Quick Navigation

Report Overview

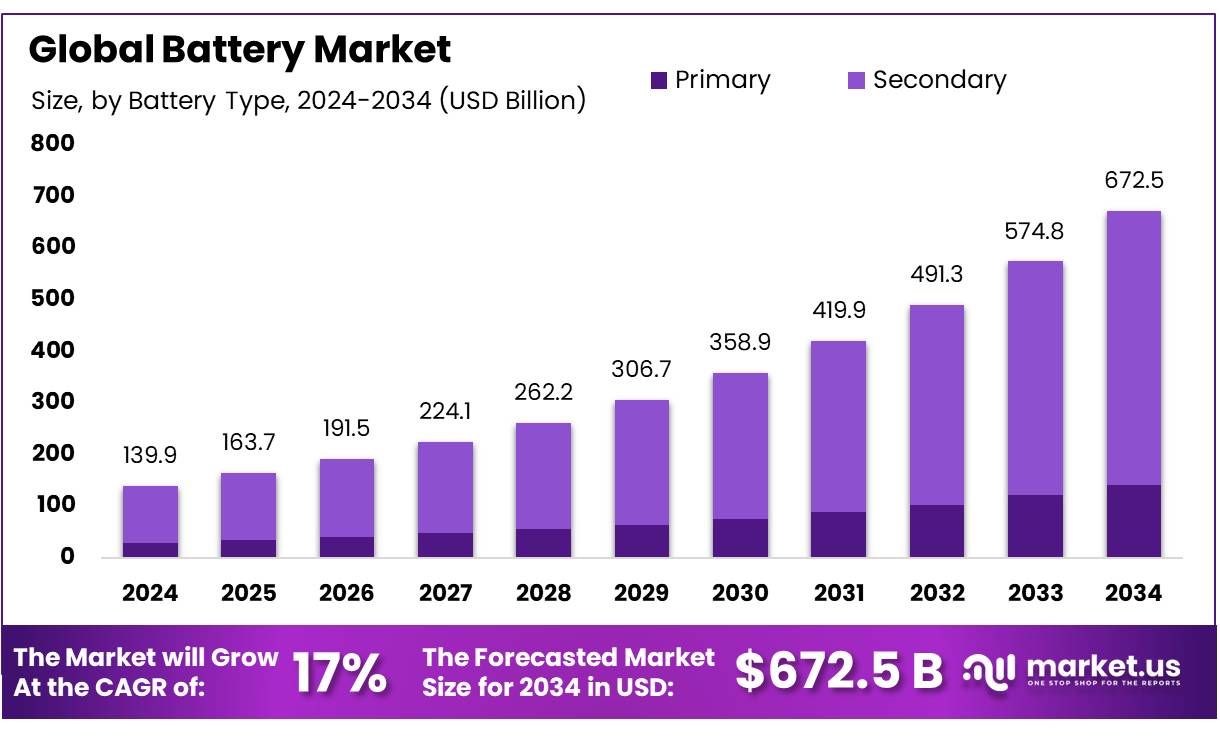

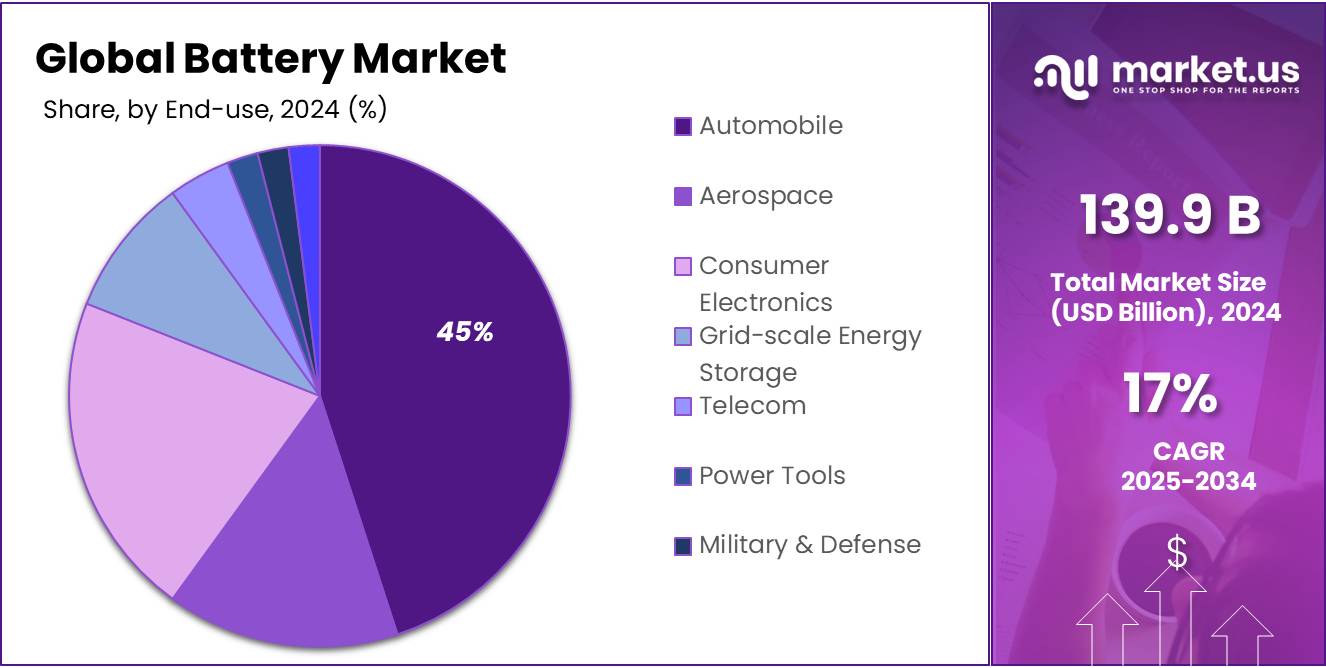

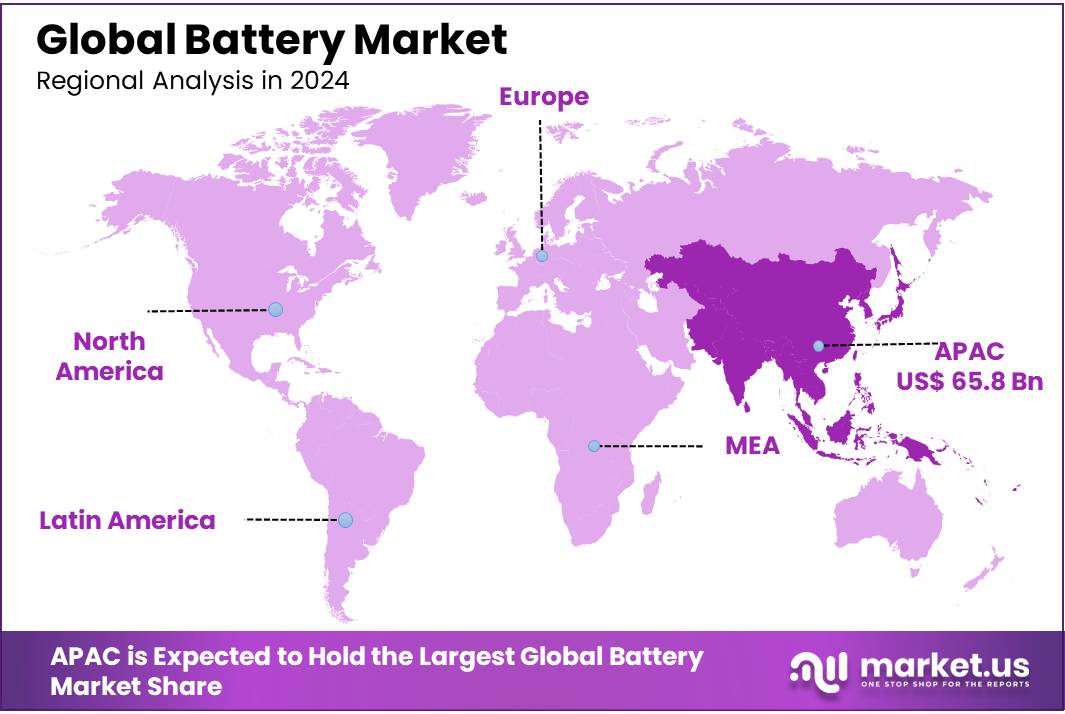

The Global Battery Market size is expected to be worth around USD 672.5 Bn by 2034, from USD 139.9 Bn in 2024, growing at a CAGR of 17.0% during the forecast period from 2025 to 2034. In 2024, Asia Pacific dominated the market with a 47.10% share, generating USD 65.8 Bn in revenue.

The market for electric vehicles (EVs) is expanding rapidly, significantly contributing to the growth of the battery market. This increase is further supported by the rising integration of renewable energy sources into power grids, necessitating robust energy storage solutions. The unpredictable availability of solar and wind energy requires dependable storage systems, like batteries, to ensure consistent electricity supply. Notably, technologies such as flow batteries and solid-state batteries are becoming popular in the renewable sector due to their scalability and enhanced durability, aiding in the shift towards a cleaner energy mix.

In 2023, battery storage emerged as the fastest-growing commercially available energy technology, with deployment rates more than doubling from the previous year. This growth spans utility-scale projects, behind-the-meter installations, mini-grids, and solar home systems, all of which contribute to increased electricity access. Additionally, the surge in EV adoption, which saw a 40% increase in 2023, primarily fueled the demand for batteries, with 14 million electric cars accounting for the majority of energy sector battery usage.

The automotive industry is crucial in driving the battery market forward. Governments across the globe are enacting various regulations and offering incentives to boost EV adoption and promote sustainable transportation. The U.S., China, and European countries are particularly proactive, providing subsidies, tax credits, and other benefits to facilitate the transition to cleaner vehicle technologies. This shift is propelling the demand for lithium-ion and lead acid batteries, which are essential for hybrid vehicles and auxiliary power systems.

Analysts’ Viewpoint

The global battery market is currently experiencing a transformative phase, driven by technological advancements and evolving consumer demands. Innovations in battery chemistry and design are opening up new avenues for applications across various sectors, including electric vehicles, renewable energy storage, and consumer electronics. As the market expands, there is a significant shift towards more sustainable and efficient energy storage solutions.

Lithium-ion batteries continue to dominate the market due to their high energy density and longer lifecycle compared to traditional battery technologies. However, the rising demand for more environmentally friendly alternatives is accelerating research into solid-state batteries, which offer improved safety and potentially higher energy capacities. This segment is poised for rapid growth, contingent on overcoming current technological and cost barriers.

Battery recycling remains a critical component of the market’s sustainability efforts. With increasing regulatory pressure and consumer awareness, companies are investing in recycling technologies that can recover valuable materials, reduce environmental impact, and decrease reliance on raw material extraction.

Key Takeaways

- battery market is projected to grow from USD 139.9 billion in 2024 to USD 672.5 billion by 2034, at a CAGR of 17.0%.

- Asia Pacific dominated the market with a 47.10% share, generating USD 65.8 billion in revenue.

- Crystalline Silicon was the leading technology with a 64.20% market share, favored for its efficiency and durability.

- Secondary batteries dominated, holding a 78.20% market share due to their rechargeability and widespread use in various applications.

- Lead Acid batteries captured a 38.30% share of the battery technology market, valued for their reliability and cost-effectiveness.

- The Automobile sector held a 45.40% share of the battery market, highlighting the critical role of batteries in the automotive industry, especially in EVs.

By Type Analysis

In 2024, Crystalline Silicon held a dominant market position, capturing more than a 64.20% share of the battery market by technology. This significant market share reflects the widespread adoption of crystalline silicon in various battery applications due to its high efficiency and durability. Manufacturers prefer this technology for its proven performance in both consumer electronics and larger scale energy storage solutions.

As the demand for sustainable and reliable energy solutions continues to rise, crystalline silicon technology is expected to maintain its lead into 2025. This trend is supported by ongoing advancements in material science and manufacturing processes that aim to enhance the efficiency and reduce the costs of crystalline silicon batteries, making them more accessible and appealing to a broader range of consumers and industries.

By Battery Type Analysis

In 2024, Secondary batteries held a dominant market position, capturing more than a 78.20% share of the overall battery market. This type of battery, known for its rechargeability, has become increasingly popular due to its extensive use in consumer electronics, electric vehicles, and renewable energy storage systems.

The robust growth in these sectors has propelled the demand for secondary batteries as they provide efficient energy solutions that can be used repeatedly, reducing waste and overall costs. Looking into 2025, the market for secondary batteries is expected to continue expanding. Innovations in battery technology, such as improvements in energy density and charging speed, are likely to further enhance their attractiveness and utility across various applications.

By Technology Analysis

In 2024, Lead Acid batteries held a dominant market position, capturing more than a 38.30% share of the battery technology market. This enduring popularity stems from their reliability, cost-effectiveness, and well-established recycling processes. Lead Acid batteries are commonly used in automotive starters, uninterruptible power supplies, and emergency lighting systems, where their ability to deliver high surge currents is particularly valuable.

Despite the growth in newer battery technologies, Lead Acid remains a preferred choice in many traditional applications due to its proven track record and ongoing enhancements in battery design and lifespan. Moving into 2025, the market for Lead Acid batteries is expected to remain strong, supported by steady demand in industrial and automotive sectors, and improvements aimed at increasing energy density and reducing environmental impact.

By End-use Analysis

In 2024, the Automobile sector held a dominant market position in the battery market, capturing more than a 45.40% share. This significant stake reflects the growing reliance on batteries within the automotive industry, particularly with the surge in production and adoption of electric vehicles (EVs). Batteries, especially high-capacity, rechargeable types, are crucial for powering modern vehicles, from hybrid models to fully electric cars.

As environmental concerns and fuel economy standards intensify, the demand for efficient and durable batteries in the automobile sector is projected to increase even further into 2025. The ongoing advancements in battery technology, such as enhanced charging times, greater energy densities, and longer lifespans, are expected to bolster this trend, driving broader adoption across the global automotive market.

Key Market Segments

By Type

- Stationary

- Motive

By Battery Type

- Primary

- Secondary

By Technology

- Lead Acid

- Flooded

- VRLA-Gel

- VRLA-AGM

- Lithium Ion

- Lithium Cobalt Oxide

- Lithium Iron Phosphate

- Lithium Manganese Oxide

- Lithium Nickel Cobalt Aluminum Oxide

- Lithium Nickel Manganese Cobalt Oxide

- Others

- Nickel-based

- Solid State Battery

- Single-Layer

- Multi-Layer

- Flow Battery

- Others

By End-use

- Aerospace

- Automobile

- Passenger vehicles

- Commercial vehicles

- Consumer Electronics

- Grid-scale Energy Storage

- Telecom

- Power Tools

- Military & Defense

- Others

Drivers

Increased Demand for Electric Vehicles (EVs)

One major driving factor for the battery market is the rapidly increasing demand for electric vehicles (EVs). According to the International Energy Agency (IEA), global electric car sales doubled in 2021, surpassing 6.6 million units. This surge is a clear indicator of the growing consumer and governmental interest in electric vehicles as a sustainable alternative to combustion engines. Governments worldwide are bolstering this shift through various incentives and regulatory measures.

For instance, the European Union has set ambitious targets to reduce greenhouse gas emissions, with proposals to end the sale of new petrol and diesel cars by 2035. This policy framework significantly fuels the demand for EVs, consequently driving the need for advanced battery technologies capable of longer ranges and faster charging times.

In the United States, the government has introduced tax credits for electric vehicle purchasers under the Inflation Reduction Act of 2022, aiming to make EVs more accessible to a broader population. Additionally, substantial investments are being channeled into charging infrastructure to support this transition, with the U.S. Department of Energy allocating billions of dollars towards enhancing the national charging network.

The combined effect of consumer preferences for more sustainable transportation options and strong legislative support is expected to keep the demand for batteries high. As batteries are a core component of electric vehicles, advancements in this sector are crucial for the EV market’s expansion. Battery manufacturers are responding by investing in new technologies and increasing production capacities to meet the anticipated demand, ensuring that the battery industry remains at the forefront of the energy transition.

Restraints

Supply Chain Constraints Impacting Battery Production

A significant restraining factor for the battery market is the vulnerability of supply chains, particularly for critical raw materials necessary for battery production such as lithium, cobalt, and nickel. These materials are crucial for manufacturing high-performance rechargeable batteries, which are central to the growth of electric vehicles (EVs), renewable energy storage, and portable electronics.

According to the U.S. Department of Energy’s 2020 report on energy storage, the limited supply of these essential minerals and their concentration in specific geographical areas pose significant risks. For instance, more than half of the world’s cobalt supply, a critical component of lithium-ion batteries, comes from the Democratic Republic of Congo. This geographical concentration can lead to supply instability due to political, economic, or social unrest.

The COVID-19 pandemic further exposed these vulnerabilities when it disrupted global supply chains, leading to delays in battery production and increases in raw material costs. As reported by BloombergNEF, the prices of lithium carbonate have more than tripled over the course of 2021 due to supply shortages and surging demand from the battery sector.

Governments and industry players are actively seeking solutions to these challenges. Initiatives like the European Union’s Raw Materials Alliance aim to secure access to critical materials and reduce dependency on single-source countries by fostering local mining activities and promoting recycling technologies. The U.S. has also launched similar strategies, aiming to strengthen domestic supply chains and build reserves of essential minerals.

Growth Opportunity

Renewable Energy Integration Offers Significant Growth Opportunities for Batteries

The integration of renewable energy sources such as solar and wind into the power grid presents a significant growth opportunity for the battery industry. As these renewable sources are inherently intermittent—solar power depends on sunlight, and wind power depends on wind—batteries are essential for storing energy when production exceeds demand and supplying it when demand exceeds production.

According to the International Renewable Energy Agency (IRENA), the total installed capacity of solar and wind energy increased by approximately 200 gigawatts globally in 2020 alone. IRENA projects that to achieve climate goals, by 2030, the world needs to double the installed capacity of renewable energy sources from 2020 levels. This substantial increase in renewable installations will drive the demand for battery systems capable of managing and stabilizing the energy supply from these sources.

Governments worldwide are recognizing this need and are implementing supportive policies and initiatives. For instance, the European Green Deal aims to make Europe climate-neutral by 2050, which includes significant investments in renewable energy and battery storage solutions. The United States, under its Energy Storage Grand Challenge, aims to create and sustain global leadership in energy storage technology, utilization, and exports by 2030.

Trends

Solid-State Batteries: The Next Revolution in Battery Technology

A major trend in the battery industry is the development and impending commercialization of solid-state batteries. This technology promises to dramatically improve the performance and safety of batteries compared to the current lithium-ion technology. Solid-state batteries replace the liquid or gel-form electrolyte with a solid electrolyte, which can lead to higher energy densities, faster charging times, and reduced risk of fires.

As reported by BloombergNEF, research and development in solid-state technology have accelerated, with significant investments from major automotive and tech companies aiming to overcome the challenges of scalability and cost. By 2030, it is expected that solid-state batteries will begin to enter the market in significant numbers, particularly in sectors such as electric vehicles (EVs) and portable electronics, where safety and energy density are paramount.

Government initiatives are also playing a crucial role in supporting this trend. For example, the U.S. Department of Energy has funded multiple projects under its Advanced Research Projects Agency-Energy (ARPA-E) to advance solid-state battery technology. These projects focus on enhancing the conductivity and stability of solid electrolytes and developing innovative manufacturing processes that could lower production costs.

Regional Analysis

In 2024, the Asia-Pacific (APAC) region emerged as a dominating force in the global battery market, holding a significant 47.10% share, valued at approximately USD 65.8 billion. This dominance is primarily driven by the rapid industrialization and expanding consumer electronics sector across major economies such as China, India, and South Korea. China, in particular, stands out as the global leader in battery production and consumption, largely due to its substantial investments in electric vehicle (EV) manufacturing and renewable energy installations.

The region’s commitment to clean energy and technology advancements has fueled a surge in demand for various types of batteries, from lithium-ion to advanced lead-acid. Government initiatives across the region further support this growth through subsidies for EVs, incentives for renewable energy projects, and ambitious targets for reducing carbon emissions. For example, China’s latest Five-Year Plan emphasizes the development of energy storage technologies and aims to significantly increase the production capacity of lithium-ion batteries to maintain its lead in the global market.

Moreover, the strategic establishment of manufacturing hubs and the localization of supply chains in APAC countries enhance their competitive edge, ensuring a steady supply of materials and reduced logistical costs. As the region continues to innovate and invest in battery technology, its market share is expected to expand even further, underpinning APAC’s critical role in shaping the global battery landscape. This robust market presence not only highlights APAC’s pivotal position but also its potential to drive future market trends in the battery industry globally.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

A123 Systems is a leading developer and manufacturer of lithium-ion batteries and systems, primarily serving the transportation, electric grid, and commercial markets. Known for their innovative approach, they focus on delivering high-performance lithium iron phosphate batteries. The company has made significant strides in providing battery solutions that enhance the safety and performance of electric vehicles and energy storage systems.

BSLBATT USA specializes in manufacturing lithium batteries, offering solutions that cater to a range of applications including renewable energy, marine, and industrial equipment. Their products are renowned for reliability and efficiency, focusing on sustainable energy solutions. BSLBATT continues to expand its market presence by leveraging advanced technology and customer-focused innovations.

BYD Company Ltd. is a Chinese multinational firm with a substantial footprint in the battery technology and electric vehicle sectors. As one of the largest battery manufacturers in the world, BYD also produces electric buses, trucks, and monorails, emphasizing its role in promoting sustainable transportation solutions globally.

C&D Technologies Inc. provides high-quality energy storage solutions, focusing on the production of lead-acid batteries. Their products are integral to telecommunications, UPS systems, and other critical backup power applications. C&D Technologies prides itself on reliability and technological innovation to meet diverse market demands.

Top Key Players

- A123 Systems, LLC

- BSLBATT USA

- BYD Company Ltd

- C&D Technologies Inc

- Chaowei Power Holding Ltd.

- Clarios, LLC

- CROWN BATTERY

- Delphi Automotive

- Discover Battery

- East Penn Manufacturing Co.

- EnerSys, Inc.

- Exide Technologies

- Fengfang Co. Ltd

- Johnson Controls Inc

- Panasonic Corporation

- Saft Groupe SA

- Samsung SDI Co

- The Furukawa Battery Co. Ltd.

Recent Developments

A123 Systems showcased its latest advancements, including the introduction of a new Semi-Solid-State Battery (SSSB) with an impressive energy density of 350Wh/kg. This new product, expected to launch in 2024, is part of A123’s strategy to set new standards in battery performance and safety.

In 2024, BYD Company Ltd continued to solidify its position as a powerhouse in the global battery and electric vehicle (EV) markets. With a market share of 17.2%, BYD stood as the second-largest power battery manufacturer, trailing only behind CATL. This represented a significant increase from their previous year’s performance, demonstrating a robust annual growth in their installed battery capacity, which reached 153.7 GWh, up by 37.5% compared to 2023.

BSLBATT USA secured $21 million in Series A financing, a move aimed at expanding its technological capabilities and distribution networks. This funding will also enhance BSLBATT’s focus on worker safety and product performance in various applications, especially in sectors like low-speed vehicles and golf carts.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 139.9 Bn |

| Forecast Revenue (2034) | USD 672.5 Bn |

| CAGR (2025-2034) | 17% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Stationary, Motive), By Battery Type (Primary, Secondary), By Technology (Lead Acid, Lithium Ion, Nickel-based, Solid State Battery, Flow Battery, Others), By End-use (Aerospace, Automobile, Consumer Electronics, Grid-scale Energy Storage, Telecom, Power Tools, Military And Defense, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | A123 Systems, LLC, BSLBATT USA, BYD Company Ltd, C&D Technologies Inc, Chaowei Power Holding Ltd., Clarios, LLC, CROWN BATTERY, Delphi Automotive, Discover Battery, East Penn Manufacturing Co., EnerSys, Inc., Exide Technologies, Fengfang Co. Ltd, Johnson Controls Inc, Panasonic Corporation, Saft Groupe SA, Samsung SDI Co, The Furukawa Battery Co. Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |