Quick Navigation

Report Overview

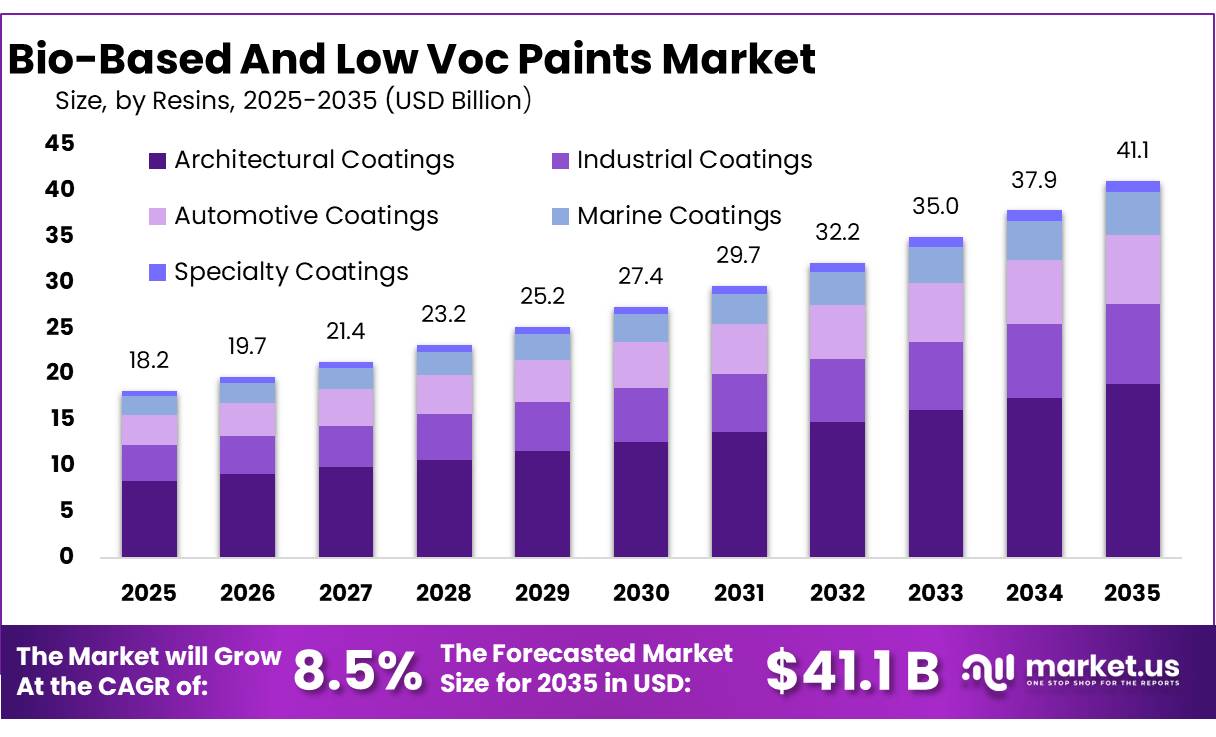

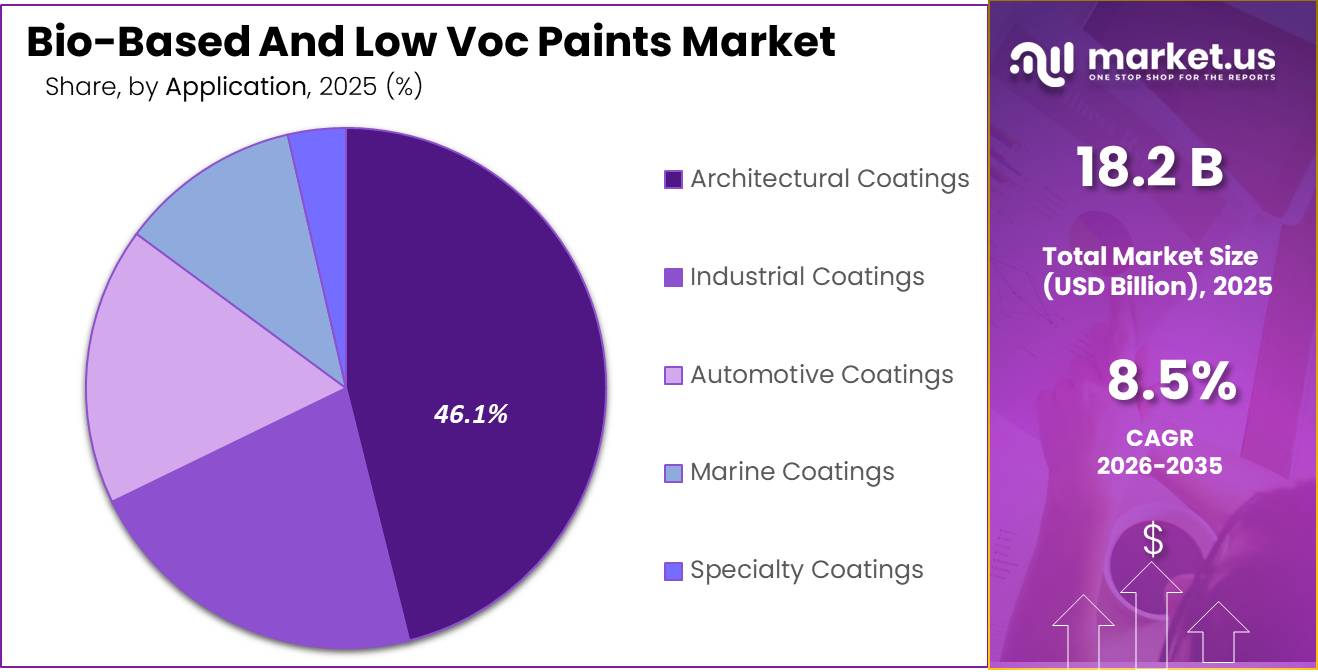

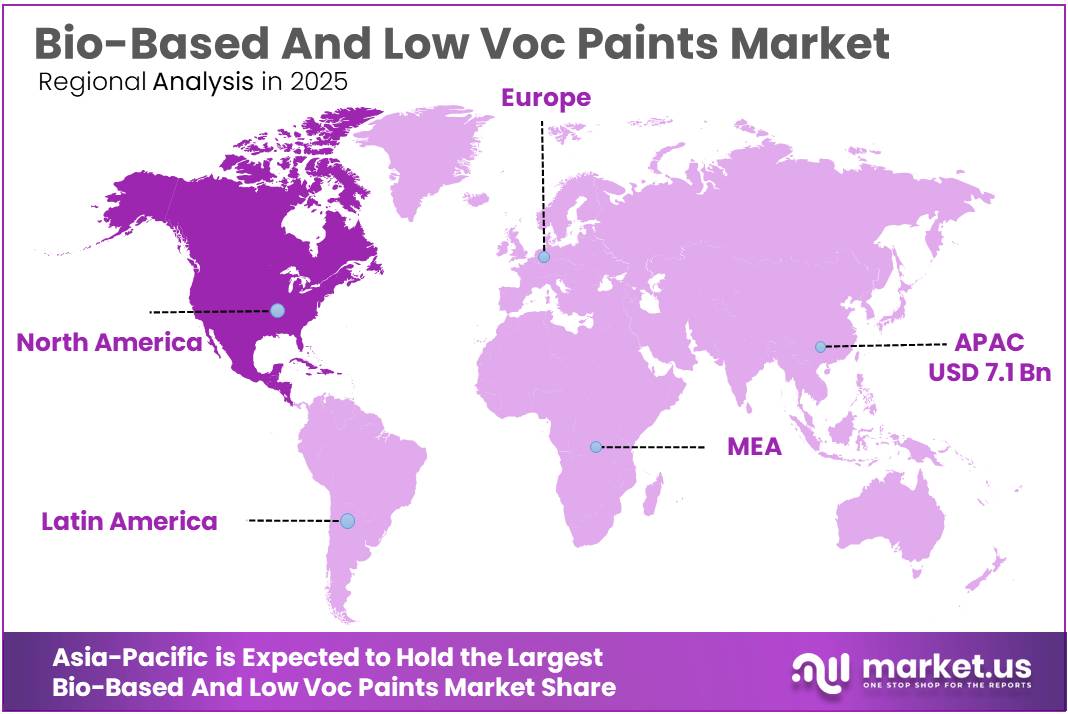

The Global Bio-Based And Low Voc Paints Market size is expected to be worth around USD 41.1 Billion by 2035, from USD 18.2 Billion in 2025, growing at a CAGR of 8.5% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 39.3% share, holding USD 7.1 Billion revenue.

Bio-based and low-VOC paints are moving from niche “green” products to mainstream coating systems as manufacturers replace fossil solvents with waterborne binders, renewable resins, bio-based additives and lower-emission formulation packages. Industrial demand is being shaped by indoor-air-quality rules, building sustainability requirements and corporate Scope 3 reduction programs. The U.S. EPA’s architectural coatings rule is estimated to reduce VOC emissions by 103,000 Mg/year, or 113,500 tons/year, while the EU Paints Directive limits VOC content in specified paints and varnishes to reduce solvent emissions.

The industrial scenario is supported by measurable coatings demand: the American Coatings Association states that the U.S. paint and coatings industry generated US$33.2 billion in product shipments, employed 312,000 workers, exported US$2.8 billion, and delivered a US$1.6 billion trade surplus in 2024.

Regulatory pressure is also strong. In the U.S., federal architectural-coating VOC limits are set under 40 CFR Part 59, while South Coast AQMD Rule 1113 lists limits such as 50 g/L for flats, 50 g/L for floor coatings and 100 g/L for form-release compounds. In Europe, the EU Paints Directive requires product VOC-limit labelling, and the EU Ecolabel criteria for decorative paints and varnishes are valid until 31 December 2032, supporting lower VOC and SVOC thresholds.

Driving factors include stricter air-quality rules, indoor-health awareness, and the need to reduce fossil raw-material dependence. In the U.S., EPA architectural coating VOC limits are expressed in grams per liter, while California regions can reduce industrial maintenance coating limits from 450 g/L to 250 g/L, and as low as 100 g/L in South Coast areas.

Regulation remains a core driver. The U.S. EPA’s architectural-coatings VOC rule is estimated to reduce VOC emissions by 103,000 Mg/year, or 113,500 tons/year, by limiting VOC content in coatings. In Europe, Directive 2004/42/EC limits VOCs in certain paints, varnishes, and vehicle refinishing products, supporting reformulation toward waterborne and low-solvent products.

The USDA BioPreferred Program also supports purchasing of bio-based products; interior latex and waterborne alkyd paints require 20% minimum biobased content, while interior oil-based and solventborne alkyd paints require 67%.

Cargill is contributing from the bio-based raw-material side through renewable coatings chemistries for epoxy, polyurethane, alkyd, acrylic, polyester, polyimide and polyamide systems. Its Priplast™ 3238 is described as a 100% bio-based amorphous polyester polyol for bio-based polyurethane systems, while Priamine™ 1071 is positioned for high-solids, low-VOC epoxy and polyurea formulations.

Key Takeaways

- Bio-Based And Low Voc Paints Market size is expected to be worth around USD 41.1 Billion by 2035, from USD 18.2 Billion in 2025, growing at a CAGR of 8.5%.

- Low-VOC Paints held a dominant market position, capturing more than a 48.7% share.

- Acrylic Resins held a dominant market position, capturing more than a 39.2% share.

- Architectural Coatings held a dominant market position, capturing more than a 46.1% share.

- Retail Stores held a dominant market position, capturing more than a 39.5% share.

- Asia-Pacific stands as the leading region in the bio-based and low VOC paints market, holding a dominant share of 39.3% with an estimated value of USD 7.1 billion.

By Type Analysis

Low-VOC Paints dominate with 48.7% driven by rising health awareness and strict environmental norms

In 2025, Low-VOC Paints held a dominant market position, capturing more than a 48.7% share. This strong presence is mainly linked to increasing consumer awareness about indoor air quality and the health risks associated with traditional paints. Homeowners, especially in urban areas, are gradually shifting toward safer alternatives that emit fewer harmful chemicals. Regulatory pressure has also played a big role, with governments encouraging the use of eco-friendly coatings across residential and commercial construction projects.

By Resins Analysis

Acrylic Resins lead with 39.2% as they offer strong durability and easy application

In 2025, Acrylic Resins held a dominant market position, capturing more than a 39.2% share. This segment stayed ahead mainly because of its reliable performance in both interior and exterior paints. Acrylic-based coatings are widely preferred as they dry quickly, resist weather changes, and maintain color for a longer time. These features make them a practical choice for both residential and commercial projects, especially where long-lasting finishes are important.

By Application Analysis

Architectural Coatings dominate with 46.1% as construction demand keeps rising steadily

In 2025, Architectural Coatings held a dominant market position, capturing more than a 46.1% share. This segment remained strong mainly because of continuous growth in residential and commercial construction. From new housing projects to renovation work, there is a constant need for paints that are safe, durable, and visually appealing. Low-VOC and bio-based coatings are becoming a preferred choice in buildings, especially where indoor air quality and environmental standards matter more than before.

By Distribution Channel Analysis

Retail Stores lead with 39.5% as buyers prefer to see and choose paints in person

In 2025, Retail Stores held a dominant market position, capturing more than a 39.5% share. This channel stayed ahead mainly because many customers still like to visit stores, check color options, and get advice before buying paints. For products like bio-based and low-VOC paints, where finish and shade matter a lot, physical stores offer a better buying experience. Store staff also help customers understand product features, which builds confidence, especially for first-time users of eco-friendly paints.

Key Market Segments

By Type

- Bio-Based Paints

- Low-VOC Paints

- Bio-Based and Low-VOC Hybrid Paints

By Resins

- Acrylic Resins

- Polyurethane Resins

- Epoxy Resins

- Alkyd Resins

- Other Resins

By Application

- Architectural Coatings

- Industrial Coatings

- Automotive Coatings

- Marine Coatings

- Specialty Coatings

By Distribution Channel

- Online Retail

- Retail Stores

- Contractors/Distributors

- Direct Sales

Emerging Trends

Shift toward plant-based innovation and green building materials shaping the market

One of the most noticeable trends in bio-based and low VOC paints is the growing shift toward plant-based innovation. Manufacturers are now actively using natural inputs like soybean oil, algae, and other renewable sources to develop safer coatings. This trend is strongly supported by sustainability goals and government-led green building programs. For example, initiatives such as LEED certification and environmental standards in many countries are pushing builders to use low-emission materials in homes, offices, and public spaces.

At the same time, the connection with agriculture is becoming stronger. According to FAO insights, global agrifood systems are under pressure to become more sustainable, with a clear focus on reducing environmental impact while maintaining production. This directly supports the use of renewable plant-based raw materials in industries like paints. By 2025–2026, companies are not just focusing on reducing VOC levels but also increasing the share of bio-based content in their products.

Rising use of advanced bio-materials supported by agriculture-linked supply chains

Another key trend is the increasing use of advanced bio-materials backed by strong agricultural supply chains. Paint companies are now investing in new technologies that convert biomass into high-performance coatings. This includes using plant oils, natural resins, and even microorganisms to create durable and low-emission paints. These developments are happening because industries are trying to reduce dependence on fossil fuels while still meeting performance standards.

From a broader perspective, agriculture plays a major role here. Large-scale production of crops like soybean and flaxseed ensures a steady supply of raw materials for bio-based chemicals and coatings. This link between farming and manufacturing is becoming more structured, with governments encouraging bio-economy models that connect both sectors. By 2026, this trend is expected to grow further as countries push for circular economy practices and reduced carbon footprints.

Drivers

Stricter VOC Rules Are Pushing Cleaner Paints

One major driving factor for bio-based and low-VOC paints is the rising pressure to cut harmful solvent emissions from buildings, homes and industrial coating use. Governments are making this shift stronger through rules on volatile organic compounds. In the U.S., the EPA’s Architectural Coatings rule is expected to cut VOC emissions by about 113,500 tons per year, which clearly supports demand for lower-VOC paint systems.

In Europe, Directive 2004/42/EC limits VOC content in paints, varnishes and vehicle refinishing products to reduce ground-level ozone formation. These rules make low-odor, water-based and bio-based paints more attractive for professional users, housing projects and public buildings. As a result, manufacturers are not treating low-VOC paint as a premium option only; it is becoming a compliance-driven requirement in many mature markets.

Large Ingredient Suppliers Are Making Bio-Based Paint More Practical

Another strong factor is the growing supply of renewable ingredients from large industrial companies. Cargill, a major food and bioindustrial company, operates in 70 countries with more than 155,000 employees, and its 2025 impact report says it creates nature-derived, bio-based products and biofuels. This matters because paint makers need reliable suppliers for bio-based oils, resins and additives at industrial scale. BASF also shows how large chemical companies are supporting the shift.

In 2025, BASF said its biomass-balanced coatings portfolio included more than 250 products across 3 regions and 3 business areas, while helping reduce around 8 million kg of CO₂ in 2024. This kind of development makes bio-based and low-VOC paints more realistic for wider commercial use, not just small sustainability projects.

Restraints

High cost of bio-based raw materials limits wider adoption

One of the main challenges for bio-based and low VOC paints is the higher cost of raw materials compared to traditional petroleum-based inputs. Many of these eco-friendly paints rely on agricultural feedstocks such as corn, sugarcane, and vegetable oils. However, producing these materials at scale is not always cheap. According to data from the Food and Agriculture Organization and global bioenergy studies, a large portion of these crops is already being used for fuel and energy. For example, around 16% of global corn production was used for bioethanol by 2022, showing how demand from multiple industries is increasing pressure on supply.

This rising competition pushes prices higher, making bio-based ingredients more expensive for paint manufacturers. Governments are promoting green alternatives, but subsidies are often not enough to fully balance the cost gap. By 2025–2026, many small and mid-sized manufacturers still find it difficult to switch completely to bio-based inputs because of these higher costs. As a result, end products like eco-friendly paints can be priced higher, which slows down adoption, especially in price-sensitive markets.

Competition with food supply creates supply chain pressure

Another major restraining factor comes from the direct link between bio-based materials and the food industry. Many of the raw materials used in eco-friendly paints come from crops that are also essential for food production. This creates a situation where industries compete for the same resources. Reports highlight that crops like sugarcane and vegetable oils are increasingly diverted toward biofuel and industrial use, raising concerns about food availability and pricing.

At the same time, global bio-based chemical production is heavily dependent on agriculture, with bioethanol alone accounting for more than 80% of total bio-based chemical production capacity. This shows how strongly industries rely on food-linked resources. Government bodies, including the FAO, have pointed out that such competition can lead to higher food prices and pressure on farmland. By 2026, this challenge continues to affect the steady supply of raw materials for bio-based paints.

Opportunity

Expanding agricultural output creating strong base for bio-based paint materials

One of the biggest growth opportunities for bio-based and low VOC paints is the steady rise in global agricultural production, especially oil crops that are used as raw materials. According to the Food and Agriculture Organization, global oil crop production reached around 1.2 billion tonnes by 2024, showing a strong increase of nearly 50% compared to earlier years. This matters because many bio-based paints depend on plant oils like soybean, palm, and sunflower. As production continues to grow, it becomes easier for manufacturers to secure raw materials at scale.

Governments are also supporting this shift by promoting bio-economy models, where agriculture supports industrial production. Farmers benefit from higher demand, while industries get a stable supply of renewable inputs. This balance is helping bio-based paints move from niche products to more mainstream use. Over time, this link between farming and manufacturing is expected to lower costs and improve availability, making sustainable paints more accessible to everyday consumers.

Rising vegetable oil production supports large-scale eco-friendly coatings

Another major opportunity comes from the sharp growth in vegetable oil production, which plays a key role in bio-based paint formulations. Data from FAO reports shows that vegetable oil production has increased by over 130% between 2000 and 2021, mainly driven by palm and soybean oil output. These oils are widely used not just in food, but also in industrial applications like coatings, adhesives, and paints.

This creates a strong push for industries to replace petroleum-based chemicals with plant-based alternatives. At the same time, the large-scale availability of vegetable oils ensures that production can meet growing demand without major supply issues. This trend is turning into a long-term opportunity, where the connection between agriculture and eco-friendly industries continues to strengthen, supporting the wider adoption of bio-based and low VOC paints.

Regional Insights

Asia-Pacific dominates with 39.3% share, valued at around USD 7.1 Bn driven by rapid construction growth

Asia-Pacific stands as the leading region in the bio-based and low VOC paints market, holding a dominant share of 39.3% with an estimated value of USD 7.1 billion. This strong position is largely supported by the region’s fast-growing construction sector, expanding urban population, and increasing awareness of environmentally friendly products. Countries such as China, India, and Southeast Asian nations are witnessing continuous infrastructure development, including residential housing, commercial spaces, and industrial facilities, all of which require large volumes of coatings.

The region also benefits from its massive population base, as Asia accounts for nearly 60% of the global population, which directly drives housing demand and renovation activities. Rising middle-class income levels and urbanization trends are encouraging consumers to invest in better-quality and safer paints, including low-VOC and bio-based options. Governments across the region are also promoting green building standards and environmental regulations, which further supports the adoption of eco-friendly coatings.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE is one of the strongest players in the bio-based and low VOC paints space due to its wide chemical portfolio and strong focus on sustainable coatings. In 2025, the company reported total sales of around €59.7 billion, showing its large global scale and influence in raw materials and resins used in paints. The company continues to invest in bio-based dispersions and low-emission technologies. Its coatings-related business has also generated billions in valuation, reflecting strong demand for eco-friendly solutions.

Cargill plays a key role by supplying bio-based raw materials like vegetable oils and plant-derived chemicals used in eco-friendly paints. The company operates in over 66 countries with more than 160,000 employees, highlighting its strong global supply network. It also contributes significantly to agricultural output, handling about 25% of U.S. grain exports, which supports the availability of renewable feedstock for coatings. This strong agricultural base gives Cargill an advantage in the bio-based paints value chain.

Benjamin Moore & Co is known for its premium architectural coatings and has steadily expanded its low-VOC and eco-friendly paint lines. The company operates through a network of over 7,500 independent retailers, making it a strong player in the residential paint segment. Its focus is on high-performance paints with reduced emissions, aligning with growing green building trends. The brand’s consistent presence in North America helps it maintain a strong position in the sustainable coatings segment.

Top Key Players Outlook

- BASF SE

- Cargill Inc.

- Benjamin Moore & Co. (Berkshire Hathaway)

- Auro Pflanzenchemie AG

- BioAmber

- Dulux

- Mowilex

Recent Industry Developments

BASF SE is playing a key role in the bio-based and low VOC paints value chain by supplying dispersions, resins, and sustainable chemical solutions used in eco-friendly coatings. In 2025, the company reported total sales of about €59.7 billion, showing its strong global presence and ability to support large-scale coatings production

By 2026, Benjamin Moore & Co is continuing to invest in sustainability, with internal initiatives such as recycling 2.5 million gallons of wash materials to reduce waste, highlighting its commitment to greener production practices

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 18.2 Bn |

| Forecast Revenue (2035) | USD 41.1 Bn |

| CAGR (2026-2035) | 8.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Bio-Based Paints, Low-VOC Paints, Bio-Based and Low-VOC Hybrid Paints), By Resins (Acrylic Resins, Polyurethane Resins, Epoxy Resins, Alkyd Resins, Other Resins), By Application (Architectural Coatings, Industrial Coatings, Automotive Coatings, Marine Coatings, Specialty Coatings), By Distribution Channel (Online Retail, Retail Stores, Contractors/Distributors, Direct Sales) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | BASF SE, Cargill Inc., Benjamin Moore & Co. (Berkshire Hathaway), Auro Pflanzenchemie AG, BioAmber, Dulux, Mowilex |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |