Quick Navigation

Report Overview

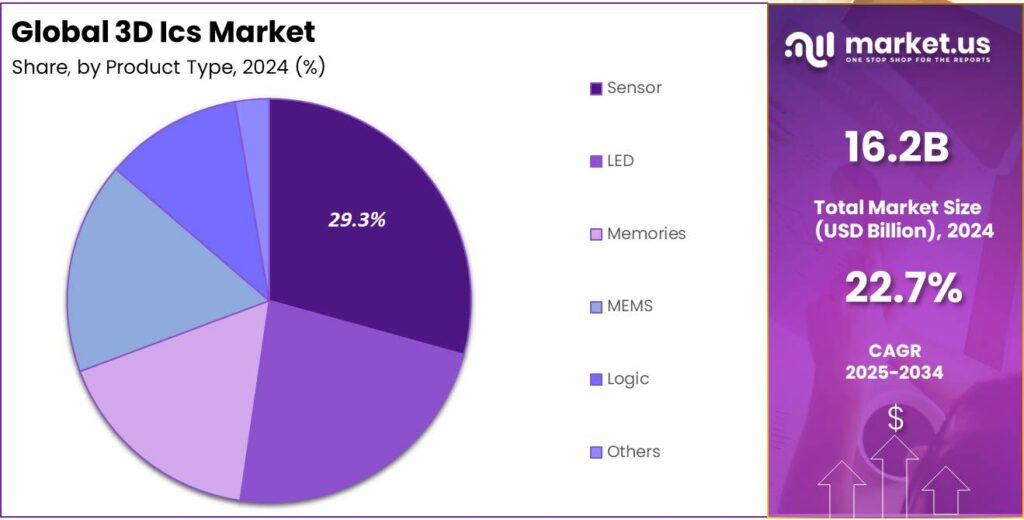

The Global 3D Ics Market size is expected to be worth around USD 125 Billion By 2034, from USD 16.2 Billion in 2024, growing at a CAGR of 22.70% during the forecast period from 2025 to 2034. In 2024, North America held over 39.1% of the global 3D ICs market, generating around USD 6.3 billion in revenue. The U.S. market for 3D ICs was valued at USD 5.70 billion, with a projected CAGR of 20.87%.

Three-dimensional integrated circuits (3D ICs) are an advanced form of microelectronics where multiple layers of active electronic components are vertically stacked. This architecture allows for a denser configuration of components, resulting in smaller, more powerful devices capable of high performance. The integration is achieved through techniques such as TSVs, wafer and microbump bonding, which allow for direct electrical connections across these stacked layers.

The 3D ICs market is experiencing significant growth, driven by the demand for compact, high-performance electronic devices across various sectors, including consumer electronics, automotive, healthcare, and high-performance computing. As traditional planar ICs reach their physical and performance limits, 3D ICs offer a viable solution by enabling faster communication between stacked chips and reducing power consumption.

The primary drivers of the 3D ICs market include the need for greater functionality within smaller devices, lower power consumption, and enhanced performance. The ability to stack ICs vertically significantly reduces the footprint and allows for faster data transfer speeds, which is crucial for applications in mobile devices, AI, data centers, and IoT devices.

Investment in 3D IC technology is growing, as it presents opportunities for innovation in device miniaturization and performance enhancement. However, the technology also comes with risks, particularly in the high costs associated with R&D and manufacturing complexities. The precise alignment and bonding required make the production process challenging and potentially costly.

The growing popularity of 3D ICs is driven by their ability to meet the technological needs of modern electronics. Manufacturers are adopting this technology to address challenges related to size and power constraints. As 3D ICs are increasingly featured in consumer products, their advantages are becoming more widely recognized and valued.

The 3D ICs market offers significant development opportunities, particularly in high-speed data processing and enhanced memory. As industries like VR, AI, and big data analytics advance, demand for 3D ICs is set to rise. Additionally, the drive for smaller, more efficient devices continues to fuel innovation, creating new growth opportunities.

Key Takeaways

- The Global 3D ICs Market size is expected to reach USD 125 Billion by 2034, growing from USD 16.2 Billion in 2024, with a CAGR of 22.70% during the forecast period from 2025 to 2034.

- In 2024, the Sensor segment held a dominant position in the 3D ICs market, capturing more than a 29.3% share.

- The Consumer Electronics segment was also dominant in 2024, holding more than a 36.7% share of the 3D ICs market.

- North America captured more than 39.1% of the global 3D ICs market in 2024, which translated to approximately USD 6.3 billion in revenue.

- In 2024, the U.S. market for 3D Integrated Circuits (3D ICs) was valued at $5.70 billion and is projected to grow at a CAGR of 20.87%.

U.S. 3D Ics Market Size

The U.S. market for 3D Integrated Circuits (3D ICs) reached a valuation of $5.70 billion in 2024. The market is projected to grow at a compound annual growth rate (CAGR) of 20.87%.

This robust growth can be attributed to several factors including advancements in semiconductor technology, increasing demand for electronic devices with higher performance and lower energy consumption, and the growing adoption of 3D ICs in various sectors such as healthcare, automotive, and consumer electronics.

Strategic investments by leading tech firms in 3D IC solutions, along with government initiatives supporting the semiconductor industry, are expected to drive market growth. As technology evolves, the U.S. 3D IC market is set to maintain its growth, fueled by continued advancements and greater integration of electronics in modern devices.

In 2024, North America held a dominant market position in the global 3D ICs industry, capturing more than a 39.1% share, which translated to approximately USD 6.3 billion in revenue. This leadership can be attributed to several key factors that uniquely position North America at the forefront of the semiconductor and electronics sectors.

The region’s robust technological infrastructure and substantial investments in R&D have fostered an environment conducive to innovation in 3D IC technology. Major tech firms in the U.S., along with supportive government policies aimed at enhancing semiconductor manufacturing capabilities, have significantly contributed to the market’s expansion.

North America benefits from a strong presence of leading semiconductor companies, which are pivotal in driving the adoption of advanced technologies including 3D ICs. These companies not only contribute directly to market growth through their innovations but also through strategic partnerships and acquisitions that enhance their production capacities.

The growing use of 3D ICs in key sectors like healthcare, automotive, and consumer electronics is driving further growth. In the automotive industry, the shift to electric and autonomous vehicles, which demand high-performance electronics, is particularly boosting the need for advanced components like 3D ICs.

Product Type Analysis

In 2024, the Sensor segment held a dominant position in the 3D ICs market, capturing more than a 29.3% share. This segment’s leadership is attributed to the widespread integration of sensors in various consumer electronics, automotive applications, and industrial equipment.

The demand for sensors in smartphones, wearables, and IoT devices, where space is limited but functionality demands are high, has been particularly instrumental in driving the growth of 3D IC sensors. These applications benefit from the enhanced performance and reduced size that 3D integration offers.

The dominance of the Sensor segment is driven by advancements in automotive technologies like autonomous driving and ADAS, which rely on sensors. As the automotive industry moves towards more automated and energy-efficient vehicles, the demand for advanced sensing technologies, compactly integrated with 3D ICs, continues to rise, strengthening the segment’s market position. This trend is expected to persist.

Moreover, the development of smart cities and industrial automation requires robust sensor networks that can perform reliably in complex environments. 3D ICs enable the dense packing of sensor arrays into these environments without sacrificing performance, driving their adoption in sectors where traditional 2D sensors might fall short.

Application Analysis

In 2024, the Consumer Electronics segment held a dominant position in the 3D ICs market, capturing more than a 36.7% share. This leadership can be attributed to the escalating demand for compact and high-performance devices like smartphones, tablets, and wearable technology.

Consumer electronics manufacturers are continually pushing the boundaries of what’s possible in device miniaturization while enhancing performance, making 3D ICs an ideal solution for meeting both objectives. The integration of 3D IC technology allows for more efficient use of space and faster data processing, which are critical factors in the competitive consumer electronics market.

The IT & Telecom segment benefits from 3D IC advancements, as data centers and network infrastructure need efficient, high-performance processing to manage large data volumes. However, this segment hasn’t reached the dominance of consumer electronics, as the transformative benefits of 3D ICs are more pronounced in consumer-facing products.

In the Military segment, the adoption of 3D ICs is driven by the need for high-performance, compact devices for modern warfare and surveillance. Their robustness under extreme conditions makes them ideal for military use. However, due to niche requirements and lower volume needs, this segment remains smaller compared to consumer electronics.

Key Market Segments

By Product Type

- LED

- Memories

- MEMS

- Sensor

- Logic

- Others

By Application

- IT & Telecom

- Military

- Consumer Electronics

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Growing Demand for Consumer Electronics

The increasing demand for consumer electronics, such as smartphones, tablets, and gaming devices, has significantly propelled the adoption of 3D Integrated Circuits (ICs). These devices require compact, high-performance components to meet consumer expectations for speed and functionality.

3D IC technology addresses these needs by enabling the stacking of multiple circuit layers, thereby enhancing performance while reducing the overall footprint. This vertical integration allows for shorter interconnects between components, leading to faster data processing and improved energy efficiency.

Restraint

High Manufacturing Costs

Despite the advantages of 3D ICs, their adoption is hindered by high manufacturing costs. The complex processes involved, such as through-silicon via (TSV) formation and wafer bonding, require advanced equipment and materials, leading to increased production expenses.

The complexity of stacking chips and ensuring heat dissipation and signal integrity in 3D ICs requires advanced packaging and specialized materials, driving up costs. This demands expensive equipment and expertise, creating a barrier for smaller companies. As a result, 3D ICs may be limited to niche markets or high-end products, hindering widespread adoption.

Opportunity

Expansion in Data Centers and High-Performance Computing

The rise of data-intensive applications, including artificial intelligence, big data analytics, and cloud computing, has led to a surge in demand for high-performance computing solutions. 3D ICs offer a promising opportunity in this sector by providing enhanced processing power and energy efficiency through their compact, vertically integrated architectures.

By reducing signal transmission distances and improving bandwidth, 3D ICs can significantly boost the performance of servers and data centers. As organizations continue to seek efficient ways to manage and process large volumes of data, the integration of 3D ICs into data center infrastructures presents a substantial growth opportunity for the technology.

Challenge

Thermal Management Issues

One of the primary challenges associated with 3D ICs is effective thermal management. The vertical stacking of multiple active layers leads to increased power density, which can result in significant heat accumulation within the chip. If not properly managed, this heat can adversely affect the performance and reliability of the device.

Developing efficient cooling solutions for 3D ICs is complex, as traditional heat dissipation methods may not be adequate for the densely packed structures. Innovations in thermal interface materials, heat spreaders, and advanced cooling techniques are essential to address these challenges and ensure the longevity and efficiency of 3D ICs in various applications.

Emerging Trends

One significant trend is the shift towards heterogeneous integration, where diverse components such as processors, memory units, and sensors are combined within a single 3D IC. This integration allows for optimized performance, as each component can be manufactured using the most suitable technology and then assembled into a cohesive system.

Through-Silicon Vias (TSVs) are a key development, providing vertical electrical connections through silicon wafers or dies. By shortening interconnects between stacked layers, TSVs enable faster signal transmission and reduced power consumption, making them ideal for high-performance computing and AI applications that demand rapid data exchange.

The industry is also exploring advanced packaging techniques like wafer-to-wafer bonding and die-to-wafer bonding. These methods enhance alignment precision between layers, improving overall device reliability and performance. Additionally, the use of new materials and fabrication processes is being investigated to further enhance the thermal and electrical properties of 3D ICs.

Business Benefits

The adoption of 3D IC technology offers several compelling advantages for businesses. 3D ICs enable significant space savings by stacking components vertically. This compactness is crucial for modern electronic devices, where reducing size without compromising functionality is a key competitive advantage.

The performance improvements associated with 3D ICs can lead to products that operate faster and more efficiently. The reduced distance between components allows for quicker data transfer and processing speeds, which is essential in sectors like data centers, gaming, and mobile devices. Enhanced performance can differentiate products in crowded markets, providing a competitive edge.

Moreover, 3D ICs contribute to lower power consumption. The shortened interconnections reduce resistive losses, leading to energy-efficient operations. This efficiency is particularly advantageous for battery-powered devices, extending their operational life and aligning with the growing consumer demand for sustainable, energy-saving products.

Key Player Analysis

Amkor Technology stands as a leading player in the 3D IC market, with extensive expertise in semiconductor packaging and testing services. The company’s unique offerings, such as advanced packaging solutions and wafer-level packaging (WLP), are crucial for building more compact and efficient integrated circuits.

ASE Group is another significant player in the 3D IC industry, recognized for its comprehensive semiconductor assembly and testing services. ASE’s advanced packaging technologies, including its 3D stacking and fan-out wafer-level packaging (FOWLP) solutions, enable the creation of high-density, high-performance ICs.

BeSang Inc., a relatively smaller but notable player in the 3D IC field, specializes in innovative semiconductor packaging solutions. BeSang’s strength lies in its expertise in microelectromechanical systems (MEMS) and its innovative 3D packaging technologies, such as TSV (Through-Silicon Via) and WLP.

Top Key Players in the Market

- Amkor Technology

- ASE Group

- BeSang Inc.

- IBM Corporation

- Intel Corporation

- Micron Technology Inc.

- Samsung Electronics Co. Ltd.

- STATS ChipPAC Ltd.

- STMicroelectronics N.V.

- Tezzaron Semiconductor

- Toshiba Corporation

- United Microelectronics Corporation

- Xilinx Inc.

- Other Major Players

Top Opportunities Awaiting for Players

The 3D Integrated Circuits (3D ICs) market presents several compelling opportunities for industry players.

- Expansion in Consumer Electronics: The ongoing demand for compact and energy-efficient electronic devices like smartphones, laptops, and tablets is driving the growth of 3D ICs, which are essential for enhancing the performance and functionality of such devices. This trend is expected to continue, offering significant opportunities for 3D IC manufacturers.

- Automotive Applications: As the automotive industry increasingly adopts advanced electronics for autonomous driving and better in-vehicle infotainment systems, there is a growing need for high-performance 3D ICs. This technology enables more efficient processing and integration of complex systems within vehicles.

- High-Performance Computing (HPC) and AI: The push towards artificial intelligence (AI) and high-performance computing across various sectors, including cloud computing and big data analytics, is propelling the adoption of 3D IC technology. These applications require high-speed data processing and enhanced memory capabilities that 3D ICs can provide.

- Innovations and Technological Advancements: Continuous technological advancements in 3D IC manufacturing processes, such as the development of new 3D chip packaging technologies by major companies like Samsung, are creating new opportunities for market expansion and the adoption of these technologies across different industries.

- Government and Institutional Support: Increasing support from governments worldwide for the semiconductor industry, through investments in R&D and initiatives aimed at boosting local microelectronics production, offers significant opportunities for 3D ICs. Such initiatives are crucial for fostering innovation and development within the sector.

Recent Developments

- June 2024: By 2027, Samsung plans to prioritize 2.5D and 3D IC designs, alongside chiplet co-packaged optics, as part of its strategy to expand its AI foundry business. This shift complements the company’s launch of cutting-edge process nodes such as SF2Z and SF4U, signaling its commitment to advancing next-gen chip technologies.

- October 2024: Faraday Technology will leverage Ansys RaptorX™ EM modeling to boost its 2.5D/3D IC packaging designs, optimizing interposers and multi-die structures for improved memory bandwidth, signal integrity, and overall application performance.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 16.2 Bn |

| Forecast Revenue (2034) | USD 125 Bn |

| CAGR (2025-2034) | 22.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (LED, Memories, MEMS, Sensor, Logic, Others), By Application (IT & Telecom, Military, Consumer Electronics, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Amkor Technology, ASE Group, BeSang Inc., IBM Corporation, Intel Corporation, Micron Technology Inc., Samsung Electronics Co. Ltd., STATS ChipPAC Ltd., STMicroelectronics N.V., Tezzaron Semiconductor, Toshiba Corporation, United Microelectronics Corporation, Xilinx Inc., Other Major Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |