Quick Navigation

- Report Overview

- Key Takeaways

- By Type Analysis

- By Panel Type Analysis

- By Frame Type Analysis

- By Installation Type Analysis

- By Technology Analysis

- By End-User Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

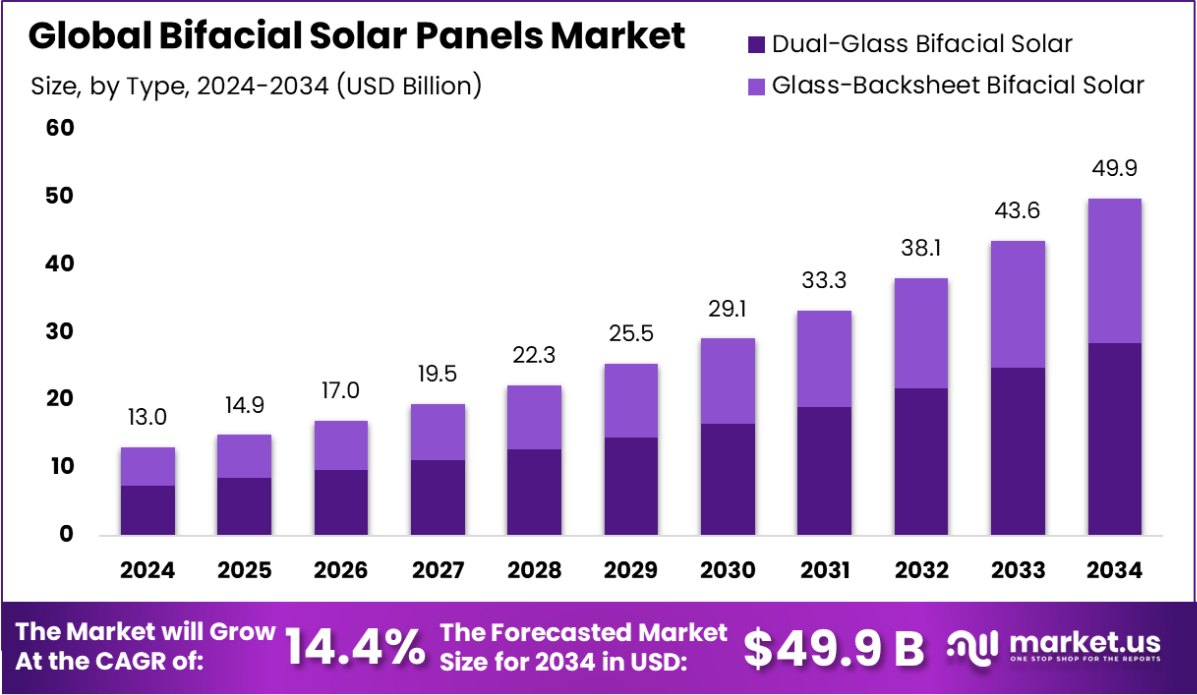

Global Bifacial Solar Panels Market is expected to be worth around USD 49.9 billion by 2034, up from USD 13.0 billion in 2024, and grow at a CAGR of 14.4% from 2025 to 2034. With a 42.9% market share, the Asia-Pacific bifacial solar panels market reached USD 5.5 billion in 2024.

Bifacial solar panels generate electricity from both sides by capturing direct sunlight on the front and reflected light on the back. These panels are designed for increased energy efficiency, leveraging high ground albedo to maximize output. The annual average bifacial gain varies between 2.4% and 22.3%, with higher gains in snow-covered or reflective environments.

They outperform monofacial panels in energy generation, producing a daily average of 0.6 to 1.2 kWh/m²/day compared to 0.5 to 1 kWh/m²/day for monofacial systems. When integrated with one-axis trackers, bifacial solar panels offer 6% to 9% more energy annually than traditional systems, making them a preferred choice for utility-scale solar projects.

The shift toward high-efficiency solar solutions is a key driver for bifacial panel adoption. Their ability to increase energy yield by 6% to 22.3% enhances project feasibility, especially in large-scale installations. Technological advancements in anti-reflective coatings and bifacial PV cell structures further improve efficiency. Governments worldwide are also incentivizing high-efficiency solar solutions, accelerating market penetration.

The growing demand for higher energy yields per square meter is pushing industries to adopt bifacial panels. Utility-scale projects prefer bifacial setups due to their superior performance with one-axis tracking systems. Countries with strong solar mandates, such as China, the U.S., and India, are leading installations.

The bifacial solar market presents lucrative opportunities in regions with high ground reflectivity, such as deserts and snow-covered areas. Innovations in mounting structures and AI-driven tracking systems will further optimize energy capture. As energy storage solutions advance, bifacial technology will integrate better into hybrid renewable setups, enhancing grid reliability.

Key Takeaways

- Global Bifacial Solar Panels Market is expected to be worth around USD 49.9 billion by 2034, up from USD 13.0 billion in 2024, and grow at a CAGR of 14.4% from 2025 to 2034.

- The Dual-Glass Bifacial Solar type dominates the market with a share of 57.6%, highlighting its robust demand.

- Monocrystalline Bifacial Solar Panels lead by panel type, capturing 52.3% of the market, preferred for their efficiency.

- Framed Bifacial Solar, with a 71.3% share, remains the favored choice due to enhanced durability and ease of installation.

- Ground-Mounted Bifacial Solar Panels hold a significant 63.3% market share, popular for their adaptability in various terrains.

- PERC technology in bifacial solar panels has captured a 72.3% share, offering superior light absorption capabilities.

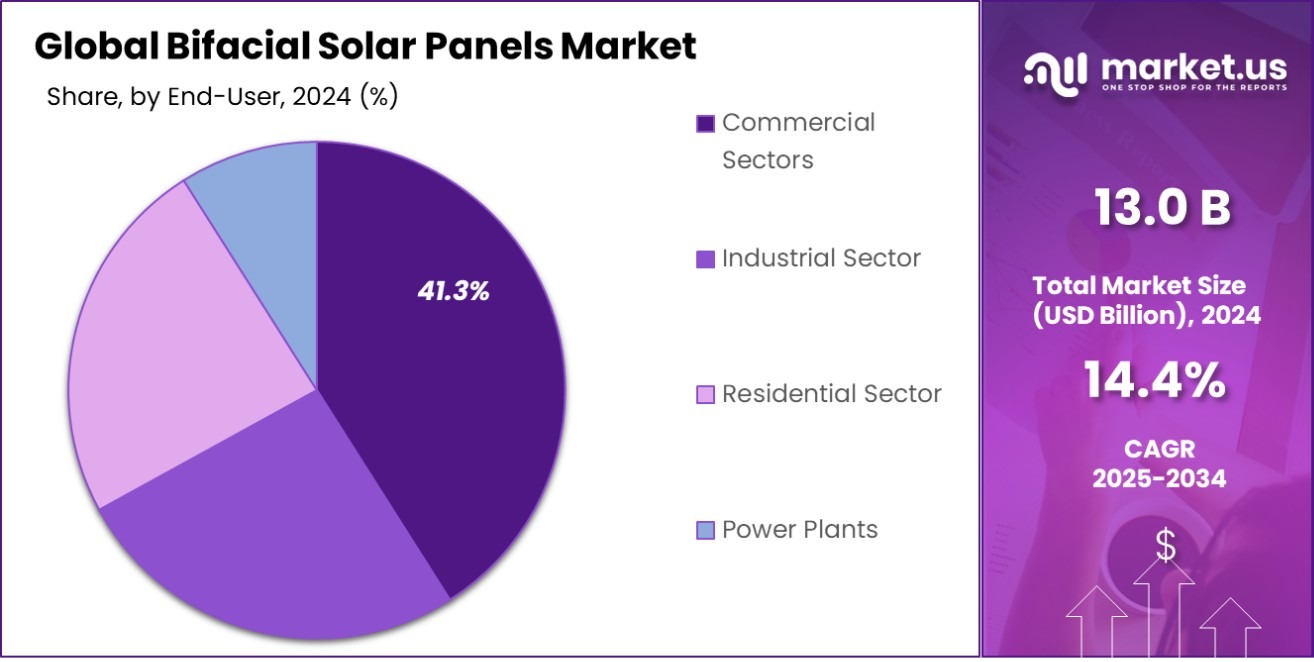

- In the end-user segment, commercial sectors utilize 41.3% of bifacial solar panels, benefiting from their increased energy generation.

- The Asia-Pacific region led the bifacial solar panels market in 2024, capturing a 42.9% share, worth USD 5.5 billion.

By Type Analysis

Dual-glass bifacial solar panels lead with 57.6% of the market share.

In 2024, Dual-Glass Bifacial Solar held a dominant market position in the “By Type” segment of the Bifacial Solar Panels Market, with a 57.6% share. This notable market share underscores the increasing preference among consumers and industries for solar panels that offer enhanced durability and performance. The dual-glass design not only protects the solar cells from environmental factors but also significantly enhances the panel’s ability to capture sunlight from both sides, thereby increasing energy yield.

The robust growth of the Dual-Glass Bifacial segment is propelled by its superior resistance to harsh weather conditions and its longer lifespan compared to traditional single-sided panels. Additionally, these panels are less prone to potential-induced degradation, making them more reliable for long-term renewable energy projects. Their adoption is particularly strong in regions with high direct and reflected solar irradiance, where their efficiency can be maximally leveraged.

The market’s inclination towards dual-glass bifacial technology is further supported by regulatory support and financial incentives aimed at promoting advanced solar solutions. As the solar industry continues to evolve, the demand for dual-glass bifacial panels is expected to grow, driven by their economic and environmental benefits. This segment’s strong performance is indicative of a wider trend towards more sustainable and efficient renewable energy solutions in the global market.

By Panel Type Analysis

Monocrystalline bifacial solar panels are preferred, capturing 52.3% of the sector.

In 2024, Monocrystalline Bifacial Solar Panels held a dominant market position in the “By Panel Type” segment of the Bifacial Solar Panels Market, capturing a 52.3% share. This substantial market share reflects the growing industry preference for monocrystalline panels due to their high efficiency and superior performance characteristics. Monocrystalline bifacial solar panels are favored for their ability to produce a high power output even in limited space, making them ideal for both residential and commercial applications.

The strong performance of monocrystalline bifacial panels is largely attributed to their high efficiency rates, which are significantly better than those of their polycrystalline counterparts. These panels are particularly effective in environments with strong direct sunlight, where they can maximize energy generation by capturing sunlight from both the front and back sides. The market’s inclination toward these panels is also driven by their aesthetic appeal, as they tend to have a more uniform and sleek appearance.

Given their durability and long-term reliability, monocrystalline bifacial panels have become a popular choice for investors looking to maximize returns on renewable energy projects. As the global push towards sustainability intensifies, the demand for these high-efficiency panels is expected to continue growing, reinforcing their strong position in the market.

By Frame Type Analysis

Framed bifacial solar panels dominate, holding a substantial 71.3% market portion.

In 2024, Framed Bifacial Solar Panels held a dominant market position in the “By Frame Type” segment of the Bifacial Solar Panels Market, commanding a 71.3% share. This significant market share underscores the robust preference for framed designs among installers and end-users, primarily due to the added durability and ease of installation that frames provide. Framed bifacial panels, with their robust structural support, are particularly favored in large-scale solar projects and harsh environmental conditions where additional protection against physical stresses is necessary.

The preference for framed bifacial solar panels is further driven by their compatibility with existing mounting systems and tracking technology, which are critical for optimizing solar energy collection. These panels are designed to enhance energy production while reducing the risk of damage during installation and maintenance, thereby offering a more reliable and user-friendly solution for both ground-mounted and rooftop solar systems.

The market’s strong inclination toward framed bifacial panels is indicative of a broader trend toward maximizing energy efficiency and durability in solar technology investments. As the market continues to expand, the demand for framed bifacial solar panels is expected to remain high, supported by their proven performance benefits and the ongoing global shift toward sustainable energy solutions.

By Installation Type Analysis

Ground-mounted bifacial solar installations are prevalent, comprising 63.3% of setups.

In 2024, Ground-Mounted Bifacial Solar Panels held a dominant market position in the “By Installation Type” segment of the Bifacial Solar Panels Market, securing a 63.3% share. This substantial market presence is attributed to the growing deployment of large-scale solar farms and utility-scale projects, where ground-mounted installations provide higher energy generation efficiency. These installations maximize the bifacial effect by optimizing panel tilt and height to capture both direct sunlight and reflected light from the ground, thereby increasing overall power output.

The preference for ground-mounted bifacial solar panels is largely driven by their ability to accommodate tracking systems, which enhance energy generation by adjusting panel orientation throughout the day. Utility-scale solar projects favor these installations due to their scalability, allowing for large-capacity solar farms that contribute significantly to grid stability and energy supply. Additionally, ground-mounted systems facilitate easier maintenance and cooling, improving long-term performance and efficiency.

As global investments in renewable energy continue to rise, particularly in regions with high solar irradiance, the adoption of ground-mounted bifacial solar panels is expected to grow. The segment’s strong market position is further reinforced by favorable government policies, incentives, and the rising demand for cost-effective, high-efficiency solar solutions in large-scale applications.

By Technology Analysis

Passivated Emitter Rear Cell (PERC) technology leads at 72.3% in this market.

In 2024, Passivated Emitter Rear Cell (PERC) held a dominant market position in the “By Technology” segment of the Bifacial Solar Panels Market, with a 72.3% share. This strong market presence highlights the widespread adoption of PERC technology due to its superior efficiency, enhanced light absorption, and improved performance in various environmental conditions. The technology’s ability to minimize electron recombination losses and increase energy conversion efficiency has made it the preferred choice for both residential and utility-scale solar installations.

The dominance of PERC technology in bifacial solar panels is driven by its cost-effectiveness and compatibility with existing manufacturing processes. By integrating an additional passivation layer, PERC cells enable higher power output without significantly increasing production costs.

This makes them an attractive option for solar developers seeking high-efficiency solutions with a competitive price-to-performance ratio. Furthermore, the ability of PERC-based bifacial panels to capture more sunlight from the rear side enhances their overall energy yield, making them suitable for regions with high solar irradiance.

As the demand for high-performance solar technologies continues to rise, the adoption of PERC-based bifacial solar panels is expected to grow. The segment’s strong position reflects the market’s inclination towards efficiency-driven advancements, further reinforcing PERC technology’s role in shaping the future of solar energy generation.

By End-User Analysis

The commercial sector is a major end-user, accounting for 41.3% usage.

In 2024, Commercial Sectors held a dominant market position in the “By End-User” segment of the Bifacial Solar Panels Market, with a 41.3% share. This substantial market share reflects the growing adoption of bifacial solar panels in commercial establishments, including office buildings, retail spaces, and industrial facilities. Businesses are increasingly investing in solar energy solutions to reduce operational costs, enhance sustainability efforts, and comply with regulatory mandates for carbon reduction.

The commercial sector’s preference for bifacial solar panels is largely driven by their higher energy efficiency and ability to generate more power within a limited space. Rooftop solar installations in commercial buildings benefit from the bifacial design, which captures reflected sunlight from surrounding surfaces, maximizing electricity generation.

Additionally, many businesses are leveraging government incentives, tax credits, and net metering policies to lower the initial investment costs and improve long-term financial returns.

As energy costs continue to rise and sustainability goals become a priority for corporations, the demand for bifacial solar panels in commercial applications is expected to grow. With advancements in solar technology and increasing awareness of clean energy benefits, the commercial segment is projected to maintain its strong market position, driving further adoption of bifacial solar solutions worldwide.

Key Market Segments

By Type

- Dual-Glass Bifacial Solar

- Glass-Backsheet Bifacial Solar

By Panel Type

- Monocrystalline Bifacial Solar Panels

- Polycrystalline Bifacial Solar Panels

- Thin-Film Bifacial Solar Panels

- Glass Bifacial Solar Panels

- Backsheet Bifacial Solar Panels

By Frame Type

- Framed Bifacial Solar

- Frameless Bifacial Solar

By Installation Type

- Ground-Mounted Bifacial Solar Panels

- Rooftop Bifacial Solar Panels

By Technology

- Passivated Emitter Rear Cell (PERC)

- Heterojunction (HJT)

- Others

By End-User

- Commercial Sectors

- Industrial Sector

- Residential Sector

- Power Plants

Driving Factors

Higher Energy Efficiency and Increased Power Output

One of the top driving factors for the bifacial solar panels market is their higher energy efficiency and increased power output. Unlike traditional single-sided solar panels, bifacial panels generate electricity from both the front and back sides. This allows them to capture direct sunlight as well as reflected light from surfaces like the ground, water, or nearby buildings.

As a result, bifacial panels can produce 10-20% more energy compared to conventional solar panels. This higher efficiency is particularly beneficial for large-scale solar farms, commercial rooftops, and urban installations where maximizing energy production is essential.

The increased power generation leads to better returns on investment, making bifacial solar panels an attractive choice for businesses, utilities, and governments focusing on renewable energy expansion.

Restraining Factors

Higher Initial Costs and Installation Challenges

One major restraining factor in the bifacial solar panels market is their higher initial costs and installation challenges. Compared to traditional monofacial panels, bifacial panels require specialized mounting systems and optimized installation angles to maximize energy generation from both sides.

Additionally, the cost of manufacturing bifacial panels is higher due to advanced cell technology and glass-based designs, increasing the overall investment cost for buyers. Many solar project developers hesitate to adopt bifacial technology due to higher upfront expenses and the need for detailed site assessments to ensure maximum efficiency.

In regions where solar incentives are limited, the adoption rate slows down, as businesses and homeowners may prefer cheaper, traditional solar options over advanced bifacial systems despite long-term benefits.

Growth Opportunity

Expanding Utility-Scale Solar Projects Worldwide

A key growth opportunity for the bifacial solar panels market is the expansion of utility-scale solar projects worldwide. Governments and energy companies are increasingly investing in large-scale solar farms to meet the growing demand for clean and sustainable energy. Bifacial solar panels are ideal for these projects because they generate higher power output, making them more cost-effective over time.

Countries with strong solar incentives and high sunlight exposure are rapidly adopting this technology to enhance grid stability and reduce reliance on fossil fuels. As energy costs continue to rise, utility-scale solar developers see bifacial panels as a long-term investment, offering better land utilization, lower levelized cost of energy (LCOE), and higher returns compared to traditional monofacial panels.

Latest Trends

Rising Adoption of Solar Tracking Systems

One of the latest trends in the bifacial solar panels market is the rising adoption of solar tracking systems. These systems help optimize energy generation by adjusting the angle of solar panels to follow the sun’s movement throughout the day. When combined with bifacial technology, solar trackers enhance light capture from both direct sunlight and reflected light, boosting overall efficiency.

Utility-scale solar farms are increasingly integrating single-axis and dual-axis tracking systems to maximize power output and improve return on investment (ROI). While solar tracking adds extra costs, its ability to increase energy yield by 20-30% makes it a valuable addition. As solar technology advances, automated tracking solutions are becoming more accessible, driving further adoption in commercial and large-scale solar projects.

Regional Analysis

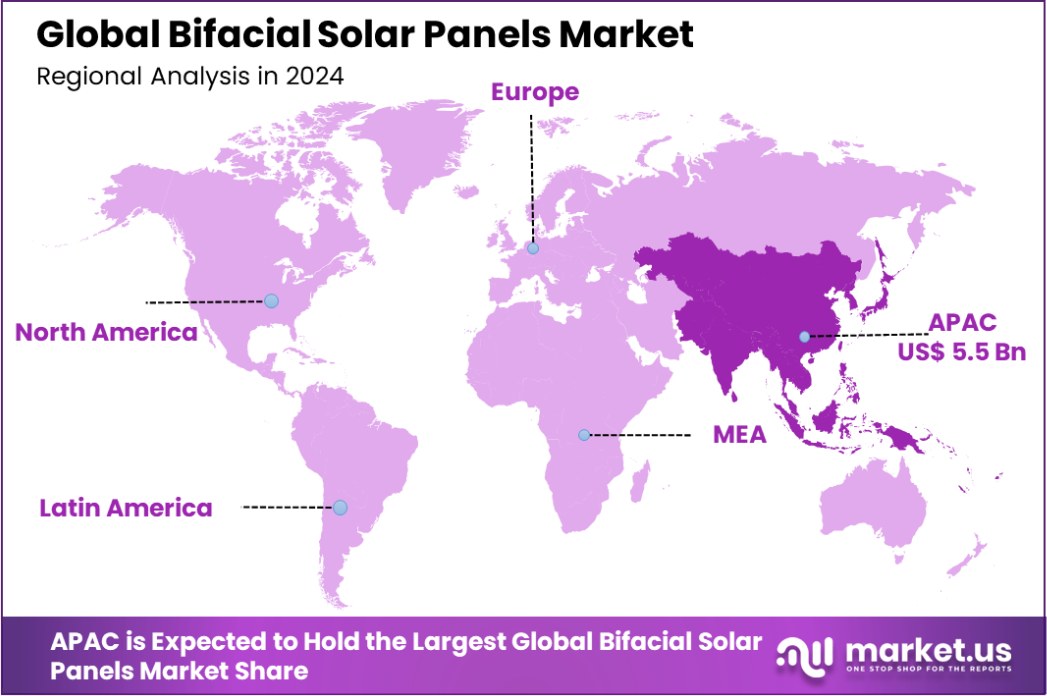

In 2024, Asia-Pacific dominated the bifacial solar panels market, holding a 42.9% share, valued at USD 5.5 billion.

In 2024, Asia-Pacific dominated the Bifacial Solar Panels Market, accounting for 42.9% of the global share, with a market value of USD 5.5 billion. The region’s leadership is driven by large-scale solar energy investments in China, India, Japan, and South Korea, supported by government policies and favorable incentives.

China, the world’s largest solar energy producer, continues to expand its bifacial panel installations, driven by ambitious renewable energy targets and falling production costs. India follows closely, with significant solar capacity additions under its National Solar Mission, further fueling regional growth.

North America is witnessing strong demand for bifacial solar panels, particularly in the United States, where federal tax credits and state-level incentives are driving adoption in utility-scale solar farms. The region is focused on increasing renewable energy capacity, with solar energy contributing over 20% of new electricity generation capacity additions.

Europe remains a key market, led by Germany, Spain, and France, where green energy policies and carbon neutrality goals accelerate bifacial solar deployments. The Middle East & Africa region is leveraging high solar irradiance for large solar projects, while Latin America sees increasing adoption in Brazil and Chile, driven by solar-friendly regulatory frameworks and declining costs.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, Canadian Solar remained a major player in the bifacial solar panels market, leveraging its strong global presence and advanced PV technology. The company’s focus on high-efficiency bifacial modules and strategic partnerships in utility-scale projects strengthened its market position.

JinkoSolar, one of the world’s largest solar manufacturers, continued to dominate with cutting-edge bifacial panel technology and large-scale deployments. Its extensive production capacity and focus on TOPCon and PERC-based bifacial panels contributed significantly to market growth.

Jolywood Group maintained a strong foothold, particularly in n-type bifacial solar cell technology, leading to higher efficiency gains. The company’s investments in TOPCon cell development and large-area bifacial modules positioned it as an industry innovator.

LG Electronics, known for premium solar products, faced increasing competition but retained a niche market with high-performance bifacial modules and advanced cell technology. However, its focus on residential and commercial solar solutions limited its scale in large utility projects.

LONGi remained a global leader, driven by its advanced monocrystalline bifacial modules and aggressive expansion in the Asia-Pacific. Its strong R&D investments in high-efficiency bifacial technology and cost reductions reinforced its dominant position.

Lumos Solar, specializing in aesthetic solar solutions, carved a market niche by integrating bifacial panels into architectural applications. Its innovative approach to solar canopy and building-integrated photovoltaic (BIPV) solutions attracted premium commercial and residential buyers.

Top Key Players in the Market

- Canadian Solar

- JinkoSolar

- Jolywood Group

- LG Electronics

- LONGi

- Lumos Solar

- MegaCell

- Neo Solar Power

- Neosun Inc

- Panasonic

- Premier Energies Limited

- Prism Solar Technologies

- Risen Energy Co., Ltd.

- Sharp Electronics

- SolarWorld

- Soleos

- SunPower Corporation

- Tigo Energy, Inc.

- Trina Solar

- Yingli Green Energy

Recent Developments

- In November 2024, LONGi introduced its new Hi-MO X10 bifacial module, achieving a world record efficiency of 25.4% for crystalline silicon solar modules based on its HPBC 2.0 cell platform.

- In 2020, JinkoSolar announced that its bifacial solar modules achieved a record efficiency of 22.49%, verified by TÜV Rheinland. The company used a new anti-reflection coating and advanced metallization technology to improve efficiency.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 13.0 Billion |

| Forecast Revenue (2034) | USD 49.9 Billion |

| CAGR (2025-2034) | 14.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Dual-Glass Bifacial Solar, Glass-Backsheet Bifacial Solar), By Panel Type (Monocrystalline Bifacial Solar Panels, Polycrystalline Bifacial Solar Panels, Thin-Film Bifacial Solar Panels, Glass Bifacial Solar Panels, Backsheet Bifacial Solar Panels), By Frame Type (Framed Bifacial Solar, Frameless Bifacial Solar), By Installation Type (Ground-Mounted Bifacial Solar PanelsRooftop Bifacial Solar Panels), By Technology (Passivated Emitter Rear Cell (PERC), Heterojunction (HJT), Others), By End-User (Commercial Sectors, Industrial Sector, Residential Sector, Power Plants) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Canadian Solar, JinkoSolar, Jolywood Group, LG Electronics, LONGi, Lumos Solar, MegaCell, Neo Solar Power, Neosun Inc, Panasonic, Premier Energies Limited, Prism Solar Technologies, Risen Energy Co., Ltd., Sharp Electronics, SolarWorld, Soleos, SunPower Corporation, Tigo Energy, Inc., Trina Solar, Yingli Green Energy |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |