Quick Navigation

Report Overview

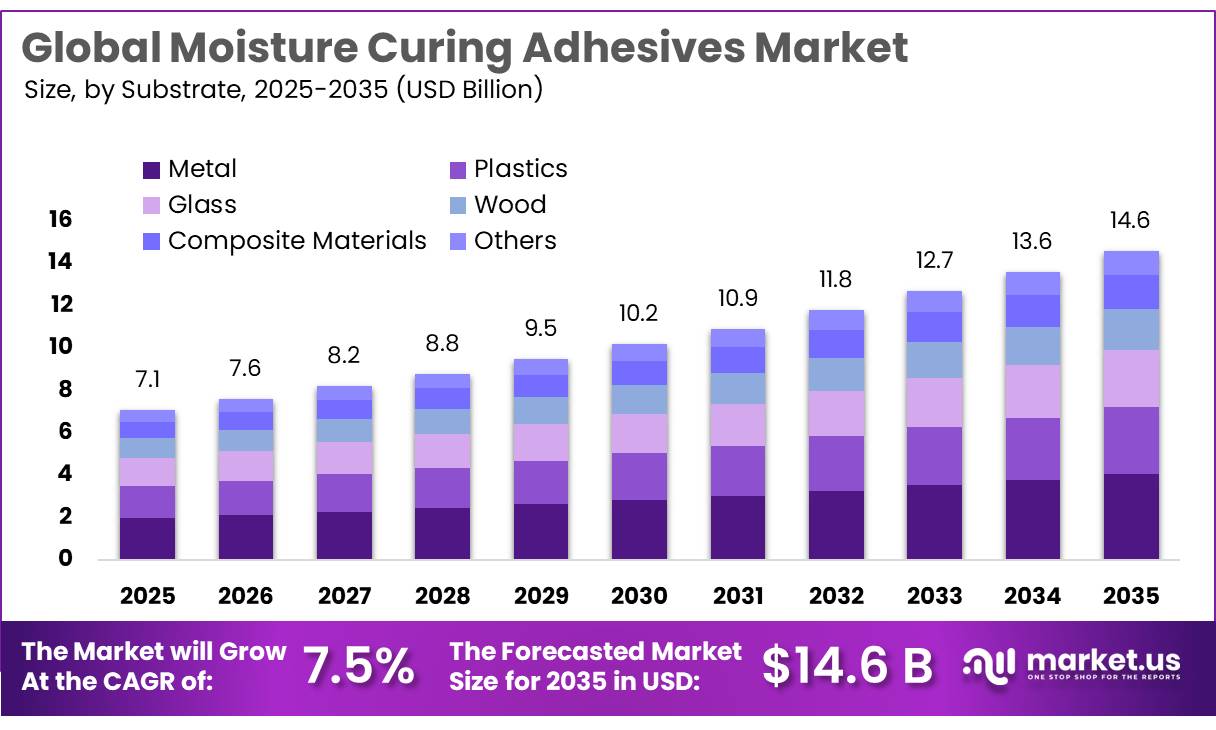

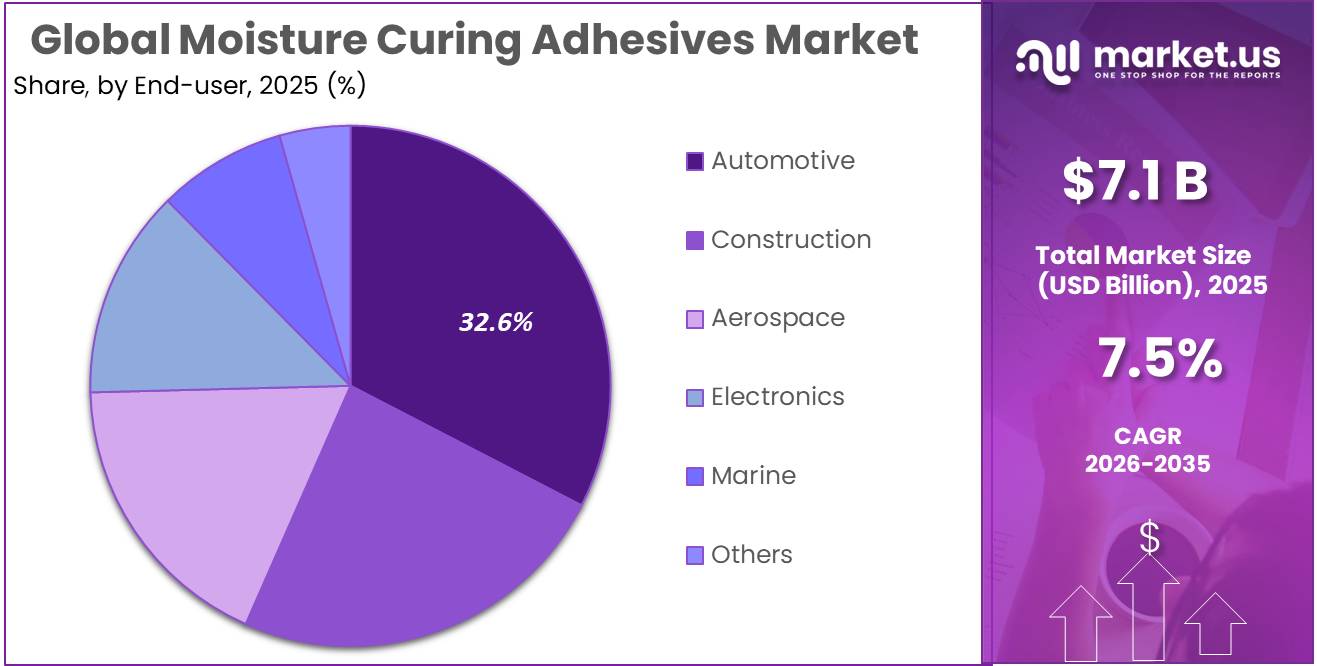

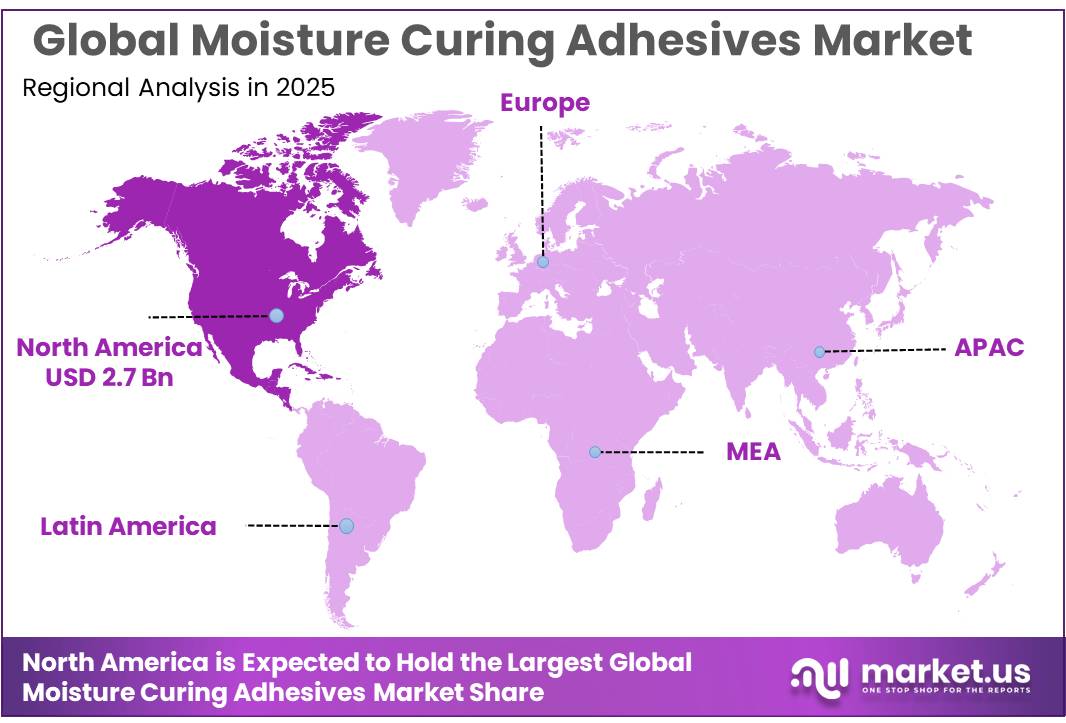

The Global Moisture Curing Adhesives Market size is expected to be worth around USD 14.6 Billion by 2035, from USD 7.1 Billion in 2025, growing at a CAGR of 7.5% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 39.3% share, holding USD 2.7 Billion revenue.

Moisture curing adhesives are one-component systems that cure by reacting with atmospheric or substrate moisture, making them valuable in construction, automotive, electronics, flexible packaging, footwear, woodworking and general assembly. In food packaging, indirect-contact adhesive use remains regulated; the U.S. FDA’s 21 CFR 175.105 allows adhesives where food contact is limited to trace exposure under good manufacturing practice, while EU food-contact rules require packaging not to endanger health or alter food quality.

The industrial scenario is strongest in construction, automotive, electronics, woodworking, appliances, and packaging-related assembly. In the United States, construction spending reached an annualized $2,152.4 billion in April 2025, while public highway construction alone stood at $146.3 billion, supporting demand for sealants, panels, flooring, insulation, and façade bonding. In Europe, construction represents about 9% of EU GDP, employs over 18 million people directly, and supports another 25 million workers, creating a large base for sustainable adhesive technologies.

Driving factors include VOC reduction, lower-energy curing, flexible bonding, and regulatory compliance. The U.S. EPA’s VOC standards are estimated to reduce VOC emissions by 90,000 tons per year, encouraging manufacturers to develop lower-emission adhesive and sealant technologies. The U.S. FDA also identifies adhesives as examples of substances applied to packaging surfaces that may fall under food-contact substance rules.

The European Commission’s Renovation Wave targets renovation of 35 million buildings by 2030, while EU packaging rules require all packaging to be recyclable by 2030, encouraging lower-emission, design-for-recycling bonding systems. Automotive electrification is another key driver. The IEA reported that global electric car sales exceeded 17 million in 2024, represented more than 20% of new car sales, and are expected to top 20 million in 2025, equal to over one-quarter of global car sales. These trends support moisture-curing adhesives in lightweight bonding, display assemblies, glazing, battery-adjacent sealing, and mixed-material joining.

Regulation is pushing the sector toward low-VOC, safer and lower-monomer technologies. In Europe, professional and industrial users of products containing more than 0.1% monomeric diisocyanates must complete training from 24 August 2023, influencing polyurethane adhesive formulation and handling practices. In the U.S., EPA’s Safer Choice program promotes products using ingredients safer for human health and the environment.

Company activity reinforces the outlook. In 2025, 3M’s updated PUR Easy 250 Wood Adhesive documentation highlighted warm-applied, moisture-curing urethane chemistry for bonding plastics and wood to metal and glass, with peel adhesion values up to 137 N/cm on glass and elongation at break of 400%.

Key Takeaways

- Moisture Curing Adhesives Market size is expected to be worth around USD 14.6 Billion by 2035, from USD 7.1 Billion in 2025, growing at a CAGR of 7.5%.

- Polyurethane Adhesives held a dominant market position, capturing more than a 45.2% share.

- Metal held a dominant market position, capturing more than a 27.8% share.

- Automotive held a dominant market position, capturing more than a 32.6% share.

- North America holds a leading position in the moisture curing adhesives market, accounting for 39.3% share with a value of USD 2.7 billion.

By Type Analysis

Polyurethane Adhesives lead with 45.2% as they offer strong bonding and flexibility across industries

In 2025, Polyurethane Adhesives held a dominant market position, capturing more than a 45.2% share. This strong position comes from their ability to provide durable bonding across a wide range of materials such as wood, metal, plastics, and composites. These adhesives are widely used in construction, automotive, and packaging because they can handle stress, moisture, and temperature changes without losing strength. Their flexibility also makes them suitable for applications where materials expand or move over time, which is common in real-world conditions.

By Substrate Analysis

Metal segment leads with 27.8% as industries rely on strong and durable bonding for heavy-duty use

In 2025, Metal held a dominant market position, capturing more than a 27.8% share. This leadership comes from the growing need for strong and long-lasting bonding solutions in industries like automotive, construction, and machinery. Moisture curing adhesives work well with metal surfaces because they provide high strength, resist corrosion, and perform reliably under tough conditions such as heat, pressure, and moisture. These features make them a preferred choice where welding or mechanical fastening may not be ideal or cost-effective.

By End user Analysis

Automotive leads with 32.6% as demand grows for strong and lightweight bonding solutions

In 2025, Automotive held a dominant market position, capturing more than a 32.6% share. This strong demand comes from the increasing use of moisture curing adhesives in vehicle manufacturing, where reliable bonding is needed for metals, plastics, and composite materials. These adhesives help improve vehicle strength while also supporting lightweight designs, which is important for better fuel efficiency and performance. They are widely used in areas like body panels, interiors, and structural components, offering durability and resistance to vibration, heat, and moisture.

Key Market Segments

By Type

- Polyurethane Adhesives

- Silicone Adhesives

- Hybrid Adhesives

- Others

By Substrate

- Metal

- Plastics

- Glass

- Wood

- Composite Materials

- Others

By End user

- Automotive

- Construction

- Aerospace

- Electronics

- Marine

- Others

Emerging Trends

Shift Toward Sustainable and Low-Waste Packaging is Emerging as a Key Trend

One of the most important trends in moisture curing adhesives is the growing shift toward sustainable packaging, especially in the food industry. The scale of food waste is pushing this change. According to the United Nations Environment Programme, around 1.05 billion tonnes of food were wasted in 2022, which equals nearly 19% of food available to consumers. This has made governments and industries rethink how materials like adhesives are used in packaging.

Moisture curing adhesives are now being redesigned to support recyclable and low-waste packaging formats. Governments are also backing this transition through global targets like SDG 12.3, which aims to reduce food waste by half by 2030. In 2025–2026, food packaging companies are focusing on adhesives that not only provide strong bonding but also help reduce leakage, improve shelf life, and support recycling processes.

Increasing Focus on Shelf Life Extension and Cold Chain Efficiency

Another key trend is the growing use of moisture curing adhesives to improve shelf life and support cold chain systems. A large amount of food is still lost before it even reaches consumers. Around 13% of food is lost in the supply chain before retail, mainly due to poor storage and handling conditions. This has pushed industries to improve packaging strength and sealing performance, where adhesives play a critical role.

Moisture curing adhesives are being widely used in flexible packaging, multilayer films, and sealed containers to protect food from moisture and contamination. This helps maintain freshness during transportation, especially in long-distance supply chains. Governments and organizations like FAO are encouraging better cold chain infrastructure to reduce these losses.

Drivers

Rising demand from packaging and food industries is driving moisture curing adhesives growth

One of the major driving factors for moisture curing adhesives is the strong growth of the packaging and food industry, where adhesives play a critical role in maintaining product safety and shelf life. In practical terms, adhesives are used in more than 80% of food packaging applications, showing how essential they are in sealing, labeling, and protecting products during transport. This widespread usage directly supports the demand for moisture curing adhesives, as they offer strong bonding and resistance to humidity, which is important for food storage.

The packaging sector alone accounts for nearly 40% of total adhesive consumption globally, making it the largest application area. As food consumption and packaged goods continue to rise, especially in urban areas, the need for reliable and durable adhesives is also increasing. Governments and food safety organizations like the Food and Agriculture Organization emphasize proper packaging to reduce food loss and improve product quality.

Infrastructure and construction growth backed by government spending is boosting demand

Another strong driving factor is the rapid growth of construction and infrastructure activities worldwide. Governments are investing heavily in housing, roads, and public infrastructure, which directly increases the demand for strong and durable adhesives. For example, the global construction sector has already crossed USD 4.5 trillion in value, highlighting its massive scale and continuous expansion.

Moisture curing adhesives are widely used in construction for bonding wood, metal, tiles, and insulation materials because they offer high strength and resistance to water and environmental conditions. They are especially useful in applications like flooring, roofing, and structural bonding, where durability is critical. Government initiatives such as smart city projects and affordable housing programs in countries like India and China are further accelerating this demand.

Restraints

Safety and Migration Risks in Food Packaging Limit Adoption

One major restraining factor for moisture curing adhesives is the risk of chemical migration when used in food packaging applications. Adhesives are widely used in packaging—more than 80% of food packaging contains adhesives in some form. However, when these adhesives come in contact with food layers, there is a concern that certain compounds can transfer into the food. A detailed study on packaging materials found that out of 55 chemical compounds identified in adhesives, nearly 57% showed migration into food simulants.

This creates a serious safety challenge for manufacturers. Food safety authorities and governments have strict rules on what materials can be used in packaging. If there is even a small risk of contamination, companies must invest heavily in testing and compliance. This increases both cost and time to market. In 2025–2026, regulatory bodies continue to tighten norms around food-contact materials, especially in Europe and North America.

Strict Environmental Regulations and VOC Limits Creating Barriers

Another important restraint comes from increasing environmental regulations related to chemical emissions and sustainability. Governments across the world are focusing on reducing volatile organic compounds (VOCs) and promoting safer materials in industrial applications. Moisture curing adhesives, especially solvent-based types, can sometimes fall under regulatory scrutiny due to emission concerns. This becomes more critical in packaging, which is one of the largest users of adhesives, accounting for nearly 40% of total adhesive consumption globally

At the same time, the packaging industry itself is under pressure to become more sustainable. Regulations are pushing companies to move toward recyclable, biodegradable, or low-emission materials. This creates a challenge for adhesive manufacturers, as they must redesign products while maintaining performance. In 2025 and 2026, industries are facing a balancing act—meeting strict environmental rules while keeping costs under control.

Opportunity

Rapid growth in food packaging and e-commerce is creating strong future demand

One of the biggest growth opportunities for moisture curing adhesives comes from the fast expansion of the food packaging and e-commerce sectors. Packaging is already the largest application area for adhesives, accounting for nearly 40% of total adhesive use globally. At the same time, the global packaging adhesives market is expected to reach around USD 14.6 billion in 2025, showing how strong the demand base already is. This growth is closely linked to the rising consumption of packaged food and the need for safe, sealed, and long-lasting packaging.

Food organizations such as the Food and Agriculture Organization highlight that proper packaging plays a key role in controlling moisture and extending shelf life, which directly increases the need for reliable adhesive solutions. Moisture curing adhesives are especially useful here because they perform well in humid conditions and help maintain package integrity. With global plastic packaging usage crossing 150 million tonnes annually, the scale of opportunity becomes even clearer.

Infrastructure expansion and industrial growth are opening new application areas

Another strong opportunity lies in the growth of infrastructure and industrial development worldwide. Governments across emerging economies are investing heavily in housing, transportation, and smart city projects, which require durable bonding materials. Moisture curing adhesives are well suited for these applications because they provide strong adhesion to materials like wood, metal, and concrete while resisting moisture and environmental stress.

The packaging sector alone is expected to grow further, reaching around USD 17.6 billion in 2026, reflecting continued expansion driven by e-commerce and manufacturing demand. Additionally, the rise of over 2.7 billion online consumers globally is increasing the need for secure packaging and logistics solutions. Governments are encouraging the use of long-lasting and sustainable materials in construction and manufacturing, which supports the use of advanced adhesive systems.

Regional Insights

North America dominates with 39.3% share valued at USD 2.7 Bn driven by strong industrial and packaging demand

North America holds a leading position in the moisture curing adhesives market, accounting for 39.3% share with a value of USD 2.7 billion, supported by its well-established industrial base and steady demand from key sectors such as construction, automotive, and packaging.

The region benefits from a mature adhesives industry, with the broader adhesives and sealants market reaching around USD 16.02 billion in 2025, showing a strong foundation for advanced adhesive technologies. The United States plays a central role, contributing the majority of regional demand due to its large-scale manufacturing and infrastructure activities.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

3M is a well-established player in moisture curing adhesives, supported by its strong materials science and adhesive technologies portfolio. In 2025, the company reported total revenue of USD 24.9 billion, reflecting a 1.5% year-on-year growth, with an operating margin of 18.6%. Its adhesives segment benefits from continuous innovation and integration into automotive, construction, and industrial applications. The company’s consistent R&D investment and global presence across 70+ countries help strengthen its role in advanced bonding solutions.

Henkel is one of the leading adhesive manufacturers globally, with a strong footprint in moisture curing technologies. In 2025, the company recorded total sales of €20,495 million, despite a -5.1% decline due to market conditions. Its Adhesive Technologies segment remains a major revenue contributor, supporting industries such as packaging, automotive, and electronics. Henkel’s focus on high-performance and sustainable adhesive solutions positions it well in the evolving market landscape through 2026.

Sika AG plays a key role in construction and industrial adhesives, including moisture curing systems. In 2025, the company generated sales of CHF 11,201.3 million, showing a -4.8% year-on-year change in a challenging market environment. Despite this, Sika maintains strong demand in infrastructure and construction sectors, where durable bonding is essential. Its global operations and product innovation help expand its presence in high-performance adhesives, particularly for structural and weather-resistant applications.

Top Key Players Outlook

- 3M

- Henkel AG & Co. KGaA

- Sika AG

- Bostik (Arkema Group)

- H.B. Fuller Company

- Dow Inc.

- Illbruck

- M and Henkel AG & Co. KGaA

Recent Industry Developments

In 2026, Henkel expects organic sales growth of 1.0% to 3.0%, with its Adhesive Technologies unit projected to maintain margins between 16.5% and 18.0%, showing confidence in its core industrial adhesive business.

In 2026, Sika expects moderate growth of around 1% to 4% in local currencies, supported by infrastructure demand and product innovation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 7.1 Bn |

| Forecast Revenue (2035) | USD 14.6 Bn |

| CAGR (2026-2035) | 7.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Polyurethane Adhesives, Silicone Adhesives, Hybrid Adhesives, Others), By Substrate (Metal, Plastics, Glass, Wood, Composite Materials, Others), By End user (Automotive, Construction, Aerospace, Electronics, Marine, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | 3M, Henkel AG & Co. KGaA, Sika AG, Bostik (Arkema Group), H.B. Fuller Company, Dow Inc., Illbruck, M and Henkel AG & Co. KGaA |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |