

In 2025, the Global Field-Programmable Gate Array (FPGA) Market was valued at USD 11.2 billion. The market is projected to grow at a CAGR of 10.2% during 2026–2035, reaching approximately USD 29.7 billion by 2035. Asia-Pacific dominated the global market in 2025, accounting for more than 45.7% of the total market share and generating approximately USD 5.1 billion in revenue.

According to the World Semiconductor Trade Statistics, the global semiconductor market is expected to reach about USD 772 billion in 2025, representing nearly 22% year-on-year growth. Demand is being driven by logic and memory chips used in artificial intelligence, cloud computing, automotive electronics and industrial automation. These industries increasingly use FPGAs for flexible processing, signal control, hardware testing and system prototyping.

UNIDO also reported that Asia and Oceania generated around 57.2% of global manufacturing value added in 2024. This strong manufacturing base supports large-scale production of electronic boards, communication equipment, and industrial systems containing programmable logic devices. Asia-Pacific’s leadership is further supported by its major role in global electronics production.

The region manufactures high volumes of smartphones, network equipment, base stations and consumer devices that use programmable logic for security, interface control and rapid product modification. The Semiconductor Industry Association reported that global semiconductor sales reached approximately USD 298.5 billion in Q1 2026, while annual sales growth in China and Asia-Pacific/All Other exceeded 70%.

Key Takeaway

- The Global Field-Programmable Gate Array (FPGA) Market was valued at USD 11.2 billion in 2025.

- The market is projected to reach USD 29.7 billion by 2035, growing at a 10.2% CAGR.

- Low-end FPGA devices led the device category with a 44.8% share in 2025.

- SRAM-based FPGAs dominated the architecture segment with a 45.6% share in 2025.

- The 20–90 nm process-node category held the largest share at 67.6% in 2025.

- IT and Telecommunication led the end-user segment with a 38.67% share in 2025.

- Asia-Pacific’s 45.7% share represents approximately USD 5.1 billion of the 2025 market value.

By Configuration

Low-End FPGAs Lead with a 44.8% Market Share

In 2025, low-end FPGA devices held a dominant market position, capturing more than a 44.8% share. Their leadership is primarily supported by widespread adoption across high-volume, cost-sensitive electronics, Internet of Things devices, consumer equipment, testing systems, and embedded applications.

According to the International Data Corporation, global smartphone shipments reached approximately 1.2 billion units in 2025. Smartphones, peripheral modules, supporting boards, and production-testing equipment require several basic logic, connectivity, and interface-control functions that can be efficiently managed using low-end FPGAs instead of more expensive high-performance devices.

Demand is further strengthened by the expanding global connected-device ecosystem. GSMA Intelligence projected that worldwide IoT connections would reach approximately 25.2 billion by 2025, with Asia-Pacific accounting for nearly 44% of total connections and around 35% of global IoT revenue. This growing installed base creates substantial demand for affordable and programmable logic components used in sensors, gateways, communication modules, and embedded controllers.

By Architecture

SRAM-Based FPGAs Lead with a 45.6% Share

In 2025, SRAM-based FPGAs held a dominant market position, capturing more than a 45.6% share. Their leadership is supported by the growing demand for fast, flexible, and low-latency processing across digital infrastructure. SRAM cells store configuration data in on-chip memory, allowing FPGA devices to be reprogrammed rapidly without replacing the underlying hardware.

According to the International Telecommunication Union, global end-user internet traffic reached approximately 8.8 zettabytes in 2025, while mobile broadband traffic increased by around 19% annually and fixed broadband traffic grew by nearly 16%.

The continued expansion of global data traffic supports the adoption of reconfigurable logic in networking, cloud computing, and telecommunications equipment. UNCTAD also estimated that the digital economy is expanding by approximately 10% to 12% annually and could contribute more than two-thirds of new value creation over the coming decade.

By Node Size

In 2025, FPGAs manufactured on 20–90 nm process nodes held a dominant market position, capturing more than a 67.6% share. Their leadership is supported by a practical balance of performance, manufacturing cost, and long-term reliability.

According to the U.S. Department of Commerce, semiconductors produced on 28–90 nm process nodes are widely used in microcontrollers, analog and mixed-signal chips, and power devices that are shipped in tens of billions of units annually.

The 20–90 nm range also allows FPGA manufacturers to integrate programmable devices into existing electronic boards without requiring major changes to power requirements, cooling systems or product architecture. The Semiconductor Industry Association has indicated that global semiconductor unit shipments remain heavily supported by discrete devices, analog chips and microcontrollers.

By End User

IT and Telecommunication Leads with a 38.67% Share

In 2025, IT and Telecommunication held a dominant market position, capturing more than a 38.67% share of the FPGA market. Its leadership is supported by the growing need for programmable hardware capable of managing rising data traffic, evolving communication standards, and an increasing number of connected users. According to the International Telecommunication Union, global mobile-cellular subscriptions reached approximately 9.2 billion in 2025, equivalent to around 112 subscriptions per 100 people.

Mobile broadband penetration also reached approximately 99 subscriptions per 100 people, while 5G networks covered nearly 55% of the global population. Mobile base stations, core routers, data centers, and edge-computing nodes use FPGAs for packet processing, network timing, encryption, signal processing, and interface conversion.

Key Market Segments

By Configuration

- Low-End

- Mid-Range

- High-End

By Architecture

- SRAM-based FPGA

- Flash-based FPGA

- Anti-fuse FPGA

By Node Size

- ≥90 nm

- 20-90 nm

- ≤16 nm

By End User

- IT & Telecommunication

- Consumer Electronics

- Aerospace & Defence

- Industrial

- Automotive

- Healthcare

- Other End-Use Industries

Geopolitical Impact Analysis

Geopolitical tensions are increasing costs and delivery risks across the FPGA supply chain. WTO tariff data indicate that the global simple average applied MFN tariff increased from 5.7% to 6.3% in 2025, while 47 member states raised duties on at least 1 strategic-technology category, including semiconductors and electronic components. In the United States, the average applied MFN tariff rose from 3.4% in 2023 to 11.2% in 2025.

Additional Section 301 measures introduced surcharges of up to 50% on selected Chinese semiconductors, wafers and polysilicon inputs from January 1, 2025. These tariffs increase FPGA production costs because wafers, substrates, packaging materials and assembled boards often cross several international borders. UNCTAD also reported that Red Sea and Suez Canal disruptions extended Asia–Europe container transit times by approximately 7–10 days, encouraging semiconductor companies to hold larger inventories and safety stocks.

Energy-price volatility creates further pressure on FPGA manufacturers. According to the International Energy Agency, wholesale electricity prices in major manufacturing regions were around 20% above pre-COVID averages in 2024, despite declining by approximately 20% from 2023. Semiconductor fabrication plants can consume hundreds of megawatt-hours of electricity each day, making power costs an important part of wafer pricing.

Export restrictions and trade controls affecting gallium and germanium have also reportedly increased some compound-semiconductor input costs by 30–50%. As a result, FPGA suppliers and buyers are adopting multiple sourcing, alternative shipping routes and larger inventories, while placing greater importance on supply security rather than only the lowest unit price.

Regional Analysis

Asia-Pacific held the leading position in the FPGA market, accounting for 45.7% of global revenue, equal to approximately USD 5.1 billion in 2025. This strong share is supported by the region’s large electronics, telecommunications and industrial manufacturing base across China, Japan, South Korea, Taiwan, India and ASEAN countries.

High production volumes of smartphones, networking equipment, data-center systems, automotive electronics and industrial automation devices create steady demand for reprogrammable logic used in base stations, routers, embedded boards and industrial controllers.

The region also benefits from a well-developed semiconductor supply chain, with foundries, outsourced semiconductor assembly and testing companies, PCB manufacturers and equipment producers located close to major system manufacturers. This integrated structure helps reduce delivery times and supports faster movement from product design to commercial production.

Continued investment in 5G networks, cloud infrastructure, smart factories and advanced electronics manufacturing is further increasing FPGA adoption for signal processing, hardware acceleration and system control. Government-backed semiconductor programs, skilled engineering talent and strong capital investment also support regional growth.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Drivers

| Driver | (~) % CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI & ML Inference Acceleration Demand | +3.2% | North America, Asia-Pacific | Short term (≤ 2 years) |

| 5G Network Infrastructure Buildout | +2.1% | Asia-Pacific, Europe, North America | Short term (≤ 2 years) |

| Data Center Hardware Acceleration Adoption | +1.8% | North America, Europe | Short term (≤ 2 years) |

| Aerospace & Defense Modernization Programs | +1.3% | North America, Europe | Medium term (2–4 years) |

| Automotive ADAS & Electrification Electronics | +1.1% | Asia-Pacific, Europe, North America | Medium term (2–4 years) |

| Industrial Automation & Smart Manufacturing | +0.9% | Asia-Pacific, Europe | Short term (≤ 2 years) |

AI & ML Inference Acceleration Demand

The structural pivot of hyperscale data centers toward real-time AI inference workloads has made FPGA-based acceleration a primary commercial lever, fundamentally reshaping vendor business models from one-time hardware sales toward recurring co-design services and IP licensing engagements.

FPGAs deliver energy efficiency advantages of roughly 1.4× over comparable GPU implementations and up to 4.7× over CPU baselines on identical inference pipelines a critical differentiator as data center operators face power density ceilings of 40–60 kW per rack in AI-optimized facilities.

The AI inference segment of the broader semiconductor market was tracking a CAGR approaching 19% through 2025–2030, with FPGAs capturing a structurally durable slice of this spend due to their reconfigurability advantage.

The ability to reprogram logic in the field as model architectures evolve from transformer attention mechanisms to multimodal pipeline stages eliminates the 18–36 month ASIC re-spin cycle and the associated non-recurring engineering costs that typically range from $5 million to $30 million per tape-out at advanced nodes.

Restraints

| Restraint | (~) % CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| US–China Advanced Semiconductor Export Controls | -2.4% | Global (highest impact: China, East Asia) | Short term (≤ 2 years) |

| High Per-Unit Cost of High-End FPGAs | -1.5% | Global (highest impact: Emerging Markets) | Short term (≤ 2 years) |

| Oligopolistic Vendor Concentration Risk | -1.1% | Global | Medium term (2–4 years) |

| Capital Expenditure Constraints Among Mid-Market OEMs | -0.8% | Europe, Asia-Pacific | Short term (≤ 2 years) |

| Advanced Node Foundry Capacity Allocation Bias | -0.7% | Global (highest impact: North America, Taiwan) | Short term (≤ 2 years) |

US–China Advanced Semiconductor Export Controls

The Bureau of Industry and Security’s October 2022 export controls subsequently expanded in October 2023 and further clarified through 2025 guidance directly froze the ability of US-headquartered FPGA vendors to ship high-performance programmable logic devices to a broad class of Chinese end-users, including subsidiaries of Chinese parent companies operating in third-country jurisdictions.

The licensing presumption of denial applied to advanced logic nodes, specifically those featuring non-planar architectures at or below 16 nm / 14 nm, directly disqualifies the highest-margin FPGA product tiers from China-bound revenues, compressing blended ASPs across the affected vendor portfolios by an estimated 8–15% on affected SKUs.

Challenges

| Challenge | (~) % CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| FPGA Engineering Talent Deficit | -1.8% | Global (highest impact: North America, Europe) | Long term (≥ 4 years) |

| HDL Design Complexity & Toolchain Friction | -1.3% | Global | Medium term (2–4 years) |

| Advanced Node Semiconductor Supply Constraints | -1.1% | Global (highest impact: TSMC-dependent vendors) | Medium term (2–4 years) |

| ASIC Migration Pressure at Scale | -0.9% | North America, Asia-Pacific | Medium term (2–4 years) |

| Power Envelope Constraints at Edge | -0.7% | Global | Short term (≤ 2 years) |

| IP Security & Bitstream Piracy Risk | -0.5% | Asia-Pacific, Europe | Long term (≥ 4 years) |

FPGA Engineering Talent Deficit

The FPGA engineering talent shortage is a structural industry challenge rather than a temporary hiring issue. Engineering education has increasingly shifted toward software and computer science, reducing the number of professionals trained in VHDL, SystemVerilog, synthesis constraints, timing closure, and high-level synthesis.

According to the VDI/IW Ingenieurmonitor, Germany recorded 271 open electrical and electronics engineering positions for every 100 unemployed engineers in Q3 2025. The shortage is even more serious in FPGA roles because they require several specialized design and verification skills.

As a result, FPGA contractor rates are around 15–25% higher than comparable ASIC design roles, while complex SoC projects may face delays of 6–12 months. Tools such as Intel oneAPI and AMD Vitis AI can reduce development pressure, but they may introduce new timing and verification risks, increasing costs and weakening FPGA competitiveness against GPUs in mid-complexity applications.

Opportunities

| Opportunity | (~) % CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Embedded FPGA (eFPGA) IP Licensing Model | +2.6% | Global (highest impact: North America, Asia-Pacific) | Medium term (2–4 years) |

| Healthcare & Medical Imaging Hardware Acceleration | +1.7% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| India & Southeast Asia Semiconductor Localization Push | +1.4% | India, Vietnam, Malaysia, Thailand | Long term (≥ 4 years) |

| Low-Power FPGA Expansion in IoT & Smart Infrastructure | +1.2% | Global (highest impact: Asia-Pacific, Europe) | Short term (≤ 2 years) |

| Space & Satellite Radiation-Hardened FPGA Segment | +0.9% | North America, Europe | Long term (≥ 4 years) |

| Open-Source FPGA Toolchain Ecosystem Monetization | +0.6% | Global | Long term (≥ 4 years) |

Embedded FPGA (eFPGA) IP Licensing Model

The eFPGA IP licensing model remains a major untapped opportunity in the FPGA value chain. Unlike discrete FPGA sales, eFPGA allows SoC developers to license reconfigurable logic as an embedded IP block and integrate it directly into custom chips.

The segment generated less than USD 200 million in annual revenue during 2025–2026, while the discrete FPGA market was more than 10 times larger. Growth is supported by hyperscale chip developers seeking post-silicon programmability without costly new tape-outs and edge AI vendors requiring inference engines that can be updated as models change.

eFPGA fabric priced at approximately USD 0.15–0.40 per logic element under royalty-based structures can deliver gross margins above 80%, compared with 45–55% for discrete FPGA hardware. However, wider adoption requires stronger EDA integration, foundry qualification at 5 nm, 3 nm and sub-3 nm nodes, and partnerships with fabless SoC companies. These areas remain underdeveloped, leaving a large share of potential demand unserved.

Key Players Analysis

Tier-1 FPGA suppliers include Intel’s Altera business, AMD’s Xilinx division, and Lattice Semiconductor, which together hold a major share of global programmable-logic revenue and design activity. In April 2025, Intel reported that Altera generated USD 1.5 billion in fiscal 2024 revenue, with a GAAP gross margin of USD 361 million and a GAAP operating loss of USD 615 million.

Intel also invested about USD 15.3 billion in research and development against total 2024 revenue of approximately USD 66.1 billion, representing an R&D intensity of nearly 23%. AMD recorded USD 25.8 billion in 2024 revenue, while its Embedded segment generated USD 3.6 billion, compared with USD 5.3 billion in 2023.

Lattice reported USD 509.4 million in 2024 revenue, down 30.9% year-on-year, while maintaining an adjusted EBITDA margin of 31.8% and a non-GAAP gross margin above 65%. Intel, AMD and Lattice are estimated to collectively represent around 60–65% of FPGA revenue.

Tier-2 participants mainly focus on specialized applications. Microchip generated approximately USD 8.6 billion in fiscal 2024 revenue. QuickLogic recorded around USD 20.1 million in 2024 revenue, USD 51.9 million in assets, and USD 24.9 million in equity. Its Q1 2026 revenue reached USD 5.1 million, increasing 16.8% year-on-year. NVIDIA reported USD 60.9 billion in fiscal 2024 revenue, including USD 47.5 billion from Data Center.

Top Key Players in the Market

- Intel Corporation

- Xilinx, Inc.

- Qualcomm Technologies, Inc.

- NVIDIA Corporation

- Broadcom

- AMD, Inc.

- Quicklogic Corporation

- Lattice Semiconductor Corporation

- Achronix Semiconductor Corporation

- Microchip Technology Inc.

Recent Developments

- In May 2026, QuickLogic advanced its radiation-hardened FPGA portfolio by continuing the production ramp of its RadPro family on Intel’s 18A process technology. The company reported Q1 2026 revenue from continuing operations of USD 5.1 million, up 16.8% year-on-year and 35.3% compared with Q4 2025. New product revenue supported the increase as RadPro devices moved into volume qualification for aerospace and defense programs.

- In April 2025, Intel agreed to sell a 51% stake in Altera to Silver Lake in a deal valuing the FPGA business at USD 8.7 billion. Altera generated USD 1.5 billion in 2024 revenue, with a GAAP gross margin of USD 361 million and a GAAP operating loss of USD 615 million. Intel retained a 49% stake and continued as a key foundry partner, giving Altera greater flexibility to invest in AI, communications, edge computing, and programmable logic.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 11.2 Billion |

| Forecast Revenue (2035) | USD 29.7 Billion |

| CAGR (2026-2035) | 10.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Configuration (Low-End, Mid-Range, High-End); By Architecture (SRAM-based FPGA, Flash-based FPGA, Anti-fuse FPGA); By Node Size (≥90 nm, 20-90 nm, ≤16 nm); By End User (IT & Telecommunication, Consumer Electronics, Aerospace & Defence, Industrial, Automotive, Healthcare, Other End-Use Industries) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Intel Corporation, Xilinx, Inc., Qualcomm Technologies, Inc., NVIDIA Corporation, Broadcom, AMD, Inc., Quicklogic Corporation, Lattice Semiconductor Corporation, Achronix Semiconductor Corporation, Microchip Technology Inc. |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Market")