Quick Navigation

Report Overview

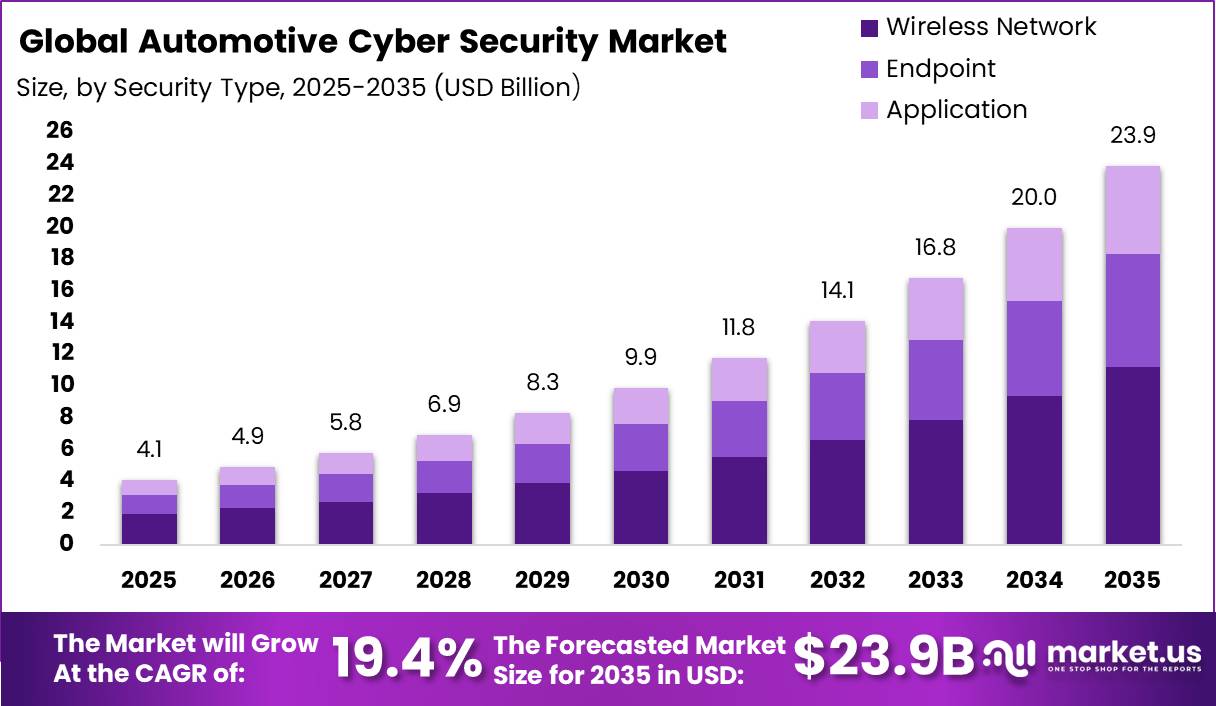

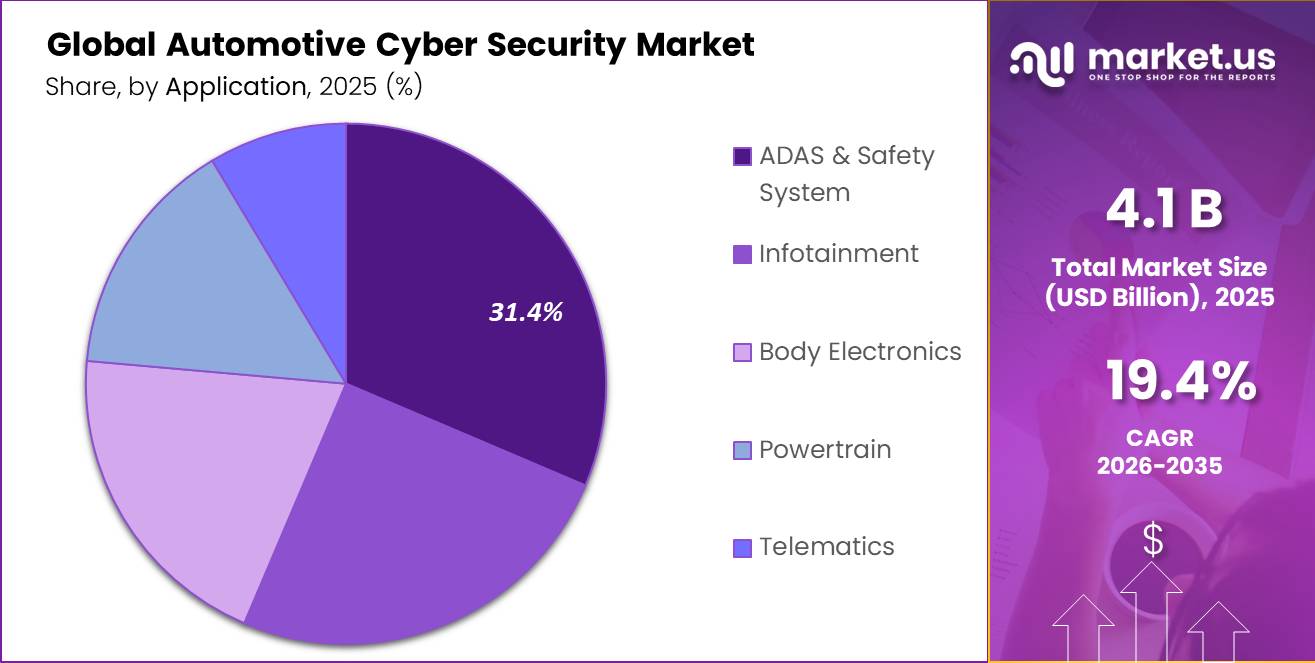

Global Automotive Cyber Security Market size is expected to be worth around USD 23.9 Billion by 2035 from USD 4.1 Billion in 2025, growing at a CAGR of 19.40% during the forecast period 2026 to 2035.

The automotive cyber security market covers technologies and services that protect vehicle electronics, software, communications, and data from unauthorized access and cyberattacks. This market spans in-vehicle security, external cloud protection, and application-layer solutions. It serves passenger car manufacturers, commercial fleet operators, electric vehicle producers, and their extended supplier networks.

Key Takeaways

- Market value in 2025 stands at USD 4.1 Billion, forecast to reach USD 23.9 Billion by 2035.

- The market grows at a CAGR of 19.40% from 2026 to 2035.

- Wireless Network Security dominates the By Security Type segment with a 46.80% share.

- Passenger Cars hold the largest share in the By Vehicle Type segment at 62.70%.

- In-Vehicle Services lead the By Service segment with a 64.90% share.

- ADAS and Safety Systems lead the By Application segment with a 31.40% share.

- North America is the dominant region with a 38.10% market share.

Regulatory mandates are reshaping automotive cybersecurity from an optional investment into a legal baseline requirement. According to the SAE Mobilus research platform, UNECE WP.29 UN-R155 defines 69 specific cybersecurity attack vectors that automakers must assess and mitigate before receiving vehicle type approval. This compels OEMs to purchase structured cybersecurity solutions rather than building ad hoc defenses, creating predictable and recurring vendor revenue.

Data from Blackberry’s global automotive cybersecurity survey shows 95% of security professionals believe software-defined vehicles will significantly increase cybersecurity risks. As reported by Axios, modern connected vehicles already contain more than 100 million lines of software code and up to 100 electronic control units. This complexity gives cybersecurity vendors a structurally larger addressable surface in every new vehicle generation.

This reflects a market where compliance timelines and technical complexity reinforce each other. Vendors who offer integrated platform security covering both ECU-level and cloud-layer threats are better positioned to win multi-year OEM contracts. This signals that point-solution providers face growing pressure to consolidate or specialize to remain competitive.

Security Type Analysis

Wireless Network Security dominates with 46.80% due to broad wireless attack surface across connected fleets.

In 2025, Wireless Network Security held a dominant market position in the By Security Type segment of the Automotive Cyber Security Market, with a 46.80% share. Connected vehicles rely on cellular, Wi-Fi, Bluetooth, and V2X communication channels that each represent a distinct attack pathway. Vendors who provide unified wireless threat management platforms address the widest surface area, making this sub-segment the highest-volume revenue source in the security type category.

Endpoint Security accounts for 30% of the By Security Type segment. This sub-segment protects individual ECUs and onboard computing units from unauthorized access and firmware tampering. As vehicle electronics architectures grow more centralized under software-defined vehicle platforms, endpoint protection requirements extend to domain controllers and central compute nodes, sustaining vendor demand beyond legacy ECU deployments.

Application Security holds a 23.20% share. This sub-segment addresses vulnerabilities in in-vehicle software stacks, telematics applications, and over-the-air update pipelines. Auto-ISAC members represent more than 99% of light-duty vehicles sold in North America, reflecting how industry-wide threat intelligence sharing raises the minimum security standard for application-layer protection and reinforces structured vendor procurement across the supply chain.

Vehicle Type Analysis

Passenger Car dominates with 62.70% due to highest production volume and broadest software integration.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of the Automotive Cyber Security Market, with a 62.70% share. Passenger vehicles carry the highest density of connected features including ADAS, infotainment, telematics, and OTA update systems. This feature density creates the greatest cybersecurity management burden per vehicle, sustaining consistent vendor revenue across model lifecycles.

Commercial Vehicles represent the second sub-segment within the By Vehicle Type category. Fleet operators running logistics, delivery, and public transport services face unique threats related to cargo tracking, route data, and fleet management platforms. Regulatory requirements for commercial fleet data protection are tightening, creating demand for managed security services tailored to high-utilization, always-connected vehicle environments.

Electric Vehicles form the third sub-segment within the By Vehicle Type category. EV architectures introduce dedicated cybersecurity exposure points through charging infrastructure, battery management systems, and bidirectional energy communication protocols. As EV adoption accelerates in North America, Europe, and China, cybersecurity requirements for EV-specific hardware and charging ecosystem interfaces create a structurally distinct and growing procurement category.

Vehicle Analysis

In-Vehicle Services dominates with 64.90% due to direct exposure of onboard systems to cyber threats.

In 2025, In-Vehicle Services held a dominant market position in the By Service segment of the Automotive Cyber Security Market, with a 64.90% share. Security solutions embedded directly within vehicle systems address the most immediate threat layer, covering ECU protection, internal network monitoring, and firmware integrity management. OEMs integrating security at the vehicle hardware level generate repeating service contracts through warranty periods and post-production update cycles.

External Cloud Services form the second sub-segment within the By Service category. Cloud-based security platforms manage fleet-level threat monitoring, OTA update validation, and remote diagnostics for connected vehicle populations. As vehicle fleets grow and data volumes expand, cloud security service providers can scale commercially without proportional increases in hardware deployment costs, strengthening their margin position relative to embedded solution vendors.

Application Analysis

ADAS and Safety System dominates with 31.40% due to direct link between safety failure and liability risk.

In 2025, ADAS and Safety Systems held a dominant market position in the By Application segment of the Automotive Cyber Security Market, with a 31.40% share. Cybersecurity failures in ADAS components can result in physical harm, product recalls, and regulatory penalties, making this the highest-priority protection category for OEMs. Vendors serving this sub-segment face strict functional safety co-requirements, creating high switching costs and long-term contract stability.

Infotainment systems account for 25% of the By Application segment. These systems serve as a common entry vector for attackers due to their broad external connectivity through Bluetooth, USB, and mobile integration. Cybersecurity vendors addressing infotainment vulnerabilities must balance user experience requirements against hardening measures, creating demand for specialized application-layer security tools distinct from safety-critical system protection.

Body Electronics hold a 20% share within the By Application segment. This sub-segment covers door locks, lighting controls, HVAC, and access systems. Unauthorized access to body electronics creates both safety and privacy risks, particularly in fleet and shared mobility contexts. Cybersecurity solutions targeting body electronics are gaining procurement priority as fleet operators formalize security baseline requirements for vehicle access management.

Key Market Segments

By Security Type

- Wireless Network Security

- Endpoint Security

- Application Security

By Vehicle Type

- Passenger Car

- Commercial Vehicle

- Electric Vehicle

By Service

- In-Vehicle Services

- External Cloud Services

By Application

- ADAS and Safety System

- Infotainment

- Body Electronics

- Powertrain

- Telematics

Drivers

Software-defined vehicle architecture is a major long-term driver as vehicle functionality shifts from hardware-centric systems to software-driven platforms. Modern SDVs rely on centralized computing, connected services, OTA updates, and advanced digital features, expanding the potential cyber attack surface. Figures from the World Economic Forum show SDVs are expected to account for more than 90% of future vehicle innovation, making platform-level cybersecurity a procurement baseline rather than an optional add-on.

Key security areas include secure middleware, code integrity verification, identity and access management, runtime protection, and continuous software validation. As vehicles incorporate more software interfaces and update pathways, cybersecurity requirements extend throughout the vehicle lifecycle rather than ending at production. Based on UNECE regulation data, cybersecurity management systems are required across development, production, and post-production phases, sustaining vendor contract duration well beyond vehicle launch dates.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UNECE R155 compliance mandate | +2.9% | EU core, Japan, Korea, UK spill-over | Short term (≤ 2 years) |

| Secure OTA update expansion | +2.3% | North America, EU, China, Korea | Medium term (2-4 years) |

| Software-defined vehicle architecture | +2.1% | North America, EU, China, premium APAC | Long term (≥ 4 years) |

| Post-production VSOC build-out | +1.8% | EU, U.S., Japan, Korea | Medium term (2-4 years) |

| Supplier cyber assurance cascade | +1.7% | APAC supply chains, Mexico, Turkey, EU | Medium term (2-4 years) |

| Connected fleet growth base | +1.4% | Global, led by APAC and North America | Long term (≥ 4 years) |

Restraints

OEM budget concentration is a major restraint as automotive cybersecurity spending competes with investments in electrification, ADAS, software-defined vehicle platforms, and emissions compliance. Under UNECE R155, automakers must secure both CSMS certification and vehicle-level type approval before selling in participating markets. Procurement teams often prioritize solutions that achieve regulatory approval rather than deploying broader cybersecurity capabilities, limiting vendor upsell opportunities across Europe, Japan, South Korea, and North America.

The CSMS certification must also be maintained throughout its validity period, creating recurring compliance obligations that constrain budget flexibility. This results in tighter spending controls, stricter ROI requirements, and reduced opportunities for vendors to expand beyond minimum regulatory scope. Vendors who cannot demonstrate direct compliance value face procurement rejection regardless of their technical capabilities.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM budget concentration | -2.1% | EU core, Japan, Korea, North America | Medium term (2-4 years) |

| Long homologation-led sales cycles | -1.8% | EU regulatory hubs, global OEM programs | Short term (≤ 2 years) |

| Uneven jurisdiction adoption | -1.6% | North America, ASEAN, LATAM, Middle East | Long term (≥ 4 years) |

| Supplier monetization ceiling | -1.4% | APAC supply chains, Mexico, Turkey, EU | Medium term (2-4 years) |

| SDV investment crowd-out | -1.3% | North America, China, EU, premium APAC | Medium term (2-4 years) |

| Geographic production shift mismatch | -1.1% | Europe, North America, APAC corridors | Long term (≥ 4 years) |

Challenges

Post-production monitoring burden is becoming a major operational challenge as automotive cybersecurity regulations extend beyond vehicle development into the entire vehicle lifecycle. Under UNECE R155, manufacturers must maintain cybersecurity detection and response capabilities throughout post-production operation, not only at vehicle launch. This requires continuous monitoring of connected fleets, software-update activities, cybersecurity incidents, and emerging vulnerabilities across vehicle populations of varying software versions.

Automakers must establish dedicated Vehicle Security Operations Centers to manage telemetry analysis, alert triage, threat correlation, and incident response on a continuous basis. The challenge intensifies across Europe, the United States, Japan, and South Korea, where automotive cybersecurity regulations are advancing most rapidly. Organizations must coordinate cybersecurity activities across vehicles, backend platforms, suppliers, and enterprise security teams simultaneously, adding significant ongoing operational cost to vehicle program budgets.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Supplier evidence overload | -1.8% | EU, APAC supply chains, Mexico, Turkey | Medium term (2-4 years) |

| SDV stack complexity | -1.7% | North America, EU, China, Korea | Long term (≥ 4 years) |

| OTA scaling risk | -1.5% | Global connected-vehicle markets | Medium term (2-4 years) |

| Post-production monitoring burden | -1.4% | EU, U.S., Japan, Korea | Medium term (2-4 years) |

| Cyber talent bottleneck | -1.3% | Global OEM hubs, Israel, India, EU | Long term (≥ 4 years) |

| Audit and documentation sprawl | -1.1% | EU regulatory hubs, global homologation programs | Short term (≤ 2 years) |

Opportunities

Tier-1 and supplier compliance SaaS is a major opportunity as automotive cybersecurity requirements extend across the supply chain. Under UNECE R155, OEMs must identify, assess, and manage supplier-related cyber risks throughout the vehicle lifecycle. Suppliers must maintain audit trails, cybersecurity documentation, risk assessments, and Software Bill of Materials records, creating demand for productized platforms that automate workflow management, evidence collection, and audit readiness.

A single automotive OEM can oversee hundreds of relevant suppliers, creating a large addressable customer base for compliance software providers. Industry estimates place annual contract values for supplier compliance platforms at approximately USD 25,000 to USD 150,000 per supplier cluster. Adoption is set to accelerate across EU-linked supply chains in APAC, Mexico, Turkey, and Eastern Europe as cybersecurity governance becomes a continuous operational requirement rather than a one-time certification exercise.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Managed vehicle cyber services | +2.7% | EU core, North America, Japan, Korea | Short term (≤ 2 years) |

| Tier-1 and supplier compliance SaaS | +2.2% | EU, APAC supply chains, Mexico, Turkey | Medium term (2-4 years) |

| Fleet SOC and OTA security | +2.0% | North America, EU, GCC, China | Medium term (2-4 years) |

| SDV runtime protection layers | +2.4% | North America, EU, China, Korea | Long term (≥ 4 years) |

| Used-vehicle cyber certification | +1.5% | EU, U.S., Japan, UK | Long term (≥ 4 years) |

| Cybersecurity roll-up platforms | +1.8% | EU, Israel, U.S., Japan | Medium term (2-4 years) |

Regional Analysis

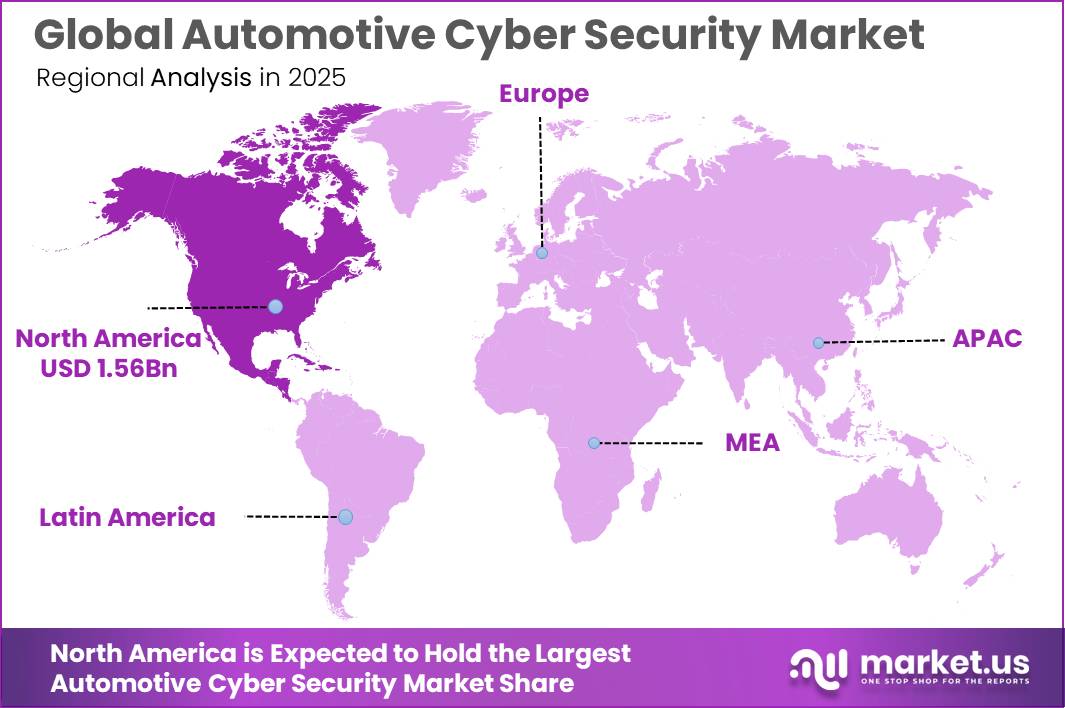

North America Dominates the Automotive Cyber Security Market with a Market Share of 38.10%, Valued at USD 1.56 Billion

North America holds a 38.10% share valued at USD 1.56 Billion, driven by high connected vehicle penetration and the presence of major OEM and Tier-1 supplier ecosystems. Intel data shows connected vehicles generate up to 25 GB of data per hour, amplifying demand for cloud-connected security infrastructure across North American fleets. In January 2025, VicOne and MediaTek demonstrated xCarbon at CES 2025 to secure vehicle telematics and V2X communications, reflecting active innovation investment in this region.

Europe holds the second-largest regional position, anchored by the UNECE WP.29 UN-R155 regulation that mandates cybersecurity management systems for all new vehicles sold in participating markets. German, French, and UK OEMs are among the first to embed compliance frameworks into vehicle development programs, creating steady procurement cycles for certified cybersecurity vendors. Regulatory enforcement timelines in Europe continue to compress the window for non-compliant vehicle programs.

Asia Pacific is the fastest-growing regional market, driven by high vehicle production volumes in China, Japan, South Korea, and India alongside expanding connected vehicle ecosystems. China’s rapid EV adoption introduces dedicated cybersecurity requirements for vehicle-to-grid and charging infrastructure interfaces. Japan and South Korea bring mature Tier-1 supplier networks already beginning UNECE-aligned compliance programs, widening the addressable vendor market across the region.

Latin America and the Middle East and Africa represent earlier-stage adoption regions. Both regions lack mandatory cybersecurity vehicle regulations at the scale of UNECE markets, slowing structured procurement. However, fleet operators in the GCC and Brazil are beginning to adopt managed vehicle security services as fleet digitization expands. This creates an early-mover opportunity for vendors willing to build regional partnerships ahead of formal regulatory mandates.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Competitive Analysis

Sheelds positions itself as a specialist in automotive-grade intrusion detection and network monitoring for in-vehicle environments. ENISA threat landscape data shows supply-chain attacks accounted for 40% of observed cyber incidents across connected industries. Sheelds’ focus on real-time ECU-level anomaly detection targets the highest-risk layer for OEMs managing large supplier networks, giving it a defensible niche against broader platform vendors.

Vector Informatik GmbH provides development tools, network analysis software, and cybersecurity testing solutions deeply embedded in OEM vehicle development workflows. IBM’s 2024 data breach report places the global average breach cost at USD 4.88 Million, underscoring the financial stakes that push OEMs toward verified, pre-production security integration. Vector’s early-stage toolchain positioning means its solutions address compliance requirements before vehicles reach production, reducing OEM exposure to post-launch cybersecurity liabilities.

Key Players

- Sheelds

- Vector Informatik GmbH

- NXP Semiconductors N.V.

- Harman International

- Broadcom Inc.

- Denso Corporation

- Honeywell International, Inc.

- Guard Knox Cyber-Technologies Ltd.

Recent Developments

- January 2024 – During Pwn2Own Automotive 2024, security researchers uncovered 49 unique zero-day vulnerabilities across automotive systems and received USD 1.32 Million in total awards, highlighting the scale of unresolved attack surfaces in connected vehicle platforms.

- December 2025 – ETAS announced a collaboration with Microsoft to bring its automotive software development and security tools to Microsoft Azure, supporting secure cloud-based vehicle software engineering and lifecycle management across OEM programs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.1 Billion |

| Forecast Revenue (2035) | USD 23.9 Billion |

| CAGR (2026-2035) | 19.40% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Security Type (Wireless Network Security, Endpoint Security, Application Security), By Vehicle Type (Passenger Car, Commercial Vehicle, Electric Vehicle), By Service (In-Vehicle Services, External Cloud Services), By Application (ADAS and Safety System, Infotainment, Body Electronics, Powertrain, Telematics) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Sheelds, Vector Informatik GmbH, NXP Semiconductors N.V., Harman International, Broadcom Inc., Denso Corporation, Honeywell International Inc., Guard Knox Cyber-Technologies Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The automotive cybersecurity market involves the development and implementation of security measures to protect vehicles and their electronic systems from cyber threats and attacks.

Automotive cybersecurity is essential in protecting modern vehicles' increasing array of electronic systems and connectivity features from potential cyber threats that could compromise safety, data privacy, or vehicle functionality.

The global Automotive Cyber Security market is anticipated to be USD 22.2 billion by 2032. It is estimated to record a steady CAGR of 22% in the review period 2023 to 2032. It is likely to total USD 3.9 billion in 2023.

Need for Automotive Cybersecurity

Automotive cybersecurity is important to protect vehicles from cyberattacks, which can have serious consequences, including:

- Loss of control of the vehicle

- Access to sensitive data, such as personal information or financial data

- Theft of the vehicle

- Damage to infrastructure

- Injuries or deaths

Key challenges facing vehicle systems today include increasing complexity, connected and autonomous vehicle technology development, the need for industry-wide cybersecurity standards and sophisticated cyber threats against automotive systems.

Top 3 Targeted Industries for Cybersecurity

- Healthcare

- Financial services

- Government

Automotive cybersecurity markets play an integral part in maintaining consumer trust in vehicle safety and data privacy, encouraging innovation within secure connected vehicle technologies, as well as contributing to industry-wide cybersecurity regulations and standards.