Quick Navigation

Report Overview

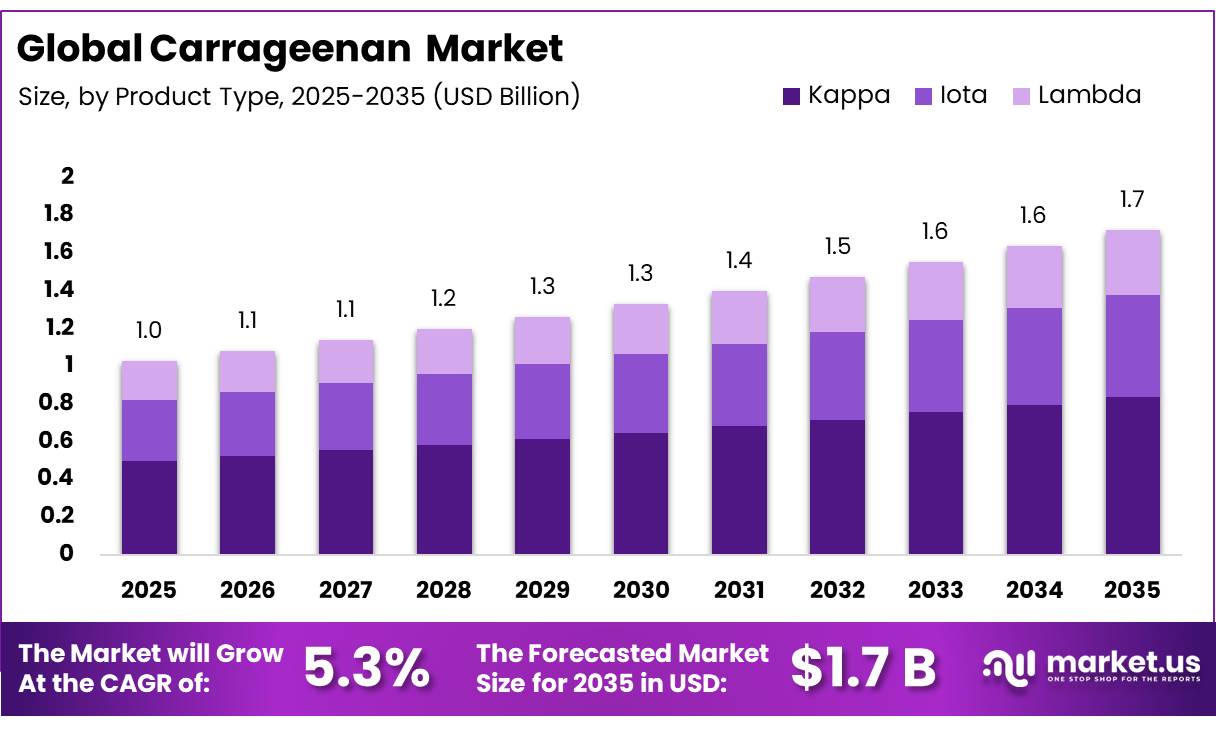

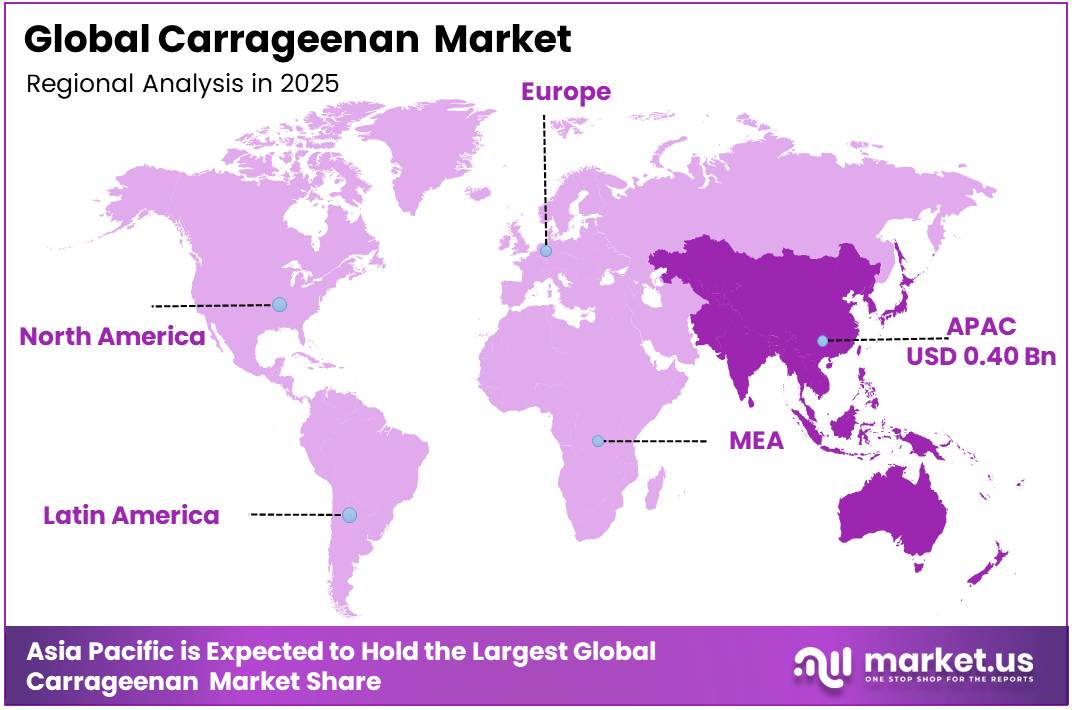

The Global Carrageenan Market size is expected to be worth around USD 1.7 Billion by 2035, from USD 1.0 Billion in 2025, growing at a CAGR of 5.3% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 38.5% share, holding USD 0.4 Billion revenue.

The global food and beverage industry remains the strongest growth driver for the carrageenan market. Carrageenan is widely used as a thickening, gelling, and stabilizing ingredient in dairy products, processed meat, plant-based food, beverages, yogurt, ice cream, cottage cheese, and flavored milk. Its role in improving texture, product stability, and shelf life has made it an important ingredient in large-scale food processing.

- According to FAO data, world milk production reached nearly 979 million tonnes in 2024, showing a 1.4% year-on-year increase. The OECD-FAO Agricultural Outlook 2025–2034 further projects milk production to reach 1,146 million tonnes by 2034, growing at 1.8% per year. India also remains a major dairy market, with milk output reaching 239.3 million tonnes in 2023–24, up 63.56% compared to a decade earlier, as reported by the Ministry of Fisheries, Animal Husbandry & Dairying. This steady rise in dairy production is expected to increase the use of carrageenan in processed dairy applications.

Key Takeaways

- The Global Carrageenan Market was valued at USD 1.0 billion in 2025.

- The global market is projected to grow at a CAGR of 5.3% and is estimated to reach USD 1.7 billion by 2035.

- Kappa carrageenan dominates the product type segment with 48.6% share, thanks to its excellent gelling capabilities and widespread use in dairy and processed food formulations.

- Semi-refined carrageenan accounts for 46.8% of the processing technology market, indicating cost-effective production and increasing use in large-scale food manufacturing.

- The stabilizer function leads with 41.7%, demonstrating a high desire for texture enhancement and product uniformity in processed food systems.

- Powder is the most popular physical form, accounting for 58.9%, due to its ease of handling, extended shelf life, and excellent solubility in industrial food preparation.

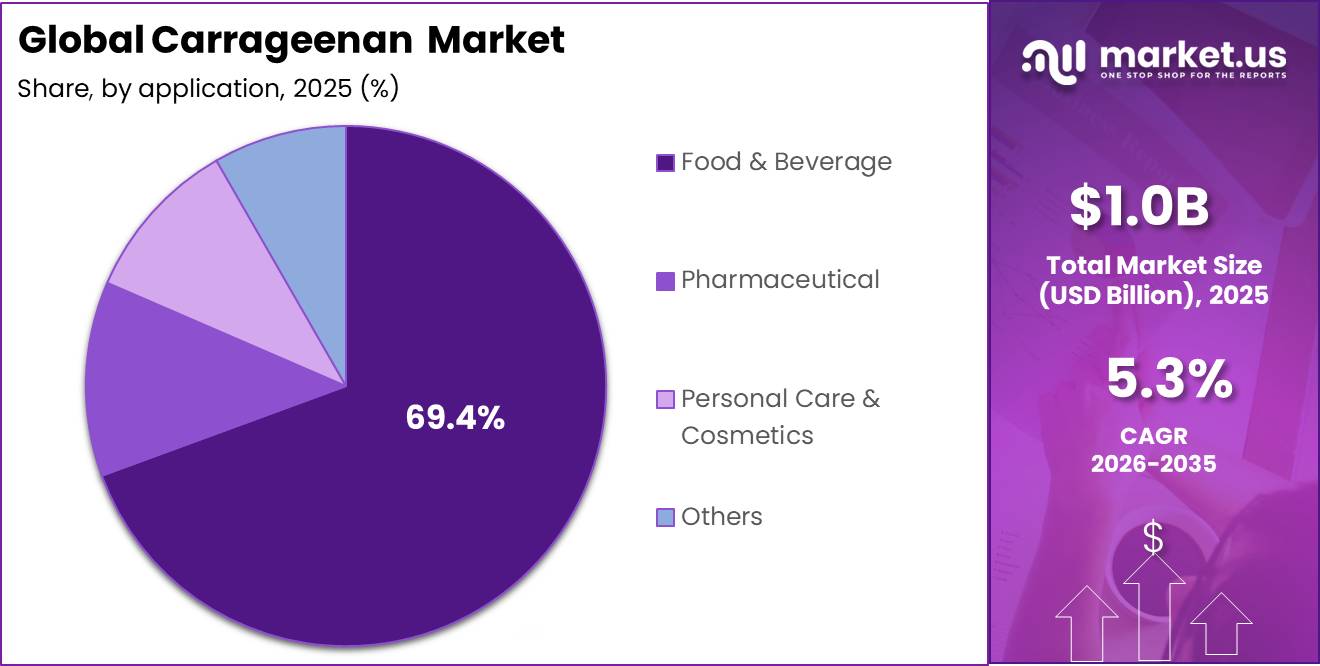

- The Food & Beverage category has 69.4% of the market, owing to its widespread use in dairy products, bread applications, sauces, and drinks for thickening, gelling, and stabilizing purposes.

- Asia Pacific is the main regional market, accounting for 38.5% of total sales, because to a strong seaweed production base, low-cost manufacturing, and rising food processing sectors.

The wider expansion of food and agricultural trade also supports carrageenan demand. As per FAO data, global food and agricultural trade increased from nearly USD 400 billion in 2000 to around USD 1.9 trillion in 2022. This shows the rising scale of processed food production and global ingredient consumption. As food manufacturers continue to focus on texture, stability, and longer shelf life, carrageenan is expected to remain a key functional ingredient across food and beverage applications.

Asia Pacific holds a dominant position in the carrageenan market, accounting for 38.5% of the regional share. This leadership is mainly supported by the region’s strong seaweed production base and fast-growing processed food industry. According to FAO’s State of World Fisheries and Aquaculture 2024, global aquaculture algae production reached 36.5 million tonnes in 2022, more than tripling since 2000. Asia accounted for more than 97% of total global seaweed output, making it the main supply hub for carrageenan raw materials.

Indonesia plays a major role in this supply chain, especially for carrageenan-producing seaweeds such as Eucheuma and Kappaphycus. The country produced around 10.8 million tonnes of seaweed in 2024, according to FAO open knowledge data. The Philippines and Indonesia are also recognized as leading suppliers of raw carrageenan feedstock, supported by the Philippine Department of Agriculture’s Seaweed Industry Roadmap 2022–2026.

Apart from raw material availability, Asia Pacific’s growing food, dairy, and pharmaceutical sectors continue to strengthen regional demand. Carrageenan is used in pharmaceutical applications as a binder and coating agent in drug formulations. In addition, the World Bank noted that developing East Asia and Pacific grew by 5.1% in 2023, which was higher than global economic growth. This economic strength supports higher industrial output, stronger food processing activity, and rising consumer spending.

Overall, Asia Pacific’s leadership in seaweed production, combined with its expanding processed food, dairy, and pharmaceutical industries, is expected to keep the region at the center of global carrageenan market growth through 2035.

Carrageenan Market Segmentation

Product Type Analysis

Kappa represents dominant Segment in the Market.

In 2025, the kappa carrageenan segment dominated the market, accounting for 48.6%. Its leadership is primarily driven by its superior gelling properties, which enable the formation of strong, stable, and high-strength gels at lower concentrations compared to iota and lambda carrageenan. This functionality makes kappa carrageenan highly suitable for a wide range of food applications, particularly in processed meat and dairy products.

- According to the Food and Agriculture Organization (FAO), global meat production reached approximately 373 million tonnes and milk production totaled around 979 million tonnes in 2024. Kappa carrageenan plays a critical role in these sectors by improving texture, stabilizing emulsions, reducing water separation, and maintaining product consistency.

- In addition, its broad regulatory approval, including recognition under EU food additive code E407 and safety validation by the FAO/WHO Joint Expert Committee on Food Additives (JECFA), has strengthened its adoption across international markets. These advantages continue to position kappa carrageenan as the leading product type in the global carrageenan industry.

Processing Technology Analysis

Semi-Refined Technology Leads Processing Market.

In 2025, the semi-refined processing technology category dominated the market, accounting for 46.8%. Its leadership is mainly driven by lower production costs and high processing efficiency. According to the FAO, global seaweed production reached 36.3 million tonnes in 2021, rising significantly from 11.8 million tonnes in 2001. A large share of this production comes from Kappaphycus alvarezii, the key raw material used in SRC manufacturing, which is widely cultivated in Indonesia and the Philippines. Unlike refined carrageenan production, semi-refined processing uses a simpler alkaline treatment method and avoids costly solvent recovery and energy-intensive filtration stages.

FAO data also shows that carrageenan represented 47.8% of global seaweed trade in 2023, highlighting its strong commercial importance. As demand continues to rise from large food manufacturers, the combination of affordability, scalability, and efficient processing has strengthened the position of semi-refined carrageenan technology as the preferred choice across industrial-scale applications.

Function Analysis

Carrageenan Are the Most Widely Used for Stabilizer.

In 2025, the stabilizer category dominated the market, accounting for 41.7%. Its dominance is strongly linked to growing demand from the dairy and meat industries, where carrageenan plays a critical role in maintaining product texture, consistency, and shelf life. According to FAOSTAT, global milk production reached 985 million tonnes in 2024, while meat production rose to 374 million tonnes, reflecting strong consumption and processing activity worldwide.

The International Dairy Federation (IDF) reported that global per capita dairy consumption reached 119.1 kg in 2023, while Asia accounted for 36% of global bovine milk production, further supporting large-scale demand for stabilizer-grade carrageenan. In addition, carrageenan (E407) is approved for use in food applications under international and U.S. food regulations, including the Codex Alimentarius GSFA and 21 CFR §172.620. Its unique combination of protein compatibility, cold-water functionality, and stability across different food formulations continues to make it one of the most widely used stabilizers in dairy, meat, and confectionery products.

Form Analysis

Powder form Held a Major Share of the Carrageenan Market.

In 2025, the powder category dominated the market, accounting for 58.9%. The strong market share of powdered carrageenan is supported by its ease of storage, long shelf life, and suitability for large-scale industrial applications. Carrageenan is naturally produced in powder form through the processing of red seaweed species such as Kappaphycus and Eucheuma, which are harvested, alkali-treated, dried, and milled into standardized particle sizes.

- According to the FAO, global seaweed production reached 37.8 million tonnes in 2022. Carrageenan also represented 47.8% of global seaweed trade value in 2023, with most international trade conducted in dry powder form under HS Code 130239. Powdered carrageenan offers precise dosing and easy blending in dairy, meat, bakery, and processed food products, making it highly preferred by manufacturers. Its lower transportation and storage costs compared to liquid alternatives further strengthen its commercial appeal.

The importance of stable and easy-to-handle ingredients has increased as global food trade reached USD 1.7 trillion in 2021, while processed food exports accounted for 15.5% of total global exports by 2020. In addition, international standards from JECFA and Codex Alimentarius (E407) recognize carrageenan in dry powder form, supporting its widespread adoption across global food manufacturing industries.

Application Analysis

Carrageenan Are Mostly Utilized in the Food & Beverage Sector.

In 2025, the food and beverage segment dominated the market, accounting for 69.4%. The segment’s leadership is driven by the widespread use of carrageenan as a thickener, stabilizer, and gelling agent in processed foods and beverages. Carrageenan (INS 407) is recognized by the FAO/WHO Joint Expert Committee on Food Additives (JECFA) with an acceptable daily intake (ADI) of “not specified,” reflecting its broad regulatory acceptance in food applications. Its importance is particularly evident in the dairy industry, where the International Dairy Federation (IDF) reported global milk production of 782 million tonnes in 2023.

- According to the FAO, global meat production reached 371 million tonnes in 2023, with carrageenan widely used in processed meat products to enhance water retention, texture, and product stability. In addition, the FAO estimated the global food import bill at USD 2.22 trillion in 2025, highlighting the vast scale of food manufacturing worldwide. This strong demand across dairy, meat, and processed food sectors continues to support the dominant position of the food and beverage segment in the carrageenan market.

Key Market Segments

-

By Product Type

- Kappa

- Iota

- Lambda

-

By Processing Technology

- Alcohol Precipitation

- Gel Press

- Semi-refined

-

By Function

- Thickening Agent

- Gelling Agent

- Stabilizer

- Others

-

By Form

- Powder

- Flakes

- Liquid

- Gel

-

By Application

- Food & Beverage

- Pharmaceutical

- Personal Care & Cosmetics

- Others

Drivers

Plant-based dairy and hybrid food texturization demand

Carrageenan demand is increasing due to its ability to improve viscosity, suspension, stability, and mouthfeel in plant-based beverages, dairy alternatives, desserts, and hybrid meat products. Even at low inclusion levels, carrageenan helps stabilize complex protein-water-fat systems, making it a cost-effective ingredient for food manufacturers. Europe’s plant-based food market reached €5.8 billion in 2022, while plant-based milk and drink sales in Europe were valued at €2.2 billion in 2024. Globally, plant-based milk sales reached approximately USD 27.31 billion in 2025. As a result, carrageenan suppliers are increasingly focusing on application-specific texture solutions tailored to oat, almond, pea, and blended protein formulations.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plant-based dairy and hybrid food texturization demand | 1.40% | Europe core, North America core, urban APAC | Medium term (2-4 years) |

| Processed food reformulation toward multifunctional seaweed hydrocolloids | 1.10% | EU, North America, Latin America spill-over, Gulf food import hubs | Short term (≤ 2 years) |

| Southeast Asian raw-seaweed scale supporting cost-competitive carrageenan output | 0.90% | Indonesia, Philippines, China processing base, EU import markets | Medium term (2-4 years) |

| Regulatory continuity in major food markets preserving usage optionality | 0.70% | U.S. core, EU core, export-oriented APAC suppliers | Short term (≤ 2 years) |

| European product-launch intensity in dairy, desserts, meat alternatives and private label | 0.80% | Germany, Spain, France, Netherlands, Denmark, Poland | Medium term (2-4 years) |

| Traceability and sustainability requirements favoring integrated suppliers | 0.60% | EU, UK-adjacent supply chains, premium North America, Chile and ASEAN export chains | Long term (≥ 4 years) |

Restraints

Raw seaweed supply volatility

The main challenge facing the carrageenan market is the volatility of seaweed raw material supply, as carrageenan production depends heavily on seaweed sourced from Southeast Asia, particularly Indonesia and China.

- According to FAO data, global seaweed exports declined by 4.4% year-over-year during January–September 2025, while export values increased by 9.4% and average prices rose from USD 3.92/kg to USD 4.48/kg. This increase in feedstock costs is putting pressure on carrageenan processors, reducing profit margins and limiting long-term pricing commitments. A 10%–15% rise in seaweed costs can significantly impact profitability, potentially slowing market growth and delaying capacity expansion plans.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw seaweed supply volatility | -1.40% | APAC source base, EU, North America | Short term (≤ 2 years) |

| Regulatory use restrictions | -0.90% | EU core, UK, premium export markets | Medium term (2-4 years) |

| Yield loss from climate stress | -1.10% | Philippines, Indonesia, APAC corridors | Medium term (2-4 years) |

| Freight and energy cost inflation | -0.70% | EU importers, North America, global trade lanes | Short term (≤ 2 years) |

| Formulation substitution risk | -0.80% | North America, EU, developed Asia | Medium term (2-4 years) |

| Quality inconsistency in supply chain | -0.60% | Global, multi-origin sourcing markets | Medium term (2-4 years) |

Opportunity

Active packaging films

Carrageenan-based active and intelligent packaging is emerging as a promising growth opportunity beyond its traditional use as a food stabilizer and thickener. The opportunity gained momentum after the European Union’s Packaging and Packaging Waste Regulation came into force in February 2025, encouraging the adoption of recyclable, compostable, and sustainable packaging solutions from 2026 onward.

Research shows that carrageenan films can provide antimicrobial, antioxidant, oxygen-scavenging, and spoilage-indicator properties, creating higher-value applications in food packaging. If just 2%–3% of current carrageenan production shifts to packaging uses, suppliers could achieve 1.5x–2.5x higher revenue per kilogram, supporting stronger market growth in Europe, Japan, and South Korea.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Pharma-grade delivery systems | 1.20% | EU, North America, developed Asia | Medium term (2-4 years) |

| Active packaging films | 1.00% | EU core, Japan, South Korea | Medium term (2-4 years) |

| Wet pet food premiumization | 0.90% | North America core, EU, Japan | Short term (≤ 2 years) |

| Value-added origin integration | 1.40% | Indonesia, Philippines, China export chains | Medium term (2-4 years) |

| Reformulation-as-a-service | 0.80% | EU, North America, ANZ | Short term (≤ 2 years) |

| Hybrid hydrocolloid M&A platforms | 0.70% | EU, Latin America, APAC processing hubs | Long term (≥ 4 years) |

Challenge

Feedstock quality variability

Feedstock quality variability remains a key challenge for the carrageenan industry because product performance depends heavily on seaweed species, maturity, moisture levels, contamination, and drying quality. According to industry observations, consistent access to high-quality seaweed remains limited across major producing regions.

FAO data show that global seaweed export values increased by 9.4% during January–September 2025, while average export prices rose from USD 3.92/kg to USD 4.48/kg, despite lower trade volumes. This indicates rising raw material costs without corresponding improvements in quality consistency. As a result, processors face fluctuating extraction yields, additional blending requirements, higher quality-control expenses, and increased inventory costs, which can slow overall market growth and profitability.

Challenges Impact Analysis

| Challenge | (~) % Potential CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Feedstock quality variability | -1.10% | Indonesia, Philippines, EU importers | Medium term (2-4 years) |

| Processing cost pass-through gaps | -0.80% | EU, North America, APAC export hubs | Short term (≤ 2 years) |

| Multi-market compliance complexity | -0.70% | EU regulatory hubs, North America, Japan | Medium term (2-4 years) |

| Application reformulation burden | -0.90% | North America core, EU, developed Asia | Medium term (2-4 years) |

| Supplier concentration exposure | -1.00% | Global, APAC logistics corridors | Long term (≥ 4 years) |

| Scale-up capability mismatch | -0.60% | Southeast Asia processing clusters, China | Medium term (2-4 years) |

Geopolitical Impact Analysis

The carrageenan industry is facing significant supply chain challenges due to ongoing global trade disruptions. According to UNCTAD, trade volume through the Suez Canal declined by 42% in early 2024, while the IMF reported a 50% year-on-year drop in canal trade flows during the first two months of the year. Since most commercial carrageenan is produced from red seaweed cultivated in the Philippines and Indonesia, disruptions along major shipping routes have directly affected global supply. Rerouting vessels around the Cape of Good Hope has extended Asia–Europe transit times by 10–20 days, representing a 30–50% increase over normal voyage durations.

Freight costs on key routes rose nearly five times at peak disruption, while fuel surcharges increased by 15–25% per container. These higher logistics costs have raised the landed price of semi-refined carrageenan (SRC) for food manufacturers, particularly in Europe. As of April 2026, Suez Canal traffic remains 70–90% below historical levels, continuing to pressure supply chains and processing margins. This is particularly important for the dairy sector, where the International Dairy Federation (IDF) reported global milk production of 782 million tonnes in 2023, creating strong demand for stabilizers such as carrageenan.

Additional pressure has come from the escalation of U.S.–China trade tensions in 2025. China introduced retaliatory tariffs of 10–15% on a range of U.S. agricultural and food products in March 2025, creating uncertainty across food ingredient supply chains. China remains a major buyer of Indonesian seaweed, with its share of Indonesia’s seaweed exports increasing from approximately 85% in 2024 to 88% in 2025. UNCTAD also reported that global seaweed exports reached USD 3.9 billion in 2022, with Indonesia and the Philippines serving as leading suppliers of seaweed and carrageenan products.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Carrageenan Market.

In 2025, the Asia-Pacific region dominated the worldwide carrageenan market with a 38.5% share. This geographical domination is fueled by complete control over raw material marine resources, a highly concentrated low-cost seaweed farming infrastructure, and fast developing domestic processed food production facilities. The region is both a primary production powerhouse and a major consumption hub for texturizing hydrocolloids.

According to World Population Review data, Asia-Pacific accounts for more than 60% of the world’s current human population, providing a vast consumer base for packaged convenience foods, beverages, and personal care items. The region’s dominant position is further strengthened by generous government aquaculture subsidies, lax coastal zoning rules, and a large pool of competitive labor that maintains raw material harvesting prices much lower than Western benchmarks.

Furthermore, rapid urbanization in major emerging markets such as China, India, and Vietnam has expedited the industrial adoption of automated, high-throughput food manufacturing systems. These large-volume processing lines necessitate massive, consistent volumes of locally sourced carrageenan to stabilize regional dairy formulas, canned pet food systems, and processed chicken products without incurring exorbitant international transportation costs.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global carrageenan market has a moderately consolidated to oligopolistic competitive structure, with a small group of multinational hydrocolloid manufacturers controlling a significant percentage of the premium refined and semi-refined supply chains. Tier-1, vertically integrated businesses dominate the sector, most notably Cargill, CP Kelco, Ingredion, IFF (DuPont’s hydrocolloid operations), and Gelymar, who maintain a strong market position in high-value food and pharmaceutical categories. These leading companies use advanced multi-stage refining capabilities, stringent regulatory compliance frameworks, and extensive application knowledge to obtain long-term supply deals with international food, beverage, and personal care brands.

This oligopolistic dynamic is further bolstered by substantial entry obstacles, such as expensive capital needs for specialized extraction technology, purifying infrastructure, and global food safety certifications. Furthermore, upstream raw material availability is extremely concentrated; FAO FishStatJ data show that Southeast Asia, notably Indonesia and the Philippines, accounts for roughly 98% of worldwide seaweed volume (Kappaphycus and Eucheuma species). Established industry leaders maintain an unassailable competitive edge by locating localized processing factories near key aquaculture hubs, lowering international logistics costs, and stabilizing feedstock pipelines against raw material fluctuations.

The Major players in the industry

- DuPont

- Ingredion Incorporated

- Ashland

- CP Kelco U.S., Inc.

- Cargill, Inc.

- Ceamsa

- W Hydrocolloids, Inc.

- Gelymar

- Caldic B.V.

- Ina Food Industry Co. Ltd.

- Gumindo Perkasa Industri

- ACCEL Carrageenan Corporation

- BLG

- MCPI Corporation

- AEP Colloid

- Marcel Carrageenan

- TBK Manufacturing Corporation

- Shemberg Ingredients and Gums Corporation

- Prinova Group LLC

- LAUTA Ltd.

- Aquarev Industries

- Bang &Bonsomer

- AgargelIndustria e ComercioLtda

- Zhenpai Hydrocolloids Co., Ltd.

- Tate & Lyle

- Other Key Players

Key Development

- November 2024: Tate & Lyle PLC completed the acquisition of CP Kelco from J.M. Huber Corporation for approximately USD 1.8 billion, with the transaction closing on 15 November 2024. Under the agreement, Huber retained an approximately 16% equity stake in the combined business and secured 2 board seats. The acquisition significantly strengthened Tate & Lyle’s hydrocolloid portfolio, adding carrageenan, pectin, xanthan gum, refined locust bean gum, and citrus fiber, while expanding its presence in food texture and stabilization solutions.

- October 2025: W Hydrocolloids Inc. introduced RICOGEL 84894, a specialized carrageenan-based gelling solution developed for plant-based abalone meat alternatives. The launch marked the company’s expansion into the growing alternative protein sector and broadened its application-focused carrageenan product portfolio.

- December 2025: W Hydrocolloids Inc. participated in the Food Ingredients Europe 2025 exhibition in Paris, France. The company showcased its expanded hydrocolloid ingredient range and targeted new supply partnerships with European food manufacturers seeking natural seaweed-derived stabilizers and gelling agents.

- January 2026: W Hydrocolloids Inc. launched RICOGEL 86420, a carrageenan-based stabilizer designed for all-purpose cream applications. Together with RICOGEL 84894, the new product reinforced the company’s innovation strategy across both traditional dairy products and rapidly growing plant-based food categories.

- May 2026: International Flavors & Fragrances (IFF) announced a definitive agreement to divest its Food Ingredients business to funds advised by CVC Capital Partners for approximately USD 4.3 billion. The business, which includes carrageenan, emulsifiers, and sweeteners, contributes about 30% of IFF’s annual sales. The transaction reflects an enterprise value-to-EBITDA multiple of approximately 10x, based on 2025 EBITDA of USD 430 million. IFF will retain a 10% minority stake valued at around USD 200 million, while expected net cash proceeds of approximately USD 3.8 billion will primarily support debt reduction and share repurchases. The transaction is expected to close by the end of Q2 2027, subject to regulatory approvals.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$1.0 Bn |

| Forecast Revenue (2035) | US$1.7 Bn |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Kappa, Iota, Lambda), By Processing Technology (Alcohol Precipitation, Gel Press, Semi-refined), By Function (Thickening Agent, Gelling Agent, Stabilizer, Others), By Form(Powder, Flakes, Liquid, Gel), By Application (Food & Beverage, Pharmaceutical, Personal Care & Cosmetics, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | DuPont, Ingredion Incorporated, Ashland, CP Kelco U.S. Inc. , Cargill, Inc. Ceamsa, W Hydrocolloids, Inc. Gelymar, Caldic B.V., Ina Food Industry Co. Ltd., PT. Gumindo Perkasa Industri, ACCEL Carrageenan Corporation, BLG, MCPI Corporation, AEP Colloid, Marcel Carrageenan, TBK Manufacturing Corporation, Shemberg Ingredients and Gums Corporation, Prinova Group LLC, LAUTA Ltd., Aquarev Industries, Bang &Bonsomer, AgargelIndustria e ComercioLtda, Zhenpai Hydrocolloids Co. Ltd., Tate & Lyle, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |