Quick Navigation

Report Overview

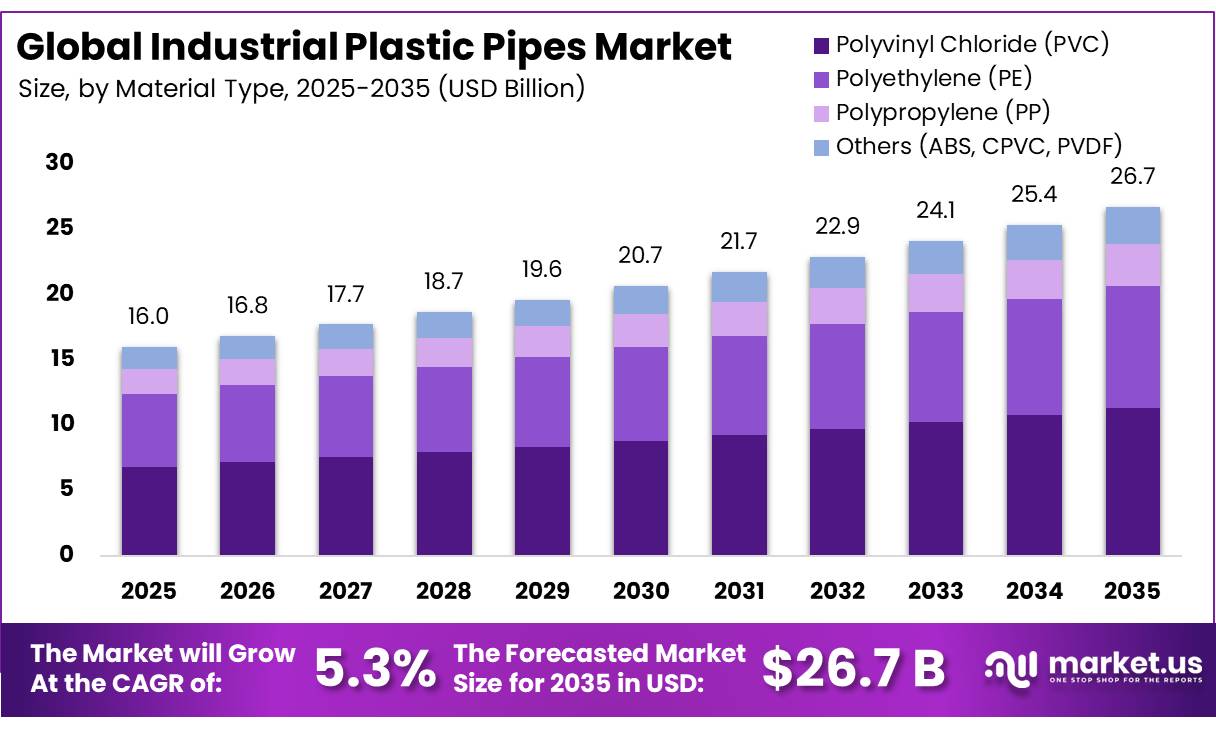

In 2025, the Global Industrial Plastic Pipes Market was valued at USD 16.0 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.3%, reaching about USD 26.7 billion by 2035. In 2025, Asia Pacific led the market, achieving over 42.2% share with a revenue of USD 6.8 Billion.

Industrial plastic pipes are widely used across water distribution, wastewater management, industrial processing, mining, oil and gas transportation, and agricultural irrigation systems due to their corrosion resistance, durability, lightweight structure, and lower maintenance requirements compared to conventional metal piping. Materials such as polyvinyl chloride (PVC), high-density polyethylene (HDPE), polypropylene (PP), and chlorinated polyvinyl chloride (CPVC) have become essential components of modern infrastructure projects.

- According to the WHO/UNICEF Joint Monitoring Programme (JMP) and the United Nations, approximately 1 billion people lacked access to safely managed drinking water services in 2024, underscoring the growing need for investments in water supply infrastructure, treatment facilities, and expanded pipeline networks across both developed and developing regions worldwide.

Key Takeaways

- The Global Industrial Plastic Pipes Market was valued at USD 16.0 billion in 2025.

- The market is projected to grow at a CAGR of 5.3% and is estimated to reach USD 26.7 billion by 2035.

- By material type, Polyvinyl Chloride (PVC) led the market in 2025 with a 42.5% share, supported by its widespread use in water supply and sewerage networks.

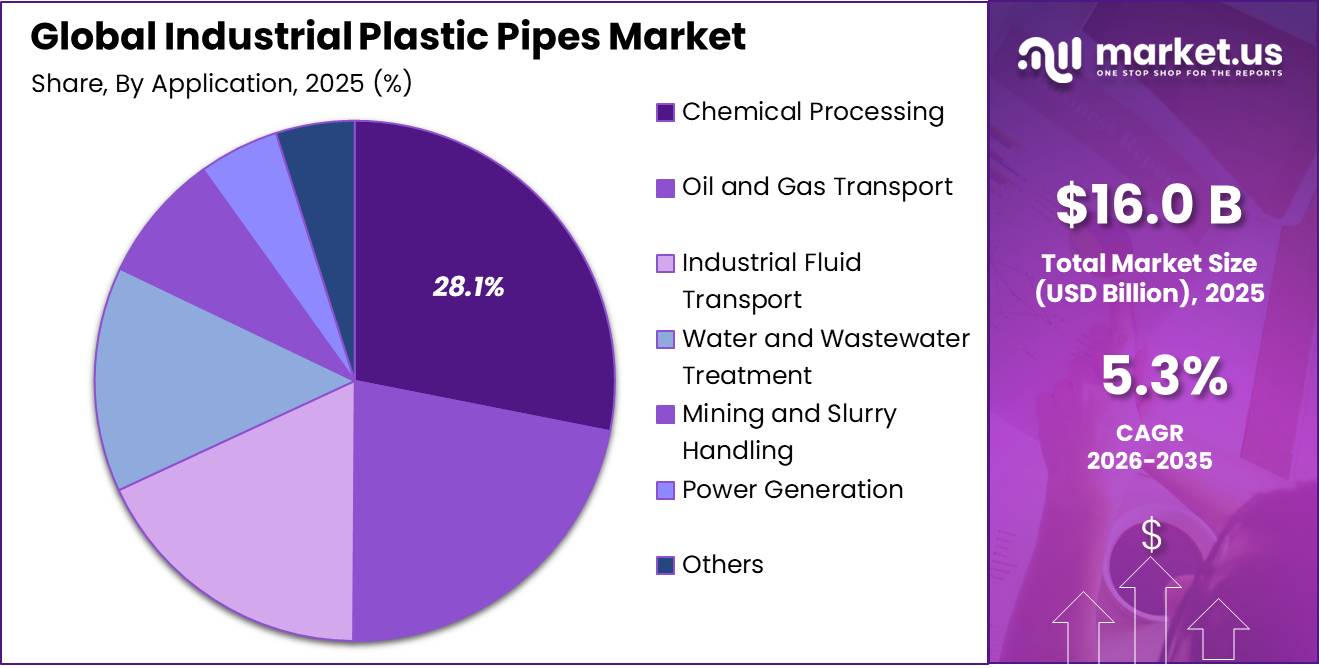

- By application, Chemical Processing held the largest share at 28.1% in 2025, driven by demand for corrosion-resistant piping in process industries.

- By pressure rating, High Pressure (Above 12 bar) systems dominated with a 48.2% share in 2025, reflecting demand from oil & gas and industrial fluid transport.

- By diameter, Medium Diameter (200-600 mm) pipes accounted for the largest share at 42.1% in 2025, balancing flow capacity with installation economics.

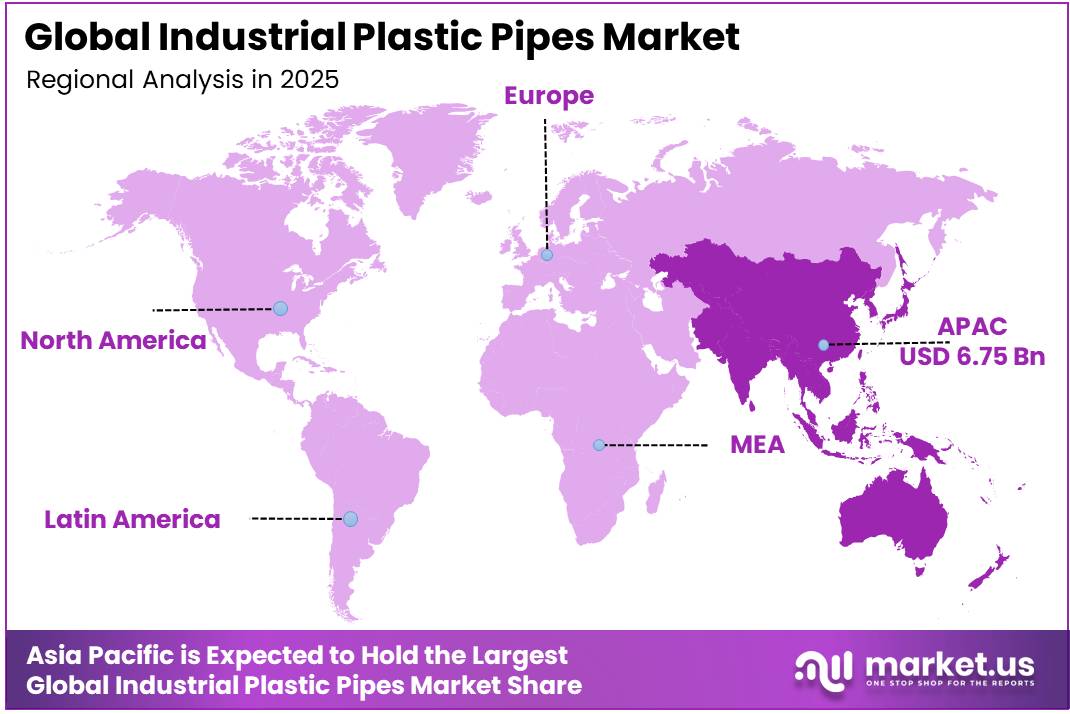

- By region, Asia Pacific led the market in 2025 with a 42.2% share, supported by rapid industrialization and infrastructure investment.

The World Bank estimates that nearly 57% of the global population lives in urban areas in 2024, creating sustained demand for municipal water distribution and wastewater systems that extensively utilize plastic piping technologies. As cities expand and industrial facilities modernize, demand for durable pipe systems continues to rise. Plastic pipes are increasingly preferred in these projects because they offer long service life, chemical resistance, and lower installation costs than many traditional materials.

- In March 2026, the IEA reported that the average desalination plant was roughly 10 times larger than 15 years earlier, while the largest facilities could produce around 1 million cubic metres of water per day. This expansion indicates increasing requirements for extensive water-intake, treatment, brine-discharge, and distribution pipeline infrastructure.

Industrial Plastic Pipes Market Segmentation

Material Type Analysis

Polyvinyl Chloride (PVC) leads the market due to its durability and broad industrial usage.

In 2025, Polyvinyl Chloride (PVC) held a dominant market position, capturing more than a 42.5% share of the industrial plastic pipes market. The material maintained its leading position because of its strong resistance to corrosion, chemicals, and moisture, making it suitable for a wide range of industrial and infrastructure applications. PVC pipes continued to be widely used in water distribution systems, wastewater networks, industrial fluid transportation, and construction projects where long service life and low maintenance requirements were important considerations.

- In November 2025, the U.S. Environmental Protection Agency announced USD 3 billion in new funding and USD 1.1 billion in redistributed funding for identifying and replacing lead service lines. The agency’s updated inventory estimated that approximately 4 million lead service lines remained active across the United States, including 3 million confirmed lines and around 1 million estimated among service lines with unknown materials.

Polyethylene (PE) is the fastest growing segment in the industrial plastic pipes market. In 2025, the segment experienced strong demand due to its flexibility, impact resistance, and ability to handle high-pressure applications. PE pipes gained wider acceptance in industrial water transport, mining operations, gas distribution networks, and infrastructure projects where durability and leak-free performance were essential.

Application Analysis

Chemical Processing leads the market due to its constant demand for corrosion-resistant piping solutions.

In 2025, Chemical Processing held a dominant market position, capturing more than a 28.1% share of the industrial plastic pipes market by application. The segment maintained its leading position because chemical manufacturing facilities require piping systems that can safely transport aggressive liquids, acids, alkalis, and other corrosive substances.

- In December 2025, Eurostat reported that the European Union produced 224 million tonnes of chemicals in 2024, representing a 6% increase from 2023. Production included 172 million tonnes of chemicals hazardous to human health and 66 million tonnes hazardous to the environment.

Oil and gas transport is the fastest growing segment in the industrial plastic pipes market by application. In 2025, the segment witnessed increasing adoption of plastic piping solutions for fluid gathering, water injection systems, produced water management, and selected hydrocarbon transport applications. Operators increasingly preferred advanced plastic pipes because of their resistance to corrosion, lightweight design, and ease of installation across challenging terrains. The growing focus on reducing maintenance costs and extending pipeline service life further supported demand within the sector.

Pressure Rating Analysis

High Pressure (Above 12 bar) dominates the market due to its extensive use in demanding industrial operations.

In 2025, High Pressure (Above 12 bar) held a dominant market position, capturing more than a 48.2% share of the industrial plastic pipes market by pressure rating. The segment led the market because high-pressure piping systems are widely required across industries such as chemical processing, oil and gas, mining, water transmission, and industrial manufacturing. These applications demand pipes that can withstand elevated operating pressures while maintaining safety and performance over long periods.

- In June 2026, PHMSA reported that the United States had 413,289 miles of natural-gas transmission and gathering pipelines in 2025, including 300,158 miles of transmission pipelines. PHMSA also states that transmission pipelines may operate at pressures exceeding 1,000 psi.

Medium Pressure (5–12 bar) is the fastest growing segment in the industrial plastic pipes market by pressure rating. In 2025, the segment recorded strong growth as industries increasingly adopted medium-pressure piping systems for water distribution, wastewater management, industrial fluid transfer, and utility infrastructure projects. Ongoing infrastructure development and modernization projects contributed to greater adoption of medium-pressure plastic pipes.

Diameter Analysis

Medium Diameter (200–600 mm) leads the market due to its wide use in industrial and utility pipeline networks

In 2025, Medium Diameter (200–600 mm) held a dominant market position, capturing more than a 42.1% share of the industrial plastic pipes market by diameter. The segment accounted for a significant portion of demand because these pipes are commonly used across water transmission systems, wastewater networks, industrial processing facilities, and utility infrastructure projects. Their size makes them suitable for handling substantial fluid volumes while maintaining installation flexibility and operational efficiency.

- In March 2026, the Oklahoma Department of Environmental Quality listed a USD 2.5 million project for Grand Lake Public Works Authority involving 6,150 linear feet of 12-inch HDPE waterline, booster-pump rehabilitation, a 1-million-gallon standpipe, and a backup generator.

Small Diameter (Below 200 mm) is the fastest growing segment in the industrial plastic pipes market by diameter. In 2025, the segment experienced notable growth due to increasing use in local distribution networks, industrial fluid transfer lines, process piping systems, and facility-level infrastructure. These pipes are widely selected for applications that require efficient fluid movement, easier installation, and lower material consumption. Their lightweight structure and adaptability make them suitable for both new installations and replacement projects.

Key Market Segments

By Material Type

- Polyvinyl Chloride (PVC)

- Polyethylene (PE)

- Polypropylene (PP)

- Others (ABS, CPVC, PVDF)

By Application

- Chemical Processing

- Oil and Gas Transport

- Industrial Fluid Transport

- Water and Wastewater Treatment

- Mining and Slurry Handling

- Power Generation

- Others

By Pressure Rating

- High Pressure (Above 12 bar)

- Medium Pressure (5-12 bar)

- Low Pressure (Below 5 bar)

By Diameter

- Medium Diameter (200-600 mm)

- Small Diameter (Below 200 mm)

- Large Diameter (Above 600 mm)

Driver Analysis

Lead-line replacement and service-line inventory compliance pull-through

EPA-required lead service line inventories became enforceable by October 16, 2024, and utilities that missed the deadline face violation exposure, public notification requirements, and in larger systems online inventory disclosure obligations, which converts pipe replacement from a deferred maintenance choice into a tracked compliance program. The U.S. federal funding base is also material: the Bipartisan Infrastructure Law provides $15 billion for lead service line replacement through FY2022-FY2026, creating a defined funding runway that directly supports HDPE, PVC, and related distribution-pipe demand where utilities replace legacy metallic lines and associated fittings.

The volume impact is amplified by the final 2024 Lead and Copper Rule Improvements framework referenced by state agencies, including replacement rates of 7% per year and a 10-year replacement orientation in implementation messaging, which favors standardized, bid-eligible plastic pipe systems because utilities need lower installed cost, corrosion resistance, and rapid contractor deployment rather than premium material complexity. Commercially, this driver shifts demand toward municipal-spec products, tracing/documentation services, and bundled pipe-plus-connection offerings, raising visibility for manufacturers with utility approvals and local distribution coverage.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lead-line replacement and service-line inventory compliance pull-through | +2.4% | North America core, EU spill-over | Short term (≤\leq≤ 2 years) |

| Public water and wastewater capex acceleration | +2.1% | North America core, APAC corridors, Middle East project zones | Medium term (2-4 years) |

| Irrigation and water-efficiency pipeline modernization | +1.6% | North America West, India corridors, arid agriculture belts | Medium term (2-4 years) |

| Metal-to-plastic substitution in utility networks | +1.4% | North America core, EU, selected Latin America | Medium term (2-4 years) |

| Building code and underground utility installation activity | +1.1% | North America, urban APAC, GCC cities | Short term (≤\leq≤ 2 years) |

| Resin inflation and compliance-led product mix upgrade | +0.8% | Global, strongest in North America and EU manufacturing bases | Long term (≥\geq≥ 4 years) |

Restraint Analysis

Housing starts slow down.

The clearest demand-side restraint is the deterioration in near-term construction throughput, because plastic pipe consumption in building services, drainage, site utilities, and light infrastructure is highly correlated with project starts and completions rather than permits alone; in May 2026, U.S. privately owned housing starts fell to 1.177 million units annualized, down 15.4% month over month and 8.7% year over year, while completions fell to 1.313 million, down 8.1% from April and 14.2% from May 2025, which implies weaker short-cycle call-offs for PVC, CPVC, PE, and ancillary fittings even where the permit pipeline remains relatively stable at 1.413 million.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing starts slowdown | -2.0% | North America core, EU spill-over, urban APAC | Short term (≤\leq≤ 2 years) |

| Resin and energy cost volatility | -1.7% | Global, strongest in North America and EU | Short term (≤\leq≤ 2 years) |

| PVC regulatory exposure | -1.4% | North America core, EU compliance-heavy markets | Medium term (2-4 years) |

| Public funding release delays | -1.2% | North America core | Short term (≤\leq≤ 2 years) |

| Standards and approval lag | -0.9% | North America, EU, selected APAC corridors | Medium term (2-4 years) |

| Freight and warehousing inflation | -0.8% | Global, strongest in large-landmass markets | Short term (≤\leq≤ 2 years) |

Opportunity Analysis

Hydrogen-ready gas distribution

Hydrogen-ready polymer infrastructure is a long-dated adjacency and therefore a true opportunity, because it is not yet a mainstream demand engine for industrial plastic pipes but could become a premium niche if producers qualify formulations and barrier concepts for low-blend and pilot-network applications before standards crystallize; California’s independent study found hydrogen blends up to 5% in natural gas are generally safe, while blends above 20% have a higher likelihood of permeating plastic pipes, making material engineering, testing, and selective-use designs an open technical-commercial white space rather than a commoditized market today.

The upside is strategic because even limited early adoption can support premium pricing, higher R&D-backed switching costs, and footholds in future gas-network retrofits, especially in EU pilots and U.S. decarbonization hubs where hydrogen funding programs are expanding, and manufacturers that secure field data and utility approvals early could capture 10% to 20% higher ASPs on qualified specialty product lines than on standard gas-distribution pipe.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Water reuse pipe networks | +2.3% | North America West, GCC, Australia, EU drought belts | Medium term (2-4 years) |

| Rural tap-water scale-up | +2.0% | India core, South Asia spill-over, Africa emerging markets | Medium term (2-4 years) |

| Stormwater and flood systems | +1.7% | North America core, EU flood-prone corridors, coastal APAC | Short term (≤\leq≤ 2 years) |

| Pipe-as-a-system monetization | +1.3% | North America, EU, India, Middle East | Short term (≤\leq≤ 2 years) |

| Hydrogen-ready gas distribution | +1.1% | EU pilots, California, selected APAC energy hubs | Long term (≥\geq≥ 4 years) |

| Rural utility financing channels | +0.9% | North America rural, India tier-2/3, LATAM | Short term (≤\leq≤ 2 years) |

Challenges Analysis

Multi-layer compliance burden

Compliance complexity with evolving chemical, safety, and performance regulations constitutes a long-horizon challenge rather than an outright restraint because PVC, PE, and related pipes remain approved and widely used, yet the regulatory trajectory such as EPA’s TSCA risk evaluation for vinyl chloride, designated a High-Priority Substance with production volumes between 10 and less than 20 billion pounds per year and recognized as a known human carcinogen requires continuous monitoring, data collection, testing, and potential reformulation.

These evolving requirements do not shut down sales but impose 1% to 3% of revenue in ongoing compliance, testing, auditing, and certification costs for larger firms and a disproportionate burden for smaller producers, while lengthening time-to-market for new grades by several quarters, reducing flexibility to pivot product portfolios quickly, and cumulatively trimming roughly 0.8 to 1.0 percentage point from otherwise attainable CAGR in a lighter-regulation scenario.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Resin price whiplash | -1.4% | North America core, EU hubs, APAC exporters | Medium term (2-4 years) |

| Skilled extrusion labor gaps | -1.2% | North America, EU manufacturing belts, India | Medium term (2-4 years) |

| Volatile freight and handling | -1.0% | North America corridors, EU, APAC trade lanes | Short term (≤\leq≤ 2 years) |

| Multi-layer compliance burden | -0.9% | North America, EU regulatory hubs | Long term (≥\geq≥ 4 years) |

| Capex and asset-utilization risk | -0.8% | Global, especially fast-growing APAC | Long term (≥\geq≥ 4 years) |

| Data and asset-visibility gaps | -0.7% | Global, strongest in fragmented emerging markets | Medium term (2-4 years) |

Geopolitical Impact Analysis

Ongoing Conflicts Influence Raw Material Global And Supply Chains.

The ongoing geopolitical tensions, including the Russia–Ukraine conflict and instability in parts of the Middle East, have continued to affect the industrial plastic pipes market in 2025 and 2026. Industrial plastic pipes depend heavily on petrochemical-based raw materials such as polyethylene (PE) and polyvinyl chloride (PVC), making the industry sensitive to disruptions in energy and chemical supply chains. Fluctuations in crude oil and natural gas markets have created uncertainty in raw material pricing, increasing production costs for pipe manufacturers in several regions.

At the same time, reconstruction and infrastructure rehabilitation activities in conflict-affected areas are creating future opportunities for the industrial plastic pipes sector. Water supply networks, wastewater systems, and utility infrastructure often require significant rebuilding after periods of disruption. As governments and international organizations plan long-term recovery projects, demand for durable and cost-effective plastic pipe systems is expected to rise. While geopolitical tensions continue to create short-term supply chain challenges, they are also encouraging greater investment in infrastructure resilience, which may support sustained demand for industrial plastic pipes in the coming years.

Regional Analysis

Asia-Pacific Dominates Industrial Plastic Pipes Market with 42.2% Share

Asia-Pacific emerged as the dominant regional market for industrial plastic pipes, accounting for 42.2% of the global market and reaching a value of USD 6.75 billion in 2025. The region’s leadership is supported by large-scale investments in water infrastructure, industrial expansion, urban development, and utility modernization projects. Rapid population growth and increasing industrial activity across several Asia-Pacific economies have created strong demand for efficient water distribution and wastewater management systems, where plastic pipes are extensively used. Industrial plastic pipes continue to benefit from investments because of their durability, corrosion resistance, and lower installation costs compared to traditional materials.

North America maintained a significant position due to ongoing replacement of aging water infrastructure and increasing investments in industrial facilities. Utilities and municipalities across the region have focused on upgrading pipeline networks to improve efficiency and reduce water losses. Europe also represented an important market, supported by strict environmental regulations, sustainable construction practices, and continued investments in wastewater treatment infrastructure.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Industrial Plastic Pipes market operates in a moderately fragmented competitive environment, with several international and regional manufacturers competing across different material categories, pressure ratings, and end-use applications. No single company controls a dominant portion of the global market, as demand is spread across construction, water management, industrial processing, mining, and energy sectors.

Key global participants include Aliaxis Group, JM Eagle, Georg Fischer, Wavin, China Lesso Group Holdings. These companies focus on expanding production capacity, developing high-performance pipe materials, and strengthening their presence in water infrastructure and industrial applications. Many leading players are also investing in sustainable manufacturing practices and recyclable plastic solutions to align with changing environmental requirements.

The Major Players In The Industry

- JM Eagle, Inc.

- Aliaxis Group S.A.

- Sekisui Chemical Co., Ltd.

- Georg Fischer Ltd.

- Chevron Phillips Chemical Company

- Westlake Pipe & Fittings

- China Lesso Group Holdings Ltd.

- Finolex Industries Ltd.

- Astral Poly Technik Limited

- Prince Pipes and Fittings Ltd.

- Supreme Industries Ltd.

- Uponor Corporation

- Rehau Group

- Wavin N.V.

- Pipelife International GmbH

- Charlotte Pipe and Foundry Company

- ATC Plastics, LLC

- Plastika Kritis S.A.

- Future Pipe Industries

- AMIBLU (Amiblu Holding GmbH)

Key Development

- In April 2026, JM Eagle reported an operating network of 17 U.S. manufacturing plants, 2 distribution centres, more than 1,200 employees and annual revenue exceeding US$2 billion. Its logistics system included around 100 trucks, while annual pipe production was described as enough to circle the globe 12 times.

- In March 2026, China Lesso reported 2025 revenue of RMB 24,315 million, with plastic piping systems contributing RMB 20,784 million, or 5% of total revenue, showing its continued focus on core pipe products.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 16.0 Bn |

| Forecast Revenue (2035) | USD 26.7 Bn |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Polyvinyl Chloride (PVC), Polyethylene (PE), Polypropylene (PP), and Others (ABS, CPVC, PVDF)), By Application (Chemical Processing, Oil and Gas Transport, Industrial Fluid Transport, Water and Wastewater Treatment, Mining and Slurry Handling, Power Generation, and Others), By Pressure Rating (High Pressure (Above 12 bar), Medium Pressure (5-12 bar), and Low Pressure (Below 5 bar)), By Diameter (Medium Diameter (200-600 mm), Small Diameter (Below 200 mm), and Large Diameter (Above 600 mm)) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | JM Eagle, Inc., Aliaxis Group S.A., Sekisui Chemical Co., Ltd., Georg Fischer Ltd., Chevron Phillips Chemical Company, Westlake Pipe & Fittings, China Lesso Group Holdings Ltd., Finolex Industries Ltd., Astral Poly Technik Limited, Prince Pipes and Fittings Ltd., Supreme Industries Ltd., Uponor Corporation, Rehau Group, Wavin N.V., Pipelife International GmbH, Charlotte Pipe and Foundry Company, ATC Plastics, LLC, Plastika Kritis S.A., Future Pipe Industries, AMIBLU (Amiblu Holding GmbH) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |