Quick Navigation

Report Overview

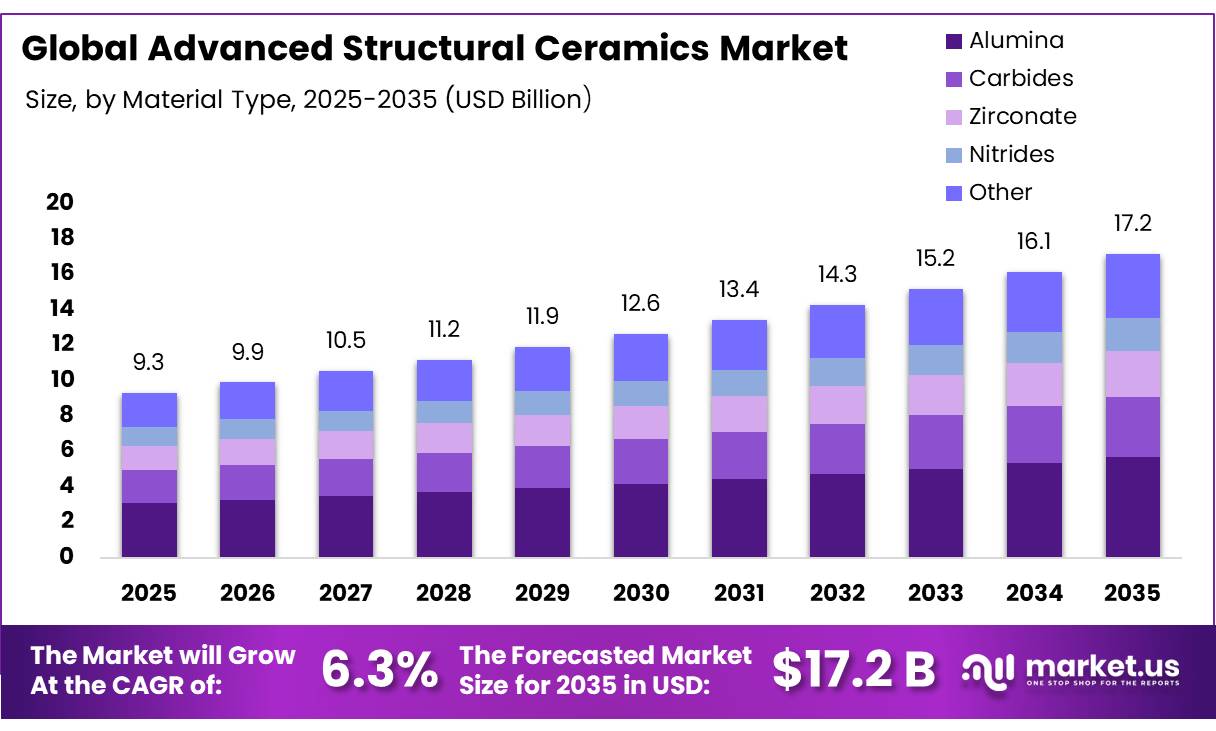

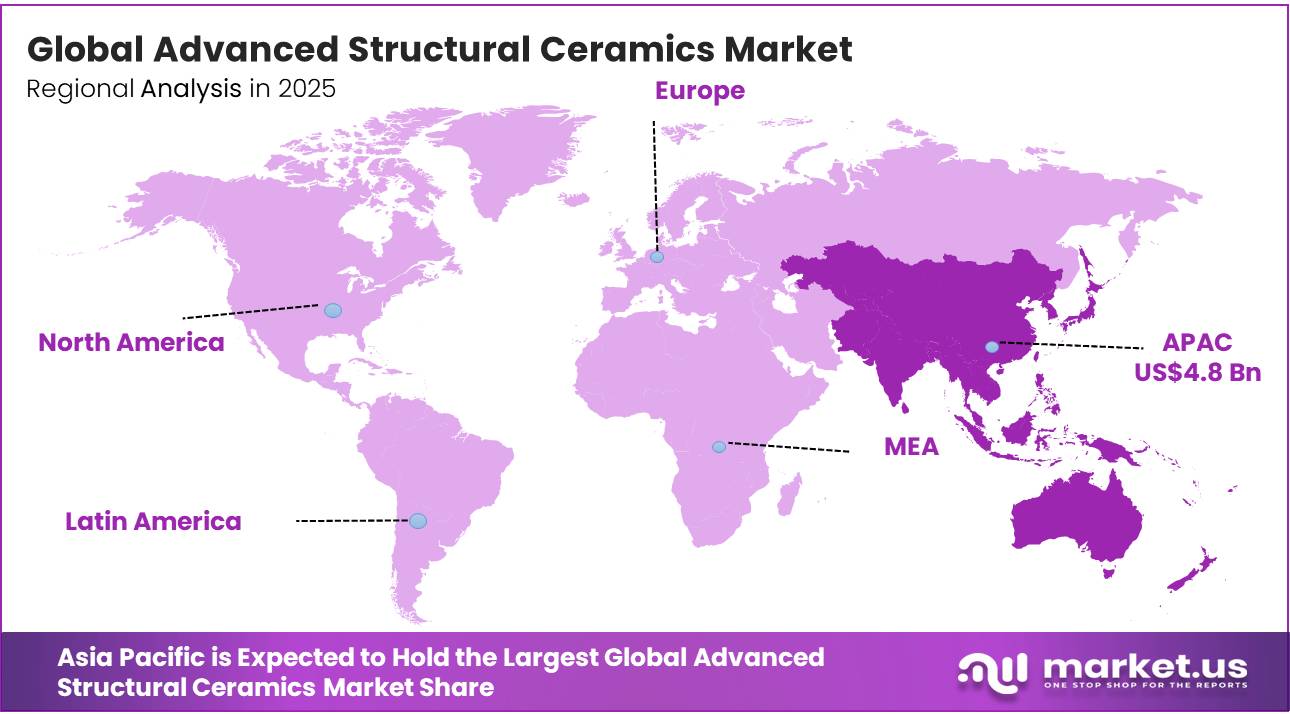

The Global Advanced Structural Ceramics Market size is expected to be worth around USD 17.2 Billion by 2035, from USD 9.3 Billion in 2025, growing at a CAGR of 6.3% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 51.3% share, holding USD 4.8 Billion revenue.

Advanced structural ceramics comprise a class of high-performance inorganic materials engineered to deliver superior mechanical strength, thermal stability, and resistance to wear, corrosion, and chemical degradation. Key material types such as alumina, carbides, zirconates, and nitrides are widely utilized in applications where conventional materials fail under extreme operating conditions. Their combination of low density, high hardness, and ability to maintain structural integrity at elevated temperatures makes them essential across high-performance industrial environments.

Demand patterns are closely aligned with the evolution of advanced manufacturing and high-technology sectors. Industrial applications account for a significant share of usage, particularly in cutting tools, wear-resistant components, and high-temperature processing equipment. Semiconductor and electronics manufacturing further represents a critical demand base, where ceramics are used in wafer processing equipment, insulating substrates, and thermal management systems requiring high purity and dimensional stability. In automotive and energy sectors, increasing electrification and efficiency requirements are further driving adoption in components exposed to thermal and mechanical stress.

Technological progress in nano-engineering, composite ceramics, and precision manufacturing is expanding the performance envelope of these materials, addressing limitations such as brittleness and processing complexity. At the same time, supply chain considerations and high production costs remain key constraints. Regionally, Asia Pacific dominates due to its strong manufacturing ecosystem and concentration of electronics and industrial production, reinforcing its central role in global demand and supply dynamics.

Key Takeaways

- The global advanced structural ceramics market was valued at USD 9.3 billion in 2025.

- The global advanced structural ceramics market is projected to grow at a CAGR of 6.3% and is estimated to reach USD 17.2 billion by 2035.

- Based on the material types of advanced structural ceramics, alumina dominated the advanced structural ceramics market, with a market share of around 32.8%.

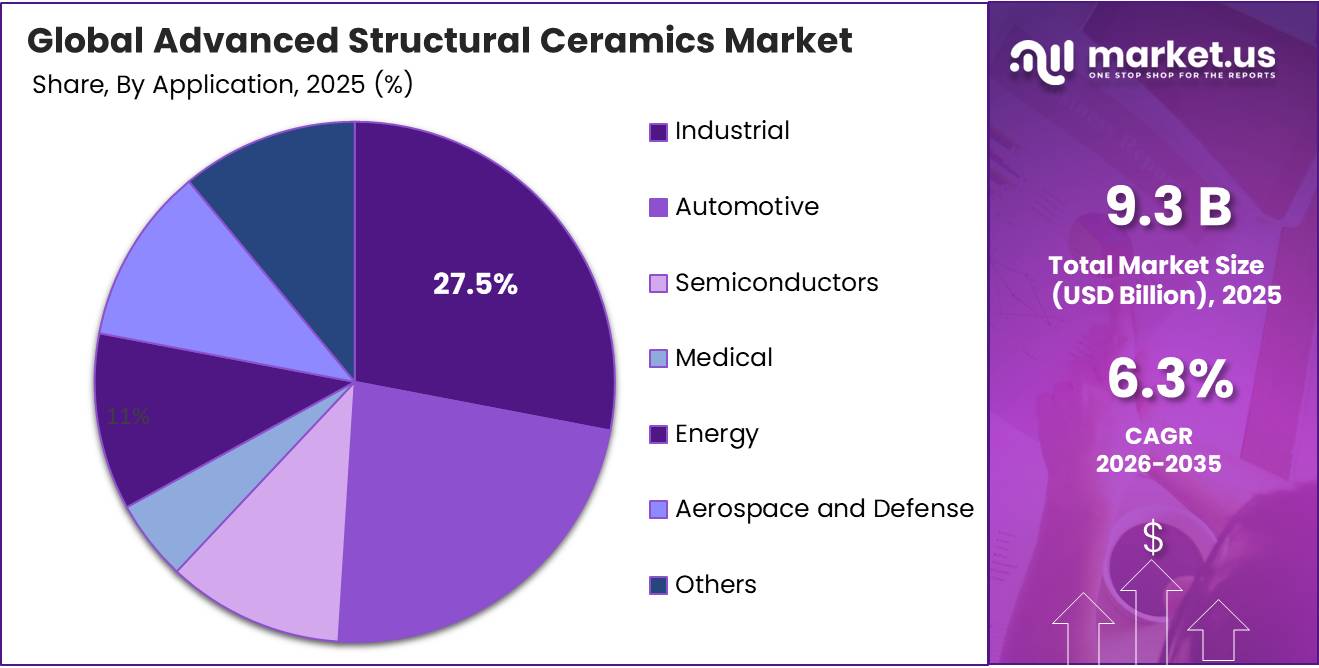

- Among the applications of advanced structural ceramics, industrial applications held a major share in the market, 27.5% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the advanced structural ceramics market, accounting for around 51.3% of the total global consumption.

Material Type Analysis

Alumina Held the Largest Share in the Advanced Structural Ceramics Market.

Alumina holds a leading position within the advanced structural ceramics material landscape, comprising around 32.8% of the market share, due to its strong balance of mechanical performance, thermal resistance, and economic viability. Its widespread usage is supported by mature processing technologies and a stable supply chain, enabling consistent production at scale.

The material’s high hardness, wear resistance, and ability to withstand moderate-to-high temperatures make it suitable for demanding operational environments across multiple industries. Similarly, its electrical insulating properties combined with strong chemical stability drive extensive use in electronic substrates, semiconductor equipment components, and precision insulating parts.

Its relatively lower cost compared to other advanced ceramics further strengthens its adoption across high-performance and cost-sensitive applications. Furthermore, ongoing improvements in powder processing and sintering technologies continue to enhance product quality and consistency, supporting broader integration into automotive, electronics, and select energy applications.

Application Analysis

Advanced Structural Ceramics Are Mostly Utilized in Industrial Applications.

Industrial applications represent the leading demand segment within the advanced structural ceramics market, with a market share of 27.5%, driven by the extensive use of high-performance materials in environments characterized by continuous mechanical stress, abrasion, and chemical exposure. These materials are widely integrated into equipment and systems where operational reliability and extended service life are critical, particularly in heavy machinery, manufacturing tools, and process industries.

The segment’s dominance is further supported by increasing automation and modernization of industrial infrastructure, which has heightened the demand for durable and precision-engineered components. Similarly, continuous improvements in manufacturing technologies have enhanced the cost-efficiency and scalability of ceramic-based solutions, reinforcing their adoption across diverse industrial environments.

Key Market Segments

By Material Type

- Alumina

- Carbides

- Zirconate

- Nitrides

- Other

By Application

- Automotive

- Semiconductors

- Medical

- Energy

- Industrial

- Aerospace and Defense

- Others

Drivers

Intensifying Need for Structural Materials with Superior Performance Under Extreme Operating Conditions.

Escalating performance requirements across aerospace propulsion, energy systems, semiconductor fabrication, and high-temperature industrial processing are reinforcing the need for materials capable of sustaining extreme operating conditions without degradation. Advanced structural ceramics are increasingly preferred due to their ability to maintain mechanical integrity at temperatures significantly exceeding those of conventional metals.

Certain advanced ceramics can operate at temperatures up to 2200°C, whereas most engineering metals begin to lose structural stability or melt between 1200°C and 1500°C, establishing a clear performance differential in high-temperature environments. This capability is critical in applications such as gas turbines, hypersonic vehicles, and nuclear systems, where materials are exposed to simultaneous thermal, mechanical, and chemical stresses.

For instance, silicon nitride-based ceramics have demonstrated the ability to retain high strength at 1400°C, with some engineered grades achieving up to 2.8 times higher strength compared to conventional variants under similar conditions. The advanced ceramics can sustain high stress rates up to 33,000 MPa/sec at elevated temperatures while maintaining strength levels comparable to room-temperature performance.

Similarly, emerging applications such as hypersonic flight and next-generation nuclear technologies require materials that can withstand temperatures exceeding 2000°C alongside oxidation and corrosive exposure, further intensifying reliance on carbide- and nitride-based ceramic systems. This convergence of extreme thermal, mechanical, and chemical demands continues to position advanced structural ceramics as indispensable materials in next-generation high-performance systems.

Restraints

High Processing Complexity and Manufacturing Costs Limit Wider Adoption of Advanced Structural Ceramics.

High processing complexity and manufacturing costs continue to constrain the broader adoption of advanced structural ceramics, reflecting the precision-intensive and energy-demanding nature of their production. Fabrication typically involves high-purity powder synthesis, controlled shaping, and sintering at temperatures often exceeding 1,600°C. These requirements increase energy consumption and impose strict process controls to avoid defects such as porosity or microcracking.

Material losses during machining further elevate costs, as ceramics often require post-sintering finishing using diamond tools due to their extreme hardness. The Oak Ridge National Laboratory has highlighted that achieving near-net-shape manufacturing remains challenging, particularly for complex geometries, leading to higher rejection rates and extended production cycles. Additionally, high-purity inputs such as alumina and silicon carbide demand tightly controlled supply chains, adding procurement complexity. These combined factors limit scalability, particularly in cost-sensitive applications, and necessitate continuous process optimization to improve yield, reduce waste, and enhance manufacturing efficiency.

Opportunity

Strengthening Semiconductor and Electronics Ecosystems: Enhancing Application Scope for Advanced Structural Ceramics.

Strengthening semiconductor and electronics ecosystems is materially expanding the application scope for advanced structural ceramics, particularly in high-precision fabrication environments. Semiconductor manufacturing processes require materials with ultra-high purity, dimensional stability, and resistance to plasma, chemicals, and thermal stress. Ceramic components are integral to wafer fabrication stages, including deposition, etching, lithography, and chemical mechanical planarization, where they ensure process consistency and yield stability.

The increasing complexity of semiconductor nodes is intensifying material performance requirements. Fabrication at advanced nodes involves temperatures exceeding 1200°C, plasma densities reaching 10¹² ions/cm², and dimensional tolerances within ±2 micrometers, necessitating the use of high-performance ceramics such as alumina, aluminum nitride, and silicon carbide. These materials must meet purity thresholds above 99.9%, reinforcing their role as critical enabling components in semiconductor equipment.

In parallel, electronics miniaturization and the transition toward high-power devices such as silicon carbide and gallium nitride systems are increasing reliance on ceramics capable of operating under higher thermal loads and power densities. These structural shifts collectively position advanced ceramics as indispensable materials within expanding semiconductor and electronics manufacturing ecosystems.

Trends

Development of Nano-Engineered and Composite Ceramic Systems.

Advancements in nano-engineered and composite ceramic systems are increasingly redefining performance thresholds of structural ceramics by addressing long-standing limitations related to brittleness and fracture resistance. The incorporation of nano-scale reinforcements into ceramic matrices can significantly enhance mechanical properties. For instance, the addition of silicon oxycarbonitride (SiCNO) phases into alumina matrices has shown up to 151% improvement in flexural strength and over 34% increase in compressive strength, highlighting the measurable impact of nanoscale engineering on structural performance.

Material design approaches are progressively shifting toward multi-phase and nanostructured architectures, where nanoparticles, fibers, or carbon-based nanofillers such as carbon nanotubes are embedded within ceramic matrices to improve toughness, stiffness, and thermal stability. A majority of nanocomposite research, approximately 88% of reported studies, utilizes multi-walled carbon nanotubes as reinforcement, reflecting a strong directional focus in nano-engineering strategies. These approaches are aimed at overcoming the intrinsic brittleness of monolithic ceramics while preserving their high-temperature and corrosion-resistant properties.

These developments are enabling broader deployment of advanced ceramics in high-stress environments such as aerospace propulsion, semiconductor fabrication, and energy systems, where enhanced durability, thermal stability, and reliability are critical performance requirements.

Geopolitical Impact Analysis

Geopolitical Fragmentation and Supply Chain Realignment Reshaping the Advanced Structural Ceramics Value Chain.

Geopolitical tensions have introduced a structural layer of supply chain fragility across the advanced structural ceramics value chain, primarily through export controls, critical mineral restrictions, and regional trade realignments. Advanced ceramics rely heavily on high-purity inputs such as alumina, silicon carbide, and silicon nitride precursors, many of which are concentrated in limited geographies. The export licensing requirements and trade restrictions on critical minerals have tightened since 2023, contributing to higher procurement uncertainty and extended lead times for industrial ceramic components used in semiconductor and high-temperature applications.

Semiconductor manufacturing, a key downstream consumer of structural ceramics, has experienced intensified trade restrictions on tools, chips, and materials across major economies, reinforcing regional segmentation of supply chains. Government-led export control frameworks targeting advanced semiconductor equipment and dual-use technologies have indirectly affected ceramic demand cycles by constraining equipment expansion and altering fab localization strategies. This has increased reliance on domestic or allied sourcing for precision ceramic parts used in wafer processing chambers, insulating substrates, and thermal management systems.

Industrial end-users are responding through inventory buffering, supplier diversification, and regionalized procurement strategies, particularly in electronics and energy sectors where continuity of operations is critical. These adjustments are gradually reshaping procurement architectures, with increased emphasis on supply chain redundancy and localized manufacturing ecosystems for ceramic components used in extreme environment applications.

Regional Analysis

Asia Pacific Maintains the Largest Share in the Global Advanced Structural Ceramics Market.

The Asia Pacific represents the dominant regional market for advanced structural ceramics, holding about 51.3% of the total global consumption, supported by a strong manufacturing base, rapid industrialization, and expanding high-technology sectors. The region benefits from the presence of large-scale production ecosystems across electronics, automotive, energy, and industrial machinery, which collectively drive sustained demand for high-performance ceramic materials.

Additionally, countries such as China, Japan, South Korea, and India play a central role in consumption and production, with established capabilities in materials engineering and precision manufacturing. Similarly, the strong semiconductor and electronics manufacturing footprint in the region significantly contributes to the adoption of advanced structural ceramics, particularly in wafer processing equipment, insulating components, and thermal management systems.

- According to the Semiconductor Industry Association (SIA), year-to-year sales in August 2025 were up in the Asia Pacific (43.1%), contributing to the demand for advanced structural ceramics.

Furthermore, favorable government initiatives promoting advanced manufacturing, combined with increasing investments in high-value industries, are further strengthening regional growth. The availability of skilled labor and cost-effective production capabilities enhances the competitiveness of the Asia Pacific as a key hub in the global advanced structural ceramics value chain.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of advanced structural ceramics concentrate on strengthening material innovation, process optimization, and application-specific engineering. Significant emphasis is placed on developing high-purity powders, refining sintering techniques, and enhancing microstructural control to improve toughness, thermal stability, and wear resistance. Companies further invest in precision machining and near-net-shape manufacturing to reduce material waste and improve cost efficiency while enabling complex geometries for high-performance applications.

Strategic collaboration with end-use industries such as semiconductor equipment, automotive systems, and aerospace engineering supports the co-development of customized ceramic components tailored to specific operational environments. Expansion of production capacity in proximity to high-demand industrial clusters helps improve supply chain responsiveness and reduce lead times. Additionally, manufacturers focus on integrating advanced ceramics with composite and hybrid material systems to expand functional capabilities and diversify application portfolios across demanding industrial and electronic environments.

The Major Players in The Industry

- 3M Company

- Advanced Ceramics Manufacturing

- Blasch Precision Ceramics, Inc.

- CeramTec GmbH

- CoorsTek, Inc.

- Ferrotec Holdings Corporation

- KYOCERA Corporation

- Materion Corporation

- Maxon

- Morgan Advanced Materials plc

- Murata Manufacturing Co., Ltd.

- Nishimura Advanced Ceramics Co., Ltd.

- Ortech Advanced Ceramics

- Paul Rauschert GmbH and Co. KG

- Saint-Gobain

- Schunk Group

- Lucideon

- Other Key Players

Key Development

- In April 2026, Hydra Manufacturing and Lucideon announced a collaboration to accelerate the development of advanced ceramic additive manufacturing (AM) solutions.

- In March 2026, a memorandum of understanding was signed between Oak Ridge National Laboratory and General Atomics Electromagnetic Systems (GA-EMS) with the objective of collaborating on advanced ceramic matrix composite materials for applications in extreme environments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$9.3 Bn |

| Forecast Revenue (2035) | US$17.2 Bn |

| CAGR (2025-2035) | 6.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2021-2024 |

| Forecast Period | 2025-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Application (Alumina, Carbides, Zirconate, Nitrides, and Other), By Application (Automotive, Semiconductors, Medical, Energy, Industrial, Aerospace and Defense, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | 3M Company, Advanced Ceramics Manufacturing, Blasch Precision Ceramics, Inc., CeramTec GmbH, CoorsTek, Inc., Ferrotec Holdings Corporation, KYOCERA Corporation, Materion Corporation, Maxon, Morgan Advanced Materials plc, Murata Manufacturing Co., Ltd., Nishimura Advanced Ceramics Co., Ltd., Ortech Advanced Ceramics, Paul Rauschert GmbH and Co. KG, Saint-Gobain, Schunk Group, Lucideon, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |