Quick Navigation

Report Overview

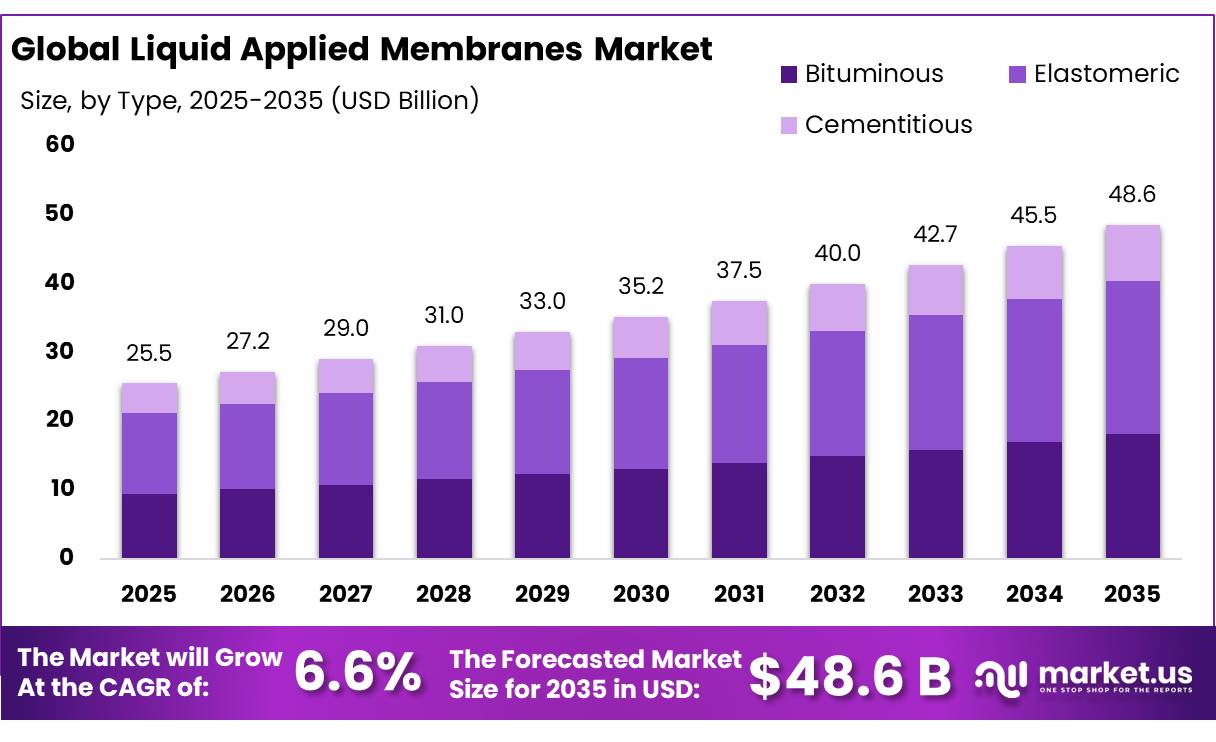

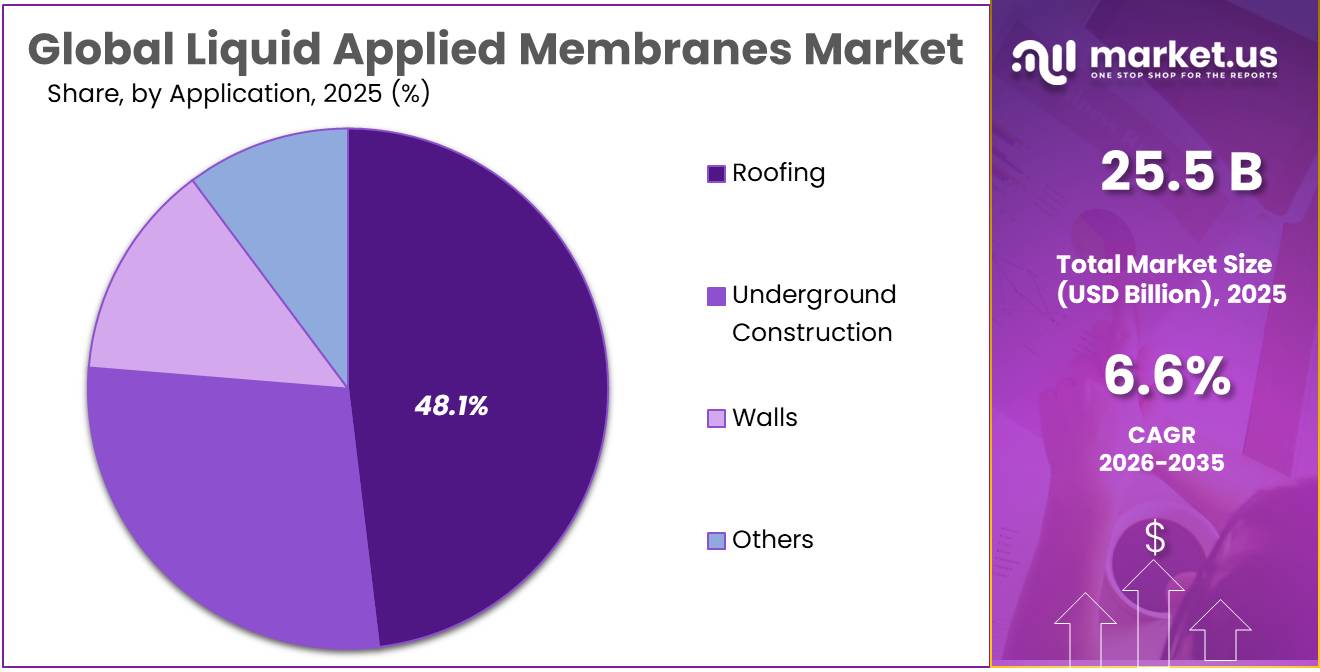

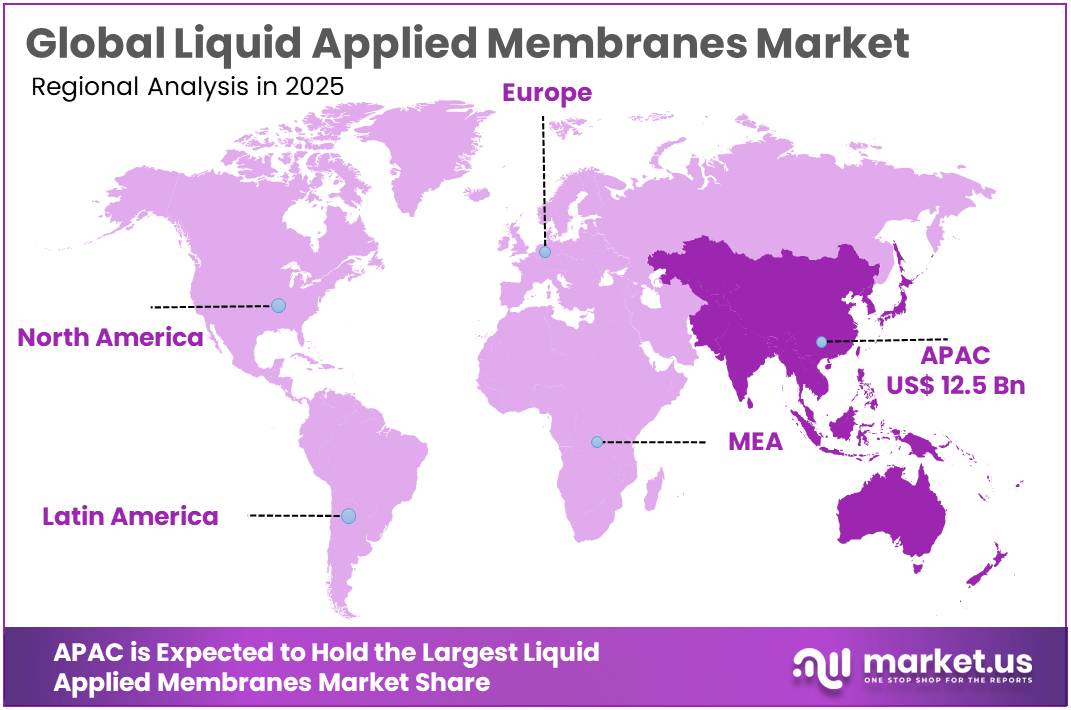

The Global Liquid Applied Membranes Market size is expected to be worth around USD 48.6 Billion by 2035, from USD 25.2 Billion in 2025, growing at a CAGR of 6.6% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 49.3% share, holding USD 12.5 Billion revenue.

Liquid-applied membranes are gaining importance as seamless waterproofing systems for roofs, podiums, basements, wet areas and refurbishment projects, because they can be applied around complex penetrations and reduce leakage risk versus jointed sheet systems. The industry is being shaped by aging buildings, climate-resilient construction and energy-efficient roofing, as buildings account for around 30% of global energy demand and contributed about 20% of demand growth since 2019, according to the IEA.

The industrial scenario is being shaped by renovation, climate resilience and stricter building-performance policy rather than only new construction. Buildings and construction consumed 32% of global energy and contributed 34% of global CO₂ emissions in the UNEP 2024/25 assessment, making envelope durability and roof protection important parts of lower-carbon asset management. In Europe, buildings account for around 40% of energy use, around 50% of gas consumption and roughly 80% of household energy use for heating, cooling and hot water, supporting refurbishment demand for roofs, terraces and facades.

Demand drivers are strongest in repair, reroofing, infrastructure protection and low-carbon refurbishment. UNEP/GlobalABC reported that buildings and construction accounted for 34% of global energy demand and 34% of emissions in 2023, keeping pressure on regulators and asset owners to extend building life through waterproofing and envelope upgrades.

In Europe, the revised Energy Performance of Buildings Directive entered force on 28 May 2024, requires national transposition by 29 May 2026, and targets a fully decarbonized building stock by 2050, supporting renovation-led demand. In the U.S., the Bipartisan Infrastructure Law authorizes USD 1.2 trillion, including USD 550 billion in new investments, supporting bridges, transport, water, and public infrastructure where durable waterproofing systems are required.

Among leading chemical players, Sika remains a key reference supplier. In 2025, Sika reported sales of CHF 11,201.3 million, local-currency growth of 0.6%, material margin of 54.9%, adjusted EBITDA margin of 19.2%, net profit of CHF 1,045.3 million, and operating free cash flow of CHF 1,356.1 million. Sika also announced seven bolt-on acquisitions in 2025, supporting capacity expansion and innovation-led construction growth.

Key Takeaways

- Liquid Applied Membranes Market size is expected to be worth around USD 48.6 Billion by 2035, from USD 25.2 Billion in 2025, growing at a CAGR of 6.6%.

- Elastomeric held a dominant market position, capturing more than a 45.8% share.

- Roofing held a dominant market position, capturing more than a 48.1% share.

- Asia-Pacific holds the leading position in the liquid applied membranes market, accounting for 49.3% share with a market value of around USD 12.5 billion.

By Type Analysis

Elastomeric leads with 45.8% due to its flexibility and strong waterproofing performance

In 2025, Elastomeric held a dominant market position, capturing more than a 45.8% share. This strong position comes from its ability to stretch and adapt to surface movement without cracking, which makes it highly reliable for waterproofing applications. Builders and contractors prefer elastomeric membranes for roofs, walls, and terraces because they can handle temperature changes and structural shifts better than many other materials. These membranes also form a seamless layer, which helps prevent water leakage and reduces long-term maintenance issues.

By Application Analysis

Roofing leads with 48.1% driven by rising demand for long-lasting waterproof protection

In 2025, Roofing held a dominant market position, capturing more than a 48.1% share. This strong share comes from the growing need to protect buildings from water damage, leaks, and weather exposure. Liquid applied membranes are widely used on roofs because they create a seamless and flexible layer that can easily cover cracks, joints, and uneven surfaces. This makes them a practical choice for both new construction and repair work. Many contractors prefer these membranes as they are easy to apply and help extend the life of roofing systems without major structural changes.

Key Market Segments

By Type

- Bituminous

- Elastomeric

- Cementitious

By Application

- Roofing

- Underground Construction

- Walls

- Others

Emerging Trends

Shift Toward Sustainable and Food-Safe Waterproofing Systems is a Key Trend

One of the latest trends in liquid applied membranes is the growing shift toward sustainable and food-safe waterproofing solutions, especially in facilities linked to food storage and processing. The scale of food waste globally is pushing this change. According to global data, around 1.05 billion tonnes of food were wasted in 2022, which equals nearly 19% of food available to consumers, while an additional 13% is lost in the supply chain before retail. This highlights how critical proper infrastructure is in reducing losses.

In 2025–2026, industries are increasingly choosing liquid applied membranes that are low-emission, durable, and safe for environments where food is handled. Governments are also supporting this shift through initiatives like SDG 12.3, which focuses on cutting global food waste by half by 2030. These membranes are being used in warehouses, cold storage units, and food processing plants because they create seamless, leak-proof surfaces that reduce moisture damage.

Increasing Integration with Cold Chain and Smart Infrastructure

Another important trend is the growing integration of liquid applied membranes into cold chain and modern storage systems. A large portion of food loss is linked to poor storage conditions, especially where moisture and temperature control are not maintained. Studies show that nearly one-third of food produced globally is lost or wasted, and this loss is closely tied to infrastructure gaps

Liquid applied membranes are now being widely used in cold storage facilities, transport hubs, and processing plants to prevent water penetration and maintain stable internal conditions. Governments and organizations like FAO are promoting better storage infrastructure to improve food security and reduce environmental impact. By 2026, there is a clear trend toward combining waterproofing with smart infrastructure planning, where materials are chosen not just for durability but also for efficiency and long-term performance.

Drivers

Rising Need to Reduce Food Loss Through Better Storage Infrastructure

One major driving factor for liquid applied membranes is the growing need to protect food during storage and handling. A large amount of food is still lost because of poor infrastructure, especially where moisture and leakage damage storage facilities. According to the Food and Agriculture Organization, nearly 13.3% of food—around 1.31 billion tonnes—is lost between harvest and retail every year.

This is pushing governments and industries to improve storage conditions, especially in warehouses, silos, and cold storage units. Liquid applied membranes are becoming important here because they provide strong waterproofing and prevent moisture from entering structures. In 2025–2026, many countries are investing in better food storage infrastructure under programs linked to food security and waste reduction goals like SDG 12.3. These membranes are easy to apply and form seamless layers, which makes them ideal for protecting storage buildings from leaks and dampness. The result is simple—less moisture means less spoilage and better food quality.

Increasing Focus on Hygiene and Food Safety in Processing Facilities

Another strong driver is the growing focus on hygiene and food safety in processing environments. When buildings are exposed to water leakage or damp conditions, it increases the risk of contamination and mold growth, which can damage food products. The United Nations Environment Programme reports that about 19% of food available to consumers is wasted globally, highlighting how important proper handling and storage conditions are.

To reduce this waste, food companies are upgrading their facilities with better waterproofing and protective systems. Liquid applied membranes help keep surfaces dry and easy to clean, which supports strict hygiene standards. Governments are also tightening food safety regulations, encouraging industries to use materials that prevent leakage and contamination. By 2026, more food processing plants are expected to adopt these membranes as part of their infrastructure upgrades.

Restraints

High Application Sensitivity and Surface Preparation Challenges Limit Adoption

One major restraining factor for liquid applied membranes is the need for proper surface preparation and controlled application conditions. These membranes perform well only when applied on clean, dry, and stable surfaces. In real-world environments, especially in food storage and processing facilities, maintaining such ideal conditions is not always easy. According to the Food and Agriculture Organization, around 13% of food—about 1.25 billion tonnes—is lost in the supply chain before retail

To reduce such losses, industries invest in better storage infrastructure, but improper membrane application can lead to leaks and moisture entry, defeating the purpose. Government initiatives under SDG 12.3 encourage improved storage systems, yet the success of these systems depends heavily on correct installation practices. In 2025–2026, many projects still face delays or performance issues because trained labor and proper site conditions are not always available.

Performance Variability Under Moisture and Harsh Operating Conditions

Another key restraint is the performance variability of liquid applied membranes in extreme or constantly wet environments. While these membranes are designed to resist water, continuous exposure to moisture, temperature changes, and chemical cleaning can affect their long-term durability. This is especially relevant in food-related facilities where hygiene requires frequent washing and wet conditions. According to the United Nations Environment Programme, about 1.05 billion tonnes of food were wasted in 2022, equal to 19% of food available to consumers

This level of waste highlights how critical proper storage and infrastructure are, but if membranes degrade over time, they can allow moisture infiltration, leading to spoilage and contamination risks. Governments are pushing for stronger food safety and storage standards, but the materials used must perform consistently under real conditions. By 2026, industries are increasingly aware of this gap between expected and actual performance.

Opportunity

Growing Demand for Cold Storage and Food Infrastructure Creates Strong Opportunity

One major growth opportunity for liquid applied membranes is the rapid expansion of cold storage and food infrastructure across the world. A large portion of food is still lost due to poor storage conditions, especially where moisture and leakage damage facilities. According to the United Nations Environment Programme, about 1.05 billion tonnes of food were wasted in 2022, which is nearly 19% of food available to consumers. In addition, around 13% of food is lost before reaching retail, mainly due to supply chain inefficiencies

This has pushed governments and industries to invest in better storage systems, including warehouses, cold chains, and food processing units. Liquid applied membranes are gaining importance here because they provide seamless waterproofing, helping protect buildings from leaks and dampness. In 2025–2026, many countries are improving food storage under sustainability goals like SDG 12.3, which aims to reduce food waste by half. These membranes help maintain dry and stable environments, which is critical for preserving food quality.

Increasing Focus on Reducing Food Waste Through Better Facility Protection

Another strong opportunity comes from the global push to reduce food waste by improving facility protection and hygiene. Food loss is not only a supply issue but also linked to poor building conditions, where moisture can lead to spoilage and contamination. Reports show that households alone account for about 60% of global food waste, highlighting how sensitive food quality is to storage and handling conditions

To address this, governments and organizations like FAO and UNEP are encouraging investments in better infrastructure and food safety systems. Liquid applied membranes are being used more widely in food processing plants, storage facilities, and logistics centers to prevent water penetration and maintain clean environments. By 2026, industries are focusing on long-lasting and easy-to-maintain building materials that support hygiene and reduce operational risks.

Regional Insights

Asia-Pacific dominates with 49.3% (USD 12.5 Bn) driven by strong construction growth and infrastructure expansion

Asia-Pacific holds the leading position in the liquid applied membranes market, accounting for 49.3% share with a market value of around USD 12.5 billion. This dominance is mainly supported by rapid urbanization and large-scale construction activities across countries like China, India, Japan, and Southeast Asia. The region has seen continuous growth in residential housing, commercial buildings, and industrial infrastructure, all of which require effective waterproofing solutions.

In 2025, the region continued to benefit from increasing government investments in infrastructure and smart city development programs. Countries such as India and China have been focusing heavily on urban expansion, with millions of square meters of new construction being added every year. This directly increases the demand for roofing and waterproofing materials, including liquid applied membranes. The construction sector in Asia-Pacific remains one of the largest globally, contributing a major share to coating and building material consumption.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Sika AG remains a leading player in liquid applied membranes through its strong construction chemicals portfolio, especially in waterproofing and roofing systems. In 2025, the company reported total sales of around CHF 11,201.3 million, with an EBITDA of CHF 2,064.7 million and net profit of CHF 1,045.3 million. It operates in 100+ countries with over 33,000 employees, supporting global infrastructure projects. Its membrane solutions are widely used in roofing, basements, and tunnels, helping improve durability and water resistance in construction.

Pidilite Industries is a strong regional player in waterproofing and adhesive-based membrane solutions, especially in India and Asia. In 2025, the company generated revenue of around ₹13,000+ crore (USD ~1.5–1.6 billion) with a steady growth rate of 10–12% annually. It operates across 70+ countries with a wide product portfolio including waterproofing brands like Dr. Fixit. The company focuses heavily on retail and construction segments, making it a key contributor to liquid membrane demand in developing markets.

Top Key Players Outlook

- Sika AG

- Pidilite Industries

- BASF SE

- Chembond Chemicals

- The Dow Chemical Company

- Fosroc International

- Saint Gobain

- H.B. Fuller Construction Products Inc

- Applied Membranes, Inc

- Soprema

Recent Industry Developments

By 2026, Dow is focusing on cost optimization and sustainability, supported by initiatives like its $2 billion transformation program, while maintaining steady demand in coatings-related applications.

In 2025, Chembond Chemicals reported consolidated revenue of around ₹201 crore in FY2025, showing a 12.9% year-on-year growth, with operating profit improving to about ₹13 crore.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 25.5 Bn |

| Forecast Revenue (2035) | USD 48.6 Bn |

| CAGR (2026-2035) | 6.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Bituminous, Elastomeric, Cementitious), By Application (Roofing, Underground Construction, Walls, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Sika AG, Pidilite Industries, BASF SE, Chembond Chemicals, The Dow Chemical Company, Fosroc International, Saint Gobain, H.B. Fuller Construction Products Inc, Applied Membranes, Inc, Soprema |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |