Quick Navigation

Report Overview

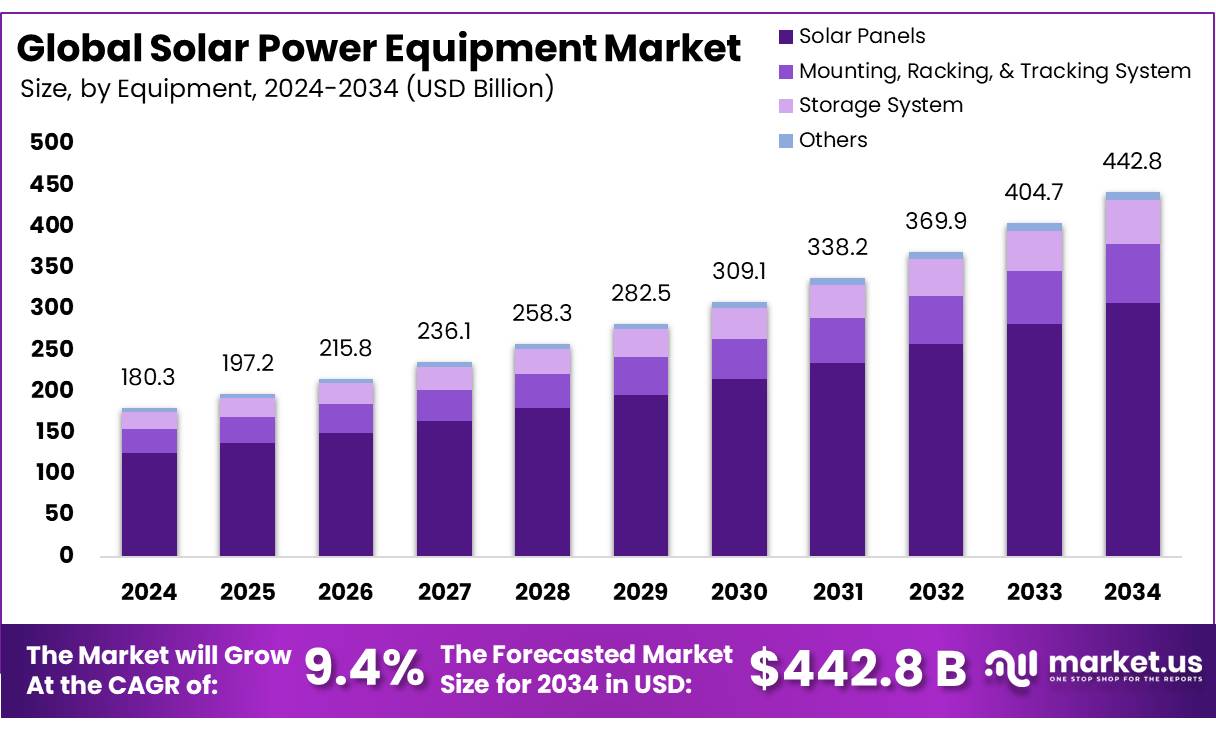

The Global Solar Power Equipment Market size is expected to be worth around USD 442.8 billion by 2034, from USD 180.3 billion in 2024, growing at a CAGR of 9.4% during the forecast period from 2025 to 2034.

The Solar Power Equipment Market has emerged as a cornerstone of the renewable energy sector, driven by increasing energy demand, declining technology costs, and stringent environmental regulations. Solar power equipment, including photovoltaic (PV) modules, inverters, mounting systems, and tracking systems, forms the backbone of solar energy generation.

The industry continued to lead the energy transition in 2024, representing over 66% of new capacity. Storage accounted for another 18% of new capacity, meaning solar and storage accounted for 84% of all new capacity. Solar’s increasing competitiveness against other technologies has allowed it to quickly increase its share of total U.S. electrical generation, from just 0.1% in 2010 to over 6% in 2024.

The market has experienced robust growth due to increasing environmental concerns, supportive government policies, and technological advancements, positioning it as a cornerstone of the global energy transition. This reflects a dynamic landscape driven by widespread adoption across residential, commercial, industrial, and utility-scale applications.

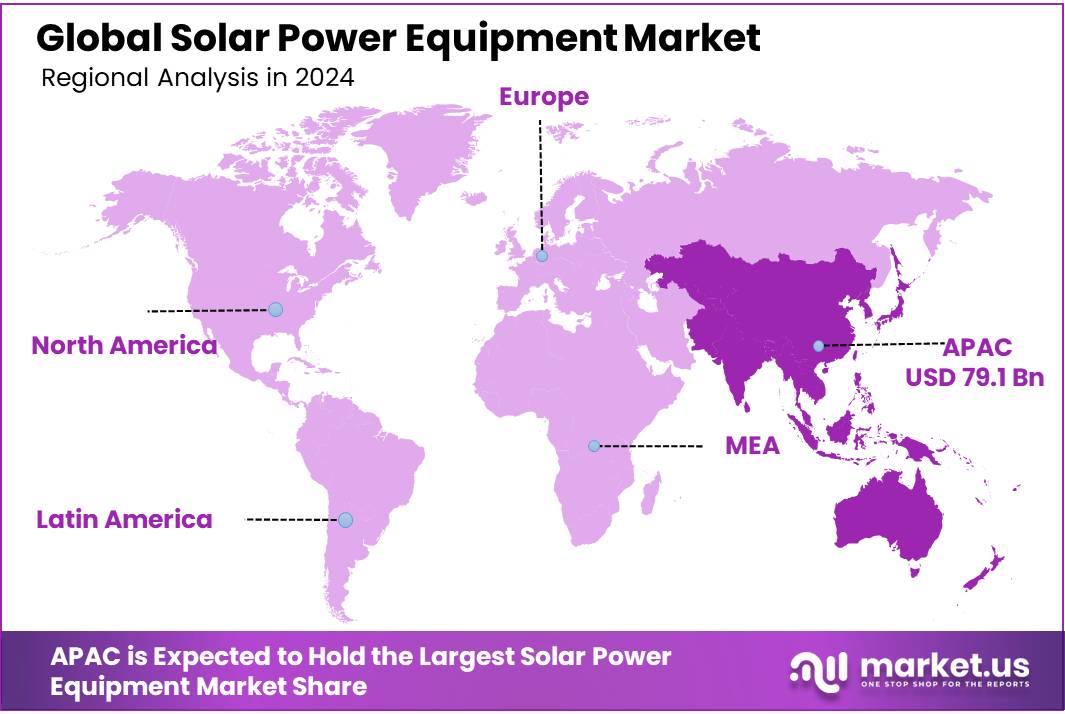

The Asia-Pacific region dominates, accounting for over 43% of the market share in 2024, led by China, Japan, and India, where rapid urbanization and government incentives fuel demand. Technological advancements, such as bifacial solar panels and lithium-ion battery storage, enhance efficiency and reliability, further propelling market growth. However, challenges like high initial installation costs and competition from conventional energy sources persist.

Key Takeaways

- The Global Solar Power Equipment Market is expected to grow from USD 180.3 billion in 2024 to USD 442.8 billion by 2034 at a 9.4% CAGR.

- Solar panels dominate with a 69.6% market share, driven by cost reductions, efficiency gains, and government incentives.

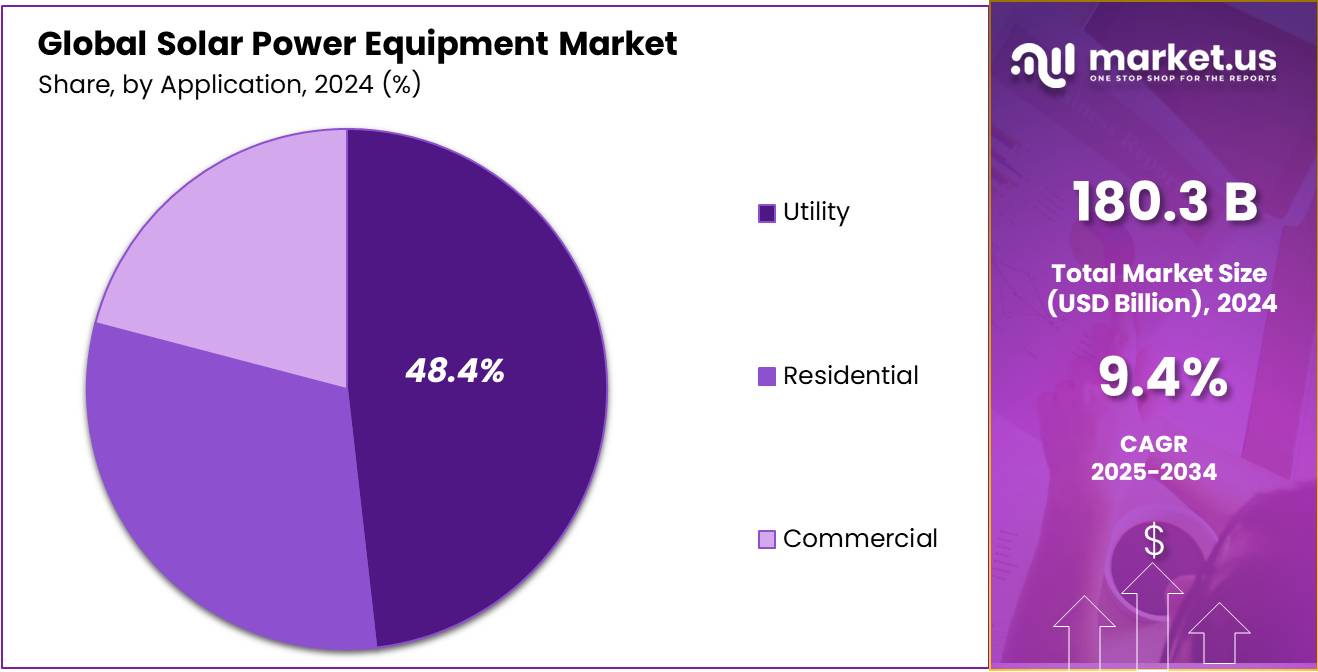

- The utility sector leads with a 48.4% share, fueled by large-scale solar farms and cost-effective energy storage solutions.

- Asia-Pacific holds a 43.9% market share, valued at USD 79.1 billion, due to industrialization and strong renewable energy policies.

Analyst Viewpoint

The Solar Power Equipment Sector is buzzing with potential, driven by global demand for clean energy and supportive policies, but it’s not without its hurdles. Investment opportunities are plentiful, especially in solar panel manufacturing and innovative technologies like bifacial and perovskite cells, which promise higher efficiency and lower costs.

However, risks loom large high interest rates, labor shortages, and supply chain bottlenecks, like delays in high-voltage equipment, which could slow progress. Trade policies, such as potential tariffs on Southeast Asian imports, add uncertainty. Consumer insights reveal a cautious but growing interest in solar solutions, particularly among homeowners and businesses eyeing cost savings.

Technologies like smart inverters and blockchain-based peer-to-peer energy trading are making solar more appealing by boosting efficiency and enabling direct energy sales, which resonates with tech-savvy consumers. On the regulatory front, the Inflation Reduction Act’s tax credits have been a game changer, boosting deployment compared to pre-IRA projections.

By Equipment

In 2024, Solar Panels held a dominant market position in the solar power equipment sector, capturing more than a 69.6% share. Their widespread adoption was driven by falling costs, improved efficiency, and strong demand from both residential and commercial installations. Governments worldwide continued to push for renewable energy, offering subsidies and tax incentives that further boosted solar panel sales.

The segment is expected to maintain its lead, though growth may slow slightly as newer technologies like advanced thin-film panels and bifacial modules gain traction. Even so, traditional solar panels will likely remain the top choice due to their reliability and established supply chains.

The market is also seeing a shift toward higher-wattage panels, as developers seek to maximize energy output per square foot. While other solar equipment, such as inverters and mounting systems, play crucial roles, solar panels continue to be the backbone of the industry.

By Application

In 2024, the Utility Sector held a dominant market position in the solar power equipment market, capturing more than a 48.4% share. This strong performance was driven by large-scale solar farms and government-backed renewable energy projects, which prioritized high-capacity installations.

Falling solar panel prices and improved energy storage solutions also made utility-scale projects more cost-effective, encouraging further investments. The utility segment is expected to maintain its lead, though growth may face challenges from grid integration issues and land availability constraints in some regions.

However, rising electricity demand and the push for decarbonization in the power sector will keep utility-scale solar a key focus. Innovations in floating solar farms and hybrid renewable systems could also open new expansion opportunities.

Key Market Segments

By Equipment

- Solar Panels

- Mounting, Racking, and Tracking System

- Storage System

- Others

By Application

- Utility

- Residential

- Commercial

Drivers

Government Policies Fueling Solar Power Equipment Growth

One major driving factor for the solar power equipment industry is supportive government policies and incentives. These initiatives make solar energy more affordable and encourage its adoption across homes, businesses, and large-scale projects.

This push is not just about meeting climate goals but also about making clean energy accessible to everyday people, which is transforming how we power our lives. In the United States, the Inflation Reduction Act (IRA) of 2022 has been a game-changer. It provides tax credits of up to 30% for solar installations, covering both residential and commercial projects.

Policies like foreign direct investment in renewable projects have attracted global manufacturers, increasing the production of solar panels and related equipment. These numbers highlight how government initiatives are not just numbers on paper, they’re empowering communities, creating jobs, and making solar a practical choice for millions.

Restraints

Policy and Regulatory Uncertainty: A Major Restraint in Solar Power Equipment Deployment

One of the significant challenges hindering the growth of solar power equipment in India is the lack of clear and consistent policy and regulatory frameworks. This uncertainty affects investors and developers, making it difficult to plan and execute solar projects effectively.

A study supported by the World Bank and the Energy Sector Management Assistance Program (ESMAP) revealed that approximately 63% of solar developers identified policy and regulatory barriers as the most critical obstacles to solar power development in India. These barriers include issues like the bankability of Power Purchase Agreements (PPAs), long-term policy planning, and clarity in guidelines.

The bankability of PPAs is a particular concern. Developers often find that the terms of PPAs are not favorable enough to secure financing from banks and other financial institutions. This situation leads to delays in project implementation and increases the financial risk for developers.

Opportunity

Government Initiatives Driving Solar Power Equipment Growth in India

India’s solar energy sector has experienced remarkable growth in recent years, largely due to proactive government initiatives. As of March 2025, the country’s total installed solar capacity reached 105.65 GW, comprising 81.01 GW from ground-mounted projects, 17.02 GW from rooftop solar systems, 2.87 GW from hybrid projects, and 4.74 GW from off-grid systems.

A significant contributor to this growth is the “PM Surya Ghar: Muft Bijli Yojana,” launched in February 2024. With an allocation of ₹75,021 crore, this scheme aims to install rooftop solar panels in one crore households, providing up to 300 units of free electricity monthly. Subsidies under this program range from ₹30,000 to ₹78,000 per household, depending on the system’s capacity.

The Development of Solar Parks and Ultra Mega Solar Power Projects scheme has been instrumental in facilitating large-scale solar installations. Initially targeting 20,000 MW, the scheme’s capacity was later enhanced to 40,000 MW, supporting states and union territories in setting up solar parks with necessary infrastructure.

Trends

Emerging Factor: Surge in Domestic Solar Manufacturing Capacity

India is witnessing a significant shift in its solar energy landscape, marked by a substantial increase in domestic solar manufacturing capacity. This development is not only enhancing the country’s energy self-reliance but also creating numerous employment opportunities.

According to the Ministry of New and Renewable Energy (MNRE), the government has launched initiatives to bolster domestic manufacturing of solar photovoltaic (PV) modules. Under the Production Linked Incentive (PLI) scheme, the government aims to establish an integrated manufacturing capacity of 39,600 MW for solar PV modules.

The PLI scheme is designed to provide financial incentives to companies setting up manufacturing units for high-efficiency solar PV modules. By promoting domestic manufacturing, the scheme aims to reduce India’s dependence on imported solar equipment, thereby enhancing energy security and fostering economic growth.

Regional Analysis

Asia-Pacific: Dominant Force in the Global Solar Power Equipment Market

The Asia-Pacific (APAC) region stands at the forefront of the global solar power equipment market, commanding a substantial 43.9% share and reaching a market value of USD 79.1 billion. This dominance is propelled by a confluence of factors, including rapid industrialization, escalating energy demands, and robust governmental support for renewable energy initiatives.

China, as the world’s largest producer and consumer of solar equipment, plays a pivotal role in this landscape. In the first half of 2024 alone, China exported a record 120,427 megawatts (MW) of solar modules, underscoring its manufacturing prowess and commitment to renewable energy expansion.

India, another significant player in the region, has made remarkable strides in solar energy deployment. With a focus on achieving ambitious renewable energy targets, India has implemented various schemes and incentives to promote solar installations across residential, commercial, and industrial sectors.

The APAC region’s dominance is further reinforced by its comprehensive supply chain, encompassing raw material procurement, manufacturing, and distribution networks. This integrated approach not only ensures cost-effectiveness but also facilitates the rapid deployment of solar solutions to meet the region’s growing energy needs.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

- ABB Group is a global leader in solar power equipment, offering inverters, automation, and grid integration solutions. Known for its high-efficiency technologies, ABB supports utility-scale and residential solar projects. The company focuses on smart energy management and sustainability, enhancing solar power adoption.

- Canadian Solar is a major solar manufacturer, producing panels, inverters, and energy storage systems. With a strong global footprint, it serves residential, commercial, and utility-scale markets. The company emphasizes cost-effective, high-performance solar solutions and invests heavily in innovation. Canadian Solar’s integrated supply chain and project development expertise strengthen its competitive edge in the solar industry.

- Enphase Energy specializes in microinverters and energy management systems for solar power. Its advanced technology enhances efficiency, reliability, and monitoring for residential and commercial installations. Enphase’s smart energy solutions, including battery storage, support grid independence. The company’s focus on innovation and customer-centric products has solidified its position as a leader in decentralized solar energy systems.

Top Key Players in the Market

- ABB Group

- Canadian Solar

- Enphase Energy, Inc.

- First Solar Inc.

- GCL-Poly Energy Holdings Limited

- Hanwha Q CELLS

- JA Solar

- JinkoSolar

- Kyocera Corporation

- LONGi Solar

- REC Group

- Renesola Ltd.

- Risen Energy Co., Ltd.

- Shunfeng International

- SMA Solar Technology AG

- SolarEdge Technologies, Inc.

- Sungrow Power Supply Co., Ltd.

- Sunrun Inc.

- Trina Solar

- Vivint Solar

Recent Developments

- In 2024, ABB completed the sale of its solar inverter business to Marici Holdings, The Netherlands B.V. as part of its portfolio optimization strategy. This move allows ABB to focus on core electrification and automation technologies while exiting the solar inverter market.

- In 2024, Canadian Solar secured contracts for 1.5 GW of solar projects in Brazil and Spain, as reported in their Q3 2024 earnings call, reinforcing their global leadership in solar project development. Canadian Solar announced the opening of a 5 GW solar module manufacturing facility in Mesquite, Texas.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 180.3 Billion |

| Forecast Revenue (2034) | USD 442.8 Billion |

| CAGR (2025-2034) | 9.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Equipment (Solar Panels, Mounting, Racking, and Tracking System, Storage System, Others), By Application (Utility, Residential, Commercial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | ABB Group, Canadian Solar, Enphase Energy, Inc., First Solar Inc., GCL-Poly Energy Holdings Limited, Hanwha Q CELLS, JA Solar, JinkoSolar, Kyocera Corporation, LONGi Solar, REC Group, Renesola Ltd., Risen Energy Co. Ltd., Shunfeng International, SMA Solar Technology AG, SolarEdge Technologies, Inc., Sungrow Power Supply Co. Ltd., Sunrun Inc., Trina Solar, Vivint Solar |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |