Quick Navigation

Report Overview

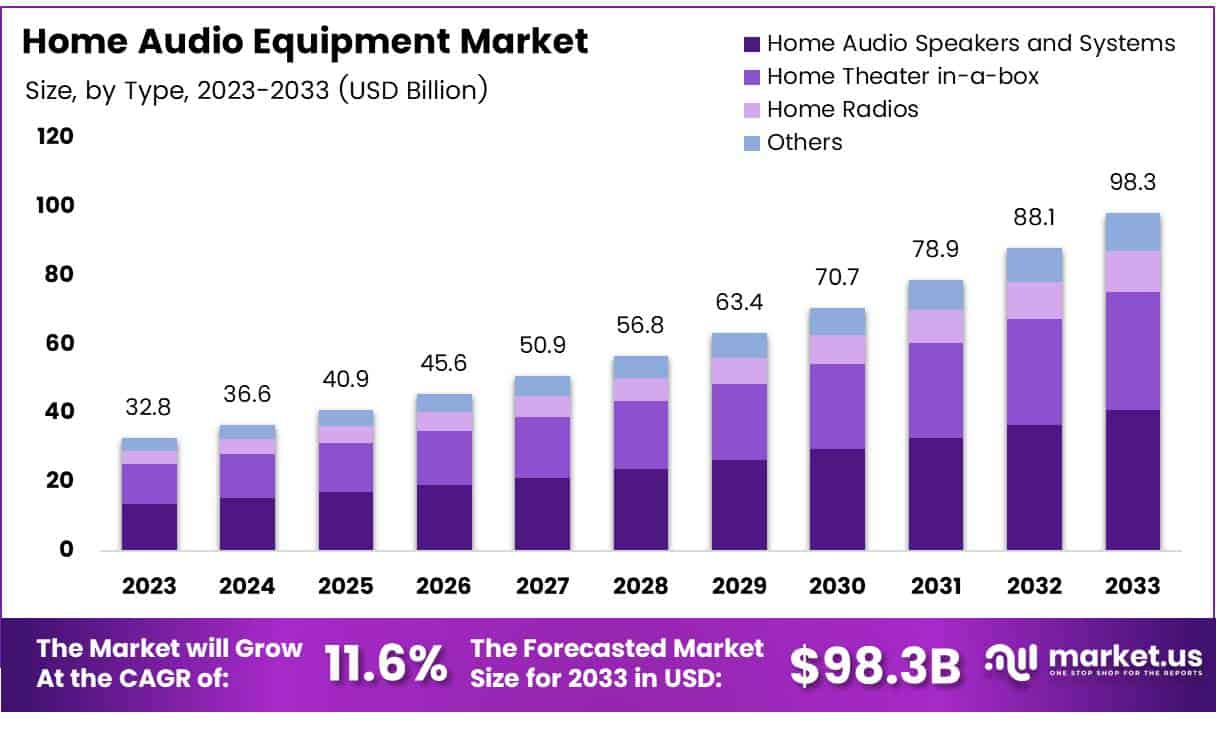

The Global Home Audio Equipment Market size is expected to be worth around USD 98.3 Billion by 2033, from USD 32.8 Billion in 2023, growing at a CAGR of 11.6% during the forecast period from 2024 to 2033.

Home Audio Equipment comprises devices designed to reproduce, amplify, and deliver sound for home entertainment. This category includes a broad spectrum of products such as speakers, soundbars, headphones, and audio systems that enhance the audio experience in residential settings.

The Home Audio Equipment Market refers to the economic landscape encompassing the manufacture, distribution, and sale of these audio devices. It encompasses both traditional consumer electronics vendors and emerging tech companies that innovate and drive trends within this sector.

The Home Audio Equipment Market is experiencing significant growth, driven by innovations in wireless technology and consumer demand for high-quality home entertainment solutions. The integration of smart technology, such as voice-controlled assistants, has expanded the functionality of home audio devices, making them central to the smart home ecosystem.

This convergence of audio quality and smart tech is creating new opportunities for manufacturers and vendors in the space. Additionally, the shift towards streaming services has bolstered the market, as consumers seek superior sound experiences to complement their digital content consumption.

Government investments and regulatory frameworks significantly impact the Home Audio Equipment Market. Regulations pertaining to wireless technology, energy consumption, and material use influence product design and market entry strategies.

Furthermore, government initiatives to support technological advancements in consumer electronics indirectly benefit the home audio sector by facilitating infrastructure improvements and fostering a conducive environment for innovation.

These regulatory and investment landscapes ensure that products not only meet consumer expectations for functionality and sustainability but also adhere to safety and environmental standards.

According to a recent survey, the headphone market has shown robust growth, with total sales anticipated to surpass one billion units by 2024. This surge reflects an increasing consumer preference for personal audio consumption, driven by mobile technology and streaming services.

Similarly, the stereo speaker industry has witnessed substantial growth, with projected revenues reaching approximately 26.5 billion U.S. dollars in 2024. This trend underscores a robust demand for high-quality audio experiences in home settings.

The Audio & Visual Equipment Rental industry in the US has expanded at an average annual rate of 4.5% between 2018 and 2023, indicating a growing preference for access over ownership among consumers, particularly in urban and tech-savvy demographics.

Furthermore, digital consumption habits are also evolving; as of early 2023, 75% of Americans ages 12 and older have engaged with online audio in the past month, with 70% listening in the past week. Additionally, nearly 105 million people in the United States, or 30% of the population, have used smart speakers monthly in 2023.

Key Takeaways

- The global home audio equipment market is projected to reach USD 98.3 billion by 2033, growing from USD 32.8 billion in 2023 at a CAGR of 11.6%.

- Home Audio Speakers and Systems led the market in 2023, holding a 34.9% share, driven by innovations in sound technology and demand for high-quality audio.

- Wireless technology dominated the market in 2023, due to consumer preference for convenience and flexibility.

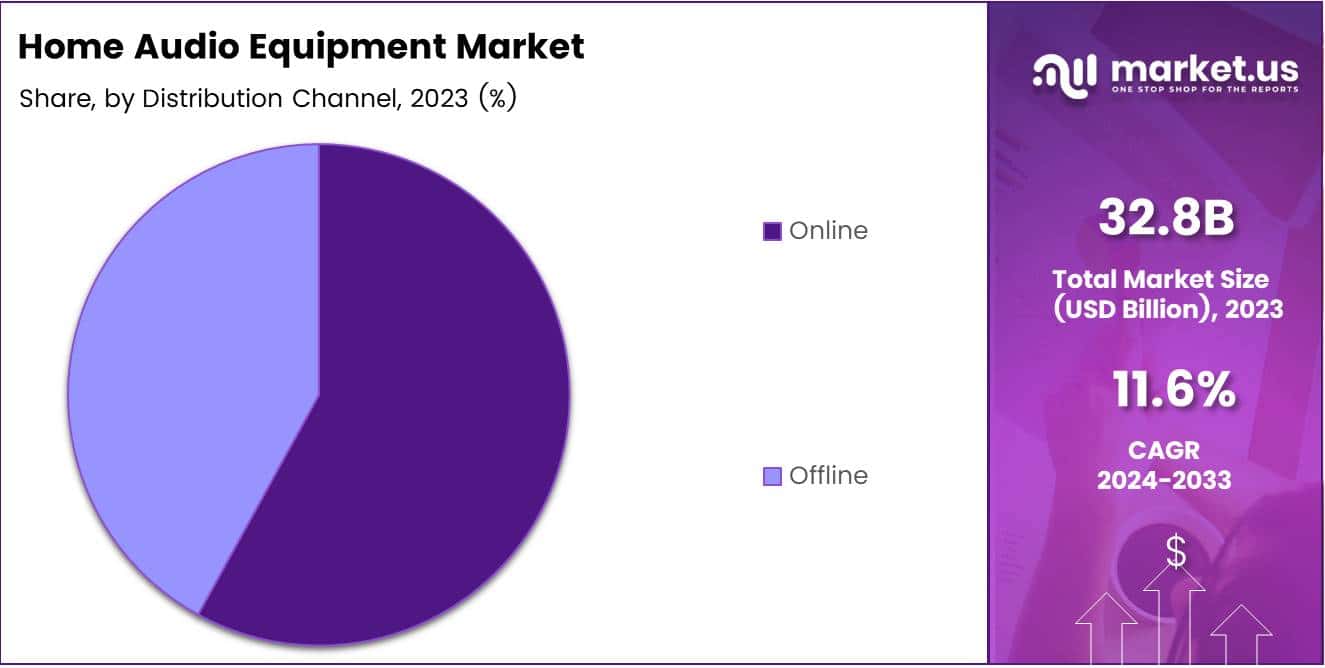

- Online channels represented the leading distribution channel in 2023, with a significant share of overall sales, reflecting the growth of e-commerce and consumer shopping preferences.

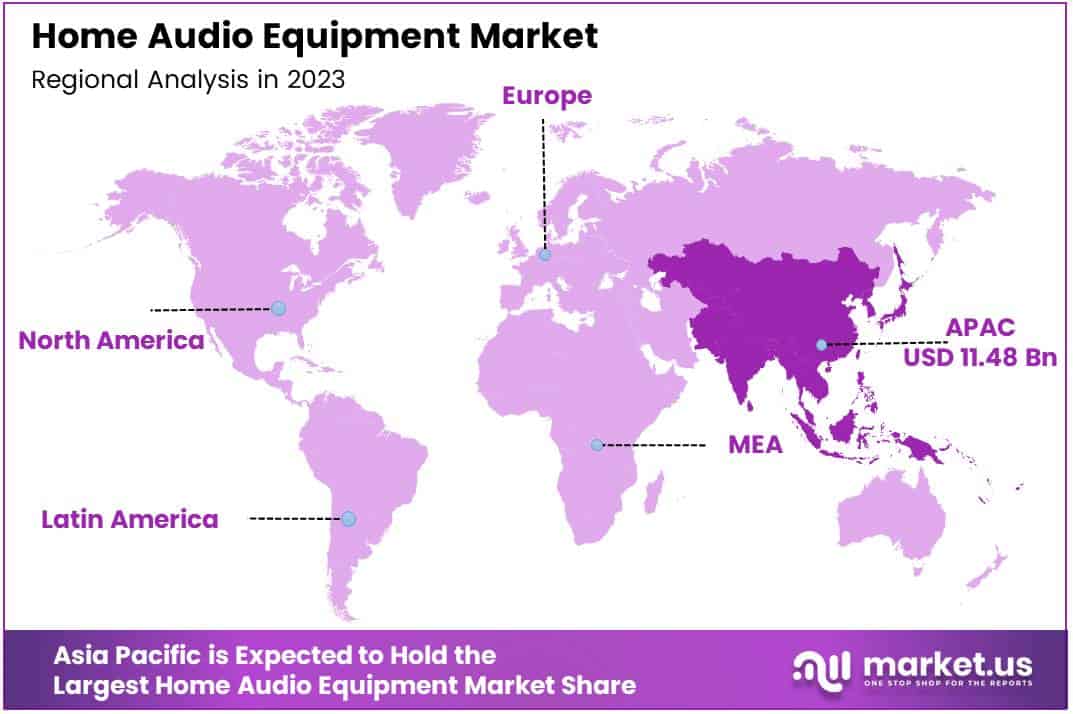

- Asia Pacific held the largest market share in 2023 at 35.8%, valued at approximately USD 11.48 billion, supported by rapid urbanization and growing disposable incomes.

Type Analysis

Home Audio Market Dominated by Speakers with 34.9% Share in 2023

In 2023, Home Audio Speakers and Systems held a dominant market position in the By Type Analysis segment of the Home Audio Equipment Market, with a 34.9% share. This segments robust performance can be attributed to ongoing innovations in sound technology and increasing consumer demand for high-quality audio experiences at home.

Home Theater in-a-box followed, leveraging its compact design and all-inclusive features, appealing to consumers seeking a theater-like audio experience without the complexity of traditional setups. Home Radios, though possessing a smaller market share, continued to find a niche among consumers who prefer classic and straightforward listening solutions.

The Others category, which includes specialized audio equipment like multi-room audio systems, showed potential for growth as consumers increasingly opt for customized audio solutions tailored to their individual preferences and home layouts. Together, these segments underscore a dynamic market landscape driven by diverse consumer needs and technological advancements.

Technology Analysis

Wireless Technology Dominates the Home Audio Equipment Market in 2023

In 2023, wireless technology held a dominant market position in the By Technology Analysis segment of the home audio equipment market. This dominance can be attributed to the growing consumer preference for convenience and flexibility in home entertainment systems.

Wireless audio solutions, such as Bluetooth, Wi-Fi, and other streaming protocols, offer significant advantages in terms of ease of installation, mobility, and the elimination of complex cable setups. The rise in smart homes and integration with IoT devices has further fueled the adoption of wireless home audio solutions, with seamless connectivity being a key driver for consumers.

In contrast, the wired segment, while still holding a significant share of the market, has witnessed a gradual decline in popularity. Despite its robustness in delivering high-quality audio and reliable performance, wired systems are often perceived as less convenient and aesthetically appealing due to the limitations posed by cables and the need for physical connections.

As consumer demand shifts toward more flexible, space-efficient solutions, the wired technology segment is expected to experience slower growth relative to its wireless counterpart in the coming years.

Distribution Channel Analysis

Online Distribution Channel Dominates the Home Audio Equipment Market in 2023

In 2023, online channels held a dominant position in the By Distribution Channel Analysis segment of the Home Audio Equipment Market, accounting for a significant share of overall sales. The continued expansion of e-commerce platforms and the growing consumer preference for the convenience of online shopping have contributed to this trend.

The ease of comparing product features, prices, and customer reviews online has further fueled the growth of online sales, particularly for home audio systems that require detailed research before purchase. Additionally, the availability of multiple payment options, coupled with attractive online-exclusive discounts and promotions, has reinforced the shift toward digital purchasing.

Offline distribution channels, however, continue to maintain a presence in the market, particularly through brick-and-mortar retailers and specialty audio stores. Despite the growth of online shopping, physical retail outlets remain important for consumers who prefer to experience products firsthand before making a purchase. I

n 2023, offline sales are expected to account for a smaller, yet substantial portion of the market, driven by in-store demonstrations and personalized customer service that online platforms are not always able to replicate.

Overall, while online distribution channels are forecasted to continue their dominance, offline channels still hold relevance in the overall sales strategy for home audio equipment.

Key Market Segments

By Type

- Home Theater in-a-box

- Home Audio Speakers and Systems

- Home Radios

- Others

By Technology

- Wired

- Wireless

By Distribution Channel

- Online

- Offline

Drivers

Increasing Demand for High-Quality Sound

The demand for high-quality sound systems is growing as more consumers seek premium home audio equipment for enhanced listening experiences. People are no longer satisfied with basic audio setups; they want clearer, richer sound that replicates the theater experience at home.

As a result, sales of high-end sound systems, including speakers, soundbars, and home theater systems, are on the rise.

Alongside this, rising disposable income, especially in emerging economies, is allowing a larger segment of consumers to afford these advanced systems. Moreover, the increasing popularity of smart homes is driving further growth, with consumers seeking home audio equipment that integrates seamlessly with other smart devices. Features like voice control, multi-room audio, and wireless connectivity have become highly desirable.

Additionally, technological advancements, such as Dolby Atmos and high-resolution audio formats, are enhancing audio quality and providing immersive experiences. These innovations are making it easier for consumers to upgrade their home entertainment setups, contributing to a broader market expansion.

Together, these drivers—consumer demand for superior sound, greater affordability, smart home integration, and continuous audio technology improvements—are shaping the growth trajectory of the home audio equipment market.

Restraints

Restraints in the Home Audio Equipment Market

The home audio equipment market faces several challenges that could hinder its growth. One key restraint is the intense competition within the industry. The presence of well-established brands alongside new entrants often leads to aggressive price competition, which can squeeze profit margins for manufacturers.

As companies strive to offer more affordable products, they may find it difficult to maintain profitability while still meeting consumer expectations for quality and innovation.

Another significant challenge is the availability of substitute products. With the rise of portable Bluetooth speakers, wireless headphones, and other personal audio devices, many consumers are opting for these alternatives instead of investing in traditional, fixed home audio systems. These substitutes often offer convenience, portability, and ease of use, which can diminish demand for larger, more permanent home audio setups.

As consumer preferences shift towards these versatile, space-saving options, manufacturers of home audio equipment must find ways to differentiate their products or risk losing market share to these more flexible alternatives. In addition, the rise of streaming services and smart home devices that offer integrated audio solutions presents another obstacle for traditional home audio equipment, which may struggle to offer comparable features or user experiences.

Growth Factors

Growth Opportunities in the Home Audio Equipment Market

The home audio equipment market is experiencing significant growth, driven by several key factors. One major opportunity lies in the growing popularity of smart speakers, like Amazon Echo and Google Home, which have become central to connected home environments.

These devices, equipped with voice-activated controls, enable consumers to integrate audio seamlessly into their daily lives, and the demand for them is expected to continue expanding.

Additionally, the increasing trend of smart homes is creating opportunities for home audio companies to partner with home automation providers. By offering integrated audio systems that work with other smart home devices, manufacturers can cater to consumers seeking a more convenient and immersive home experience. Another growth avenue is the rising demand for wireless audio solutions.

With technologies like Wi-Fi, Bluetooth, and AirPlay, consumers are moving away from traditional wired systems in favor of wireless setups, which offer greater flexibility and ease of use. This shift opens up opportunities for companies to innovate in delivering high-quality, wireless home audio systems that cater to modern consumer preferences for convenience and connectivity.

As these trends continue to evolve, the home audio market is poised to expand further, driven by innovations in smart technology, seamless integration, and consumer demand for flexible, high-performance audio solutions.

Emerging Trends

Key Trends Shaping the Home Audio Equipment Market

The home audio equipment market is being shaped by several innovative trends that reflect consumer preferences for convenience, personalization, and advanced technology. One of the most notable developments is the integration of Artificial Intelligence (AI) into audio devices.

AI-driven features, such as personalized sound adjustments based on user preferences and voice recognition for hands-free control, are becoming increasingly popular as they enhance the overall user experience. Additionally, there is a growing demand for portable and compact audio solutions.

Consumers are looking for high-quality audio products that are not only easy to move and set up but also capable of delivering premium sound performance without taking up excessive space. This shift is prompting manufacturers to innovate with smaller, more efficient designs. Another key trend is the rise of True Wireless Stereo (TWS) systems.

TWS technology, which powers wireless earphones, portable speakers, and stereo systems, is gaining momentum due to its ease of use, improved connectivity, and premium sound quality. The demand for TWS devices has surged, driven by their convenience and ability to eliminate the clutter of traditional wired systems.

These trends highlight a clear consumer preference for more advanced, flexible, and user-friendly audio solutions, creating significant opportunities for growth in the home audio sector. As technology continues to evolve, it is expected that the demand for smarter, more compact, and wire-free audio solutions will persist.

Regional Analysis

Asia Pacific leads home audio equipment market

Asia Pacific leads the market, accounting for 35.8% of the total market share, valued at approximately USD 11.48 billion. The region’s dominance can be attributed to the growing demand for premium sound systems driven by rapid urbanization, increasing disposable incomes, and the rising popularity of home entertainment technologies.

In particular, countries like China, Japan, and India have witnessed significant market expansion due to the increasing adoption of smart homes and advanced audio technologies, such as wireless and surround sound systems.

Regional Mentions:

North America holds a significant share, driven by a mature market in the United States, which is known for its high consumer spending on luxury home entertainment products. A key factor for North America’s growth is the increasing preference for high-fidelity audio equipment, coupled with the rising popularity of streaming services that enhance demand for premium home audio systems.

Europe also maintains a notable share in the market. The demand for home audio equipment is driven by the high adoption rate of advanced audio technologies in Western European countries like Germany, France, and the UK. Consumer preferences in the region are increasingly shifting toward immersive audio experiences, such as Dolby Atmos and high-resolution audio.

The Middle East and Africa (MEA) and Latin America exhibit slower but steady growth, primarily driven by increasing disposable income and the growing preference for entertainment technologies. However, the market in these regions remains relatively smaller in comparison to North America, Europe, and Asia Pacific, with growth largely fueled by emerging economies and improving infrastructure.

Key Regions and Countries covered іn thе rероrt

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The competitive landscape of the global home audio equipment market in 2023 is defined by a diverse set of industry leaders, ranging from established multinational corporations to specialized audio brands.

Key players such as Samsung, Harman International, LG Electronics, Bose Corporation, and Panasonic Holdings continue to dominate, leveraging their strong brand equity and extensive distribution networks. These companies are focusing on enhancing their product portfolios with innovative features such as smart home integration, wireless connectivity, and superior sound quality to meet evolving consumer preferences.

Samsung and LG Electronics maintain a leading position through their integration of advanced technologies such as AI and IoT into home audio solutions, aligning with the growing demand for smart audio systems. Samsung’s continued investment in premium audio technologies, including its soundbars and QLED television sound systems, exemplifies this shift towards offering a holistic home entertainment experience.

Harman International, a subsidiary of Samsung, further strengthens this trend by advancing premium audio solutions, including its JBL and AKG brands, which are known for their high-quality sound and robust product lines in both portable and home audio segments.

Bose remains a pivotal player with its reputation for delivering premium sound quality across various product categories. The company’s strategic focus on personalized sound experiences, including voice-controlled devices and noise-canceling technologies, positions it well for continued market leadership.

Meanwhile, companies like Intex Technologies, Akai, and Nakamichi offer competitive pricing, catering to the budget-conscious segment while still delivering reliable audio performance. Smaller firms such as Vistron and Nice North America are carving out niches with specialized products that appeal to regional markets, particularly in Asia.

Top Key Players in the Market

- SAMSUNG

- HARMAN International

- Intex Technologies

- JVCKENWOOD Corporation

- Akai (inMusic, Inc.)

- Audio Partnership Plc

- Vistron (Dong Guan) Audio Equipment Co., Ltd.

- LG Electronics

- Nakamichi Corporation

- Nice North America

- Panasonic Holdings Corporation

- Bose Corporation

- Dolby Laboratories, Inc.

- XPERI INC

- Koninklijke Philips N.V.

- SHARP CORPORATION

Recent Developments

- In October 2024, Gladia raised $16 million in Series A funding to launch its groundbreaking multilingual real-time audio transcription and analytics engine, designed to enhance accessibility and data processing across multiple languages and industries.

- In September 2024, AI start-up Longform.ai secured €300,000 in funding, aiming to revolutionize the field of audio data analysis by leveraging cutting-edge machine learning techniques to extract valuable insights from spoken content.

- In August 2023, USound received a €10 million minority growth investment to support the development and scaling of its next-generation audio products, which include innovative technologies for improving sound quality and user experience in consumer electronics.

- In August 2024, Puma Private Equity invested £5.5 million into IRIS Audio Technologies, a leader in audio processing and enhancement solutions, helping the company accelerate the rollout of its advanced audio technology products to global markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 32.8 Billion |

| Forecast Revenue (2033) | USD 98.3 Billion |

| CAGR (2024-2033) | 11.6% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Home Theater in-a-box, Home Audio Speakers and Systems, Home Radios, Others), By Technology (Wired, Wireless), By Distribution Channel (Online, Offline) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | SAMSUNG, HARMAN International, Intex Technologies, JVCKENWOOD Corporation, Akai (inMusic, Inc.), Audio Partnership Plc, Vistron (Dong Guan) Audio Equipment Co., Ltd., LG Electronics, Nakamichi Corporation, Nice North America, Panasonic Holdings Corporation, Bose Corporation, Dolby Laboratories, Inc., XPERI INC, Koninklijke Philips N.V., SHARP CORPORATION |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |