Quick Navigation

Report Overview

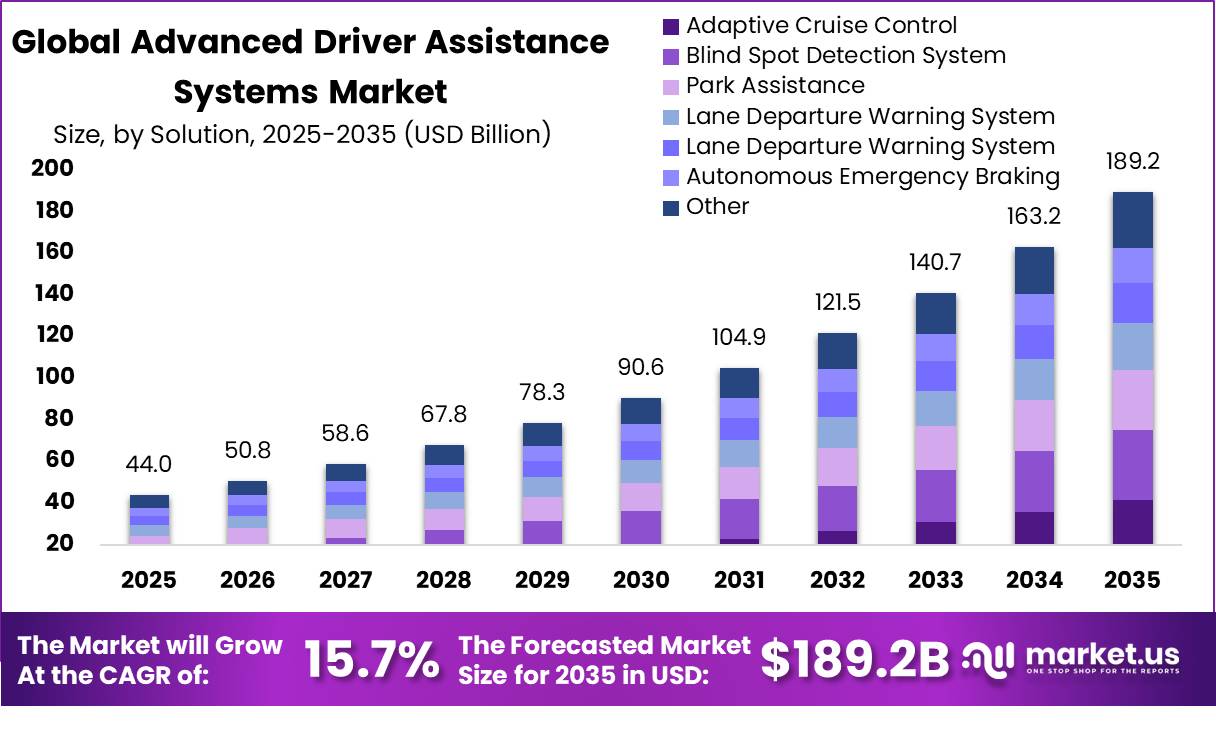

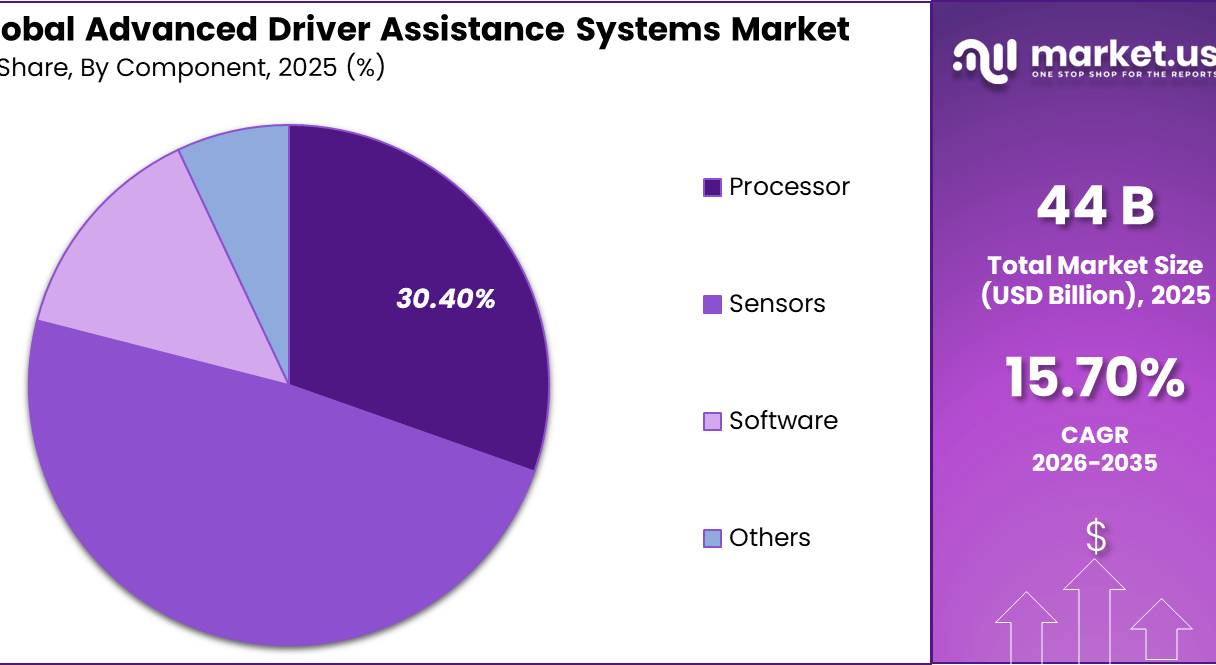

Global Advanced Driver Assistance Systems Market size is expected to be worth around USD 189.2 Billion by 2035 from USD 44 Billion in 2025, growing at a CAGR of 5.00% during the forecast period 2026 to 2035.

The Advanced Driver Assistance Systems market covers electronic safety and perception technologies embedded in passenger and commercial vehicles. These systems include adaptive cruise control, automatic emergency braking, blind spot detection, lane departure warning, tire pressure monitoring, and adaptive front lighting. This reflects a market structured around hardware components, software stacks, and OEM integration programs across global vehicle platforms.

Key Takeaways

- Advanced Driver Assistance Systems Market size reached USD 44 Billion in 2025 and is forecast to reach USD 189.2 Billion by 2035 at a CAGR of 5.00%.

- By Solution, Adaptive Cruise Control dominates with a 21.80% share in 2025.

- By Component, Sensors hold the dominant position with a 48.60% share.

- By Vehicle, Passenger Cars represent the leading segment with a 67.40% share.

- North America leads all regions with a 35.80% market share, valued at USD 15.752 Billion in 2025.

Government mandates are directly reshaping ADAS procurement timelines. The EU General Safety Regulation requires fitment of AEB, lane-keeping assist, and driver drowsiness detection across new vehicle categories. The U.S. FMVSS No. 127 rule, finalized in 2024, requires automatic emergency braking on nearly all light vehicles by September 2029. These mandates convert ADAS from optional content into baseline engineering spend.

According to MITRE analysis of approximately 98 million U.S. passenger vehicles, 5 ADAS features including forward collision warning, AEB, pedestrian detection warning, pedestrian AEB, and lane departure warning each exceeded 90% market penetration by the 2023 model year. This means baseline ADAS content is no longer a differentiator in the U.S. passenger segment. Suppliers must compete on software depth, sensor accuracy, and integration capability rather than feature presence alone.

A U.S. safety survey reported that 57% of drivers said at least one ADAS feature kept them from a crash. Consumer acceptance at this scale signals that feature trust is building across mainstream buyers. This creates a commercial foundation for upselling more advanced packages, including highway assist and automated parking bundles, to existing ADAS-equipped vehicle owners.

Solution Analysis

Adaptive Cruise Control dominates with 21.80% due to OEM standardization across mid-range platforms.

In 2025, Adaptive Cruise Control held a dominant market position in the By Solution segment of the Advanced Driver Assistance Systems Market, with a 21.80% share. ACC integrates radar and camera inputs to manage vehicle speed and following distance automatically. Based on Consumer Reports data from approximately 47,000 drivers, ACC recorded a satisfaction rate of 63%, confirming that real-world usability supports continued OEM investment in this feature across volume nameplates.

Blind Spot Detection System accounts for 18.00% of the By Solution segment. BSD uses short-range radar or ultrasonic sensors to alert drivers to vehicles in adjacent lanes. Consumer Reports data shows rear cross-traffic warning, a closely related function, reached 72% satisfaction among surveyed drivers. This satisfaction level signals strong stickiness in the feature set. Suppliers packaging BSD with RCTW can expect higher attach rates and reduced churn in fleet procurement cycles.

Park Assistance holds a 15.00% share within the By Solution segment. This system uses ultrasonic sensors and camera feeds to guide low-speed maneuvering in constrained spaces. Backup camera satisfaction reached 69% in Consumer Reports data, confirming that proximity-sensing features convert well with everyday urban drivers. This creates a clear bundling opportunity pairing park assistance with rear-view camera systems in mass-market vehicle programs.

Component Analysis

Sensors dominate with 48.60% due to multi-sensor fusion requirements across ADAS architectures.

In 2025, Sensors held a dominant market position in the By Component segment of the Advanced Driver Assistance Systems Market, with a 48.60% share. OEM integration of radar, LiDAR, ultrasonic, and camera arrays drives sensor volume across every ADAS function tier. This hardware concentration means sensor suppliers hold structural pricing power. Any supply disruption in radar or camera modules directly affects multiple ADAS system outputs across the same vehicle platform.

Processors account for 30.40% of the By Component segment. Centralized vehicle computing platforms are replacing distributed ECU architectures. This shift concentrates more processing demand into fewer, higher-performance chips per vehicle. Processor suppliers who secure OEM design wins early in platform development cycles lock in multi-year revenue with high switching costs, creating durable revenue visibility across vehicle program lifespans of five to seven years.

Software holds a 14.00% share in the By Component segment. Software increasingly determines the functional ceiling of ADAS hardware already installed in vehicles. Over-the-air update capability allows feature expansion and perception algorithm improvements after vehicle sale. This structure separates software gross margin from hardware bill-of-materials economics, meaning suppliers who control the software layer capture recurring post-sale revenue that hardware-only vendors cannot access.

Vehicle Analysis

Passenger Cars dominate with 67.40% due to regulatory mandates targeting light vehicle categories.

In 2025, Passenger Cars held a dominant market position in the By Vehicle segment of the Advanced Driver Assistance Systems Market, with a 67.40% share. Safety regulations across the EU, U.S., China, and Japan specifically target passenger vehicle categories for mandatory ADAS fitment. This regulatory concentration directs the largest share of OEM procurement and Tier 1 integration spend toward passenger platforms, reinforcing segment dominance through compliance-driven volume rather than discretionary buyer preference.

Commercial Vehicles, including Light Commercial Vehicles and Heavy Commercial Vehicles, represent the remaining share of the By Vehicle segment. Fleet operators are deploying driver monitoring and collision avoidance systems to reduce accident-related insurance liabilities and regulatory penalties. This creates a distinct procurement pattern where total cost of ownership arguments, rather than consumer safety ratings, drive purchase decisions. Suppliers entering this sub-segment need fleet-scale pricing models and telematics integration capabilities.

Key Market Segments

By Solution

- Adaptive Cruise Control (ACC)

- Blind Spot Detection System (BSD)

- Park Assistance

- Lane Departure Warning System (LDWS)

- Tire Pressure Monitoring System (TPMS)

- Autonomous Emergency Braking (AEB)

- Adaptive Front Lights (AFL)

- Others

By Component

- Processor

- Sensors

- Radar

- LiDAR

- Ultrasonic

- Others

- Software

- Others

By Vehicle

- Passenger Cars

- Commercial Vehicle

- Light Commercial Vehicle

- Heavy Commercial Vehicle

Drivers

The primary regulatory anchor for North American ADAS demand is FMVSS No. 127, finalized in 2024. This rule requires automatic emergency braking and pedestrian AEB as standard on nearly all U.S. light vehicles by September 2029. Performance thresholds include no-contact stopping at up to 62 mph and pedestrian detection in both daylight and darkness. These requirements favor scalable radar-camera architectures and push OEM procurement timelines several years ahead of the 2029 deadline.

MITRE analysis of approximately 98 million U.S. vehicles and 21.2 million crashes found that AEB reduced rear-end crash involvement from 46% in model years 2015 to 2017 to 52% in model years 2021 to 2023. Vehicles with pedestrian AEB showed a 9% reduction in single-vehicle frontal crashes involving non-motorists. A pre-COVID PARTS study found FCW and AEB together reduced front-to-rear crashes by 49 to 50%. This safety performance record gives regulators and OEMs a verified basis for mandating and expanding AEB content.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU GSR fitment mandate expands baseline ADAS content | +2.5% | EU core, UK alignment, Eastern Europe manufacturing base | Short term (≤ 2 years) |

| U.S. FMVSS 127 accelerates forward-sensing standardization | +1.6% | U.S. core, Mexico assembly corridor, Canada spill-over | Medium term (2-4 years) |

| Euro NCAP 2026 tightens safety-performance benchmarks | +1.4% | Europe core, Japan and South Korea export programs | Short term (≤ 2 years) |

| China vehicle scale drives ADAS penetration into volume segments | +2.2% | China core, ASEAN spill-over, global sourcing impact | Short term (≤ 2 years) |

| Centralized vehicle compute raises software-led ADAS value | +1.8% | North America, EU, China, South Korea | Medium term (2-4 years) |

| Safety compliance shifts ADAS from option pack to platform standard | +1.1% | Global, strongest in compact and mid-size vehicle lines | Medium term (2-4 years) |

Restraints

Euro NCAP 2026 tightens crash-avoidance and safe-driving requirements across motorcycle detection, junction scenarios, degraded-condition robustness, and driver monitoring. Road validation requirements extend to 2,000 km for certain speed and steering functions. A sub-5-star outcome can damage model positioning across European markets. This forces OEMs to engineer beyond bare compliance, adding tens of millions of dollars in validation spend per multi-nameplate platform cycle and delaying revenue recognition for new ADAS options.

An academic driver perception study found that approximately 70% of surveyed drivers activate an ADAS feature most or all of the time, yet approximately 40% reported that ADAS often compromises their safety when active. This trust gap between usage frequency and perceived safety creates a commercial risk. OEMs and suppliers face reputational and liability exposure if high-use systems generate driver-reported safety concerns, which can slow adoption of premium ADAS tiers and trigger regulatory scrutiny on feature performance claims.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tariff-led vehicle inflation | -1.4% | North America core, EU exporters, Mexico corridors, Japan/Korea imports | Short term (≤ 2 years) |

| Cybersecurity compliance overload | -1.1% | EU, UK, global OEM platforms supplying Europe | Medium term (2-4 years) |

| Rare-earth magnet bottlenecks | -0.9% | EU, India, Japan, Korea, North America tier chains | Short term (≤ 2 years) |

| Validation cost escalation | -1.0% | EU core, premium OEM hubs, APAC export programs | Medium term (2-4 years) |

| Mid-segment affordability squeeze | -1.3% | Mass-market North America, EU, India, ASEAN, LATAM | Medium term (2-4 years) |

| Software liability and recall risk | -0.8% | North America, EU, China, Korea, Japan | Long term (≥ 4 years) |

Challenges

ADAS validation burden is deepening as systems move beyond fixed-function hardware logic into software-intensive perception and decision layers. Regression testing requirements expand with every calibration change, sensor substitution, and OTA update cycle. Figures from MITRE analysis confirm that AEB effectiveness improved measurably across successive model years, which means each new software generation must clear a rising performance baseline before deployment approval.

Validation overhead reduces effective scaling speed by approximately 1.2 percentage points of CAGR. OEMs and Tier 1 suppliers must invest in industrialized scenario simulation, closed-loop validation toolchains, hardware-in-the-loop capacity, and stricter feature-release governance. Sensor sourcing instability adds a further 1.3 percentage point drag. These combined frictions create an opening for validation-as-a-service providers and simulation software vendors to capture recurring engineering spend from volume OEMs lacking in-house testing infrastructure depth.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Sensor sourcing instability | -1.3% | East Asia supply nodes, EU OEM clusters, North America assembly corridors | Medium term (2-4 years) |

| ADAS validation overload | -1.2% | EU regulatory hubs, US testing corridors, Japan, South Korea | Long term (≥ 4 years) |

| Compliance workflow expansion | -0.9% | United States, EU, Japan | Medium term (2-4 years) |

| Specialized talent scarcity | -1.0% | Germany, France, US, Japan, South Korea, India engineering hubs | Medium term (2-4 years) |

| Software stack integration strain | -1.1% | EU premium OEMs, US platform developers, China smart-vehicle clusters | Long term (≥ 4 years) |

| Cybersecurity lifecycle load | -0.8% | EU connected fleets, Japan, South Korea, North America | Long term (≥ 4 years) |

Opportunities

The primary forward opportunity in ADAS lies in converting installed hardware capability into recurring post-sale software revenue. NHTSA’s 2024 to 2033 NCAP roadmap expands scoring toward advanced crash-avoidance and vulnerable-road-user protection functions. UNECE Regulation No. 171 establishes a regulatory structure for Driver Control Assistance Systems. Together, these frameworks increase the installed base of vehicles capable of supporting monetizable software layers across multiple geographic markets.

Software-enabled ADAS packages can lift per-vehicle lifetime revenue by several hundred dollars while improving gross margins. Lower incremental delivery cost and lower customer acquisition expense relative to traditional hardware sales drive this margin advantage. Tiered highway-assist packages, parking automation bundles, and subscription-based safety upgrades each represent a distinct revenue event. This means a single vehicle generates multiple commercial transactions over its lifecycle rather than a one-time bill-of-materials sale.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Paid ADAS feature unlocks | +2.2% | North America, EU, China, Japan | Short term |

| Commercial vehicle ADAS scaling | +1.8% | EU, North America, China | Medium term |

| Emerging-market retrofit safety kits | +1.4% | India, ASEAN, LATAM, MEA | Short term |

| Low-cost ADAS for mass EV platforms | +2.0% | China, EU, Southeast Asia | Medium term |

| Driving-data monetization layers | +1.1% | North America, EU, Japan | Medium term |

| ADAS capability roll-up strategy | +1.6% | Europe, North America, Israel, China | Long term |

Regional Analysis

North America Dominates the Advanced Driver Assistance Systems Market with a Market Share of 35.80%, Valued at USD 15.752 Billion

North America holds 35.80% of the global ADAS market, valued at USD 15.752 Billion in 2025. The U.S. FMVSS No. 127 mandate, finalized in 2024, drives near-term procurement across light vehicle programs. Insurance differentiation tied to FCW and AEB-equipped vehicles further extends civilian adoption. This regulatory and financial incentive structure gives North American OEMs and Tier 1 suppliers a defined demand floor through the compliance window ending in 2029.

Europe represents the second major ADAS region. The EU General Safety Regulation mandates fitment of AEB, lane-keeping assist, and driver drowsiness detection across new passenger and commercial vehicles. Euro NCAP 2026 tightens crash-avoidance benchmarks further, including tougher motorcycle detection and junction scenarios. In June 2026, Geely received EU certification for its producer-developed ADAS technology, marking the first Chinese system to meet EU regulatory standards and signaling intensifying competitive pressure on European incumbents.

Asia Pacific represents a structurally important growth region for ADAS. China’s vehicle production scale drives ADAS penetration into volume segments, and Chinese OEMs are standardizing ADAS features across mass-market electric vehicle platforms. Japan and South Korea contribute through export-oriented programs that must meet Euro NCAP and NHTSA benchmarks. This dual compliance requirement pushes APAC suppliers to develop sensor and software stacks validated across multiple regulatory frameworks simultaneously.

Latin America and the Middle East and Africa remain earlier-stage ADAS markets. Neither region has binding federal ADAS mandates equivalent to EU GSR or U.S. FMVSS 127. Retrofit safety kit adoption and imported vehicle content represent the primary ADAS entry channels in these regions. Suppliers targeting Latin America, India, ASEAN, and MEA must localize ADAS algorithms for non-lane-disciplined traffic conditions, which differ structurally from the organized highway environments that current Level 2 systems are optimized for.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Competitive Analysis

Mobileye built its competitive position on integrated EyeQ chip-and-software architecture deployed across global OEM programs. This integration depth creates high switching costs for any OEM that has standardized its perception stack on Mobileye’s platform. However, Mobileye’s January 2026 agreement to acquire Mentee Robotics signals a strategic expansion beyond automotive ADAS into humanoid robotics, which introduces execution risk if engineering resources are split across two hardware-intensive sectors simultaneously.

Robert Bosch GmbH holds a broad hardware and software position across radar, camera, ultrasonic sensors, and domain controllers. This multi-component presence means Bosch captures revenue at several points within a single ADAS-equipped vehicle. In August 2025, indie Semiconductor acquired emotion3D GmbH to bolster perception software capabilities, reflecting competitive pressure on established Tier 1 suppliers to deepen algorithm assets. Bosch’s scale advantage remains real, but software-native challengers are narrowing the perception capability gap.

Key Players

- Altera Corporation

- Autoliv

- DENSO CORPORATION

- Continental AG

- Garmin Ltd.

- Magna International Inc.

- Mobileye

- Robert Bosch GmbH

- Valeo SA

- Wabco Holdings Inc

Recent Developments

- January 2026 – Mobileye announced a definitive agreement to acquire Mentee Robotics Ltd., an AI-first humanoid robotics company, to accelerate its AI and autonomy capabilities across automotive and robotics sectors, with the acquisition expected to close in early 2026.

- December 2025 – HARMAN International, a subsidiary of Samsung Electronics, signed a definitive agreement to acquire the ADAS business of ZF Group for approximately €1.5 Billion, aiming to strengthen its ADAS and centralized compute capabilities.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 44 Billion |

| Forecast Revenue (2035) | USD 189.2 Billion |

| CAGR (2026-2035) | 5.00% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Solution (Adaptive Cruise Control, Blind Spot Detection System, Park Assistance, Lane Departure Warning System, Tire Pressure Monitoring System, Autonomous Emergency Braking, Adaptive Front Lights, Others), By Component (Processor, Sensors [Radar, LiDAR, Ultrasonic, Others], Software, Others), By Vehicle (Passenger Cars, Commercial Vehicle [Light Commercial Vehicle, Heavy Commercial Vehicle]) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Altera Corporation, Autoliv, DENSO CORPORATION, Continental AG, Garmin Ltd., Magna International Inc., Mobileye, Robert Bosch GmbH, Valeo SA, Wabco Holdings Inc |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |