Quick Navigation

Report Overview

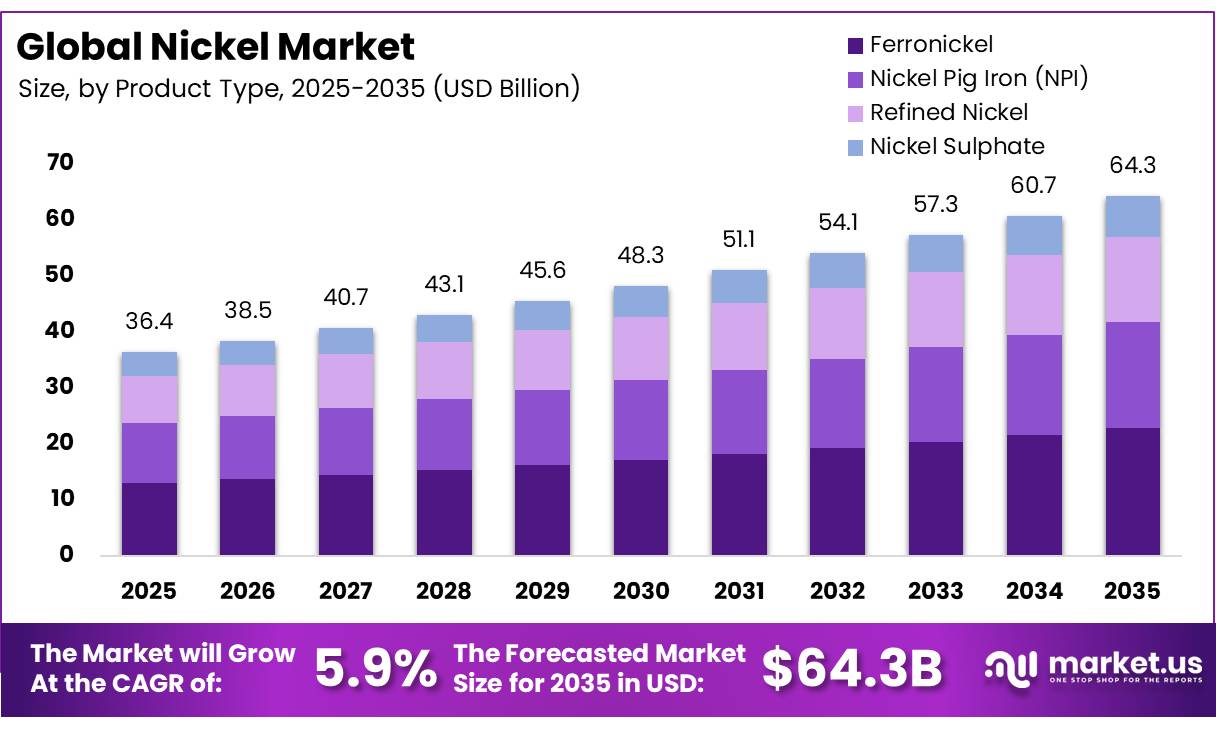

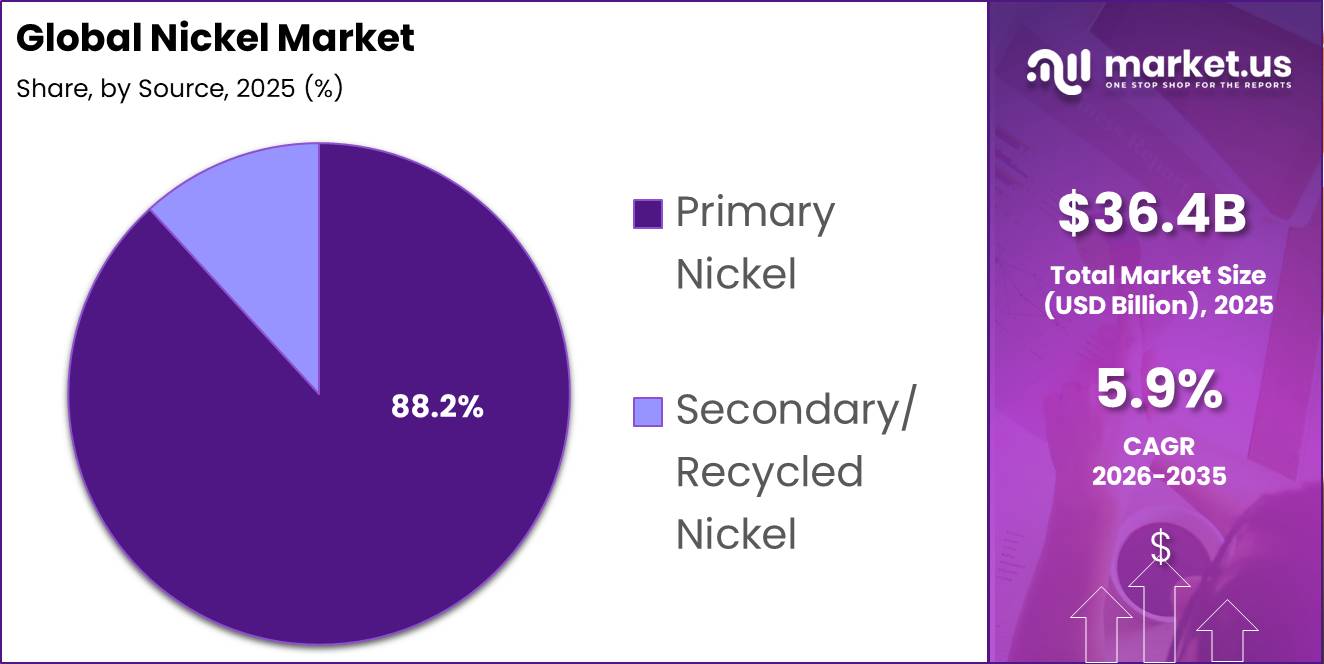

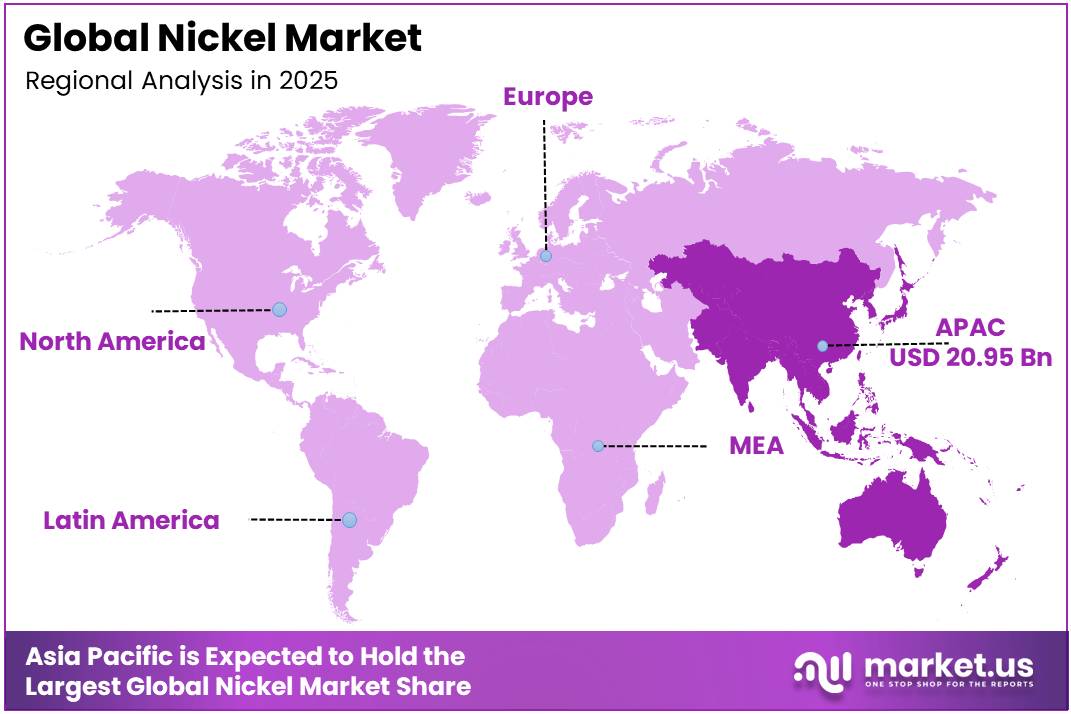

In 2025, the Global Nickel Market was valued at USD 36.4 billion. Between 2026 and 2035, this market is estimated to register a CAGR of 5.9%, reaching approximately USD 64.3 billion by 2035. In 2025, Asia Pacific led the market, achieving over 57.6% share with a revenue of USD 20.95 billion.

The Nickel market is a global metals and mining sector encompassing the production, refining, and trading of nickel a silvery-white metal with exceptional corrosion resistance, hardness, and thermal conductivity supplied to stainless steel producers, battery manufacturers, alloy fabricators, and electroplating operations worldwide.

- According to the U.S. Geological Survey’s February 2026 assessment, global nickel mine production reached an estimated 9 million metric tons in 2025, increasing by 5% from approximately 3.71 million metric tons in 2024. The increase was mainly supported by expanding operations in Indonesia and improved production conditions in Canada and New Caledonia.

Key Takeaways

- The Global Nickel Market was valued at USD 36.4 billion in 2025.

- The market is projected to grow at a CAGR of 5.9% and is estimated to reach USD 64.3 billion by 2035.

- Ferronickel is the dominant product type, accounting for 35.6% of the market in 2025, driven by its primary role in stainless steel production across Asian markets.

- Class II Nickel is the dominant class segment at 68.4%, reflecting the large-scale production of Ferronickel and Nickel Pig Iron both Class II products predominantly in Indonesia and China.

- Industrial Grade Nickel leads the grade segment at 81.3%, anchored by stainless steel and alloy manufacturing’s dominant share of global nickel consumption.

- Primary Nickel leads the source segment at 88.2%, reflecting the continued dominance of mined nickel supply over recycled alternatives in meeting global industrial demand.

- Stainless Steel Production is the dominant application at 63.8%, confirming nickel’s structural role as the essential alloying element in stainless steel manufacturing.

- Asia Pacific holds the largest regional share at 57.6%, driven by China’s dominant stainless steel production base and Indonesia’s world-leading nickel mining output.

Nickel is mined primarily from laterite and sulphide ore deposits. Indonesia is confirmed as the world’s dominant producer, accounting for more than half of global mined nickel production by IEA, 2024.

- In 2025, the Eagle Mine in Michigan produced approximately 10,000 tons of nickel in concentrate the only active U.S. nickel mine confirming North America’s continued dependence on imported primary nickel by USGS, 2026.

The primary driver expanding this industry is the surging demand for energy storage and industrial metals. For instance, electric vehicle battery manufacturing puts massive pressure on high-purity supply chains. Government clean energy mandates and infrastructure investments act as highly influential regulatory drivers. Conversely, structural market surpluses and stringent environmental compliance rules represent the primary market restraints.

The market scope segments by technology into High-Pressure Acid Leaching (HPAL) for laterite ores and advanced pyrometallurgical smelting for sulfide concentrates. The future outlook relies on integrating AI into industrial processing networks. Machine learning algorithms optimize furnace thermal efficiency, monitor structural emissions, and manage automated mining machinery. AI-powered mineral processing optimisation and predictive maintenance platforms are being deployed across nickel smelting and refining operations, improving energy efficiency and recovery rates.

Nickel Market Segmentation

By Product Type

Ferronickel Represents the Dominant Segment in the Market

In 2025, Ferronickel accounted for a leading 35.6% share of the Nickel market by product type, due to its direct use as an intermediate product in stainless steel production where its iron-nickel alloy composition is directly charged into electric arc furnaces without the additional refining step required for pure nickel metal. Ferronickel production is dominated by Indonesia and China, where large-scale rotary kiln electric furnace processing of laterite ores produces Ferronickel at lower cost than comparable Class I nickel products.

Nickel Sulphate, is the fastest-growing product type across the forecast period. Demand for nickel increased in 2024, driven substantially by battery applications in electric vehicles and energy storage by IEA. Electric vehicle sales growth, nickel sulphate conversion economics relative to Class I metal pricing, and EV battery cathode manufacturer procurement strategies are the primary growth determinants for the Nickel Sulphate segment.

By Class

Class II Nickel Represents the Dominant Segment in the Market

In 2025, Class II Nickel accounted for a leading 68.4% share of the Nickel market by class, due to the dominant production volumes of Ferronickel and Nickel Pig Iron both Class II products with nickel purity below 99% which serve the stainless steel industry’s demand for cost-competitive nickel units. Class II nickel production is concentrated in Indonesia and China, where laterite ore processing routes produce Ferronickel and NPI at lower cost than sulphide ore-based Class I refining.

Class I Nickel is the fastest-growing class segment. Battery-grade nickel sulphate derived from Class I nickel products is required for NMC lithium-ion battery cathode precursor manufacturing, creating a growing premium demand segment for high-purity Class I nickel. Between 2026 and 2035, rising electric vehicle penetration is expected to drive Class I nickel demand growth at above-market rates as battery manufacturers require consistent, high-purity nickel sulphate inputs.

By Grade

Industrial Grade Nickel Represents the Dominant Segment in the Market

In 2025, Industrial Grade Nickel accounted for a leading 81.3% share of the Nickel market by grade, due to stainless steel and alloy manufacturing’s dominant consumption of global nickel supply. Industrial Grade Nickel encompasses the full range of Ferronickel, NPI, and standard refined nickel products used in stainless steel, alloy, electroplating, and foundry applications.

- The U.S. Geological Survey reported in February 2026 that stainless steel, alloy steel, and other nickel-containing alloys generally represented more than 85% of U.S. nickel consumption in 2025.

Battery Grade Nickel is the fastest-growing grade segment across the forecast period. High-purity nickel sulphate meeting battery cathode precursor specifications commands a premium above standard industrial-grade nickel pricing reflecting its critical role in the electric vehicle battery supply chain.

By Source

Primary Nickel Represents the Dominant Segment in the Market.

In 2025, Primary Nickel accounted for a leading 88.2% share of the Nickel market by source, due to the continued dominance of mined nickel production in meeting global industrial and battery demand. Primary nickel is sourced from laterite and sulphide ore deposits with Indonesia, Philippines, Russia, Australia, and Canada representing the major producing nations.

- According to the International Nickel Study Group (INSG) in April 2025, global primary nickel usage is forecast to grow by 3% in 2025 and a further 6.2% in 2026, driven by rising demand from stainless steel, electric vehicle (EV) batteries, and other industrial applications.

Secondary/Recycled Nickel is the fastest-growing source segment. In 2025, nickel recovered from scrap accounted for approximately 60% of apparent U.S. consumption a significant proportion reflecting the maturity of nickel recycling infrastructure in North American stainless steel production by USGS, 2026. Between 2026 and 2035, rising stainless steel scrap availability, EV battery end-of-life recycling infrastructure development, and critical mineral supply chain security policy are expected to drive Secondary/Recycled Nickel’s share expansion globally.

By Application

Stainless Steel Production Represents the Dominant Application in the Market

In 2025, Stainless Steel Production accounted for a leading 63.8% share of the Nickel market by application, due to nickel’s indispensable role as an alloying element that provides corrosion resistance, ductility, and high-temperature performance to austenitic stainless steel grades the most widely produced stainless steel family globally.

- According to the World Stainless Association, global stainless steel melt shop production reached approximately 6 million metric tons in 2024, reflecting continued strong demand for nickel-bearing stainless steel grades that rely heavily on ferronickel as a cost-effective raw material.

Batteries is the fastest-growing application segment across the forecast period. Electric vehicles consolidated their position as the largest consuming segment, increasing their share considerably in the demand for nickel, with the energy sector accounting for 85% of total demand growth for battery metals between 2022 and 2024 by IEA, 2025.

Key Market Segments

By Product Type

- Refined Nickel

- Nickel Sulphate

- Ferronickel

- Nickel Pig Iron (NPI)

By Class

- Class I Nickel

- Class II Nickel

By Grade

- Battery Grade Nickel

- Industrial Grade Nickel

By Source

- Primary Nickel

- Secondary/Recycled Nickel

By Application

- Stainless Steel Production

- Batteries

- Alloy Manufacturing

- Electroplating

- Foundry & Casting

- Chemical Industry

- Aerospace Components

- Electronics & Electrical

- Catalysts

- Coinage

- Others

Driver Analysis

Battery-grade nickel sulphate and EV value-chain localization

Battery-linked nickel remains the most strategically important demand vector even though it is not yet the largest one by tonnage. The IEA reported that demand for nickel, cobalt, graphite, and rare earths grew by 6–8% in 2024, and under its medium-term clean-energy scenarios nickel demand is expected to roughly double by 2040, indicating that battery-linked pull remains structurally intact despite short-cycle EV volatility. In parallel, INSG notes that although battery-sector nickel softened in 2025, it is expected to regain momentum in 2026, and Indonesia itself is beginning to use nickel for EV battery production from 2025 onward as part of a broader domestic battery industry build-out.

Once producers shift from ferronickel/NPI exposure into sulphate, matte conversion, and precursor integration, business models migrate from commodity spread capture toward longer-term offtake structures, qualification-driven sales, and carbon-accounted supply agreements. The resulting revenue pool grows faster than flat LME-linked metal because battery-grade material embeds extra processing margins, traceability requirements, and customer lock-in, especially in China and Indonesia, while Europe and parts of North America remain selective demand centers for high-purity feed.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Indonesia downstream build-out and ore-policy control | +2.1% | Indonesia core, China refining link, APAC export corridors, global spill-over | Short term (≤ 2 years) |

| Battery-grade nickel sulphate and EV value-chain localization | +1.4% | China core, Indonesia, EU battery chain, North America selective | Medium term (2-4 years) |

| Stainless steel base-load demand resilience | +1.2% | China core, Indonesia, India, EU recovery pockets, MENA spill-over | Short term (≤ 2 years) |

| EU battery traceability and carbon-compliance regime | +0.8% | EU core, Asian exporters to Europe, global premium-material suppliers | Medium term (2-4 years) |

| Class I tightness amid Class II surplus segmentation | +1.0% | LME-linked markets, North America, EU alloy users, battery precursor hubs in Asia | Short term (≤ 2 years) |

| Supply rationalization outside Asia and higher cost floor | +0.9% | Australia, New Caledonia, Canada, EU refining assets, global benchmark pricing | Medium term (2-4 years) |

Restraint Analysis

EU compliance burden

This converts ESG from a reputational issue into a market-access cost center: importers and cathode producers must fund auditable chain-of-custody systems, third-party assurance preparation, supplier remediation programs, and documentation architectures before the 18 February 2027 battery passport phase and before later recycled-content thresholds that include 6% nickel from 18 August 2031 and 15% from 18 August 2036.

For the nickel market, the effect is not demand destruction in absolute tonnes but frictional deceleration longer supplier onboarding, higher compliance SG&A, more conservative sourcing from Indonesian and other high-scrutiny nodes, and a higher risk discount on non-transparent feedstock streams which slows conversion of nominal battery demand into bankable nickel sales growth.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural oversupply | -2.4% | Global; APAC core; EU; NA | Medium term (2-4 years) |

| Indonesia policy volatility | -1.6% | Indonesia core; China; EU buyers | Short term (≤ 2 years) |

| LFP substitution | -1.9% | China core; EU EV chain; US | Medium term (2-4 years) |

| EU compliance burden | -1.1% | EU core; Indonesia-to-EU flows | Short term (≤ 2 years) |

| Weak stainless cycle | -1.4% | China; EU industrial base; NA | Short term (≤ 2 years) |

| Ex-Indonesia cost squeeze | -1.7% | Australia; New Caledonia; Canada | Long term (≥ 4 years) |

Opportunity Analysis

Specialty alloys for hydrogen and energy systems

This is future upside rather than a baseline driver because most published nickel market growth still emphasizes stainless steel and EV batteries, while adjacent demand from hydrogen, advanced energy infrastructure, and corrosion-resistant nickel alloys remains underpenetrated and commercially fragmented; the Energy Transitions Commission identifies additional nickel demand from hydrogen electrolysers and wind applications, including about 20,000 tonnes linked to hydrogen electrolysers and 4,000 tonnes to wind, and broader energy-system deployments increasingly rely on nickel-bearing materials in harsh operating conditions.

The opportunity is for producers and alloy makers to shift part of their portfolio into engineered, specification-heavy products where average selling prices can be 1.5x to 3.0x those of commodity units and customer retention is materially higher, so even if these end uses remain modest in tonnage through 2030, capturing them can still add about 1.3 percentage points to growth through mix improvement, 400 to 700 basis points of gross-margin uplift, and lower earnings cyclicality relative to pure exposure to LME-linked commodity markets.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Battery-grade sulphate integration | +2.4% | Indonesia, China, South Korea, EU, North America | Short term (≤ 2 years) |

| Black mass recycling scale-up | +1.9% | EU, North America, India, China | Medium term (2-4 years) |

| Low-carbon nickel premium pools | +1.6% | EU, North America, Japan, South Korea | Medium term (2-4 years) |

| Specialty alloys for hydrogen and energy systems | +1.3% | EU, North America, Japan, GCC | Medium term (2-4 years) |

| Ex-China regional refining hubs | +1.8% | North America, EU, India, Australia | Short term (≤ 2 years) |

| M&A roll-up of distressed class 1 assets | +1.5% | Australia, Canada, New Caledonia, Africa | Long term (≥ 4 years) |

Challenges Analysis

Ore Quota Volatility

Indonesia’s 2026 shift back to annual RKAB approvals and the reduction of nickel ore permits to roughly 250–270 million wet tons from 379 million in 2025 has not removed supply from the market in an absolute sense, but it has materially increased planning uncertainty across miners, NPI smelters, matte converters, and battery-feed producers that had built operating schedules around more elastic ore availability.

The friction arises through stop-start mine sequencing, shorter ore-stock cover, opportunistic domestic contract repricing, and underutilization of installed smelting capacity because industry ore demand estimates of 340–350 million tons now sit above approved supply bands, creating a practical feed gap that can translate into utilization losses of 10–20 percentage points at marginal plants and higher working-capital intensity across the chain. Strategically, producers must adapt by lengthening ore inventory buffers from roughly 3–4 weeks toward 6–8 weeks, increasing mine-smelter integration, diversifying Philippine blending options where chemistry allows, and shifting from volume-maximization to yield-maximization operating models, which collectively slows the market’s realizable growth trajectory by about 1.4 percentage points even while end-market demand remains intact.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Ore Quota Volatility | -1.4% | Indonesia core, China-linked smelting, APAC stainless chain | Medium term (2-4 years) |

| Sulfur Feedstock Tightness | -1.1% | Indonesia HPAL hubs, Middle East shipping routes, Asian battery chain | Short term (≤ 2 years) |

| Class I/II Product Mismatch | -0.9% | LME-linked markets, EU battery chain, Northeast Asia refining | Medium term (2-4 years) |

| HPAL Execution Bottlenecks | -1.2% | Indonesia, PNG, Australia, North America project pipeline | Long term (≥ 4 years) |

| Technical Talent Deficit | -0.8% | Indonesia parks, Australia, Canada, EU processing clusters | Long term (≥ 4 years) |

| Traceability Cost Escalation | -0.7% | EU regulatory hubs, North America OEM chains, premium alloy buyers | Medium term (2-4 years) |

Geopolitical Impact Analysis

Russia-Ukraine Conflict and U.S.-China Trade Tensions Are Disrupting Global Nickel Supply Chains and Price Discovery

Russia is one of the world’s largest producers of Class I nickel and its supply has been under Western sanctions pressure since the invasion of Ukraine in February 2022. The USGS Mineral Commodity Summaries confirmed that concerns about continued availability of Class I nickel from Russia following the Ukraine conflict directly influenced nickel price movements and prompted Western buyers to accelerate supply chain diversification by USGS, 2024. Russian nickel imports into the United States declined as import source diversification toward Canada, Norway, Australia, and Brazil accelerated across 2022–2024 by USGS, 2026.

U.S. China trade tensions add a second layer of disruption. Tariff escalation and critical mineral trade restrictions directly affect the economics of nickel flowing through Chinese-owned supply chains into Western battery manufacturers. Rio Tinto and Glencore’s preliminary merger discussions in January 2026 before Rio Tinto confirmed it would not proceed in February 2026 reflected the strategic consolidation instinct triggered by exactly this geopolitical and supply chain pressure by SEC in January 2026.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Nickel Market

In 2025, Asia Pacific dominated the global Nickel market, holding about 57.6% of total global consumption at US$20.95 billion. This dominance is structural rooted in China’s position as the world’s largest stainless steel producer and Indonesia’s position as the world’s largest nickel producer. China’s stainless steel industry consumes the majority of global Ferronickel and NPI output both of which are predominantly produced in Indonesia and China itself creating a deeply integrated regional nickel supply and demand chain that anchors Asia Pacific’s market leadership.

- Global nickel reserves exceeded 140 million metric tons in 2025, including approximately 62 million metric tons in Indonesia, 16 million metric tons in Brazil, 8.3 million metric tons in Russia, and 7.1 million metric tons in New Caledonia.

Europe represents the second-largest regional market supported by significant stainless steel production in Germany, Finland, Sweden, and the United Kingdom, and growing battery cathode precursor manufacturing investment aligned with the EU Critical Raw Materials Act and EU Battery Regulation frameworks. North America holds a meaningful market share anchored by U.S. stainless steel and alloy manufacturing, Canadian nickel mining output, and growing EV battery supply chain investment.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Global Nickel Market operates under a consolidated oligopolistic structure at the mining and primary production level, with a small number of large multinational mining companies and state-linked enterprises controlling the majority of global nickel mine output and refining capacity. Vale S.A., Norilsk Nickel, Glencore, BHP, Anglo American, Rio Tinto, Eramet, and South32 collectively represent the dominant tier of globally significant nickel producers, each with large-scale integrated mining, processing, and refining operations across multiple geographies.

Sumitomo Metal Mining Co., Ltd. is one of the world’s leading nickel producers, In FY2025, it reported revenue of approximately USD 10.5 billion and maintained nickel production of around 65,000 metric tons. Sherritt International Corporation is a Canadian mining and refining company specializing in nickel and cobalt production from laterite ores using hydrometallurgical technology. In 2025, the company generated approximately USD 560 million in revenue and produced around 31,000 metric tons of finished nickel and 3,300 metric tons of cobalt. Terrafame Ltd. is a Finland-based mining company focused on low-carbon nickel and battery chemicals.

In 2025, Terrafame generated approximately USD 610 million in revenue and produced around 31,000 metric tons of nickel. Its battery chemicals plant has an annual production capacity of approximately 170,000 metric tons, strengthening Europe’s regional battery material supply chain.

The Major Players In The Industry

- Anglo American Plc

- BHP

- Eramet

- Glencore

- IGO Ltd.

- Metallurgical Corporation of China Ltd.

- Norlisk Nickel

- Rio Tinto

- South32 Ltd.

- Vale

- Sumitomo Metal Mining Co., Ltd.

- Sherritt International Corporation

- Jinchuan Group International Resources Co. Ltd

- Terrafame Ltd.

- Other Key Players

Key Development

- In February 2026, Vale S.A. finalized a four-party consortium agreement for the Thompson Nickel Belt through its subsidiary Vale Base Metals, formally recorded in its SEC regulatory filings. Under this strategic production collaboration, the company joined Exiro Minerals Corporation, Orion Resource Partners, and the Canada Growth Fund to advance regional critical mineral development.

- In January 2026, Rio Tinto and Glencore’s preliminary merger discussions in January 2026 involving potential combination of two of the world’s largest diversified mining companies illustrated the consolidation pressures operating at the top of the competitive hierarchy in a sustained low-price environment.

Report Scope

| Report Features | Description |

|---|---|

| Report Features | Description |

| Market Value (2025) | USD 36.4 Bn |

| Forecast Revenue (2035) | USD 64.3 Bn |

| CAGR (2026-2035) | 5.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Refined Nickel, Nickel Sulphate, Ferronickel, Nickel Pig Iron (NPI)), By Class (Class I Nickel, Class II Nickel), By Grade (Battery Grade Nickel, Industrial Grade Nickel), By Source (Primary Nickel, Secondary/Recycled Nickel), By Application (Stainless Steel Production, Batteries, Alloy Manufacturing, Electroplating, Foundry & Casting, Chemical Industry, Aerospace Components, Electronics & Electrical, Catalysts, Coinage, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Anglo American Plc, BHP, Eramet, Glencore, IGO Ltd., Metallurgical Corporation of China Ltd., Norlisk Nickel, Rio Tinto, South32 Ltd., Vale, Sumitomo Metal Mining Co. Ltd., Sherritt International Corporation, Jinchuan Group International Resources Co. Ltd, Terrafame Ltd., Other Key Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |