Quick Navigation

Report Overview

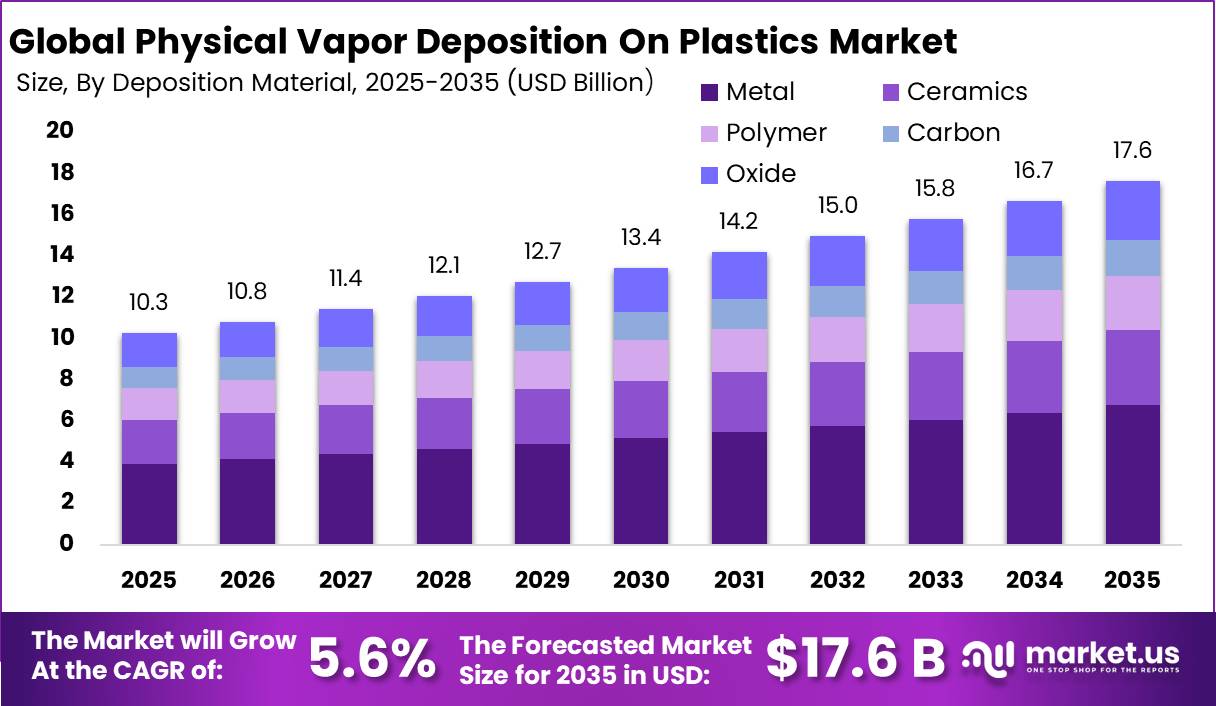

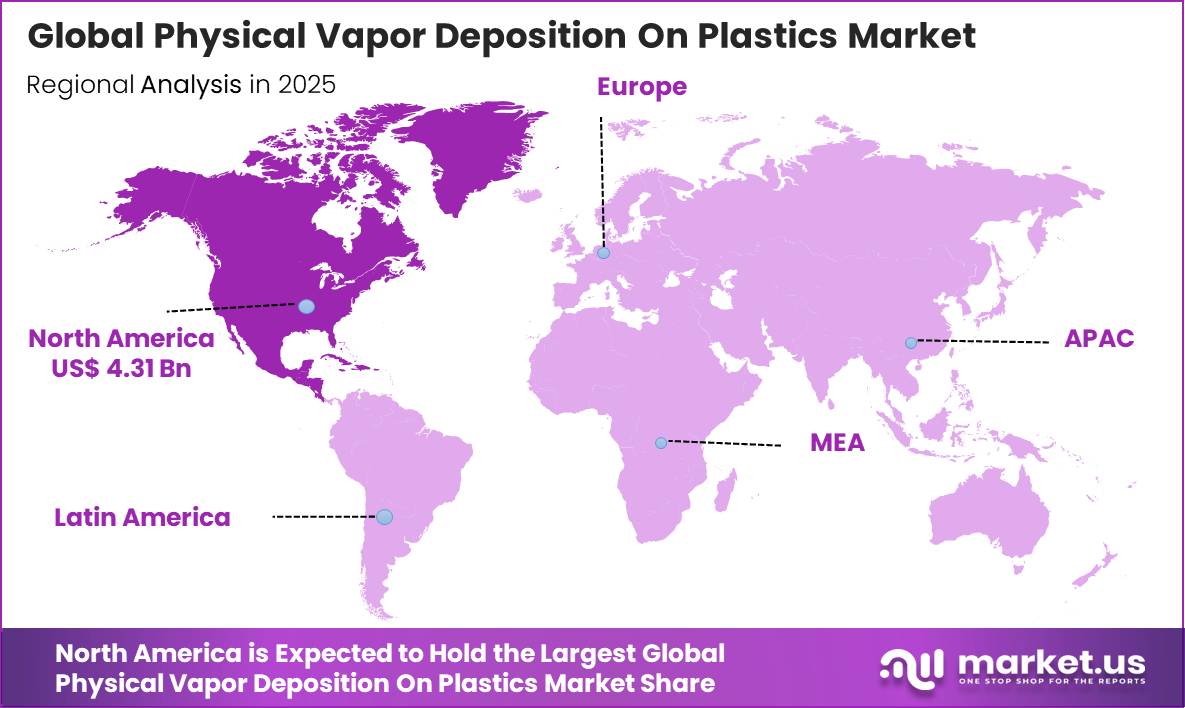

The Global Physical Vapor Deposition on Plastics Market size is expected to be worth around USD 17.8 Billion by 2035, from USD 10.3 Billion in 2025, growing at a CAGR of 5.6% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 41.8% share, holding USD 4.1 Billion revenue.

The global physical vapor deposition (PVD) on plastics market is evolving as an important segment within advanced surface engineering and thin-film coating technologies, supported by rising demand for lightweight, high-performance, and aesthetically enhanced polymer components across electronics, automotive, healthcare, and consumer appliance industries. PVD processes enable the deposition of metallic, ceramic, oxide, polymer, and carbon-based coatings on plastic substrates while maintaining low weight and design flexibility.

Increasing adoption of flexible electronics, wearable devices, smart displays, and metallized automotive interiors is accelerating the use of coated polymers such as polyimide, polyethylene terephthalate, and polyethylene naphthalene. Manufacturing advancements in sputtering, evaporation, and roll-to-roll deposition are improving coating uniformity, throughput efficiency, and compatibility with heat-sensitive substrates.

Regulatory pressure to reduce hazardous electroplating chemicals and improve sustainability performance is also encouraging the transition toward vacuum-based coating technologies. At the same time, the industry continues addressing technical limitations related to coating adhesion, thermal stability, and multilayer film durability on flexible plastic materials used in demanding operating environments.

Key Takeaways

- The global physical vapor deposition on plastics market was valued at US$10.3 billion in 2025.

- The global physical vapor deposition on plastics market is projected to grow at a CAGR of 5.6% and is estimated to reach US$17.8 billion by 2035.

- On the basis of deposition material, metals dominated the market, constituting 38.4% of the total market share.

- Based on the deposition technique, sputtering dominated the physical vapor deposition on plastics market, with a substantial market share of around 39.5%.

- Based on the substrates, physical vapor deposition on polyethylene terephthalate led the market, comprising 37.3% of the total market.

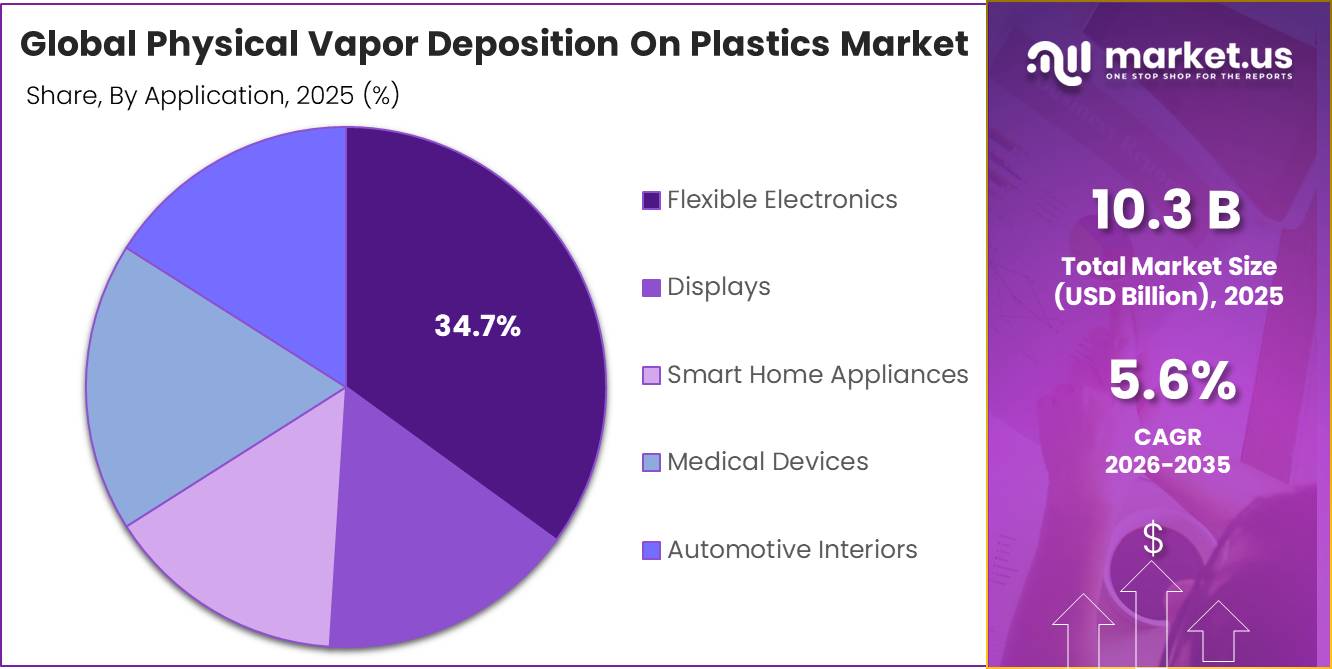

- Among the applications, flexible electronics held a major share in the physical vapor deposition on plastics market, 34.7% of the market share.

- Among the manufacturing processes, roll-to-roll is the most considerable within the market, accounting for around 59.1% of the revenue.

- In 2025, North America was the most dominant region in the physical vapor deposition on plastics market, accounting for 41.8% of the total global consumption.

Deposition Material Analysis

Metals are a Prominent Segment in the Market.

Metal-based deposition materials account for the dominant share in the physical vapor deposition on plastics market, accounting for approximately 38.4% share, reflecting their extensive use in achieving functional and aesthetic surface enhancements. Metallic coatings such as aluminum, chromium, titanium, and gold are widely employed due to their superior reflectivity, electrical conductivity, and ability to replicate premium metallic finishes on lightweight polymer substrates. These characteristics make them particularly suitable for automotive interior trims, consumer electronics housings, and smart appliance components where durability and visual appeal are critical.

Metal films deposited through sputtering and evaporation processes further provide effective electromagnetic interference shielding, supporting increasing integration in electronic devices. Their compatibility with roll-to-roll and batch processing systems further strengthens large-scale manufacturability. Additionally, continuous improvements in thin-film adhesion techniques are enhancing coating stability on heat-sensitive plastics, reinforcing the sustained preference for metal-based deposition materials across high-performance industrial applications.

Deposition Technique Analysis

Sputtering Technique Dominated the Physical Vapor Deposition on Plastics Market.

Sputtering holds the dominant position in the physical vapor deposition (PVD) on plastics market with a share of approximately 39.5%, supported by its high versatility, process stability, and strong compatibility with heat-sensitive polymer substrates. The technique enables precise control over film thickness, composition, and uniformity, making it suitable for large-area coating applications in flexible electronics, automotive interiors, and consumer device housings.

Its ability to deposit a wide range of materials, including metals, oxides, and ceramics, enhances its applicability across both functional and decorative use cases. Magnetron sputtering variants further improve deposition efficiency and coating adhesion on plastics such as PET, polyimide, and polycarbonate. Additionally, the scalability of sputtering in roll-to-roll and batch processing systems supports high-throughput manufacturing requirements, reinforcing its widespread adoption in industrial thin-film coating environments.

Substrates Analysis

Polyethylene Terephthalate is the Most Widely Utilized Substrate.

Polyethylene terephthalate (PET) accounts for approximately 37.3% share in the physical vapor deposition on plastics market, positioning it as the dominant substrate type. Its widespread adoption is supported by a balanced combination of mechanical strength, dimensional stability, transparency, and cost efficiency, making it suitable for high-volume coating applications. PET’s relatively low processing temperature allows compatibility with physical vapor deposition techniques such as sputtering and evaporation, enabling uniform deposition of metallic, oxide, and carbon-based thin films without significant substrate deformation.

It is extensively used in flexible electronics, display films, automotive interior components, and smart appliance surfaces where both functional and decorative properties are required. Additionally, PET’s ease of processing in roll-to-roll manufacturing systems enhances its scalability for industrial production, reinforcing its strong presence across multiple end-use sectors requiring lightweight and high-performance coated plastic materials.

Manufacturing Process Analysis

Roll-to-Roll Process Held a Major Share of the Physical Vapor Deposition on Plastics Market.

Roll-to-Roll (R2R) processing dominates the manufacturing landscape in the physical vapor deposition on plastics market with a share of approximately 59.1%, driven by its ability to enable continuous, high-throughput coating of flexible polymer substrates. This process is particularly suited for large-area materials such as polyethylene terephthalate (PET), polyimide, and polyethylene naphthalate films used in electronics, displays, and functional packaging applications.

R2R systems allow sequential deposition of thin films under vacuum conditions while maintaining consistent film thickness and uniformity across long substrate lengths, improving production efficiency and material utilization. Its compatibility with sputtering and evaporation techniques further enhances its industrial relevance. The method supports cost-efficient scaling for mass production of metallized films used in flexible electronics, automotive interiors, and smart surface applications, reinforcing its position as the preferred manufacturing approach for high-volume PVD coating operations on plastics.

Application Analysis

Physical Vapor Deposition on Plastics is Mostly Utilized for Flexible Electronics.

Flexible electronics accounts for approximately 34.7% share in the physical vapor deposition (PVD) on plastics market, making it the leading application segment. This dominance is driven by the increasing integration of lightweight, bendable, and miniaturized electronic systems across consumer and industrial devices. PVD-coated polymer substrates such as polyimide, polyethylene terephthalate, and polyethylene naphthalate are widely used to form conductive layers, barrier coatings, and reflective surfaces essential for flexible circuits, sensors, and wearable devices.

The ability of thin-film deposition to maintain electrical performance under repeated mechanical bending enhances its suitability for next-generation electronic architectures. Sputtered metal and oxide coatings are particularly important for enabling conductivity and environmental protection without compromising flexibility. Growing adoption of foldable displays, wearable health monitors, and smart textiles further strengthens demand, reinforcing flexible electronics as the most influential application area for PVD technologies on plastic substrates.

Key Market Segments

By Deposition Material

- Metal

- Ceramics

- Polymer

- Carbon

- Oxide

By Deposition Technique

- Sputtering

- Evaporation

- Molecular Beam Epitaxy

- Atomic Layer Deposition

By Substrates

- Polyimide

- Polyethylene Terephthalate

- Polyethylene Naphthalene

- Polyethylene and Polystyrene

By Manufacturing Process

- Roll-to-Roll

- Batch and Cluster Deposition

By Application

- Flexible Electronics

- Displays

- Smart Home Appliances

- Medical Devices

- Automotive Interiors

- Others

Drivers

Rising Adoption of Lightweight Metallized Components in Automotive and Electronics Manufacturing.

Growing substitution of metal parts with lightweight polymer components in vehicles and electronic devices is strengthening demand for physical vapor deposition (PVD) coatings on plastics. The U.S. Department of Energy states that a 10% reduction in vehicle weight can improve fuel economy by 6-8%, while replacing conventional steel structures with lightweight materials and polymer composites can reduce body and chassis weight by up to 50%.

This has accelerated the use of coated plastic trims, control panels, and electronic housings that combine low weight with metallic appearance and functional surface properties. Regulatory pressure is further influencing material selection. The European Union’s End-of-Life Vehicles Directive restricts hazardous substances, including hexavalent chromium, in vehicle manufacturing and requires vehicles to achieve 85% recyclability and 95% recoverability by weight.

These requirements are encouraging manufacturers to shift from conventional electroplating toward vacuum-based coating technologies with lower environmental impact. In electronics manufacturing, metallized polymer substrates are increasingly utilized in lightweight sensors, flexible circuits, and smart interfaces where conductive and decorative thin films are required without adding structural mass.

Restraints

Adhesion and Thermal Stability Challenges on Heat-Sensitive Plastic Substrates.

Adhesion instability and thermal sensitivity of polymer substrates remain critical technical constraints for physical vapor deposition (PVD) on plastics. Thin-film systems experience mechanical stress when deposited coatings and polymer substrates exhibit different coefficients of thermal expansion (CTE). The U.S. National Institute of Standards and Technology reported that thermal expansion behavior in supported polymer thin films varies significantly depending on substrate confinement and film thickness, affecting coating reliability under thermal cycling.

The CTE mismatch between adjacent thin-film layers can lead to interfacial delamination and cracking, particularly in constrained multilayer systems. Heat-sensitive plastics such as polyethylene terephthalate (PET) and polystyrene are especially vulnerable because many vacuum deposition processes involve elevated substrate temperatures or energetic plasma exposure.

NIST further identified thermal expansion as a key reliability parameter for thin polymer films used in electronic packaging and advanced coatings. These material limitations increase dependence on surface pretreatment, low-temperature deposition methods, and multilayer adhesion engineering, thereby adding process complexity and reducing throughput efficiency in large-scale manufacturing environments.

Opportunity

Emerging Demand for Flexible Electronics and Wearable Device Manufacturing.

Emerging deployment of flexible electronics and wearable devices is creating measurable demand for physical vapor deposition (PVD) technologies on polymer substrates. The U.S. National Institute of Standards and Technology (NIST) documented the use of thin-film gold electrodes deposited on porous polyethylene terephthalate (PET) substrates for flexible electronic and wearable sensor applications, demonstrating the growing relevance of conductive thin films on plastics in next-generation device architectures.

Flexible electronics research has increasingly focused on polymer substrates such as polyimide (PI), PET, and polyethylene naphthalene (PEN) because of their low weight, bendability, and compatibility with roll-to-roll processing. The studies published in npj Flexible Electronics reported more than 11,000 article accesses and 60 citations for wearable bioelectronics research involving skin-compatible flexible devices, indicating substantial research and industrial attention toward wearable systems.

In addition, flexible substrate technologies are supporting applications in foldable smartphones, rollable displays, medical sensors, and electronic skins, where vacuum-deposited metallic and oxide coatings are required for conductivity, barrier protection, and optical functionality.

Trends

Expansion of Functional Thin-Film Coatings Beyond Decorative Applications.

Functional thin-film coatings on plastic substrates are increasingly being deployed for electromagnetic shielding, optical management, dielectric performance, and surface protection rather than solely decorative finishes. The International Organization for Standardization published ISO 7582:2023, establishing characterization methods for metallic coatings used for electromagnetic interference (EMI) shielding on plastics, ceramics, and glass substrates, reflecting growing industrial standardization of functional coated surfaces.

Research published through the U.S. National Institute of Standards and Technology (NIST) identified conductive coatings on plastics as critical for shielding effectiveness in electronic systems, with thin metallic layers enabling electromagnetic protection without substantially increasing component thickness or weight. Additional studies on multilayer metallic thin films deposited on polypropylene (PP) and polycarbonate (PC) substrates demonstrated that shielding performance depends on conductivity ratios and layer sequencing, highlighting the transition toward engineered multifunctional coating architectures.

Functional optical coatings are also expanding on polymer substrates. Published optical materials research showed that multilayer anti-reflective coatings on plastics can reduce surface reflectance to below 0.5% across the visible spectrum, supporting applications in displays, optical sensors, and electronic interfaces.

Geopolitical Impact Analysis

Geopolitical Supply Chain Realignment and Trade Restrictions Reshaping PVD on Plastics Manufacturing Ecosystems.

Current geopolitical tensions are influencing the physical vapor deposition (PVD) on plastics market through disruptions in critical raw material supply chains, semiconductor equipment trade restrictions, and increasing localization of advanced manufacturing systems. PVD coatings rely on metals and specialty materials, including palladium, platinum-group elements, titanium, and rare earth derivatives used in sputtering targets and thin-film applications. The European Union’s Critical Raw Materials Act, adopted in 2024, identified high supply disruption risks associated with concentrated sourcing of strategic minerals and emphasized the need to diversify imports and strengthen recycling capacity. Russia’s role in palladium and platinum-group metal supply has also created procurement uncertainty. Reuters reported that Russian platinum supply was expected to decline by 9% in 2024 amid sanctions and operational constraints, contributing to tighter global availability.

Trade controls on semiconductor manufacturing technologies are additionally affecting deposition equipment ecosystems. The U.S. Department of Commerce expanded export controls in 2024, covering advanced semiconductor manufacturing items and related technologies, including equipment categories associated with thin-film processing systems. These restrictions are accelerating regional supply-chain restructuring across electronics and display manufacturing industries that utilize vacuum coating technologies on polymer substrates. Concurrently, European industrial authorities have highlighted strategic dependence on imported critical minerals, with some materials sourced predominantly from China and Russia, reinforcing investment in domestic processing and alternative material sourcing strategies.

Regional Analysis

North America Held the Largest Share of the Global Physical Vapor Deposition on Plastics Market.

In 2025, North America dominated the global physical vapor deposition on plastics market, holding about 41.8% of the total global consumption, due to its concentration of advanced electronics manufacturing, automotive lightweighting initiatives, and high-value thin-film research infrastructure. The U.S. National Institute of Standards and Technology (NIST) identified the United States as one of the world’s major manufacturing economies, with advanced manufacturing capabilities spanning electronics, precision engineering, and materials processing. The region’s strong, flexible electronics ecosystem also supports the adoption of vacuum-deposited coatings on polymer substrates. The U.S. National Academies reported that flexible electronics applications in medical devices, packaging, consumer electronics, lighting, and alternative energy depend heavily on advanced manufacturing technologies and thin-film processing systems.

North America additionally benefits from a substantial semiconductor and electronics manufacturing base utilizing thin-film deposition processes. According to the U.S. Environmental Protection Agency (EPA), 46 electronics manufacturing facilities in the United States reported greenhouse gas emissions associated with semiconductor and thin-film manufacturing operations in 2023. Automotive demand further reinforces regional dominance as manufacturers increasingly deploy metallized plastic components to reduce vehicle weight while maintaining durability and decorative performance in interior and electronic assemblies.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers in the physical vapor deposition (PVD) on plastics space concentrate on strengthening process innovation and equipment efficiency to differentiate their offerings. A key focus is advancing low-temperature deposition technologies such as enhanced sputtering and plasma-assisted evaporation to improve coating adhesion on heat-sensitive polymers like PET and polyimide. Firms also invest in roll-to-roll and inline coating systems to enable high-throughput, cost-efficient production for flexible electronics and display applications.

Material engineering efforts target multifunctional thin films that combine conductivity, optical control, and barrier properties in a single coating layer. Strategic collaborations with electronics, automotive, and medical device manufacturers help tailor application-specific solutions. Additionally, companies emphasize sustainability by reducing hazardous chemical usage and improving vacuum process energy efficiency. Expansion of localized manufacturing and after-sales service networks further supports customer retention and strengthens long-term industrial integration across key end-use sectors.

The Major Players in The Industry

- Applied Materials Inc.

- Veeco Instruments Inc.

- IHI Corporation

- OC Oerlikon Management AG

- Kurt J Lesker Company

- Leybold GmbH

- Plasma Therm LLC

- Singulus Technologies AG

- Plansee SE

- AJA International Inc.

- Other Key Players

Key Development

- In April 2024, SINGULUS TECHNOLOGIES announced the launch of its new PVD sputtering systems designed for fuel cell components and Proton Exchange Membrane (PEM) electrolyzers, expanding its portfolio in advanced vacuum coating technologies.

- In September 2023, Plasma-Therm announced the acquisition of Thin Film Equipment SrL (TFE), effective September 18, 2023. Based in Binasco, Italy, TFE specializes in sputtering and evaporation equipment for semiconductor research and production, along with high-purity materials used in physical vapor deposition thin-film applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$10.3 Bn |

| Forecast Revenue (2035) | US$17.8 Bn |

| CAGR (2026-2035) | 5.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Deposition Material (Metal, Ceramics, Polymer, Carbon, and Oxide), By Deposition Technique (Sputtering, Evaporation, Molecular Beam Epitaxy, and Atomic Layer Deposition), By Substrates (Polyimide, Polyethylene Terephthalate, Polyethylene Naphthalene, and Polyethylene & Polystyrene), By Manufacturing Process (Roll-to-Roll and Batch & Cluster Deposition), By Application (Flexible Electronics, Displays, Smart Home Appliances, Medical Devices, Automotive Interiors, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Applied Materials Inc., Veeco Instruments Inc., IHI Corporation, OC Oerlikon Management AG, Kurt J Lesker Company, Leybold GmbH, Plasma Therm LLC, Singulus Technologies AG, Plansee SE, AJA International Inc., and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |