Quick Navigation

Report Overview

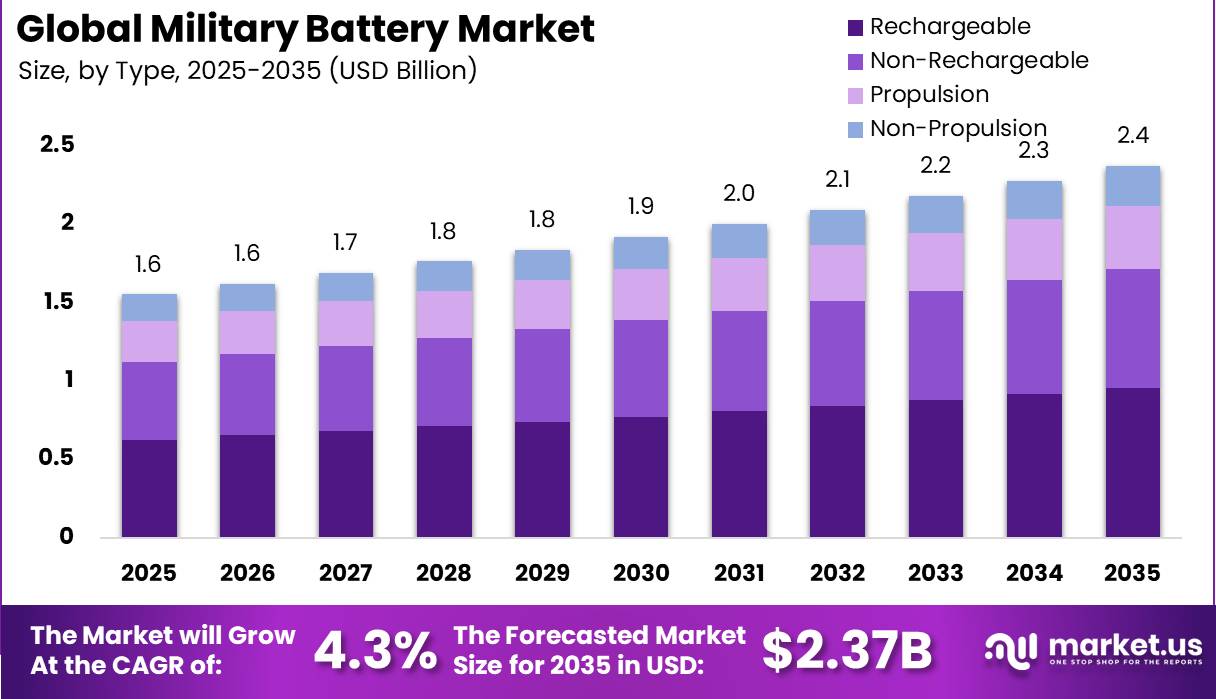

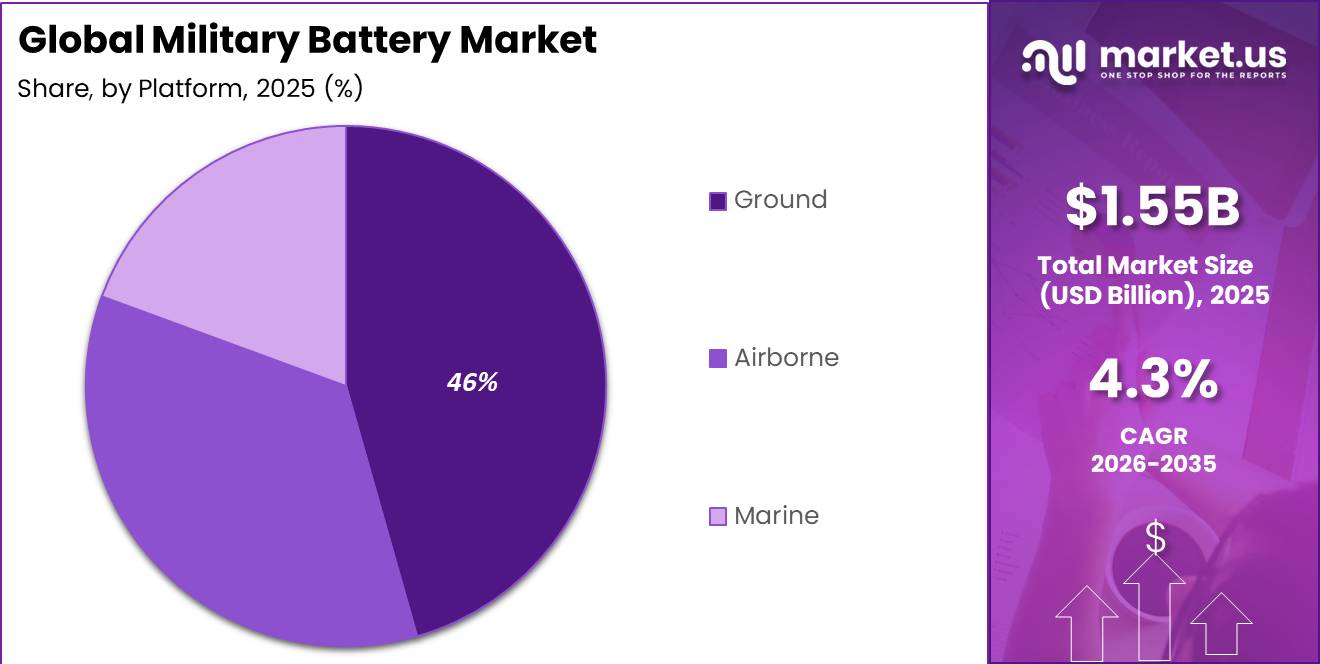

Global Military Battery Market size is expected to be worth around USD 2.37 Billion by 2035 from USD 1.55 Billion in 2025, growing at a CAGR of 4.3% during the forecast period 2026 to 2035.

The military battery market covers purpose-built energy storage systems designed for defense platforms, soldier systems, and unmanned vehicles. This market spans primary non-rechargeable cells, rechargeable packs, and advanced lithium-based chemistries. Products serve ground vehicles, airborne systems, and naval platforms across original equipment and aftermarket installation channels.

Key Takeaways

- Military Battery Market value in 2025 stands at USD 1.55 Billion, reaching USD 2.37 Billion by 2035 at a CAGR of 4.3%.

- Ground platform segment dominates with 46.0% share in the Platform segment.

- Rechargeable batteries hold 40.3% share in the Type segment.

- Lithium-based composition leads with 35.4% share in the Composition segment.

- OEM installation channel dominates with 65.6% share in the Installation segment.

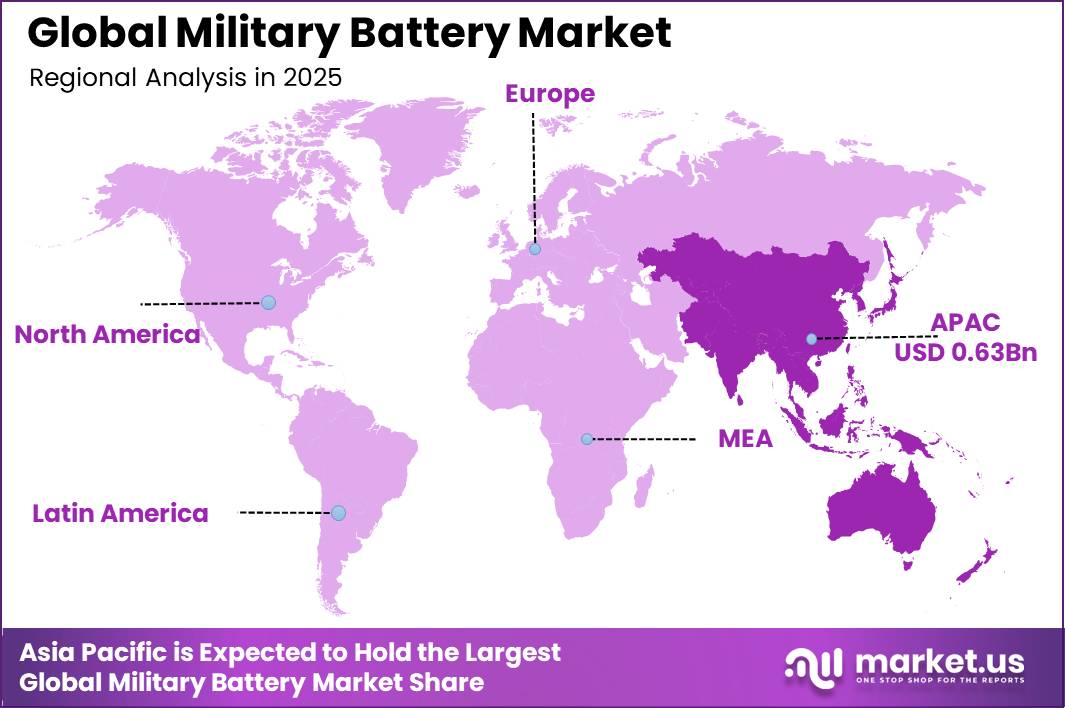

- Asia Pacific leads all regions with 40.8% market share, valued at USD 0.63 Billion in 2025.

According to Nasdaq, the U.S. Army awarded a multi-vendor Conformal Wearable Battery program with a ceiling value of approximately $1.25 Billion. This single contract signals the scale of soldier modernization investment now flowing into the battery supply chain. Suppliers that qualify under this program gain a structural revenue advantage over non-certified competitors.

As reported by Washington Technology, the Conformal Wearable Battery carries approximately 150 Wh of energy capacity per unit. This specification sets a new baseline for wearable soldier power that legacy battery chemistries cannot meet. Battery makers that do not develop compact high-energy formats risk losing soldier system contracts to newer entrants.

Defense electronics spending continues to tighten requirements around energy density, thermal management, and field logistics. Ultralife Corporation received a $5.2 Million Defense Logistics Agency contract in September 2025 for BA-5390 lithium manganese dioxide batteries used in U.S. military tactical communications systems. This contract reflects persistent procurement of mission-critical primary cells alongside newer rechargeable platforms, confirming that both segments remain commercially active through the forecast period.

Platform Analysis

Ground dominates with 46.0% due to armored vehicle and troop transport density.

In 2025, Ground held a dominant market position in the By Platform segment of the Military Battery Market, with a 46.0% share. Ground platforms encompass armored vehicles, infantry carriers, tactical trucks, and robotic ground systems that require high-capacity, high-discharge batteries for propulsion support, silent watch, and onboard electronics. This segment’s scale reflects the sheer volume of land-based military assets globally. Suppliers serving ground platforms benefit from long procurement cycles and predictable replacement demand.

Airborne platforms represent the fastest-repositioning segment within the military battery market. Fixed-wing aircraft, rotorcraft, and unmanned aerial vehicles each impose distinct weight, thermal, and energy-density constraints on battery specifications. Defense forces expanding drone fleets are accelerating airborne battery volume, creating multi-year demand for lightweight high-cycle packs across ISR, strike, and logistics unmanned missions.

Marine platforms place the most demanding thermal and depth-pressure requirements on military battery design. Submarine applications, unmanned underwater vehicles, and surface combatants require chemistries that maintain performance across wide temperature ranges and extended mission durations. Naval forces in the Indo-Pacific region are expanding undersea capability investments, making marine the segment with the longest development and qualification lead times for new entrants.

Type Analysis

Rechargeable dominates with 40.3% due to operational cost and logistics efficiency gains.

In 2025, Rechargeable held a dominant market position in the By Type segment of the Military Battery Market, with a 40.3% share. Rechargeable batteries reduce the logistical burden of continuous primary cell resupply in operational theaters. Defense procurement programs increasingly specify rechargeable formats to lower the total lifecycle cost of soldier and vehicle power systems. This shift creates a growing installed base that generates recurring demand for replacement packs and charging infrastructure.

Non-Rechargeable batteries retain a substantial share of defense procurement because primary cells offer superior shelf life, immediate readiness, and reliable performance in extreme temperature environments. Special operations, emergency locator systems, and disposable munition applications depend on non-rechargeable chemistry for mission-critical reliability. This segment remains commercially stable because no rechargeable platform can replicate primary cell shelf-life performance across all operational conditions.

Propulsion batteries represent a distinct and structurally separate sub-type from conventional power and communication batteries. Submarine propulsion, UUV drive systems, and emerging hybrid-electric ground vehicles require high-voltage, high-capacity packs engineered specifically for traction applications. As defense forces invest in quiet propulsion, the propulsion sub-type is expanding into higher contract values that standard power batteries cannot serve.

Composition Analysis

Lithium-based dominates with 35.4% due to superior energy density and weight advantage.

In 2025, Lithium-based held a dominant market position in the By Composition segment of the Military Battery Market, with a 35.4% share. Lithium chemistry enables military platforms to carry more energy at lower weight, directly improving soldier endurance, vehicle range, and drone flight duration. Defense procurement bodies across NATO and Indo-Pacific forces have standardized lithium formats as the preferred chemistry for new platform development. This composition dominance will deepen as solid-state and lithium-sulfur variants enter qualification pipelines.

Lead-acid batteries retain a meaningful presence in military inventories due to their low cost, broad supplier base, and proven reliability in vehicle starting and auxiliary power applications. Legacy military fleets still carry significant lead-acid installed bases that generate consistent replacement demand. However, fleet modernization programs are systematically displacing lead-acid with lithium-based alternatives in high-priority platforms, compressing long-term volume for this chemistry.

Nickel-based and Thermal compositions serve specialized defense niches that lithium cannot fully address. Nickel-cadmium formats maintain a role in avionic and safety-critical backup systems where established qualification records reduce re-certification risk. Thermal batteries serve single-use ordnance and missile applications where instantaneous high-power activation is required. These compositions, along with other specialty chemistries, collectively hold the balance of market share beyond lead-acid and lithium.

Installation Analysis

OEM dominates with 65.6% due to embedded specification and platform integration requirements.

In 2025, OEM held a dominant market position in the By Installation segment of the Military Battery Market, with a 65.6% share. Defense platforms integrate batteries at the design stage, binding procurement to specific chemistry, form factor, and management system specifications. OEM-qualified suppliers gain a protected revenue position for the operational life of the platform, often spanning one to two decades. This structural advantage makes OEM qualification the most valuable commercial position in the military battery supply chain.

Aftermarket installation covers battery replacement, upgrade kits, and capacity expansion for in-service platforms that require a chemistry transition or performance improvement outside the original OEM specification. This channel is growing as defense forces upgrade existing fleets to lithium-based systems without full platform replacement. Aftermarket suppliers that achieve military qualification standards can access a cost-effective entry point into defense battery procurement without competing directly against embedded OEM vendors.

Key Market Segments

By Platform

- Ground

- Airborne

- Marine

By Type

- Non-Rechargeable

- Rechargeable

- Propulsion

- Non-Propulsion

By Composition

- Rotary Lithium-based

- Lead Acid

- Nickel-based

- Thermal

- Others

By Installation

- OEM

- Aftermarket

Drivers

The strongest growth driver for military batteries is the rapid expansion of unmanned systems, which is reshaping defense battery demand from a replacement-based market into a high-consumption operational one. A 2025 U.S. government-linked assessment indicated that 2 million drones using approximately 300 Wh each could equal roughly 100% of the Department of Defense’s annual battery demand and more than 1,000% of its annual lithium-ion battery requirements. This scale of potential consumption confirms that unmanned system procurement is now the primary demand multiplier for military battery suppliers.

This shift is driving increasing deployment of drones, loitering munitions, and portable ISR systems across Europe, North America, and the Indo-Pacific. Force-modernization programs in these regions continue to accelerate platform procurement, which converts into recurring battery demand tied to operational usage rates rather than one-time purchases. Suppliers capable of delivering high-volume cylindrical and pouch-cell assemblies at military safety and reliability standards are positioned to capture this expanding revenue base. In May 2025, InoBat launched the E10 battery cell for military drones, offering charging times below 15 minutes and up to 40% higher payload capability than conventional drone batteries, illustrating the pace of product development now targeting this driver.

NATO and allied rearmament programs are lifting battery procurement intensity across ground, airborne, and naval platforms simultaneously. Soldier power modernization, including conformal wearable battery programs, is expanding battery demand beyond vehicles into individual infantry loadouts. Hybrid-electric and silent-watch vehicle architectures are generating pack contract values that exceed conventional auxiliary battery programs by a structural multiple. These three concurrent demand drivers create a compounding procurement environment that rewards suppliers with diverse platform coverage and qualified multi-chemistry product lines.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NATO and allied rearmament lifting battery procurement intensity | +1.9% | North America core, Europe core, APAC allied programs | Short term (≤ 2 years) |

| Drone and loitering-munition scale-up raising high-cycle battery volumes | +1.6% | Europe frontline demand, North America, APAC corridors, Middle East spill-over | Short term (≤ 2 years) |

| Soldier power modernization and conformal wearable battery programs | +1.1% | U.S. core, NATO interoperability markets, selective APAC defense forces | Medium term (2-4 years) |

| Hybrid-electric and silent-watch vehicle architectures expanding pack value | +1.0% | U.S. armored fleet, Europe modernization, APAC land systems | Medium term (2-4 years) |

| Battery security, domestic sourcing, and standardization policy | +0.9% | U.S. core, EU strategic autonomy corridor, India, allied reshoring markets | Medium term (2-4 years) |

| Submarine, UUV, and naval endurance upgrades favoring lithium systems | +0.7% | Indo-Pacific navies, U.S. Navy ecosystem, European naval programs | Long term (≥ 4 years) |

Restraints

Air-transport regulations for lithium-ion batteries tightened from 1 January 2026, requiring batteries shipped by air to be offered at no more than 30% state of charge absent special approvals. For military supply chains, this creates a direct readiness-commercial tradeoff because air freight is often the only viable rapid-deployment route into dispersed theaters. Batteries that arrive at reduced charge require in-theater conditioning infrastructure before use, adding operational latency to time-sensitive missions.

The practical compliance burden extends beyond paperwork to pre-shipment conditioning, additional ground handling, repacking, and in-theater charging infrastructure. These steps can add 3 to 10 days to urgent replenishment cycles and raise logistics cost per shipment by an estimated 8% to 15% for high-value ruggedized packs across NATO and Indo-Pacific routes. Expeditionary customers facing these added costs may delay battery-heavy subsystem deployments or maintain legacy chemistries in service longer, creating a near-term procurement drag estimated at 1.1 percentage points on market CAGR.

Critical mineral concentration in geopolitically sensitive supply chains creates a separate structural restraint on battery procurement timelines. Lithium, cobalt, and manganese sourcing remains concentrated in a small number of exporting countries subject to export restriction risk. Defense procurement bodies that depend on commercial lithium-ion supply chains face exposure to policy-driven supply disruptions that can delay platform battery programs and force costly reformulation cycles during active procurement periods.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical mineral concentration | -1.9% | North America core, EU, Japan, Korea | Medium term (2-4 years) |

| Battery air-shipping limits | -1.1% | Global expeditionary routes, NATO, Indo-Pacific | Short term (≤ 2 years) |

| Defense qualification delays | -1.5% | U.S., NATO Europe, allied OEM programs | Medium term (2-4 years) |

| Program-specific battery fragmentation | -1.3% | U.S. core, NATO, select APAC forces | Medium term (2-4 years) |

| Compliance and traceability burden | -0.9% | EU, UK-linked supply chains, NATO vendors | Short term (≤ 2 years) |

| Tariffs and trade-policy volatility | -1.0% | U.S.-linked imports, allied sourcing corridors | Short term (≤ 2 years) |

Challenges

Defense-grade battery qualification represents a structural bottleneck that constrains how quickly new chemistries reach operational deployment. Unlike commercial applications, defense batteries must pass validation for shock, vibration, thermal performance, shelf life, electromagnetic compatibility, and mission-specific reliability across diverse operating environments. This process prevents direct adoption of civilian battery platforms regardless of their technical performance on commercial benchmarks.

As per our research, qualification cycles for defense battery programs typically extend 12 to 24 months, while ruggedization efforts and custom pack redesigns reduce pilot-line yields by 5 to 10 percentage points compared with commercial production. Any material, component, or battery-management-system modification can trigger additional requalification periods of 4 to 9 months. This extended validation burden forces manufacturers to maintain parallel legacy and next-generation product portfolios for limited defense volumes, compressing margin across both product lines simultaneously.

Market expansion is constrained less by technology availability than by qualification timelines, which means the competitive advantage in this market belongs to suppliers with pre-qualified platforms and established testing relationships with defense agencies. Modular designs, standardized testing frameworks, digital-twin validation methods, and shared qualification programs are all gaining importance as mechanisms to compress these timelines. Suppliers that invest in these capabilities today will shorten their time-to-contract window relative to competitors still operating under legacy certification processes.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Critical minerals concentration | -1.4% | North America core, NATO Europe, Indo-Pacific allies | Long term (≥ 4 years) |

| Defense-grade qualification delays | -1.1% | U.S. programs, NATO procurement hubs, Israel, Japan, South Korea | Medium term (2-4 years) |

| Skilled electrochemistry labor gap | -0.9% | U.S. manufacturing belt, Western Europe, South Korea, Japan | Medium term (2-4 years) |

| Thermal safety integration burden | -0.8% | UAV-intensive forces, naval platforms, desert and Arctic theaters | Medium term (2-4 years) |

| Fragmented military battery standards | -0.7% | NATO fleets, U.S. tri-service programs, APAC allied integrators | Long term (≥ 4 years) |

| Traceability and compliance overhead | -0.6% | U.S. DFARS ecosystem, EU defense suppliers, allied sourcing corridors | Short term (≤ 2 years) |

Opportunities

Hybrid-electric tactical and combat vehicles represent a high-value expansion opportunity for battery suppliers capable of moving beyond auxiliary power into propulsion-adjacent energy storage. Most military fleets still rely on conventional drivetrains and legacy lead-acid systems, making this an emerging rather than current revenue stream. However, the structural shift in defense priorities toward fuel efficiency, silent mobility, and reduced logistics burden is gradually converting pilot programs into procurement commitments.

As per our research, annual demand for approximately 300,000 6T lead-acid batteries and defense studies evaluating 60 kWh-class hybrid systems for tactical vehicles confirm the scale of potential displacement. Even modest adoption across suitable fleet segments could generate incremental demand measured in the hundreds of MWh annually, alongside recurring software, monitoring, and thermal-management revenue streams. Battery-system contract values in hybrid platforms can be 8 to 15 times higher than those of conventional low-voltage battery packs. This multiple makes hybrid vehicle programs the single highest-value expansion path for qualified military battery suppliers operating today.

Solid-state battery integration for next-generation infantry power architectures and high-temperature energy storage for Middle East and desert theater operations represent additional avenues where early qualification creates durable competitive barriers. Modular swappable battery ecosystems for autonomous ground and maritime defense platforms further expand addressable revenue by converting one-time platform sales into recurring swap and service contracts. Suppliers that establish MIL-spec modular platforms and hybrid integration capabilities early are positioned to capture disproportionate contract value as these programs scale.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Battery standardization platforms | +2.4% | North America core, NATO Europe | Short term (≤ 2 years) |

| Hybrid combat vehicle packs | +2.1% | U.S., UK, Western Europe, South Korea | Medium term (2-4 years) |

| Defense drone swarm power stacks | +2.8% | U.S., NATO Europe, Israel, APAC allies | Short term (≤ 2 years) |

| Space and HAPS battery niches | +1.6% | U.S., Europe, Japan | Medium term (2-4 years) |

| Lifecycle services and digital twins | +1.9% | North America core, EU, GCC, APAC allies | Short term (≤ 2 years) |

| Allied secure supply-chain roll-ups | +2.2% | U.S., Canada, Australia, EU | Long term (≥ 4 years) |

Regional Analysis

Asia Pacific Dominates the Military Battery Market with a Market Share of 40.8%, Valued at USD 0.63 Billion

Asia Pacific commands 40.8% of the global military battery market, valued at USD 0.63 Billion in 2025. Sustained defense budget expansion across China, India, South Korea, Japan, and Australia is driving procurement of advanced battery systems for ground, airborne, and naval platforms. Indo-Pacific territorial tensions are accelerating force modernization timelines, converting long-term procurement plans into near-term battery purchase orders across all platform categories.

North America holds the second-largest regional position, anchored by U.S. defense spending on soldier modernization, unmanned systems, and vehicle electrification programs. The Conformal Wearable Battery program and Defense Logistics Agency contracts provide a structural procurement floor that stabilizes demand across primary and rechargeable battery segments. This region generates the highest contract values per unit due to rigorous military specification requirements and domestic sourcing policies.

Europe is experiencing a defense budget reset driven by NATO rearmament commitments following sustained conflict on the continent’s eastern border. Countries increasing defense expenditure to meet or exceed 2% of GDP targets are directing capital into land systems, drone fleets, and electronic warfare platforms, all of which require military-grade batteries. This spending shift is transforming Europe from a stable replacement market into an active platform procurement zone.

Latin America and the Middle East and Africa regions represent smaller but strategically relevant battery procurement zones. Gulf Cooperation Council states are investing in high-temperature capable energy storage for desert theater operations. Latin American defense forces prioritize cost-effective rechargeable formats for ground and airborne platforms. Both regions offer entry points for suppliers seeking to diversify beyond saturated NATO and Indo-Pacific procurement channels.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

EnerSys holds a structural advantage in the military battery market through its broad platform coverage across ground vehicles, aerospace, and naval applications. In September 2025, the company launched the Hawker ARMASAFE iON-X 24-volt lithium-ion batteries in 105 Ah and 162 Ah models for silent watch, robotics, and unmanned vehicle applications. This product launch directly targets the vehicle electrification and silent mobility requirements that now define NATO procurement criteria.

GS Yuasa International Ltd leverages deep manufacturing expertise in both lead-acid and lithium-based chemistries to serve defense customers across airborne, marine, and ground segments. Data from our research shows the EU allocated approximately €400 Million from the European Defence Fund to AI and drone-related projects between 2021 and 2024, creating a direct procurement tailwind for suppliers with qualified drone battery platforms. GS Yuasa’s established position in European and Indo-Pacific defense supply chains positions the company to benefit from this funded expansion of unmanned system fleets.

Key Players

- EnerSys

- GS Yuasa International Ltd

- Saft

- Exide Industries

- EaglePicher Technologies

- Bren-Tronics

- Ultralife Corporation

- CBAK Energy Technology

- Epsilor-Electric Fuel Ltd.

- Denchi Group

- VITZRO CELL, Co., Ltd

- Military Battery Systems

- FIB SPA

- EVS Supply

- AceOn Group

- Other Key Players

Recent Developments

- April 2025 – Saft America secured a US$7.54 Million contract from the U.S. Defense Logistics Agency to supply batteries for H-1, Seahawk, and CH-53 military helicopter fleets operated by the U.S. Army, Navy, Marine Corps, Air Force, and Coast Guard.

- July 2025 – Amprius Technologies received a US$10.5 Million contract from the U.S. Defense Innovation Unit to accelerate qualification and manufacturing scale-up of its silicon-anode military battery technology.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.55 Billion |

| Forecast Revenue (2035) | USD 2.37 Billion |

| CAGR (2026-2035) | 4.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Platform (Ground, Airborne, Marine), By Type (Non-Rechargeable, Rechargeable, Propulsion, Non-Propulsion), By Composition (Rotary Lithium-based, Lead Acid, Nickel-based, Thermal, Others), By Installation (OEM, Aftermarket) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | EnerSys, GS Yuasa International Ltd, Saft, Exide Industries, EaglePicher Technologies, Bren-Tronics, Ultralife Corporation, CBAK Energy Technology, Epsilor-Electric Fuel Ltd., Denchi Group, VITZRO CELL Co. Ltd, Military Battery Systems, FIB SPA, EVS Supply, AceOn Group, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |