Quick Navigation

- Report Overview

- Key Takeaways

- By Source Analysis

- By Product Type Analysis

- By Flavor Analysis

- By Product Form Analysis

- By Function Analysis

- By Application Analysis

- By Sales Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

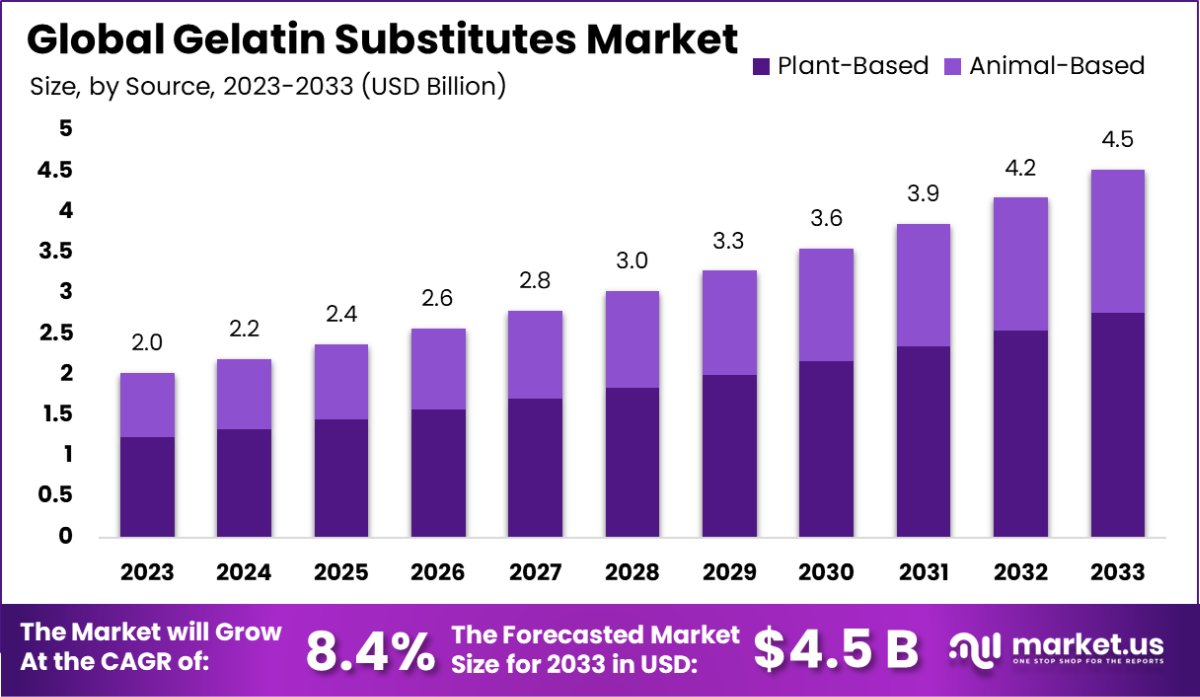

The Global Gelatin Substitutes Market is expected to be worth around USD 4.5 Billion by 2033, up from USD 2.02 Billion in 2023, and grow at a CAGR of 8.4% from 2024 to 2033. Asia-Pacific gelatin substitutes market at 42.2%, valued at USD 0.853 billion.

Gelatin substitutes are ingredients used in place of gelatin, which is derived from animal collagen. These substitutes are favored for their ability to mimic the gelling, thickening, and stabilizing properties of gelatin without using animal products, catering to vegan, vegetarian, and certain religious dietary restrictions. Common substitutes include agar-agar, pectin, carrageenan, and konjac.

The gelatin substitutes market is growing due to increasing dietary preferences for plant-based and allergen-free products. This market serves a wide range of industries, including food and beverage, pharmaceuticals, and cosmetics, where these substitutes are used for their gelling properties without the ethical and health concerns associated with animal-derived gelatin.

The market’s growth is largely driven by rising veganism and consumer awareness of animal welfare, which promote the adoption of plant-based gelatin substitutes.

Demand for gelatin substitutes is bolstered by their diverse applications in gummy candies, flavoured yogurts, and capsules, appealing to consumers seeking vegetarian and clean-label products. Opportunities in the gelatin substitutes market are expanding with innovations in food texture and stability, meeting consumer demands for high-quality, ethical food ingredients.

The Gelatin Substitutes Market is witnessing increasing demand driven by growing concerns over dietary restrictions, environmental sustainability, and ethical sourcing. As traditional gelatin production primarily involves animal-derived sources, including pigskin, bovine hides, and bones, consumers and manufacturers are turning to plant-based alternatives such as agar, pectin, and carrageenan.

These substitutes are particularly attractive in the food industry, where they mimic the textural and rheological properties of gelatin, such as gelling, thickening, and stabilizing.

In Western Europe, for instance, the gelatin market alone is substantial, with a total of 60,000 tonnes produced annually, 80% of which is used in food applications. This highlights the significant market for alternatives to gelatin in food-related products. Agar, a common gelatin substitute, is composed of two polysaccharides—agarose (70%) and agaropectin (30%)—and exhibits unique properties.

It gels at lower temperatures (below 32–42°C) and melts above 85°C, offering flexibility in various food preparations. The rising use of such substitutes in food not only caters to vegan and vegetarian dietary needs but also aligns with sustainability trends, as plant-based alternatives generally have a lower environmental impact compared to animal-derived gelatin.

The global gelatin market itself is a significant industry, with 326,000 tonnes produced in 2007. However, the shift toward plant-based substitutes is gaining momentum, supported by increasing consumer demand for cleaner and more sustainable ingredients.

As a result, manufacturers are exploring innovative solutions to replicate gelatin’s properties while minimizing environmental and ethical concerns, creating strong growth prospects for gelatin substitutes in the coming years.

Key Takeaways

- The Global Gelatin Substitutes Market is expected to be worth around USD 4.5 Billion by 2033, up from USD 2.02 Billion in 2023, and grow at a CAGR of 8.4% from 2024 to 2033.

- Plant-based sources dominate the gelatin substitutes market, accounting for 61.4% of the total.

- Agar-agar leads product types in the market with a substantial 36.4% share.

- A majority of consumers prefer unflavored gelatin substitutes, making up 64.5% of the market.

- Capsules are a popular product form, comprising 37.7% of the gelatin substitutes sold.

- Thickening and gelling functions are crucial, representing 38.8% of gelatin substitute usage.

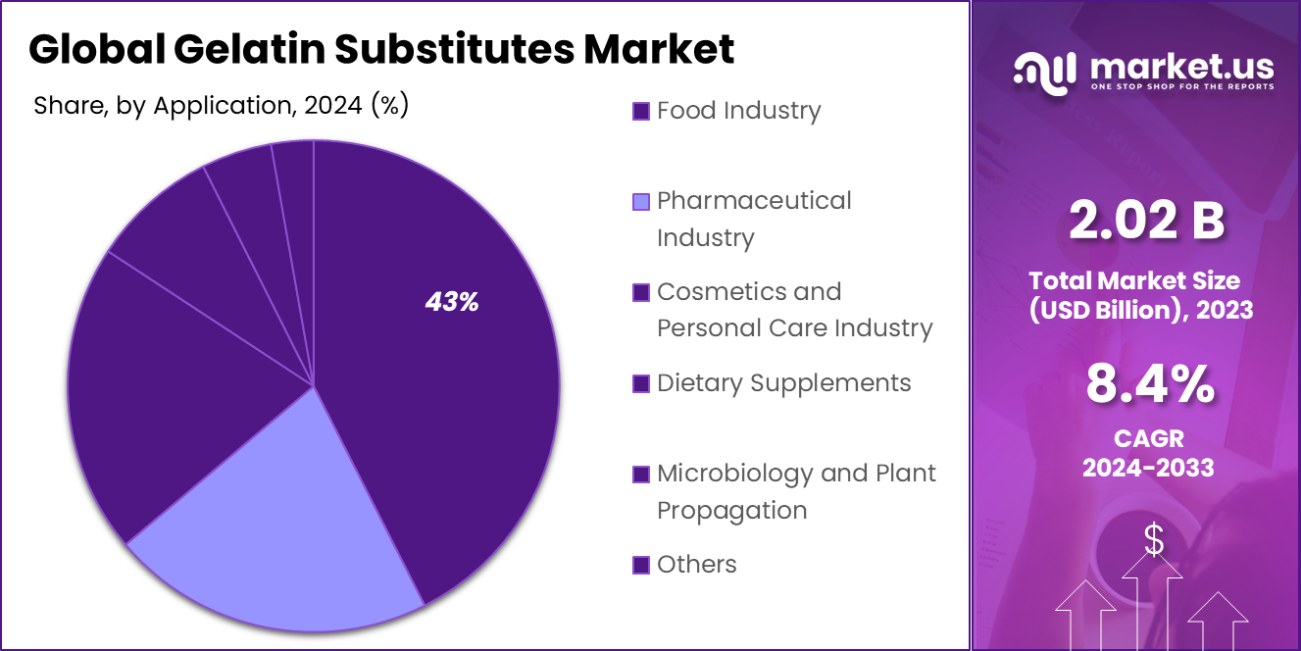

- The food industry is the primary application area, consuming 45.5% of all gelatin substitutes.

- Hypermarkets and supermarkets are key sales channels, distributing 38.6% of these products.

- The Asia-Pacific gelatin substitutes market accounts for 42.2% of the global market, valued at USD 0.853 billion.

By Source Analysis

The Gelatin Substitutes Market prominently features plant-based alternatives, accounting for 61.4% of the market share.

In 2023, Plant-Based held a dominant market position in the “By Source” segment of the Gelatin Substitutes Market, capturing a 61.4% share. This significant lead is primarily attributed to the increasing consumer shift towards vegan and vegetarian lifestyles, coupled with a growing awareness of animal welfare and environmental sustainability.

These factors have propelled the demand for plant-based alternatives like agar-agar, carrageenan, and pectin, which are perceived as more ethical and sustainable options compared to their animal-based counterparts.

The market dynamics reflect a robust preference for plant-based ingredients, not only in food industries but also in pharmaceuticals and cosmetics, where gelatin substitutes are essential for manufacturing capsules, gummies, and emulsifiers.

The versatility and functional properties of these plant-based substitutes have been enhanced by technological advancements, improving their appeal by closely mimicking the texture and performance of traditional gelatin.

Despite the strong performance of the plant-based segment, the animal-based segment still holds a significant market share, driven by traditional uses in various applications where the unique properties of animal-derived gelatin are preferred.

However, as technology progresses and consumer preferences continue to evolve, the gap is expected to widen, favoring plant-based substitutes. This shift is supported by continuous innovations and expansions in application areas, making plant-based products more accessible and desirable across global markets.

By Product Type Analysis

Agar-Agar leads product types in the Gelatin Substitutes Market with a significant 36.4% share.

In 2023, Agar-Agar held a dominant market position in the “By Product Type” segment of the Gelatin Substitutes Market, commanding a 36.4% share. Agar-Agar’s prominence is largely due to its superior gelling properties and its widespread acceptance as a vegan-friendly option, appealing to both food manufacturers and consumers seeking plant-based alternatives.

Following closely, Carrageenan and Pectin accounted for 22.1% and 18.5% of the market share, respectively, each favored for their unique textural attributes and stability in various food and pharmaceutical formulations.

Cornstarch and Xanthan Gum also held significant positions, with shares of 8.2% and 5.3%. These substitutes are prized for their thickening capabilities and are extensively used in sauces, soups, and bakery products. Guar Gum, Arrowroot, Instant Clear Gel, and Kudzu collectively made up the remaining 9.5% of the market.

Each of these has niche applications: Guar Gum in gluten-free product recipes, Arrowroot in quick-cooking dishes, Instant Clear Gel in desserts and jellies, and Kudzu in traditional Asian cuisines and natural remedies.

This diversification within the Gelatin Substitutes Market underscores the growing consumer demand for varied textural and dietary preferences across different applications, driving the innovation and adoption of these alternatives.

By Flavor Analysis

In the flavor segment, unflavored gelatin substitutes dominate, making up 64.5% of the market.

In 2023, Unflavored held a dominant market position in the “By Flavor” segment of the Gelatin Substitutes Market, with a commanding 64.5% share. This significant preference for unflavored gelatin substitutes can be attributed to their versatility in various applications.

Unflavored options are preferred by manufacturers across the food, pharmaceutical, and cosmetic industries because they offer flexibility in formulation without altering the taste profiles of the end products. This characteristic is particularly valued in complex recipes where the inherent flavor of ingredients needs to be preserved.

On the other hand, Flavored gelatin substitutes accounted for the remaining 35.5% of the market. These are popular in consumer-facing products such as jellies, desserts, and confectionaries, where they enhance the sensory attributes of the products with predetermined flavors. The market for flavored substitutes is driven by consumer demand for convenience and variety in ready-to-eat products.

The clear preference for unflavored gelatin substitutes highlights the industry’s focus on adaptability and consumer demand for customization in their food and product choices. It also reflects the ongoing innovation in the sector, where developing neutral bases that can seamlessly integrate into diverse products remains a priority.

By Product Form Analysis

Capsules are the preferred product form, comprising 37.7% of the Gelatin Substitutes Market.

In 2023, Capsules held a dominant market position in the “By Product Form” segment of the Gelatin Substitutes Market, with a 37.7% share. This leadership stems from the increasing consumer preference for vegetarian and vegan-friendly capsules in the dietary supplements and pharmaceutical sectors.

The ability of gelatin substitutes like HPMC (hydroxypropyl methylcellulose) to match the performance characteristics of gelatin while being plant-based has significantly contributed to their popularity.

Following Capsules, Gummies captured a substantial market share of 26.3%. Their growth is fueled by the demand in the nutraceutical industry, where consumers, especially children and adults who prefer not to swallow pills, favor gummy vitamins and supplements.

Powders accounted for 19.4% of the market, appreciated for their versatility in both food and pharmaceutical applications, allowing easy incorporation into various products.

Soft Gels made up 10.1% of the market, often used in the encapsulation of oils and fat-soluble vitamins, while the remaining 6.5% was represented by other forms, including emulsions and films, which are integral to specific niche applications.

This distribution highlights a robust demand for varied product forms in the Gelatin Substitutes Market, catering to diverse consumer needs and manufacturing requirements.

By Function Analysis

Thickening and gelling functions are central to the market, holding a 38.8% share.

In 2023, Thickening and Gelling held a dominant market position in the “By Function” segment of the Gelatin Substitutes Market, with a 38.8% share. This segment’s leadership is attributed to the critical role that thickening and gelling agents play in the food and pharmaceutical industries, where they are essential for achieving the desired consistency and texture in products.

These agents are especially popular in the manufacturing of desserts, jellies, and dairy products, as well as in vegan and vegetarian food preparations where they replace gelatin.

Stabilizers followed with a 29.7% market share, proving indispensable in products that require a consistent shelf life and quality, such as beverages, sauces, and processed foods. Emulsifying agents captured 21.5% of the market, favored for their ability to maintain stable emulsions in products like creams, lotions, and condiments, thereby enhancing texture and preventing separation.

The Binding segment accounted for the remaining 10%, utilized in both food and non-food applications, including pharmaceuticals where they help in tablet formation, and meat alternatives where they improve texture and cohesion. The varied functionalities of these gelatin substitutes highlight their versatility and essential role across multiple industries, driving their adoption and innovation in new product formulations.

By Application Analysis

The food industry emerges as the primary application area, capturing 45.5% of the market.

In 2023, the Food Industry held a dominant market position in the “By Application” segment of the Gelatin Substitutes Market, with a commanding 45.5% share. This significant market share reflects the critical role of gelatin substitutes in various food applications, including dairy products, desserts, meat products, and confectionery.

The shift towards plant-based and clean label products has particularly amplified the demand for these substitutes as consumers seek healthier and ethically sourced ingredients.

The Pharmaceutical Industry followed with a 20.3% share, where gelatin substitutes are increasingly used in the formulation of capsules, tablets, and emulsions, driven by the growing demand for vegan and hypoallergenic medication options.

The Cosmetics and Personal Care Industry captured 16.2% of the market, leveraging these substitutes in products that require stabilizing and thickening agents, such as creams, lotions, and hair care products.

Dietary Supplements and Microbiology and Plant Propagation sectors accounted for 9.6% and 8.4% respectively. Dietary supplements use these alternatives to cater to the vegan market and those with dietary restrictions, while in microbiology and plant propagation, gelatin substitutes are essential in culture media and plant tissue culture, emphasizing their versatility and utility across various industries.

By Sales Channel Analysis

Hypermarkets and supermarkets are the leading sales channels, representing 38.6% of gelatin substitute sales.

In 2023, Hypermarkets and Supermarkets held a dominant market position in the “By Sales Channel” segment of the Gelatin Substitutes Market, with a 38.6% share. This leadership stems from their broad consumer reach and ability to offer a wide variety of products, including an extensive range of gelatin substitutes catering to health-conscious and ethical consumers.

These retail giants are often the first choice for shoppers due to their convenience, competitive pricing, and the assurance of product quality and availability.

Convenience Stores and Discount Stores followed with market shares of 18.4% and 14.3% respectively. Convenience Stores benefit from their strategic locations and extended operating hours, making them a popular choice for quick purchases. Discount Stores attract price-sensitive consumers by offering gelatin substitutes at lower prices, appealing particularly to budget-conscious shoppers.

Food Specialty Stores and Independent Small Groceries accounted for 10.2% and 8.5% of the market. These outlets often cater to niche markets looking for specialized products not typically found in larger retail formats. Finally, Online Retail held a 10% share, a segment that continues to grow as consumers appreciate the convenience of home delivery and access to a broader range of products from different regions and brands.

Key Market Segments

By Source

- Plant-Based

- Animal-Based

By Product Type

- Agar-Agar

- Carrageen

- Pectin

- Cornstarc

- Xanthan Gum

- Guar Gum

- Arrowroot

- Instant Clear Gel

- Kudzu

- Others

By Flavor

- Unflavoured

- Flavoured

By Product Form

- Capsules

- Gummies

- Powders

- Soft Gels

- Others

By Function

- Thickening & Gelling

- Stabilizers

- Emulsifying

- Binding

- Others

By Application

- Food Industry

- Pharmaceutical Industry

- Cosmetics and Personal Care Industry

- Dietary Supplements

- Microbiology and Plant Propagation

- Others

By Sales Channel

- Hypermarkets/Supermarkets

- Convenience Stores

- Mom and Pop Stores

- Discount Stores

- Food Specialty Stores

- Independent Small Groceries

- Online Retail

- Others

Driving Factors

Growing Vegan and Vegetarian Populations

As more people globally adopt vegan and vegetarian diets due to health, ethical, or environmental reasons, the demand for gelatin substitutes has significantly increased. Gelatin, derived from animal sources, is being replaced in food products, pharmaceuticals, and cosmetics by plant-based alternatives like agar, carrageenan, and pectin.

This shift not only caters to dietary restrictions but also aligns with the broader consumer trend towards cruelty-free and sustainable products. Companies in the gelatin substitute market are innovating with new sources and improved extraction techniques to meet this rising demand.

Advancements in Food Technology and Processing

Technological advancements in the food processing industry are pivotal in driving the gelatin substitutes market. Enhanced techniques in extracting and refining plant-based gelling agents have made substitutes more accessible and cost-effective. This includes improved methods of obtaining high-quality substitutes from seaweeds, fruits, and other plant materials that can mimic gelatin’s textural properties.

These innovations help manufacturers replace gelatin in products such as gummy candies, yogurts, and desserts without compromising on texture or taste, thereby expanding the range of suitable vegetarian and vegan options.

Increased Awareness of Health Benefits

Health-conscious consumers are increasingly aware of the benefits of plant-based diets, which has led to a preference for gelatin substitutes that are perceived as healthier. Plant-based gelling agents are often richer in dietary fibers and free from cholesterol and animal fats, making them attractive alternatives for health-focused individuals.

Additionally, concerns about potential contaminants and diseases associated with animal-derived products have prompted a shift towards safer, plant-based alternatives. This health-driven demand is influencing both the development and marketing strategies of companies in the gelatin substitutes sector.

Restraining Factors

High Costs and Limited Availability Hinder Growth

Gelatin substitutes, such as agar-agar, pectin, and carrageenan, often come with a higher price tag compared to traditional gelatin, primarily due to the complexities involved in their production and sourcing of raw materials. This can be a significant barrier for manufacturers, particularly small-scale producers, who may find the costs prohibitive.

Additionally, the availability of these substitutes can be limited in certain regions, making it difficult for companies to consistently secure the necessary ingredients, thereby impacting the scalability of production and market expansion.

Consumer Preference for Gelatin-based Products Remains Strong

Despite the rising interest in vegan and vegetarian diets, a substantial segment of consumers still prefers gelatin-based products due to their familiar texture and taste. Gelatin substitutes sometimes fail to perfectly mimic these qualities, which can lead to consumer reluctance to switch to alternative products.

This preference acts as a restraint on the market as manufacturers struggle to convince consumers that their gelatin-free options are not only similar in quality but also superior in terms of health benefits and ethical standards.

Regulatory Challenges Complicate Market Entry

The market for gelatin substitutes is heavily regulated, and new entrants must navigate a complex web of food safety standards and certifications. Different regions have varying regulations concerning the use of food additives and ingredients, which can complicate the formulation and marketing of gelatin-free products.

This regulatory environment can pose a significant barrier to entry for new companies and can also slow down innovation and product development within established companies, ultimately restraining market growth.

Growth Opportunity

Rising Veganism Trend Opens New Market Segments

The global shift towards vegan and vegetarian lifestyles is creating a substantial demand for gelatin substitutes. As consumers increasingly opt for plant-based diets, the need for animal-free products grows, presenting a significant opportunity for manufacturers of gelatin substitutes like agar-agar, carrageenan, and pectin.

This trend is not only prevalent in food products but also in pharmaceuticals and cosmetics, where gelatin-free capsules and gummies are gaining popularity. Capitalizing on this dietary shift can open new market segments and drive substantial growth in the gelatin substitute industry.

Technological Advancements Enhance Product Quality and Appeal

Technological innovations in food processing and ingredient formulation are enabling manufacturers to improve the sensory and functional properties of gelatin substitutes. These advancements help in closely mimicking the texture and taste of gelatin, making gelatin-free products more appealing to a broader audience.

As technology continues to evolve, it allows for greater scalability in production and more efficient use of resources. Companies that invest in these technologies can significantly enhance their market position by offering superior products that meet consumer expectations in terms of both quality and ethical standards.

Expanding Applications in Diverse Industries

Gelatin substitutes are finding their way into a wider range of applications beyond the food industry, including pharmaceuticals, cosmetics, and even photographic industries. The versatility of these substitutes allows for their use in capsules, emulsions, and films, among others.

This expansion into diverse markets not only broadens the potential customer base but also reduces the dependency on the food sector alone for revenue. Companies that explore and innovate within these new application areas can capture growth opportunities and diversify their business risks.

Latest Trends

Clean Label Movement Boosts Natural Substitutes Demand

The clean label movement, which prioritizes simple, natural ingredients in food products, is significantly impacting the gelatin substitutes market. Consumers are increasingly scrutinizing ingredient lists, preferring products without synthetic additives or those derived from non-animal sources.

This trend is driving manufacturers to reformulate products using natural substitutes like agar-agar, pectin, and carrageenan, which align with the clean label criteria. As awareness and preference for clean label products continue to grow, the demand for these natural and transparently sourced substitutes is expected to rise, shaping the market’s trajectory.

Sustainability Focus Enhances Plant-Based Substitute Popularity

Environmental concerns are steering both consumers and producers towards sustainable food practices, with a notable impact on the gelatin substitutes market. Plant-based gelatin alternatives are viewed as more sustainable than traditional animal-based gelatin due to their lower environmental footprint in terms of water use, land use, and carbon emissions.

This growing emphasis on sustainability is not only influencing consumer choices but also prompting manufacturers to adopt eco-friendly production processes. By leveraging this trend, companies can enhance their brand image and appeal to environmentally conscious consumers.

Hybrid Products Blend Gelatin and Substitutes

An emerging trend in the market is the development of hybrid products that combine gelatin with its substitutes to balance cost, texture, and consumer acceptance. These products aim to cater to consumers who are not fully committed to abandoning gelatin but are open to reduced animal content.

By integrating a proportion of gelatin substitutes, manufacturers can lower production costs while still maintaining the textural properties that consumers expect. This approach also allows for gradual consumer adaptation to gelatin-free products, potentially broadening the market base over time.

Regional Analysis

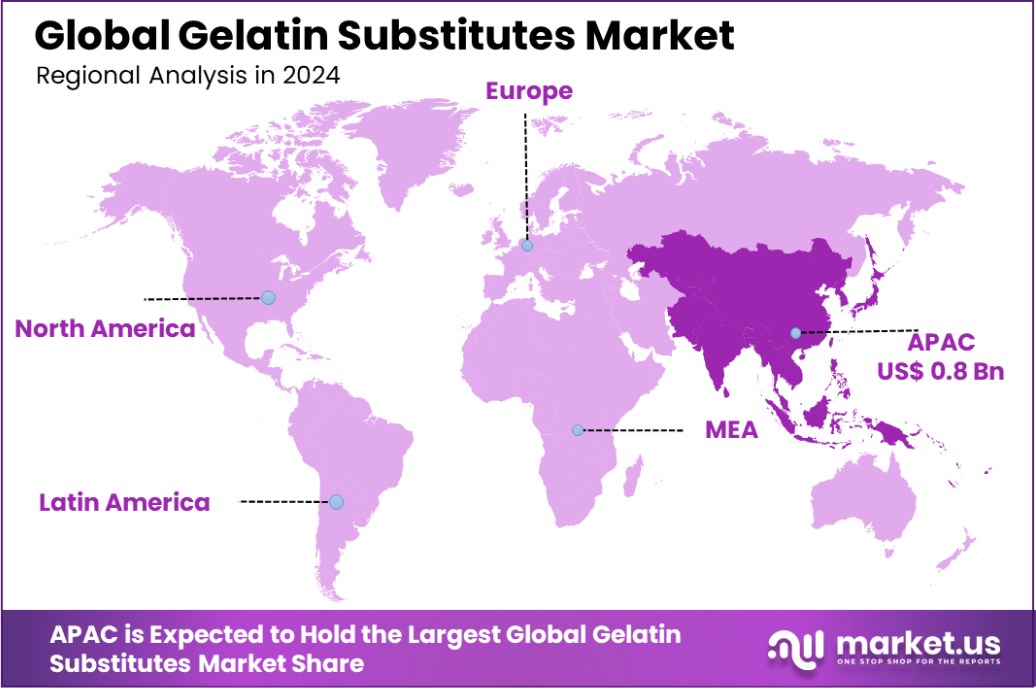

The Asia-Pacific gelatin substitutes market holds a 42.2% share, valued at USD 0.853 billion.

The gelatin substitutes market is experiencing diverse trends across various global regions, reflecting a mix of cultural, economic, and regulatory factors influencing demand and supply dynamics.

In North America, the market is driven by a strong shift towards vegan and plant-based diets, supported by increasing health consciousness among consumers. This region has seen robust growth in the use of agar-agar and carrageenan as popular gelatin alternatives in the food and pharmaceutical sectors.

Europe follows closely, with stringent EU regulations favoring the adoption of environmentally friendly and animal-free products, thus propelling the demand for gelatin substitutes. The region shows a high preference for pectin and guar gum, used extensively in dairy products and confectioneries.

Asia-Pacific, however, dominates the global landscape, holding a 42.2% market share and generating revenue of USD 0.853 billion. The market here is bolstered by rapid industrialization, expanding food processing sectors, and growing economic prosperity, particularly in countries like China and India. This region’s preference for innovative and cost-effective substitutes supports a vibrant market ecosystem.

The Middle East & Africa and Latin America, though smaller in scale, are emerging as potential growth areas. Increased urbanization and the rising vegan population in these regions are likely to boost the market. In particular, the Middle East shows a growing preference for halal-certified products, which include halal gelatin substitutes, thus opening new avenues for market expansion.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the global gelatin substitutes market in 2023, key companies such as Archer Daniels Midland, Ashland Global Holdings, Cargill, and CP Kelco have played pivotal roles. These companies, alongside others like Darling Ingredients Inc., DowDupont Inc., and DuPont de Nemours, Inc., are leading the charge in offering plant-based and synthetic alternatives that cater to the rising consumer demand for ethical, sustainable, and allergy-free products.

Archer Daniels Midland and Cargill have been particularly notable for their innovation in plant-based hydrocolloids, which are critical in applications ranging from food and beverage to pharmaceuticals, providing texture and stabilization in place of traditional gelatin.

Similarly, CP Kelco and Kerry Group have focused on advancing their portfolio of gellan gum, carrageenan, and pectin, leveraging their unique properties to match the gel strength and viscosity that gelatin typically provides.

In a specialized niche, companies like Marine Hydrocolloids and Java Biocolloid (Hakiki Group) have enhanced the extraction and refinement processes for agar-agar and other seaweed-based substitutes, which are gaining prominence due to their vegan-friendly label and superior gelling qualities.

Meanwhile, FMC Corporation and Ingredion Incorporated are pushing the boundaries in modified starches and other novel biopolymers, positioning them as viable substitutes in industrial applications.

The strategic focus for these key players involves not only expanding their product lines but also ensuring global regulatory compliance and maximizing the functional benefits of their offerings. As the market continues to evolve, these companies are expected to invest heavily in R&D to further refine their substitutes’ performance and appeal across diverse industries.

Top Key Players in the Market

- Archer Daniels Midland

- Ashland Global Holdings

- Ashland Inc.

- Cargill

- CP Kelco

- Darling Ingredients Inc.

- DowDupont Inc.

- DuPont de Nemours, Inc.

- FMC Corporation

- Gelita AG

- Glanbia Nutritionals

- Great American Spice Company

- Ingredion Incorporated

- Java Biocolloid (Hakiki Group)

- Kelco Co., Inc.

- Kerry Group

- Koninklijke DSM N.V.

- Marine Hydrocolloids

- Naturex SA

- Niblack Foods, Inc.

- Nitta Gelatin Inc.

- NOW Foods

- PB Leiner

- Rousselot SAS

- Special Ingredients Ltd.

- Tate and Lyle Plc

- The Agar Company (B&V SRL)

- Weishardt International

Recent Developments

- In 2024, Cargill is heavily investing in gelatin substitutes and the broader alternative protein sector, focusing on sustainable and innovative solutions. They’ve launched various plant-based products, such as EverSweet, a next-generation stevia sweetener, and are experimenting with mycoprotein as a meat substitute. Their efforts include collaborations with companies like Voyage Foods to create alternatives to traditional chocolate using plant-based ingredients.

- In 2023, CP Kelco expanded its biogas production by 40% at its Oklahoma facility to meet the growing demand for nature-based, sustainable ingredients. This was part of a broader initiative to increase capacity, including a 30% rise at its China plant achieved in 2020. Additionally, CP Kelco’s KELCOSENS™ Citrus Fiber won the 2024 Ringier Technology Innovation Award for Personal Care, highlighting its commitment to innovation and sustainability in the sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 2.02 Billion |

| Forecast Revenue (2033) | USD 4.5 Billion |

| CAGR (2024-2033) | 8.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Plant-Based, Animal-Based), By Product Type (Agar-Agar, Carrageen, Pectin, Cornstarc, Xanthan Gum, Guar Gum, Arrowroot, Instant Clear Gel, Kudzu, Others), By Flavor (Unflavoured, Flavoured), By Product Form (Capsules, Gummies, Powders, Soft Gels, Others), By Function (Thickening and Gelling, Stabilizers, Emulsifying, Binding, Others), By Application (Food Industry, Pharmaceutical Industry, Cosmetics and Personal Care Industry, Dietary Supplements, Microbiology and Plant Propagation, Others), By Sales Channel (Hypermarkets and Supermarkets, Convenience Stores, Mom and Pop Stores, Discount Stores, Food Specialty Stores, Independent Small Groceries, Online Retail, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Archer Daniels Midland, Ashland Global Holdings, Ashland Inc., Cargill, CP Kelco, Darling Ingredients Inc., DowDupont Inc., DuPont de Nemours, Inc., FMC Corporation, Gelita AG, Glanbia Nutritionals, Great American Spice Company, Ingredion Incorporated, Java Biocolloid (Hakiki Group), Kelco Co., Inc., Kerry Group, Koninklijke DSM N.V., Marine Hydrocolloids, Naturex SA, Niblack Foods, Inc., Nitta Gelatin Inc., NOW Foods, PB Leiner, Rousselot SAS, Special Ingredients Ltd., Tate and Lyle Plc, The Agar Company (B&V SRL), Weishardt International |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |