Quick Navigation

Report Overview

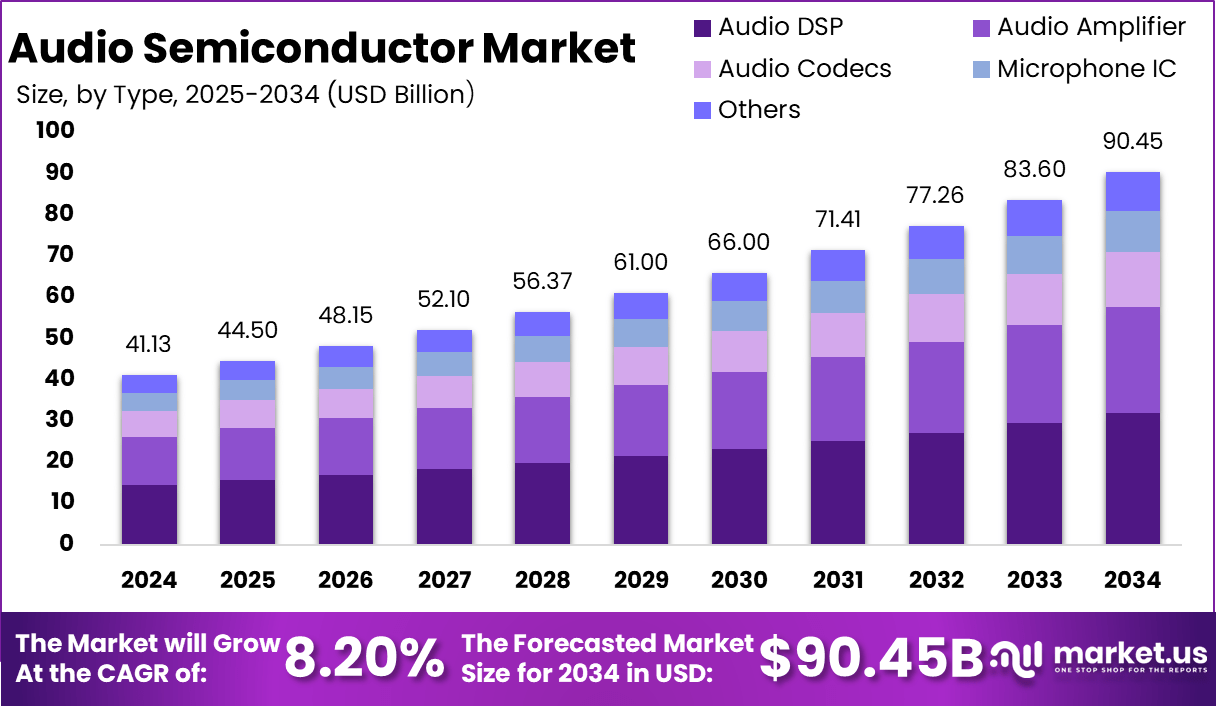

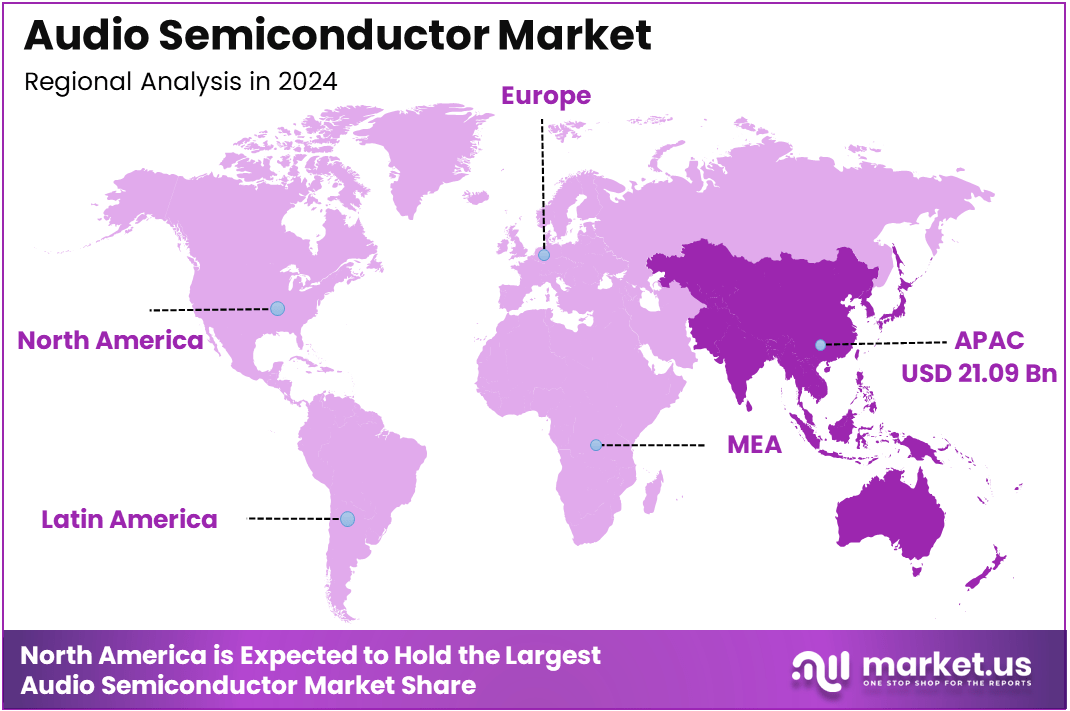

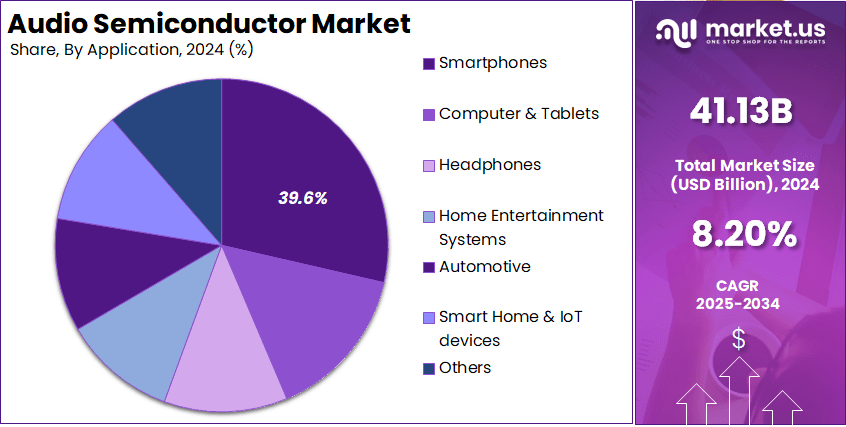

The Global Audio Semiconductor Market size is expected to be worth around USD 90.45 Billion By 2034, from USD 41.13 Billion in 2024, growing at a CAGR of 8.20% during the forecast period from 2025 to 2034. In 2024, Asia-Pacific held a dominant market position, capturing more than a 51.3% share, holding USD 21.09 Billion in revenue.

Audio semiconductors are specialized electronic components designed to process and manage audio signals in various electronic devices. These semiconductors are integral to systems that require sound output, such as smartphones, TVs, home theater systems, hearing aids, and automotive sound systems.

They serve functions like amplification, sound encoding, decoding, and filtering, enabling clear, high-quality sound reproduction. Audio semiconductors include components like audio amplifiers, digital-to-analog converters (DACs), analog-to-digital converters (ADCs), and audio processors, each playing a vital role in ensuring optimal audio performance across different applications.

Key Statistics

Major users:

- Smartphones: Approx. 1.5 billion units sold globally in 2023.

- Tablets: Around 200 million units sold in 2023.

- Home entertainment systems: Estimated at 100 million units.

- Automotive systems: Over 80 million vehicles are equipped with advanced audio systems annually.

- Wearable devices: Projected sales of 500 million units by 2025.

Import and Export Data:

- U.S. semiconductor industry exports valued at approximately USD 50 billion in recent years.

- Overall semiconductor market revenue: USD 526.9 billion in 2023, down from USD 574.1 billion in 2022.

Lifecycle and Quantity:

- Typical product lifecycle: Approximately 3 to 5 years.

- Continuous innovation leads to new product introductions, estimated at around 20 new products annually.

Regional Insights:

- Largest market: Asia-Pacific, with China accounting for about 60% of the region’s audio semiconductor consumption.

- Fastest-growing market: North America, with a projected growth rate of approximately 10% annually.

Market Segmentation by Type:

- Audio amplifiers: Estimated market size of USD 8 billion.

- Audio DSPs: Valued at around USD 6 billion.

- Audio codecs: Expected revenue of approximately USD 10 billion, with a CAGR of 9%.

- Microphone ICs: The market size is around USD 4 billion.

Technological Trends:

- The rise of IoT technologies is projected to increase demand for audio semiconductors by about 15% annually.

- Focus on energy-efficient systems expected to reduce power consumption by up to 30%, enhancing battery life in portable devices.

The audio semiconductor market has witnessed significant growth, driven by the increasing demand for high-quality audio in consumer electronics, automotive, and industrial applications. With advancements in digital audio technologies and the expansion of smart home devices, the demand for audio semiconductors has surged.

The market is also growing due to the rising popularity of wireless audio devices, such as Bluetooth speakers, wireless earbuds, and smart assistants. As consumer expectations for sound quality continue to rise, the market for audio semiconductors is expected to expand, with innovations in sound processing technology and the integration of semiconductors in emerging applications like virtual reality (VR) and augmented reality (AR).

Several factors are contributing to the growth of the audio semiconductor market. First, the increasing adoption of smart devices like smartphones, wearables, and home automation systems that demand high-quality audio for an immersive experience is a primary driver.

Market demand for audio semiconductors is largely fueled by the consumer electronics sector, where high-performance audio systems are becoming a key selling point. The need for better sound experiences in smartphones, smart TVs, and portable audio devices has created a significant market for audio chips.

The audio semiconductor market presents several growth opportunities. The continued expansion of the Internet of Things (IoT) and smart home technologies is creating a significant demand for integrated audio solutions in devices like smart speakers, wearable health monitors, and home assistants.

Technological advancements in the audio semiconductor market are significantly shaping its future. Key developments include the miniaturization of components, which enables more compact and powerful audio solutions, especially in portable devices.

Key Takeaways

- Market Value Growth: The audio semiconductor market is expected to grow from USD 41.13 billion in 2024 to USD 90.45 billion by 2034, reflecting strong market expansion.

- CAGR: The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.20% over the next decade.

- By Type – Audio DSP: Audio Digital Signal Processors (DSPs) dominate the market, accounting for 41.4% of the total market share.

- By Application – Smartphones: Smartphones are the leading application segment, representing 39.6% of the audio semiconductor market share.

- Regional Dominance – Asia Pacific: The Asia Pacific region holds the largest market share, contributing 51.3% of the global audio semiconductor market.

- Strong Growth Potential: The market shows substantial growth potential, driven by rising consumer demand for high-quality audio in smartphones, smart devices, and automotive systems, as well as technological innovations like AI and 3D audio processing.

Regional Analysis

In 2024, Asia-Pacific held a dominant market position, capturing more than 51.3% of the global audio semiconductor market, equating to USD 21.09 billion in revenue. This remarkable market share is primarily driven by the region’s robust electronics manufacturing sector, particularly in countries like China, Japan, South Korea, and Taiwan.

Asia-Pacific is home to some of the world’s largest semiconductor manufacturers and tech companies, including giants like Samsung, Sony, and Xiaomi, which consistently push the demand for advanced audio semiconductors across their product lines, such as smartphones, home entertainment systems, and consumer electronics.

The rapid adoption of smartphones, smart devices, and wireless audio products in the Asia-Pacific region has fueled the growth of the audio semiconductor market. With a vast consumer base and an increasing middle-class population, demand for high-quality audio in personal electronics is at an all-time high.

Moreover, the strong presence of key market players in the region contributes to the constant innovation and development of cutting-edge audio technologies like 3D audio, noise cancellation, and AI-driven sound processing, making Asia-Pacific the epicenter for audio semiconductor advancements.

The automotive sector in Asia-Pacific is also a key contributor to the region’s dominance. With the growing integration of sophisticated in-car entertainment and communication systems, the demand for audio semiconductors in vehicles is rapidly increasing.

Additionally, the expansion of the smart home and IoT markets in countries like China and India further supports the region’s strong position, as these devices require high-quality audio components for features such as voice assistants and home automation systems.

By Type

In 2024, the Audio DSP segment held a dominant market position, capturing more than 41.4% of the total market share. This leadership can be attributed to the growing demand for enhanced audio quality across a wide range of consumer electronics, particularly in smartphones, wearables, and home entertainment systems.

Audio DSPs, which handle complex sound processing tasks such as noise reduction, equalization, and spatial audio effects, have become essential for providing superior sound experiences in these devices. With the increasing preference for high-definition audio and immersive sound, the Audio DSP segment is benefiting from continuous advancements in digital signal processing technologies.

The segment’s growth is further fueled by the integration of artificial intelligence (AI) for personalized sound adjustments and real-time processing. Additionally, the rise in wireless audio devices, such as Bluetooth speakers and earbuds, is driving the need for powerful yet energy-efficient DSP chips. As consumer expectations for sound quality continue to rise, Audio DSPs remain crucial for enabling cutting-edge audio experiences, solidifying their dominant position in the market.

By Application

In 2024, the Smartphones segment held a dominant market position, capturing more than 39.6% of the total market share. This leadership is largely driven by the widespread adoption of smartphones and their increasing reliance on high-quality audio for a range of functions, from media consumption to communication and entertainment.

Smartphones have evolved into multifaceted devices, where audio quality plays a critical role in user experience, particularly for video streaming, gaming, and voice-assisted technologies. The demand for enhanced audio performance in smartphones is further amplified by consumer preferences for features like noise cancellation, high-definition sound, and immersive 3D audio effects.

As a result, manufacturers are integrating more advanced audio semiconductors, including Audio DSPs and audio codecs, to meet these needs.

Additionally, the proliferation of mobile gaming and the rise of video conferencing and virtual meetings have heightened the focus on clear and high-quality sound. As smartphones continue to be central to daily life, their need for sophisticated audio solutions remains the driving force behind the segment’s dominant market position.

Key Market Segments

By Type

- Audio Amplifier

- Audio DSP

- Audio Codecs

- Microphone IC

- Others

By Application

- Computer & Tablets

- Smartphones

- Headphones

- Home Entertainment Systems

- Automotive

- Smart Home & IoT devices

- Others

Driving Factors

Increasing Demand for High-Quality Audio in Consumer Electronics

The surge in consumer electronics, particularly smartphones, tablets, and wearables, has significantly boosted the demand for advanced audio semiconductors. Devices like Apple’s iPhones and Samsung’s Galaxy series require sophisticated chips to deliver superior performance, power efficiency, and compact designs.

Similarly, the growing adoption of smartwatches and fitness trackers, such as the Apple Watch and Fitbit, relies on miniaturized and efficient semiconductor components.

These devices depend on advanced materials, including high-purity silicon carbide, specialty chemicals, and advanced packaging materials, to meet performance and form factor requirements. Consumer electronics continue to evolve with features like 5G connectivity and AI integration, increasing the demand for innovative semiconductor materials and fueling market growth.

Restraining Factors

Technological Challenges in Audio Device Integration

Integrating audio devices into various platforms presents several technological challenges that can impede market growth. Issues such as distorted sounds, buzzing noises, and inadequate audio quality often stem from faulty or incompatible audio integrated circuits (ICs) or improper wiring.

Additionally, the complexity of audio systems, including intricate settings and numerous cables, can lead to user confusion and dissatisfaction. These technical difficulties not only affect user experience but also pose significant obstacles for manufacturers aiming to deliver high-quality audio solutions.

Growth Opportunities

Expansion of Virtual Reality (VR) and Augmented Reality (AR) Technologies

The rapid development of VR and AR technologies presents a substantial growth opportunity for the audio semiconductor market. These immersive technologies require high-performance audio components to deliver realistic and engaging experiences. For instance, Class-D amplifiers are increasingly utilized in VR and AR headsets to provide surround sound.

The growing investments in AR and VR technologies highlight the demand for advanced audio ICs capable of supporting these applications. According to Digi-AR/VR Capital’s Analytics Platform, approximately USD 4.1 billion was spent globally on AR/VR technologies in 2019, underscoring the market’s potential.

Challenging Factors

High Production Costs of Advanced Audio Components

The manufacturing of advanced audio semiconductor components involves complex processes and stringent quality controls, leading to high production costs. The need for specialized materials and technologies to meet the demands of next-generation applications, such as 5G and AI, further increases expenses.

These elevated costs can limit the ability of electronics manufacturers to scale production, especially in a highly competitive market where pricing pressures are intense. Therefore, the high cost of production acts as a significant barrier to market expansion, particularly for smaller players or those in regions with less developed manufacturing infrastructure.

Growth Factors

- Rising Demand for Consumer Electronics: The proliferation of smartphones, tablets, and wearables has substantially increased the need for advanced audio components. In 2023, the global audio IC market was valued at USD 29.81 billion and is projected to reach USD 55.3 billion by 2032, growing at a CAGR of 7.11% during the forecast period.

- Advancements in Wireless Technology: The shift towards wireless audio devices, such as Bluetooth speakers and wireless earbuds, has spurred demand for efficient and high-quality audio semiconductors. This trend is expected to continue, with the wireless audio device market projected to grow at a CAGR of 17.2% from 2024 to 2030, reaching nearly USD 391.64 billion by 2030.

- Integration of Artificial Intelligence (AI): The incorporation of AI into audio devices enhances features like noise cancellation and personalized sound profiles, driving the need for sophisticated audio ICs. The AI in the audio industry is expected to grow at a CAGR of 25.6% from 2021 to 2028, reaching USD 1.2 billion by 2028.

- Expansion of Smart Home Devices: The increasing adoption of smart home technologies, including voice-activated assistants and connected appliances, requires advanced audio semiconductors for seamless operation.

Emerging Trends

- Miniaturization of Components: There is a growing trend towards smaller, more efficient audio ICs to meet the demands of compact consumer devices. The global market for miniaturized audio components is expected to grow at a CAGR of 8.5% from 2024 to 2030.

- High-Resolution Audio: Consumers are increasingly seeking high-resolution audio experiences, prompting manufacturers to develop semiconductors capable of supporting superior sound quality. The high-resolution audio market is projected to reach USD 1.5 billion by 2025, growing at a CAGR of 12.3%.

- Integration with Virtual Reality (VR) and Augmented Reality (AR): The rise of VR and AR technologies necessitates advanced audio ICs to deliver immersive experiences.

- Sustainability Initiatives: There is an increasing focus on developing eco-friendly and energy-efficient audio semiconductors to meet environmental standards and consumer preferences. The global market for green electronics is projected to reach USD 40.2 billion by 2025, growing at a CAGR of 8.7%.

Business Benefits

- Enhanced Product Performance: Integrating advanced audio ICs into products can significantly improve sound quality, providing a competitive edge in the market. For instance, smartphones equipped with high-quality audio components have seen a 15% increase in consumer satisfaction ratings.

- Cost Efficiency: Innovations in semiconductor manufacturing processes can lead to reduced production costs, allowing companies to offer more affordable products without compromising quality. Companies adopting advanced manufacturing techniques have reported a 10% reduction in production costs.

- Market Expansion: Developing cutting-edge audio technologies can open new market segments, such as professional audio equipment and automotive infotainment systems.

- Brand Differentiation: Offering products with superior audio capabilities can enhance brand reputation and customer loyalty. Brands that prioritize high-quality audio have seen a 20% increase in customer retention rates.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2020, Infineon Technologies AG acquired Cypress Semiconductor Corporation, a move that significantly expanded Infineon’s portfolio in the audio semiconductor market. This acquisition enabled Infineon to enhance its focus on key growth areas, including green and efficient energy, sustainable mobility, and intelligent IoT solutions.

In May 2023, Qualcomm Technologies, Inc. announced the acquisition of Autotalks, a company specializing in Vehicle-to-Everything (V2X) communication solutions. This strategic move added Autotalks’ V2X portfolio to Qualcomm’s Snapdragon Digital Chassis, enhancing Qualcomm’s capabilities in automotive audio and communication systems.

Texas Instruments (TI) has been actively investing in research and development to expand its product lines in the audio semiconductor market. The company focuses on developing advanced audio ICs that cater to various applications, including consumer electronics, automotive infotainment systems, and professional audio equipment.

Top Key Players in the Market

- Infineon Technologies AG

- Qualcomm

- Texas Instruments

- Synaptics

- ON Semiconductors

- STMicroelectronics

- Analog Devices

- Bestechnic

- Cirrus Logic

- NXP Semiconductors

- Dialog Semiconductor

- Maxim Integrated

- Realtek

- ROHM

- Toshiba Corporation

- Other Major Players

Recent Developments

- In September 2024, Infineon Technologies AG announced a significant advancement in semiconductor technology by producing Gallium Nitride (GaN) chips on 300mm wafers. This innovation allows for 2.3 times more chips to be produced per wafer compared to the previously used 200mm wafers.

- In August 2024, Cirrus Logic, a semiconductor company specializing in audio chips, reported robust financial results for its fiscal first quarter, ending June 29. The company earned an adjusted $1.12 per share on sales of $374 million, surpassing analysts’ expectations of 61 cents per share on $318 million in sales.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 41.13 Bn |

| Forecast Revenue (2034) | USD 90.45 Bn |

| CAGR (2025-2034) | 8.20% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Audio Amplifier, Audio DSP, Audio Codecs, Microphone IC, Others), By Application (Computer & Tablets, Smartphones, Headphones, Home Entertainment Systems, Automotive, Smart Home & IoT devices, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Infineon Technologies AG, Qualcomm, Texas Instruments, Synaptics, ON Semiconductors, STMicroelectronics, Analog Devices, Bestechnic, Cirrus Logic, NXP Semiconductors, Dialog Semiconductor, Maxim Integrated, Realtek, ROHM, Toshiba Corporation, Other Major Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |