Quick Navigation

Report Overview

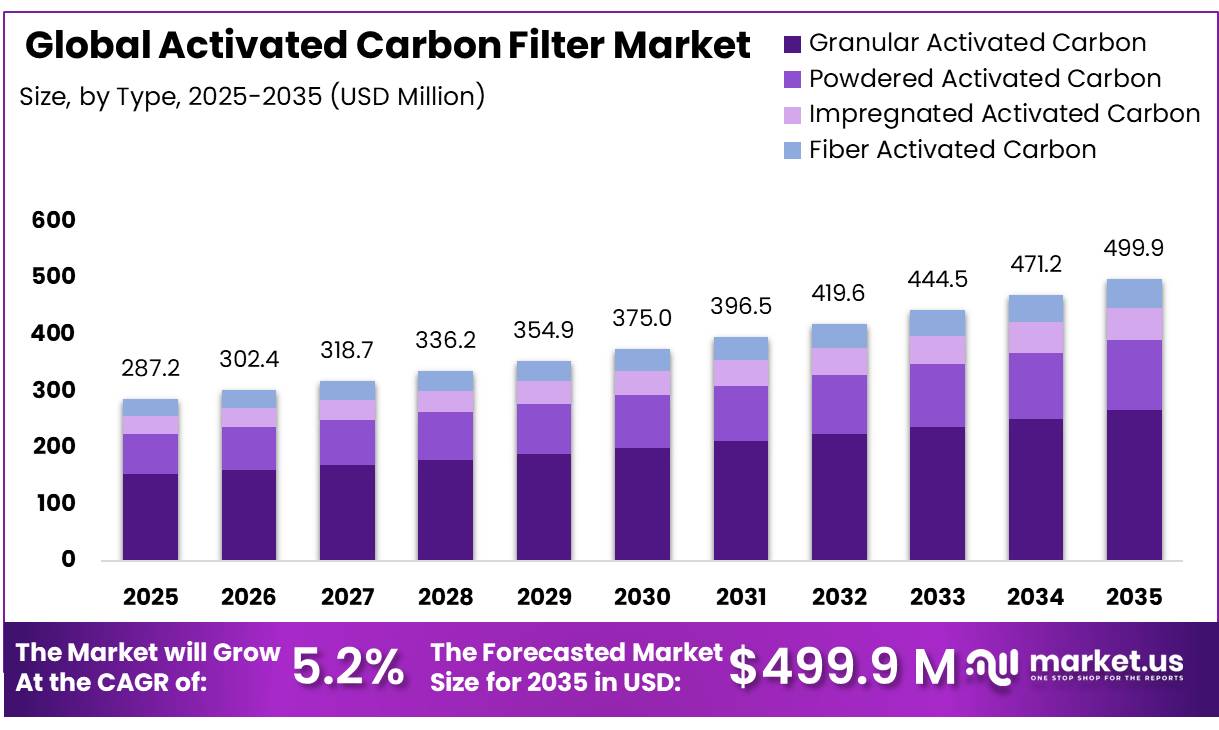

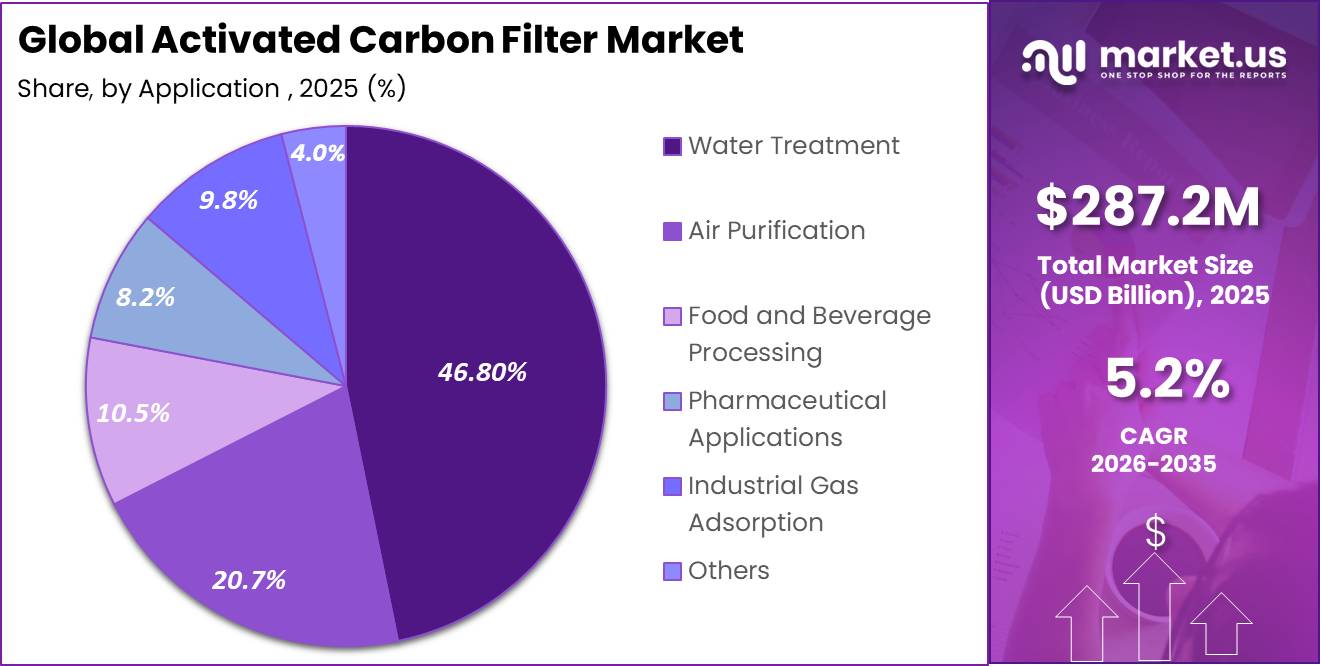

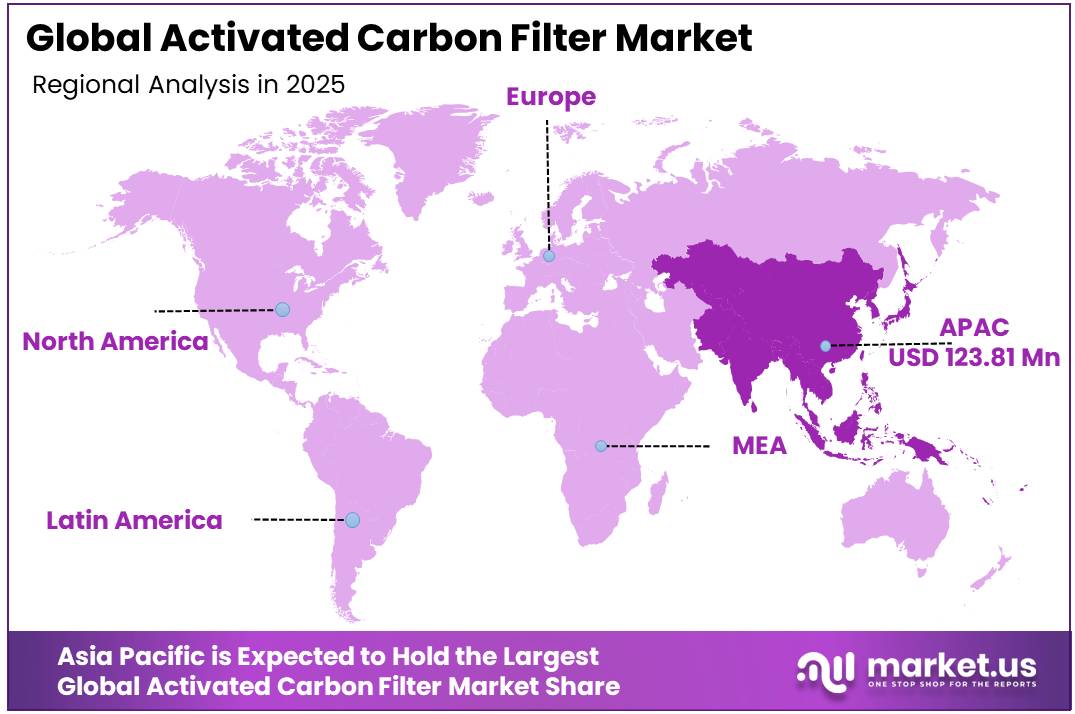

In 2025, the Global Activated Carbon Filter Market was valued at USD 287.2 Million, and between 2026 and 2035, this market is estimated to register a CAGR of 5.2%, reaching about USD 499.9 Million by 2035. Asia Pacific held a dominant market position, capturing more than a 43.1% share, holding USD 123.81 billion in revenue.

The activated carbon filter industry covers adsorption systems used in municipal water treatment, industrial wastewater, air purification, food processing, pharmaceutical production, and gas-stream cleanup. Granular activated carbon remains important because its highly porous structure captures organic chemicals, tastes, odours, and selected emerging contaminants. The U.S. Environmental Protection Agency reports that properly designed GAC systems can remove up to 99.9% of many volatile organic compounds and reduce target concentrations below 1 microgram per litre.

- WHO and UNICEF reported that 1 billion people still lacked safely managed drinking water in 2024, despite global coverage rising from 68% in 2015 to 74%. Activated carbon is also established in industrial air-emission control. EPA technical guidance indicates that carbon adsorbers can achieve 95–99% VOC removal at inlet concentrations between 500 and 2,000 parts per million when correctly designed, operated, and maintained.

Key Takeaways

- The Global activated carbon filter market was valued at USD 287.2 million in 2025.

- The Global market is projected to grow at a CAGR of 5.2% and is estimated to reach USD 499.9 million by 2035.

- Based on type, granular activated carbon dominated the activated carbon filter market, accounting for 53.5% of the total market share.

- Based on application, water treatment led the activated carbon filter market, comprising 46.8% of the total market share.

- In 2025, Asia Pacific was the most dominant region in the activated carbon filter market, accounting for 43.1% of the total market.

Regulation is creating a measurable replacement and installation cycle. The EPA continues to uphold a 4-parts-per-trillion limit for PFOA and PFOS, while its 2026 proposal could extend eligible system compliance to April 2031. EPA expects the standard to reduce exposure for about 100 million people. Research covering more than 400 commercially available PFAS also estimated that 76–87% could be treated cost-effectively through GAC filtration.

Future opportunities are expected in advanced municipal treatment, point-of-use filtration, carbon regeneration, and specialised media for shorter-chain PFAS. The European Union requires quaternary treatment for large wastewater plants by 2045, while pharmaceutical and cosmetics producers must finance at least 80% of additional treatment costs. Growth will therefore favour high-capacity systems, reactivated carbon services, lower-energy adsorption designs, and application-specific filters that improve contaminant selectivity while reducing disposal volumes and lifecycle costs. Demand should also rise steadily across chemical plants, refineries, laboratories, commercial buildings, and decentralized drinking-water systems worldwide.

Type Analysis

Granular Activated Carbon dominates with 53.5% due to strong adsorption performance and broad industrial use.

In 2025, Granular Activated Carbon held a dominant market position, capturing more than a 53.5% share. The segment benefited from its use in water treatment, industrial wastewater purification, air filtration, and chemical processing. Its reusable structure, high adsorption capacity, and suitability for continuous filtration systems supported demand during the year. During December 2025, manufacturers favored granular media because it can handle large treatment volumes and allows easier regeneration than disposable alternatives. Its effectiveness in removing organic compounds, odors, chlorine, and selected contaminants further strengthened its position across industrial installations.

Powdered Activated Carbon emerged as a growing segment due to its rapid mixing ability and flexible dosing. It gained attention in emergency water treatment, process purification, and applications requiring short contact times. Its lower installation complexity also supported adoption across smaller facilities and temporary treatment operations.

Application Analysis

Water Treatment dominates with 46.80% due to demand for contaminant removal.

In 2025, Water Treatment held a dominant market position, capturing more than a 46.80% share. The segment gained strength from the use of activated carbon filters in drinking water systems, wastewater plants, industrial process water, and household filtration units. During December 2025, demand remained firm as treatment operators focused on removing chlorine, unpleasant taste, odor, organic compounds, and trace pollutants. Granular and powdered carbon media were selected because they offer flexible installation, strong adsorption performance, and compatibility with treatment stages. These benefits kept water treatment at the center of market demand.

Air Purification emerged as a growing segment as factories, commercial buildings, laboratories, and facilities increased their focus on controlling fumes, odors, smoke, and volatile compounds. Activated carbon filters gained wider use in ventilation systems because they support cleaner air, improve indoor comfort, and help reduce harmful airborne contaminants.

Key Market Segments

By Type

- Granular Activated Carbon

- Powdered Activated Carbon

- Impregnated Activated Carbon

- Fiber Activated Carbon

By Application

- Water Treatment

- Air Purification

- Food and Beverage Processing

- Pharmaceutical Applications

- Industrial Gas Adsorption

- Others

Drivers

Expansion of compressed air & gas treatment using activated carbon filters

Growing deployment of activated carbon filters in compressed air and gas treatment systems supports approximately +1.3 percentage points of additional CAGR, as industries seek to protect downstream equipment, ensure product purity, and comply with compressed-air standards, with market commentary pointing to a dedicated activated carbon compressed air filter segment projected to grow at mid-single-digit CAGR from 2026 to 2033 and listing major global players focused on this niche.

In sectors such as electronics, automotive paint shops, food and beverage packaging, pharmaceuticals, and general manufacturing, compressed air is widely used for conveying, actuating, and blowing, but oil vapors, VOCs, and odors can contaminate products or processes; activated carbon filters installed downstream of dryers and coalescers remove such contaminants and help meet standards like ISO 8573-1 classes for compressed-air quality.

Strategically, this driver allows filter manufacturers to leverage existing relationships with compressor OEMs and industrial distributors, integrating activated carbon modules into system packages and aftermarket offerings, which generates recurring replacement revenue and raises the average filtration content per installed compressor; as compressed air and gas treatment standards propagate across newer industrializing markets, this segment’s growth realistically adds about 1.3 percentage points to overall activated carbon filter CAGR beyond the growth explained by raw environmental regulation alone.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter air & water emission norms driving activated carbon filter adoption | +2.2% | North America core, EU, China, India industrial belts | Long term (≥ 4 years) |

| Industrialization & urbanization in APAC boosting filtration demand | +1.8% | China, India, SE Asia, Middle East corridors | Medium term (2-4 years) |

| Upgrading legacy filtration in food, pharma & chemical plants | +1.5% | EU, North America, Japan, regulated APAC | Medium term (2-4 years) |

| Growth of municipal and industrial wastewater treatment infrastructure | +1.6% | China, India, EU, GCC, Latin America spill-over | Long term (≥ 4 years) |

| Expansion of compressed air & gas treatment using activated carbon filters | +1.3% | North America, EU, APAC manufacturing hubs | Medium term (2-4 years) |

| Tightening VOC, odor & indoor air quality standards | +1.2% | North America, EU regulatory hubs, urban Asia | Long term (≥ 4 years) |

Restraints

Short media lifespan & disposal constraints

Short media lifespan and disposal constraints contribute roughly -1.3 percentage points of CAGR restraint because activated carbon media must be replaced at regular intervals, and spent media handling carries both cost and regulatory friction, especially in non-industrial and small-scale deployments. In drinking-water applications, agricultural guidance notes that activated carbon effectively adsorbs organics, chlorine, and some metals, but capacity is finite and filters must be changed when saturation is reached to avoid breakthrough; industrial practice often sees media replacement cycles of 6–24 months, depending on contaminant load, which creates recurring Opex for end-users.

Strategically, these lifecycle costs can deter adoption in cost-sensitive segments and push some users toward lower‑maintenance alternatives, while regulators increasingly scrutinize disposal and regeneration processes, adding compliance overhead to carbon filter operators; as awareness of waste and sustainability issues grows into 2025–2028, this restraint realistically trims about 1.3 percentage points from potential CAGR by discouraging long-term uptake in some residential, small-commercial, and lightly regulated industrial segments.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile activated carbon raw-material costs | -1.5% | APAC production hubs, North America, EU | Medium term (2-4 years) |

| Short media lifespan & disposal constraints | -1.3% | Global, more acute in EU, North America | Long term (≥ 4 years) |

| High upfront capex for industrial and municipal filtration | -1.2% | Emerging APAC, LATAM, Africa corridors | Medium term (2-4 years) |

| Lack of standardized filtration regulations in some countries | -1.1% | APAC emerging, Africa, parts of LATAM | Long term (≥ 4 years) |

| Competition from alternative filtration technologies | -1.0% | North America core, EU, Japan | Medium term (2-4 years) |

| Limited technical know-how among smaller end-users | -0.8% | Global SME and small-utility segment | Long term (≥ 4 years) |

Opportunity

Specialty carbons for emerging contaminants

Specialty carbons for emerging contaminants represent upside because current activated carbon filters are largely optimized for traditional organics, chlorine, and odor, while regulated attention is shifting toward PFAS, pharmaceutical residues, endocrine disruptors, and microplastics in water and process streams, and technical literature and policy discussions indicate activated carbon will be part of multi-technology trains addressing these pollutants.

If specialty-carbons could capture, say, 10–15% of incremental capex and Opex in emerging contaminant treatment by 2030–2035, and command price premia of 30–50% over generic media due to performance and regulatory validation, they could add a realistic 1.6 percentage points of CAGR upside above conventional growth, especially as PFAS and pharma-related regulation broadens. Strategically, this requires investment into R&D, pilot trials and third-party validation, but positions activated carbon filters at the center of high-value segments rather than the periphery, enlarging TAM in advanced markets where utilities and industrials will spend heavily to meet new standards.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Smart, sensor-integrated activated carbon filter-as-a-service | +1.8% | North America core, EU regulatory hubs, APAC industrial clusters | Medium term (2-4 years) |

| Specialty carbons for emerging contaminants (PFAS, pharma, microplastics) | +1.6% | U.S., EU, Japan, advanced China & GCC utilities | Long term (≥ 4 years) |

| Consumer & residential IAQ and water upgrade bundles | +1.4% | North America, EU, urban APAC, GCC households | Medium term (2-4 years) |

| Energy, hydrogen and battery-material process gas purification | +1.5% | EU, North America, China, Middle East corridors | Long term (≥ 4 years) |

| Circular, low-carbon activated carbon production & regeneration | +1.3% | EU, North America, Japan, progressive APAC | Long term (≥ 4 years) |

| M&A roll-ups and OEM platform consolidation in fragmented filter market | +1.2% | APAC emerging, LATAM, Africa, India corridors | Medium term (2-4 years) |

Challenge

Climate-exposed raw-material And logistics chains

Climate-exposed raw-material and logistics chains are a systemic challenge because activated carbon production depends heavily on feedstocks and transport networks vulnerable to climate and environmental disruption, and supply-chain analyses underscore that manufacturing subsectors now face unique climate risks tied to their configurations. Coconut shell, wood, and coal supplies in APAC can be hit by cyclones, floods, droughts, and crop diseases, causing multi‑week harvest disruptions, yield drops of 10–20%, and localized price spikes, while activation plants themselves may face outages from extreme weather or regulatory closures around emissions.

Downstream, international shipping routes used to move bulk media and filters are increasingly exposed to port congestion, low‑water events in key river systems, and storm-related delays, adding 5–15 days to transit times during high-stress events and forcing OEMs and distributors to carry higher safety stocks, which ties up working capital and complicates responsiveness to demand spikes. Strategically, firms must diversify suppliers, build redundancy into logistics, and invest in climate risk modeling and traceability, all of which raise operating costs and slow expansion into some geographies where resilient supply chains are harder to establish; these frictions do not eliminate sales but realistically subtract about 1.0 percentage point from achievable CAGR as companies temper growth to protect reliability and risk profiles.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Complex specialized filtration design & quality control | -1.1% | North America core, EU regulatory hubs, advanced APAC | Long term (≥ 4 years) |

| Climate-exposed raw-material & logistics chains | -1.0% | APAC production hubs, global logistics corridors | Long term (≥ 4 years) |

| Fragmented standards & certification across regions | -0.9% | APAC emerging, Africa, LATAM corridors | Medium term (2-4 years) |

| Supply-chain coordination for cartridges & housings | -0.8% | Global OEM and pharma/food plants | Medium term (2-4 years) |

| Capital & regulatory hurdles for new carbon plants | -0.9% | APAC, Middle East, Africa, Latin America | Long term (≥ 4 years) |

| Talent gaps in process engineering & compliance | -0.8% | Global multi-plant operators | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Trade Barriers Reshaping Activated Carbon Filter Supply Chains.

Geopolitical tensions are reshaping the activated carbon filter market through trade restrictions, shipping disruption, feedstock uncertainty, and sourcing strategies. Manufacturers depend on internationally traded activated carbon, making costs sensitive to customs actions, freight availability, and bilateral trade relations.

- The United States continues to apply an antidumping duty order on certain activated carbon from China. In June 2026, the U.S. Department of Commerce revised the dumping margin for Ningxia Huahui and non-selected exporters to US$0.04 per kilogram, while the China-wide rate remained US$2.42 per kilogram. These measures can widen landed-cost differences and encourage U.S. buyers to qualify domestic or alternative overseas suppliers.

- Maritime instability adds another risk. UN Trade and Development reported that ship tonnage moving through the Suez Canal in early May 2025 remained 70% below the 2023 average. Longer routes can delay imported carbon media, filter components, and replacement inventory while increasing freight and working-capital requirements.

At the same time, environmental policy is supporting regional investment in advanced treatment capacity. European Union wastewater rules require pharmaceutical and cosmetics producers to finance at least 80% of additional quaternary-treatment costs. These developments are expected to strengthen demand for activated carbon systems, regeneration services, and held inventories. However, suppliers remain exposed to tariff changes, route disruption, raw-material price volatility, and longer approval cycles for alternative carbon grades.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Activated Carbon Filter Market.

In 2025, Asia Pacific held a dominant position in the activated carbon filter market, accounting for 43.1% of global revenue and generating USD 123.81 million. The region benefited from urbanization, expanding industrial water treatment, stricter emission control, and rising demand for filtration. Activated carbon filters gained wider use across municipal utilities, chemical plants, food-processing facilities, power stations, and ventilation systems because they remove odors, chlorine, organic compounds, and airborne pollutants.

The Asian Development Bank estimated that Asia and the Pacific requires US$4 trillion in water, sanitation, and hygiene investment through 2040, equal to about US$250 billion annually, while existing budgets cover only around 40% of the requirement. WHO also reports that one person dies from air pollution every 14 seconds in the Western Pacific Region. These conditions support future demand for granular carbon systems, replacement cartridges, regeneration services, and advanced adsorption units across China, Japan, South Korea, Southeast Asia, and Australia.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Activated carbon filter manufacturers focus on strengthening adsorption performance, product consistency, regeneration capability, and distribution reach to remain competitive. A key priority is media innovation, including high-surface-area granular carbon, powdered grades, impregnated carbon, and fiber-based filters that improve contaminant removal across water and air treatment applications. Companies also invest in automated production and testing systems, as these support uniform pore structure, reliable quality, and large-scale filter manufacturing.

Vertical integration with coal, coconut-shell, and wood-based feedstock suppliers helps secure raw material availability and improve cost control during price fluctuations. Strategic production and regeneration expansion, particularly in Asia Pacific, allows companies to serve concentrated demand from municipal treatment, industrial processing, and air purification facilities. Additionally, manufacturers emphasize application-specific filter design, technical certification, and lifecycle services, while building long-term relationships with utilities, equipment suppliers, and industrial customers to strengthen recurring replacement demand and positioning in specialized filtration segments.

Market Key Players

- TIGG LLC

- Puragen Activated Carbons

- Cabot Corporation

- WesTech Engineering Inc.

- Kuraray Co., Ltd

- Lenntech B.V.

- Donau Carbon GmbhGeneral Carbon Corporation

- Carbtrol Corp.

- Sereco S.R.L

Key Development

- In February 2026, Cabot Corporation completed the acquisition of Mexico Carbon Manufacturing from Bridgestone Corporation for approximately USD 70 million, following the agreement announced in August 2025. The deal expanded Cabot’s manufacturing presence in Mexico and strengthened its long-term supply relationship with Bridgestone.

- In August 2025, CPL Activated Carbons officially rebranded as Puragen, unifying its activated carbon engineering, filtration, reactivation, mobile treatment, and logistics services under one global purification brand.

- In April 2025, Donau Carbon completed the 100% acquisition of Kalpa Char Products, expanding its global activated carbon manufacturing presence across powdered, granular, and extruded carbon grades.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 287.2 Mn |

| Forecast Revenue (2035) | USD 499.9 Mn |

| CAGR (2026-2035) | 5.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Powdered Activated Carbon, Granular Activated Carbon, Impregnated Activated Carbon, and Fiber Activated Carbon), By Application (Water Treatment, Air Purification, Food and Beverage Processing, Pharmaceutical Applications, Industrial Gas Adsorption, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | TIGG LLC, Puragen Activated Carbons, Cabot Corporation, WesTech Engineering Inc., Kuraray Co., Ltd., Lenntech B.V., Donau Carbon GmbH, General Carbon Corporation, Carbtrol Corp., and Sereco S.R.L. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |