Quick Navigation

Report Overview

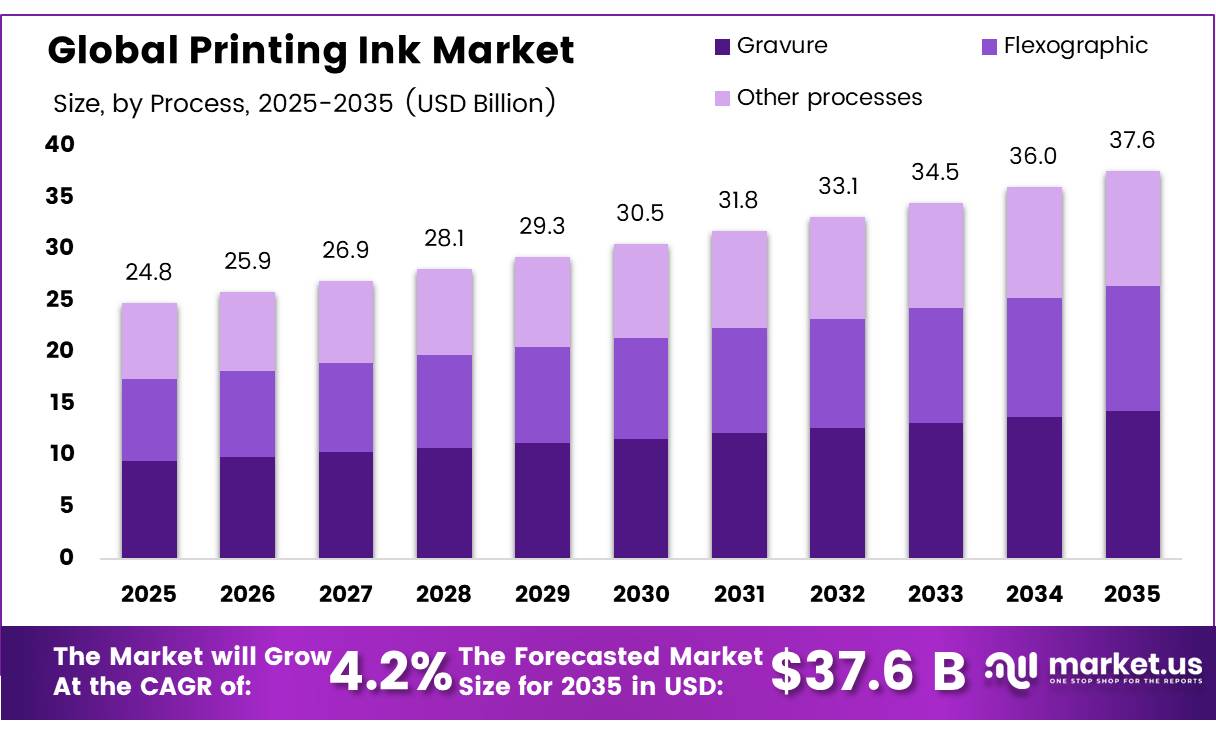

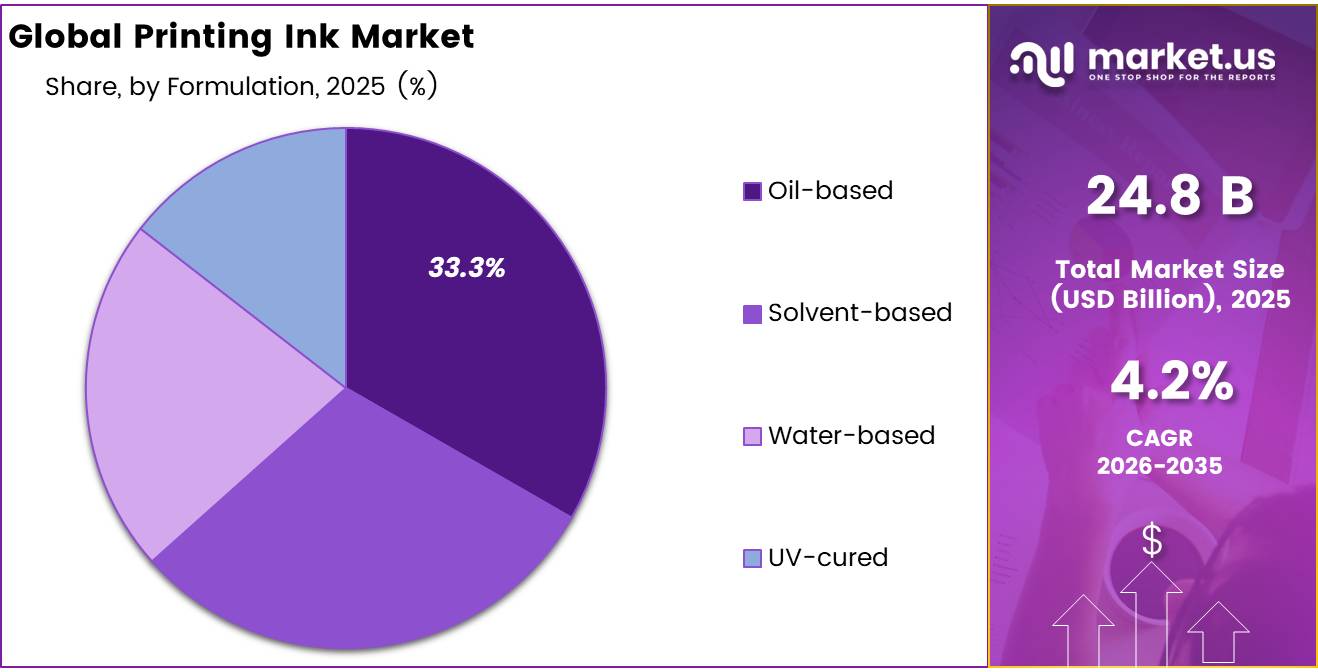

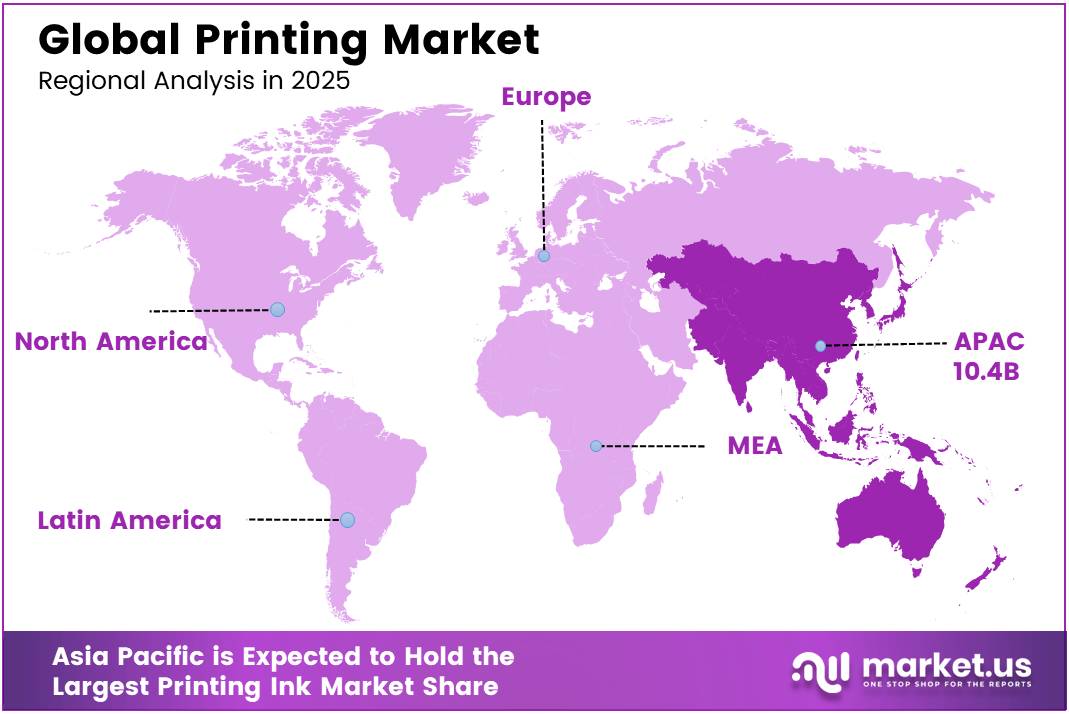

In 2025, the Global Printing Ink Market was valued at USD 24.8 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 4.2%, reaching about USD 37.6 billion by 2035. In 2025, Asia Pacific led the market, achieving over 42.1% share with a revenue of USD10.4Billion.

The printing ink industry is a critical segment of the global specialty chemicals and packaging value chain, supplying formulations for flexible packaging, labels, publications, textiles, and industrial printing. The industry is increasingly focused on developing water-based, UV-curable, and low-migration inks to comply with evolving environmental regulations and sustainability requirements.

- In April 2024, according to the U.S. Environmental Protection Agency (EPA), the Chemical Data Reporting (CDR) program reported 7.1 trillion pounds of regulated chemical production and imports in the United States, with Printing Ink Manufacturing (NAICS 325910) continuing to operate as a recognized downstream chemical manufacturing sector, demonstrating the industry’s reliance on a large specialty chemical supply base.

- In February 2025, according to the European Commission, the regulation entered into force, requiring all packaging placed on the EU market to be recyclable by 2030 and establishing packaging waste reduction targets of 5% by 2030, 10% by 2035, and 15% by 2040. These measures are accelerating demand for recyclable, low-VOC, and de-inkable printing ink formulations.

Key Takeaways

- The global printing ink market was valued at USD 24.8 billion in 2025.

- The global market is projected to grow at a CAGR of 4.2% and is estimated to reach USD 37.6 billion by 2035.

- On the basis of process, gravure printing dominated the market, constituting 38.2% of the total market share.

- Based on formulation, oil-based inks led the market, accounting for 33.3% of the total market share.

- By end-user, the packaging segment dominated the printing ink market, contributing 55.1% of the total market share.

- Based on grade, food grade printing inks held the major share in the market, accounting for 70.4% of the total demand.

- In 2025, Asia Pacific was the dominant regional market, accounting for 42.1% of the global printing ink market share.

Future growth opportunities are expected from recyclable packaging, food-contact applications, smart labels, and functional printing technologies. In August 2026, according to the European Commission, the Packaging and Packaging Waste Regulation will become applicable across all EU Member States from 12 August 2026, requiring harmonized compliance with recyclability and packaging composition standards. The regulation covers 100% of packaging placed on the EU market, encouraging manufacturers to invest in bio-based resins, low-migration pigments, and advanced ink technologies that support recycling efficiency, regulatory compliance, and long-term sustainable industrial growth

Process Analysis

Gravure Printing Dominates the Global Printing Ink Market.

Printing by means of process has enabled the gravure printing process to become the key segment that held 38.2% market share globally in the printing ink industry. Dominance of the segment was driven by their ability to produce high-quality print, better color accuracy, fast printing speeds, and applicability for high volume productions. The process is widely used in flexible packaging, magazines, catalogues, decorative laminates, and publication printing, where it is required to get high resolution graphics and premium look and feel.

Flexographic printing had continued to record significant growth owing to lower cost and shorter set up time along with rising utilization in label, corrugated box, and flexible packaging segments. Rising penetration of the segment in the rapidly growing packaging industry, such as e-commerce and retail packaging industry, further fuels the growth of the flexography process. Increasing penetration of digital and specialized printing process in textile, commercial publications, and customized packaging applications drives the segment growth.

Formulation Analysis

Oil-based Inks Command the Largest Share of the Global Printing Ink Market

In 2025, the Oil-based segment accounted for a leading 33.3% share in the market. This dominance is driven by through sheer performance. Printers and publishers rely on them for their exceptional colour intensity, strong adhesion, and the kind of durability that holds up against moisture and physical wear. Whether it’s a glossy magazine, a daily newspaper, or large-scale commercial packaging, oil-based inks deliver the crisp, long-lasting results that high-volume print operations depend on.

Solvent-based inks continue to account for a significant share of the global printing ink market, particularly in flexible packaging and label printing applications. Their fast-drying properties and strong adhesion to non-porous materials such as plastic films, aluminum foils, and laminates make them highly suitable for high-speed packaging operations where durability and efficiency are essential.

Meanwhile, UV-cured inks represent a smaller but rapidly expanding segment of the market. These inks offer instant curing, high print clarity, and superior performance on premium substrates, making them ideal for specialty packaging, decorative printing, and luxury labels. For instance, UV inks are extensively used in high-end cosmetics packaging and premium product labeling where vibrant colors, glossy finishes, and high durability are critical.

By End-User Analysis

Packaging represents the leading end-user segment in the global printing ink market, accounting for 55.1% of the total market share. The segment’s strong position is primarily driven by the rapid growth of e-commerce, rising demand for visually appealing packaging, and increasing consumption of packaged food & beverages, pharmaceuticals, and personal care products. Printing inks play a crucial role in packaging applications by improving product appearance, supporting brand identity, enabling product labeling, and enhancing consumer communication through high-quality graphics and information display.

The commercial publications, which encompass newspapers, magazines, books, brochures, and catalogues, is the fastest growing end-use application segment that contributes greatly towards market revenue. Despite the reduced use of printed material in the developed markets due to the expansion of the digital platforms, this segment remains highly relevant in developing economies due to increased reading habits.

Grade Analysis

Food Grade Printing Inks Dominate the Global Printing Ink Market

Food grade printing ink dominates the market, holding a commanding 70.4% share, as sustained growth in packaged food consumption keeps converters reliant on compliant, low-migration inks for labeling, date-coding, and branding. In June 2026, according to the USDA Economic Research Service, total U.S. food spending by consumers, businesses, and government entities reached $2.51 trillion in 2025, reflecting steady growth in both at-home and away-from-home food purchases. As converters remain bound by indirect food-additive compliance standards for packaging materials, manufacturers continue favoring formulations built specifically for food-contact safety, reinforcing this segment’s dominant position.

Pharmaceutical and clinical grade ink is gaining ground as the fastest-growing segment, driven by tightening track-and-trace obligations across drug packaging lines. According to the U.S. Food and Drug Administration, pharmaceutical trading partners must exchange product tracing data at the unit level through interoperable electronic systems, with compliance deadlines staggered through November 2026 under the Drug Supply Chain Security Act. This shift is steering manufacturers toward inks suited for precise, scannable coding on individual units.

Key Market Segments

By Process

- Gravure

- Flexographic

- Other processes

By Formulation

- Oil‑based

- Solvent‑based

- Water‑based

- UV‑cured

By End-user

- Packaging

- Commercial publication

- Textiles

- Other end‑users

By Grade

- Food grade

- Pharmaceutical / clinical grade

- Feed grade

Driver Analysis

Localization and OEM partnerships improving ink‑press integration economics

Press OEMs increasingly bundle inks and chemistry as part of installation, either through private‑label arrangements or strategic alliances with major ink companies, ensuring consistent performance, shorter setup times and guaranteed compatibility, which reduces downtime and waste for printers and supports higher ink volumes per installed press through optimized usage; printers may see reductions in spoilage and color‑matching rework of 10–20%, making higher‑quality OEM‑specified inks economically attractive even at price premiums.

Strategically, deeper OEM partnerships lock in recurring ink demand tied to the press base, turning one‑time capital sales into ongoing consumables revenue streams, and encourage data‑sharing on press performance that can feed into product improvement and predictive maintenance services. Over the next ≤2 years, expanded localization and OEM integration can plausibly add about +1.1 percentage points to CAGR beyond baseline expectations, especially in APAC, EU and North America where coordinated rollout of new press platforms and bundled chemistry is accelerating.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flexible packaging and label printing expansion driving high-performance inks | +2.1% | North America core, EU, APAC corridors, South America spill-over | Short term (≤ 2 years) |

| Digital, inkjet and UV-curable printing adoption accelerating ink consumption per job | +1.9% | North America, EU, China, India, ASEAN | Medium term (2-4 years) |

| Sustainability shift toward low-VOC, bio-based and biodegradable ink systems | +1.8% | EU regulatory hubs, North America, Japan, South Korea | Long term (≥ 4 years) |

| Growth of e-commerce packaging and brand security features boosting specialty inks | +1.5% | North America core, EU, China, India | Medium term (2-4 years) |

| Functional and electronics inks for IoT, smart packaging and printed electronics | +1.3% | North America, EU, China, South Korea, Taiwan | Long term (≥ 4 years) |

| Localization and OEM partnerships improving ink-press integration economics | +1.1% | APAC corridors, EU, North America | Short term (≤ 2 years) |

Restraint Analysis

Nitrocellulose and key resin shortages driving direct production disruption

Packaging ink producers reliant on nitrocellulose have reported allocation regimes, with some plants cutting output by double‑digit percentages 10–30% capacity curtailment in peak disruption periods—because alternative binders do not meet performance or regulatory requirements at scale, directly reducing available ink volumes for converters.

Lead times for key resins and solvents have expanded from typical 4–6 weeks to 8–12 weeks for some European and North American buyers during supply crunches, while spot prices for constrained components can spike 20–40% above contract levels, rendering some orders uneconomic and triggering temporary line idling.

This direct restriction on capacity and product availability is estimated to lower achievable CAGR by roughly 2.2 percentage points in severely affected regions over the next 1–2 years, as constrained packaging ink supply prevents converters from fully capturing underlying demand growth even when end‑customers continue to require printed packs.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nitrocellulose and key resin shortages driving direct production disruption | -2.2% | EU, North America core, APAC export corridors | Short term (≤ 2 years) |

| Fluctuating petrochemical and pigment prices compressing ink margins | -1.9% | EU, North America, China, India | Medium term (2-4 years) |

| Stringent VOC, migration and safety regulations limiting legacy ink portfolios | -1.7% | EU regulatory hubs, UK, North America | Medium term (2-4 years) |

| Declining demand for traditional print media reducing offset ink volumes | -1.5% | North America core, EU, Japan | Long term (≥ 4 years) |

| Capital and skill barriers to advanced digital and functional ink adoption | -1.3% | India, ASEAN, LATAM, Africa emerging | Long term (≥ 4 years) |

| Fragmented converter base and slow contract cycles delaying price passthrough | -1.1% | Global, with emphasis on SME printers | Medium term (2-4 years) |

Opportunity Analysis

SaaS‑enabled ink lifecycle and color management platforms

A SaaS platform that integrates color management, press profiling, consumption analytics and predictive maintenance could charge, for example, a few hundred to a few thousand dollars per site annually or a per‑click fee layered on top of ink purchases, potentially capturing 2–5% of customers’ ink spend as high‑margin software revenue; for a global supplier with several billion dollars of ink sales, converting even 10–15% of its installed base to such subscriptions by 2030 would add low‑hundreds of millions in incremental, capital‑light revenue.

Operationally, this can reduce waste by 10–20% and lower color‑related downtime by days per year per press fleet, improving converters’ unit economics and lowering customer acquisition cost for ink suppliers via stickier, data‑driven relationships. The pivot requires 2–4 years of investment in software, integration APIs with OEMs and training across North America, EU, India and China print hubs, after which recurring SaaS income and better retention could realistically lift overall market CAGR by about +2.0 percentage points above the baseline that assumes inks remain purely physical consumables.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| SaaS-enabled ink lifecycle and color management platforms | +2.0% | North America core, EU, India, China | Medium term (2-4 years) |

| Premium sustainable ink portfolios with certified low-carbon claims | +1.8% | EU regulatory hubs, North America, Japan, South Korea | Long term (≥ 4 years) |

| Nano-engineered high-performance gravure and large-format inks | +1.6% | China, EU, North America, APAC emerging markets | Medium term (2-4 years) |

| UV and hybrid systems for short-run, on-demand and web-to-print workflows | +1.5% | North America, EU, India, ASEAN | Short term (≤ 2 years) |

| Integrated security and functional inks for smart and traceable packaging | +1.4% | North America core, EU, China, GCC | Long term (≥ 4 years) |

| Regional M&A roll-ups of mid-tier sustainable and specialty ink producers | +1.2% | EU, North America, India, ASEAN | Medium term (2-4 years) |

Challenges Analysis

Ongoing raw‑material and energy volatility

Typical year‑on‑year swings of 10–20% in key petrochemicals and pigments translate into 5–10% variability in total variable cost per tonne of ink, and when combined with electricity and gas tariffs that can rise 5–15% versus pre‑2024 levels, many producers face quarterly gross‑margin compression of 200–300 basis points before any pricing response.

Because converters often operate on annual contracts, ink suppliers absorb a portion of this volatility, which forces higher working capital buffers and risk‑adjusted hurdle rates for capex: a mid‑sized packaging ink plant might hold an extra 2–3 weeks of raw‑material inventory, tying up several million dollars and raising inventory carrying costs by 50–100 basis points of sales, while delaying capacity expansions by 12–24 months until price trajectories stabilize. Over a 2–4 year horizon, the need to hedge, over‑stock and ration capex to cope with volatile inputs is likely to impose around 1.4 percentage points of friction drag on potential CAGR, as companies grow more slowly than underlying packaging and digital print demand would allow in a stable cost environment.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Ongoing raw-material and energy volatility | -1.4% | EU regulatory hubs, North America core, APAC logistics corridors | Medium term (2-4 years) |

| Complex multi-layer regulatory compliance and documentation | -1.3% | EU, UK, North America, Japan | Long term (≥ 4 years) |

| Supply-chain visibility and transport inefficiencies | -1.1% | APAC export routes, EU ports, North America inland networks | Medium term (2-4 years) |

| Structural print-media decline and asset reconfiguration | -1.0% | North America core, EU, Japan | Long term (≥ 4 years) |

| Talent and digital-skills shortages in printing and ink formulation | -0.9% | EU innovation hubs, North America, India, China | Long term (≥ 4 years) |

| Data and systems fragmentation across converters and OEMs | -0.8% | Global multi-region operations | Medium term (2-4 years) |

Geopolitical Impact Analysis

Geopolitical Headwinds and Their Growing Impact on the Global Printing Ink Market

Geopolitical tensions and trade uncertainties have created notable challenges for the global printing ink market. Since key raw materials such as pigments, resins, and solvents are sourced from specific regions, any political instability or trade disruption directly affects their availability and pricing, putting pressure on manufacturers’ costs and profit margins.

Trade protectionism has added another layer of complexity. Rising U.S. tariffs triggered retaliatory measures from trade partners, causing production costs to rise significantly and creating severe supply chain disruptions, with the industry’s heavy reliance on China making smaller manufacturers particularly vulnerable. As a result, many companies are now diversifying their sourcing toward countries such as Vietnam, India, and Mexico to reduce dependency on a single region.

In Asia Pacific, tariff uncertainty has disrupted supply chains and driven up costs, while countries heavily reliant on U.S. exports have witnessed a slowdown in packaging demand. Similarly, ongoing tensions in the Middle East have affected the availability of essential raw materials needed for high-quality ink production. Despite these challenges, geopolitical pressures are pushing the industry toward greater supply chain resilience. Ink manufacturers are increasingly investing in localized production and alternative sourcing strategies to protect their operations and maintain long-term stability in an increasingly uncertain global environment.

Regional Analysis

Asia Pacific Leads the Global Printing Ink Market Capturing 42.1% of Total Revenue

Asia Pacific dominates the global printing ink market, contributing approximately 42.1% of the total market revenue, valued at around USD 10.4 billion. This market is driven by the region’s massive manufacturing base, rapid industrialization, and explosive e-commerce growth across China, India, Japan, and Southeast Asia. Rising urbanization and growing disposable incomes continue to fuel demand for packaged goods, directly sustaining robust ink consumption across the region.

North America represents a mature and innovation-driven printing ink market, supported by strong packaging demand, expanding e-commerce activities, and increasing adoption of sustainable ink formulations. Europe also holds a significant market share due to strict environmental regulations and growing demand for eco-friendly and biodegradable inks, particularly in Germany, the UK, and France.

Meanwhile, the Middle East & Africa is witnessing steady growth driven by expanding packaging infrastructure and industrialization initiatives across GCC countries. Latin America is emerging as a promising market due to rising demand for packaged food & beverages and increasing investments in local printing and packaging industries.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global printing ink market is highly competitive and characterized by the presence of several multinational and regional manufacturers focusing on product innovation, sustainability, technological advancements, and expansion of production capacities. Major players are increasingly investing in eco-friendly ink formulations such as water-based, UV-cured, and bio-based inks to comply with strict environmental regulations and meet rising demand for sustainable packaging solutions.

Leading companies operating in the global printing ink market include DIC Corporation, Sakata INX Corporation, Toyo Ink SC Holdings Co., Ltd. are also emphasizing research and development activities to improve print quality, drying efficiency, color performance, and compatibility with advanced printing technologies including digital and flexographic printing. Strategic collaborations with packaging manufacturers, commercial printers, and consumer goods companies are helping market players strengthen their global market presence and supply chain networks.

In addition, manufacturers are expanding operations across emerging economies in Asia Pacific and Latin America to capitalize on growing packaging and labeling demand. The increasing adoption of smart packaging, specialty inks, and conductive inks for industrial and electronic applications is further encouraging companies to diversify their product portfolios and strengthen technological capabilities.

The Major Players In The Industry

- Sun Chemical (DIC Group)

- Flint Group

- Siegwerk Druckfarben AG & Co. KGaA

- Toyo Ink SC Holdings Co., Ltd.

- Sakata INX Corporation

- hubergroup Deutschland GmbH

- Tokyo Printing Ink Mfg. Co., Ltd.

- T&K Toka Co., Ltd.

- FUJIFILM Holdings Corporation

- SICPA Holding SA

- Wikoff Color Corporation

- ALTANA AG (incl. ACTEGA inks & coatings)

- Dainichiseika Color & Chemicals Mfg. Co., Ltd.

- Yip’s Chemical Holdings Limited

- Agfa-Gevaert Group (Agfa inks)

- DuPont de Nemours, Inc.

- Covestro AG

- Marabu GmbH & Co. KG

- Alite Inks

- Others Key Players

Key Development

- In May, DuPont introduced its Artistri PN1000 low-viscosity pigment inks during the drupa 2024 exhibition, focusing on improved optical density, enhanced print quality, and compliance with food-contact packaging regulations. The development reflects the growing industry focus on high-performance and safer ink solutions for packaging applications.

- In March 2024, DIC India inaugurated a new toluene-free liquid ink manufacturing plant in Gujarat with an annual production capacity of 10,000 tons. The investment of approximately INR 1.1 billion (USD 0.013 billion) highlights the company’s strategy to expand sustainable ink production and strengthen its presence in the environmentally friendly packaging ink segment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 24.8 Bn |

| Forecast Revenue (2035) | USD 37.6 Bn |

| CAGR (2026-2035) | 4.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Process (Gravure, Flexographic, and Other Processes), By Formulation (Oil-based, Solvent-based, Water-based, and UV-cured), By End-user (Packaging, Commercial Publication, Textiles, and Other End-users), By Grade (Food Grade, Pharmaceutical/Clinical Grade, and Feed Grade) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | DIC Corporation, Sun Chemical, Flint Group, Siegwerk Druckfarben AG & Co. KGaA, Toyo Ink SC Holdings Co., Ltd., Sakata INX Corporation, hubergroup Deutschland GmbH, Tokyo Printing Ink Mfg. Co., Ltd., T&K Toka Co., Ltd., FUJIFILM Holdings Corporation, SICPA Holding SA, Wikoff Color Corporation, ALTANA AG, Dainichiseika Color & Chemicals Mfg. Co., Ltd., Yip’s Chemical Holdings Limited, Agfa-Gevaert Group, DuPont de Nemours, Inc., Covestro AG, Marabu GmbH & Co. KG, Alite Inks, Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |